![Signals from Wall Street and Japan's Securities Industry to the Crypto Market [FP Weekly 25]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fuh58gemqes9azi.png&w=1920&q=75)

Table of Contents

- 1. Major News

- [Asia] Japan's Diet Advances Bill Reclassifying Crypto Assets as Financial Products

- [Institution] Digital Asset Raises $355M Led by a16z to Expand Canton Network

- Others

- 2. Data Spotlight

- Crypto Card Payment Dashboard (Link)

- Why Japan Is Betting Big on Tokenized Stocks (Link)

- 3. Four Pillars Weekly

- : : Citrea Ecosystem and its Liquidity Coordination Asset, CTR (Link)

- : : Ethena Interview: What’s Next for USDe and ENA? (Link)

- : : MapleStory Universe & $NXPC: A Validated Future via Year 1 Data (Link)

- : : Time to Buy a Japanese Exchange (Link)

- Comment

- 4. Macro & Onchain Metrics

Researcher

1. Major News

[Asia] Japan's Diet Advances Bill Reclassifying Crypto Assets as Financial Products

What Happened?

On June 11, Japan's House of Representatives passed an amendment that reclassifies crypto assets as financial products under the Financial Instruments and Exchange Act (FIEA). The bill went through a Cabinet decision on April 10 and was submitted to the Diet, and it has now cleared the lower house and moved to deliberation in the House of Councillors. It must pass the House of Councillors to become law, and the promulgation and effective dates are not yet confirmed.

The significance of this amendment is that the governing law for crypto assets itself changes. Since 2017, Japan has placed crypto assets under the Payment Services Act (PSA), managing them mainly through rules for businesses handling payment instruments. The amendment moves them to the Financial Instruments and Exchange Act, which governs stocks and bonds. Behind this is the judgment that the actual use of crypto assets has shifted from payments to investment. Japan now has more than 14M crypto accounts, and about 70% of these belong to people earning less than 7M yen (about $43,600) a year. The Financial Services Agency (FSA) said that moving a market that has grown around retail into a regulatory framework matching the asset's investment character is the rationale for this amendment.

That said, the bill does not treat crypto assets exactly the same as securities such as stocks and bonds. It places them in a separate category under the Financial Instruments and Exchange Act and layers capital-market-style rules on top. As a result, disclosure obligations for issuers, a ban on insider trading using non-public information, and market manipulation rules are newly added. The insider trading rule was a gap that did not exist under the Payment Services Act framework, and this amendment makes it a direct subject of regulation for the first time. Penalties for unregistered operators are also strengthened, and a path is created for investors to void transactions with unregistered operators and claim refunds.

At the same time, this amendment opens a regulatory path for crypto ETFs, raising the possibility of crypto ETFs launching in Japan around 2027. Taxation moves on a separate track as well. The capital gains tax on crypto assets, currently levied as miscellaneous income at up to 55%, is set to drop to a flat 20% separate taxation, the same as stocks. The FIEA rules target 2027 for implementation, and the separate taxation targets 2028.

Researcher's Comment

In Japan, crypto assets have been treated effectively as payment instruments under the Payment Services Act framework since 2017. Investor protection and anti-money laundering were the main concerns, while their character as investment assets was secondary.

This amendment is a regulatory shift that moves that position from payment instrument to investment product. Earlier, in the first quarter of 2026, the FSA carried out a reorganization that relocated crypto-asset supervision to the asset management supervision area. If that reorganization was a preceding step that moved the position of the supervisory framework at the administrative level, this legislation is the stage that puts the rules to apply to the newly placed area into actual law.

This shift is tied to Japan's national strategy. The Japanese government has pursued an "asset management nation" strategy aimed at moving household assets from deposits to investment and becoming an asset management hub, and the expansion of the new NISA (small-sum investment tax exemption) and the Tokyo Stock Exchange's push for listed companies to improve capital efficiency were part of it. Placing crypto assets within the FIEA framework amounts to bringing digital assets into the category of this strategy. The FSA's stating that the purpose of the reorganization is to realize the asset management nation also reads in this context.

The most direct change from this appears among the businesses that operate the market, especially exchanges. Until now, exchanges were businesses that held user assets and connected trades under the Payment Services Act. After the bill takes effect, they move closer to capital-market-style businesses that bear disclosure, unfair-trading response, and financial soundness obligations. Before crypto assets are treated as investment products, the operators of the market where those products trade are placed within capital-market rules first.

The change in exchange status is likely to raise market entry costs significantly. Obligations such as reserve requirements and capital adequacy ratios thicken investor protection, but they are a burden for small exchanges with weak regulatory capacity. Korea set high entry requirements such as information security certification and real-name account issuance from the start, so it effectively settled into a system of a few exchanges and became a market closer to consolidation than to new entry. Japan started with lighter payment-instrument rules and is now moving to capital-market-style rules, so the starting points are opposite but the destinations may end up similar.

Conversely, for securities firms, large financial groups, and operators that already hold multiple licenses, these are familiar rules. The fact that major securities firms such as Nomura and Daiwa reviewed entry into the crypto exchange business around the same time can also be read in this context. As crypto assets move toward rules closer to investment products than to payment instruments, the case for securities firms to enter grows, given their familiarity with product screening, customer suitability checks, internal controls, market surveillance, and risk management.

SBI's consolidation of its exchange business around SBI VC Trade is a move in the same direction. As rules rise to the capital-market level, the exchange business comes to depend less on simple trade intermediation and more on license management, listing screening, customer asset protection, AML/KYC response, and the ability to attract institutional clients. As a result, Japan's crypto exchange market is likely to be reshaped around operators with regulatory capacity and capital, beyond fee competition.

[Institution] Digital Asset Raises $355M Led by a16z to Expand Canton Network

What Happened?

On June 11, Digital Asset, which develops the Canton Network, raised $355M in a Series F round led by a16z crypto. a16z crypto put in $100M, and the round was oversubscribed against its initial $300M target, valuing the company at about $2B. Digital Asset said it plans to use the funds for expanding partnerships, M&A, and growing the Canton ecosystem.

This news drew attention for its investor composition as much as its size. Institutions spanning traditional finance and crypto participated broadly, including a subsidiary of the Abu Dhabi Investment Authority, Apollo Funds, BNP Paribas, HSBC, Citadel Securities, CME Ventures, Coinbase Ventures, S&P Global, Tradeweb, Optiver, Broadridge, and Polychain. Korea's Hanwha Investment & Securities and Japan's SBI Group also joined. CEO Yuval Rooz said that many investors received equity rather than tokens, and that a significant number are also prospective users of Canton.

The Canton Network is a blockchain with configurable privacy designed so that regulated financial institutions can tokenize and settle real-world assets (RWAs) such as bonds, loans, equities, and commodities. Its feature is issuing and settling assets on a shared ledger without exposing sensitive commercial information such as the transacting parties and amounts. Goldman Sachs, BNY Mellon, BNP Paribas, and Standard Chartered are already participating in pilots, and Visa joined as a Canton Super Validator in March and added Canton to its stablecoin settlement pilot.

Researcher's Comment

This round once again clearly shows the way the crypto market is institutionalizing, through its investor list and their character. Many of the banks, exchanges, market makers, and asset managers received equity rather than tokens, and a significant number are prospective users of Canton. This is a signal that Canton is positioning itself not as an object of token speculation but as infrastructure these players intend to actually use in operations.

The purposes for which institutional finance uses blockchain split broadly into two. One is the demand to access the onchain liquidity already accumulated on public chains such as Ethereum. Tokenized Treasuries such as BUIDL and BENJI are incorporated as stablecoin reserves or DeFi collateral, a path through which asset managers use public chains as a buy-side channel. The other is the demand to make existing workflows such as repo, collateral management, and settlement more efficient.

Canton's market fit lies in the latter. Canton recognized early that institutional finance agrees on efficiency through blockchain but finds it hard to accept a model where all transaction information is public. It addressed this through selective disclosure, permission-based access, and inter-institutional synchronization, and found its market fit there. Canton's existing results also show demand concentrated in this area. Broadridge's DLR processes about $339B in repo transactions per day, moving roughly 3% of the U.S. repo market onchain, and JPMorgan natively issued its deposit token JPMD on Canton for the purpose of making transfers and settlement among institutional clients more efficient.

At the same time, this round shows that the axis of blockchain competition is shifting. For a while, blockchain competition was about TPS, low fees, and ecosystem app expansion, and later chains with clear product demand such as Hyperliquid received higher valuations. Then, as the institutional market opened, whether a chain can provide privacy, permission structures, and atomic settlement became a new competitive category.

Within this institutional blockchain category as well, Canton targets capital-market settlement, Tempo targets payments, and Arc targets stablecoin infrastructure, each aiming at a different area while all drawing capital at high valuations. This means institutional chains are diverging by layer rather than converging into one. The participation of Hanwha Investment & Securities and SBI suggests this divergence is also spreading to the interest of Asian financial institutions.

Others

Crypto

- Venice and others draw attention as the permissionless AI narrative gains traction after Claude Fable 5 is blocked

- Circle launches cirBTC to compete in the Ethereum-based wrapped bitcoin market

- Botanix to shut down its Bitcoin L2 network amid weak user demand

- Aerodrome to introduce prediction-market-style incentives for liquidity allocation

- Humanity Protocol hit by over $32 million exploit due to multisig wallet management issue

Institution

- CFTC proposes rule for reviewing prediction-market contracts

- New York's NYDFS proposes amended stablecoin rule aligned with the GENIUS Act

- UK's FCA moves to allow mutual funds up to 10% exposure to crypto ETNs

- Coinbase, Ripple, and over 200 crypto organizations urge the Senate to vote on the CLARITY Act

- US community bank group launches ad campaign opposing the CLARITY Act's stablecoin reward provision

Tech

- Coinbase launches 'Coinbase for Agents' for trading by AI agents

- MetaMask launches Agent Wallet, giving AI bots self-custody access to Ethereum

- Ripple launches a toolkit for AI agent payments on XRPL

- Ethereum presents an outlook of transitioning into a fully ZK-based protocol within 3 to 5 years

Investment

- Ethena lands Janus Henderson backing and pursues USDe distribution cooperation

- Morpho raises $175 million co-led by Paradigm and a16z crypto

- Figure acquires Kiavi for $717 million to expand its RWA tokenization network

Asia

- Japan's three megabanks move to jointly issue a stablecoin by March 2027

- Singapore's DBS to offer tokenized gold to retail customers

- Philippine central bank says Binance and its local partner lack licenses to operate

- South Korea's Ministry of Economy and Finance says tokenized stocks are classified as securities, not crypto assets

- LG Electronics moves to build a new blockchain based on Arbitrum

2. Data Spotlight

Crypto Card Payment Dashboard (Link)

Why Japan Is Betting Big on Tokenized Stocks (Link)

3. Four Pillars Weekly

: : Citrea Ecosystem and its Liquidity Coordination Asset, CTR (Link)

- Citrea reversed the usual sequence of issuing a token first and then waiting for an economy to follow. From the mainnet launch in January 2026 to the TGE in May, lending, trading, yield products, and prediction markets were already running on top of two assets, cBTC and ctUSD. CTR arrived to hand the community the wheel of an economy that was already in motion.

- CTR positions itself not as an ordinary governance token that merely sets a protocol's operating policy, but as a coordination asset that decides where capital flows, that is, one that selects the standard routes Bitcoin capital will travel again and again. The non-transferable xCTR that holders receive by staking CTR directs liquidity incentives through a vote-escrow model, gauges, and a dual treasury. Notably, the same structure recurs at the level of individual applications such as Satsuma, and the design of the coordination asset is becoming the shared grammar of this economy.

: : Ethena Interview: What’s Next for USDe and ENA? (Link)

- Ethena does not think USDe should be understood only through APY. If USDe works, the more important metrics become collateral usage, velocity, utility, and how deeply it is integrated across DeFi and CeFi.

- Backing diversification is not meant to turn USDe into a higher-risk rewarding product. Ethena’s stated goal is to broaden rewarding sources while preserving USDe’s behavior as a predictable synthetic dollar.

- The team sees capacity as a market-structure problem, not an AUM target. USDe becomes capacity-constrained when Ethena’s hedging flow starts moving funding rates, increasing execution costs, or concentrating risk in specific venues and assets.

- Distribution will increasingly happen through exchanges, wallets, protocols, and partner products. Ethena may become the underlying rewards engine for other platforms, but the team is also building products that preserve a direct customer relationship.

- The next collateral ceiling depends on trust under stress. For USDe to become core dollar collateral, institutions need confidence in redemption integrity, peg stability, liquidity, and a risk structure that remains simple enough to underwrite.

: : MapleStory Universe & $NXPC: A Validated Future via Year 1 Data (Link)

- MapleStory Universe (MSU) departs from the conventional Web3 game playbook of issuing tokens first and waiting for users and the economic ecosystem to follow. By integrating ownership and economic systems onto the 23-year-proven MapleStory IP and its robust gameplay loop, it has successfully shifted the demand for $NXPC from mere speculation to actual consumption-driven gameplay.

- The primary source of future supply pressure for $NXPC stems from ecosystem contribution rewards, which account for 97.4% of the upcoming circulating supply. However, this is counterbalanced by a tightly interwoven sink structure designed to effectively absorb market supply. This includes in-game expenditures (character growth, equipment enhancement, and marketplace transactions), NFT lock-ins via Fusion and Fission, and a quarterly revenue-linked burn model.

- The published first-year performance data proves that this structure is more than just a theoretical hypothesis. MSU recorded approximately $31 million in ecosystem revenue, with 90.5% generated directly from core game business models (BM). Notably, in Q1 2026, user token consumption surpassed the volume of reward distribution for the first time, validating the tokenomics' sustainability.

- Furthermore, MSU 2.0 and Vibe IP represent an ambitious step to expand the utility of $NXPC from a mere in-game currency to the foundational settlement unit of a Nexon IP-based creator economy. As creators leverage AI-based production tools and game data, and as licensing and settlements are seamlessly processed on the Henesys chain, it establishes a virtuous cycle where the user pool, revenue pool, and token burn volume scale together.

: : Time to Buy a Japanese Exchange (Link)

- Japan has one of the world's deepest licensed exchange rosters, 30 registered CAESPs, yet the FSA itself acknowledges that roughly 90% of them operate at a loss under current compliance costs.

- The 2026 FIEA package adds disclosure handling, annual cybersecurity self-assessments, liability reserves of ¥2B-¥40B, and insider-trading surveillance on top of an already heavy cost stack, making sub-scale independence structurally unviable.

- Demand is about to inflect: the 20% flat tax from 2027, the 105-token FIEA whitelist, targeted 2028 spot ETF approvals, and institutional allocation intent (80% of Japanese institutions plan 2-5% of AUM in crypto within three years) all route through licensed venues.

- A license is no longer just a trading venue: embedded-finance "CaaS" distribution, gateway status for foreign stablecoins like USDC, and crypto card programs with rising usage each stack B2B and payments revenue on top of trading fees.

Comment

- 0.8¢ to 100¢: How Vote-Counting Order Created a Polymarket Inefficiency

- The 1,550 BTC Buy: Saylor's Worst Trade Ever

- Morpho Midnight: DeFi’s Boring but Necessary Future

- Can Hyperliquid’s Weekend Trading Predict Monday Opens for Korean Stocks?

- If Prediction Markets Are Gambling, What Does That Mean for Tokenization?

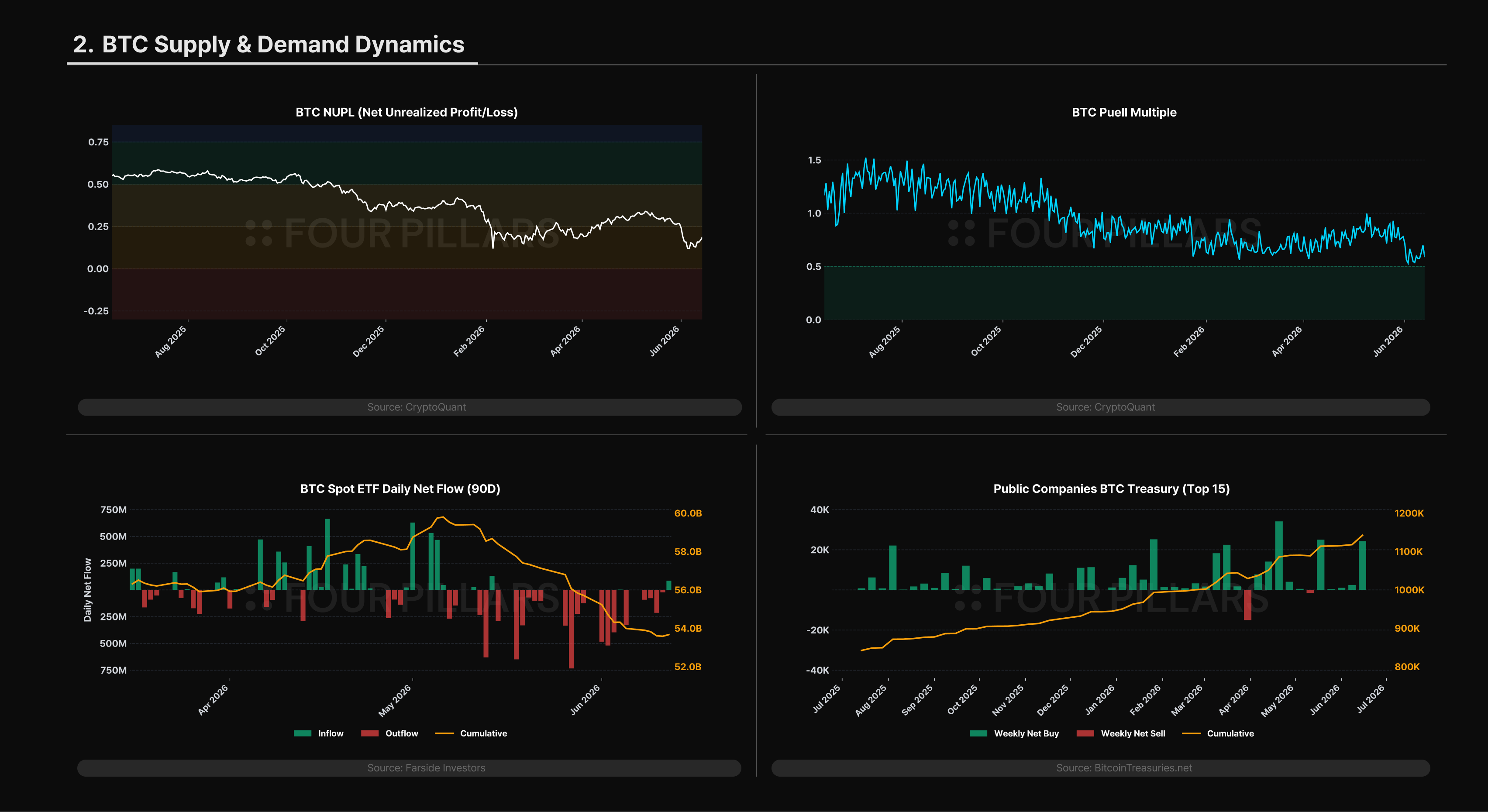

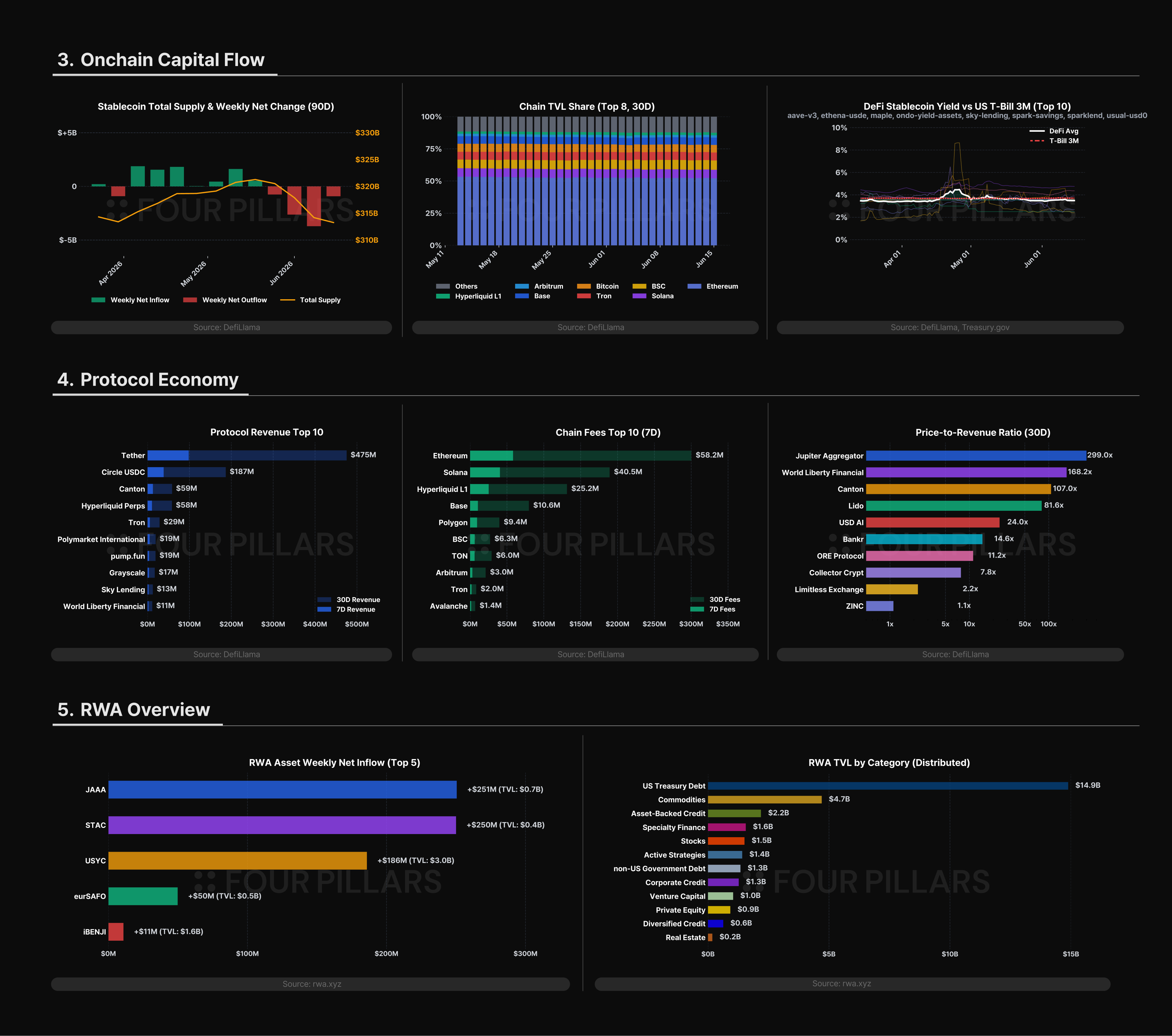

4. Macro & Onchain Metrics

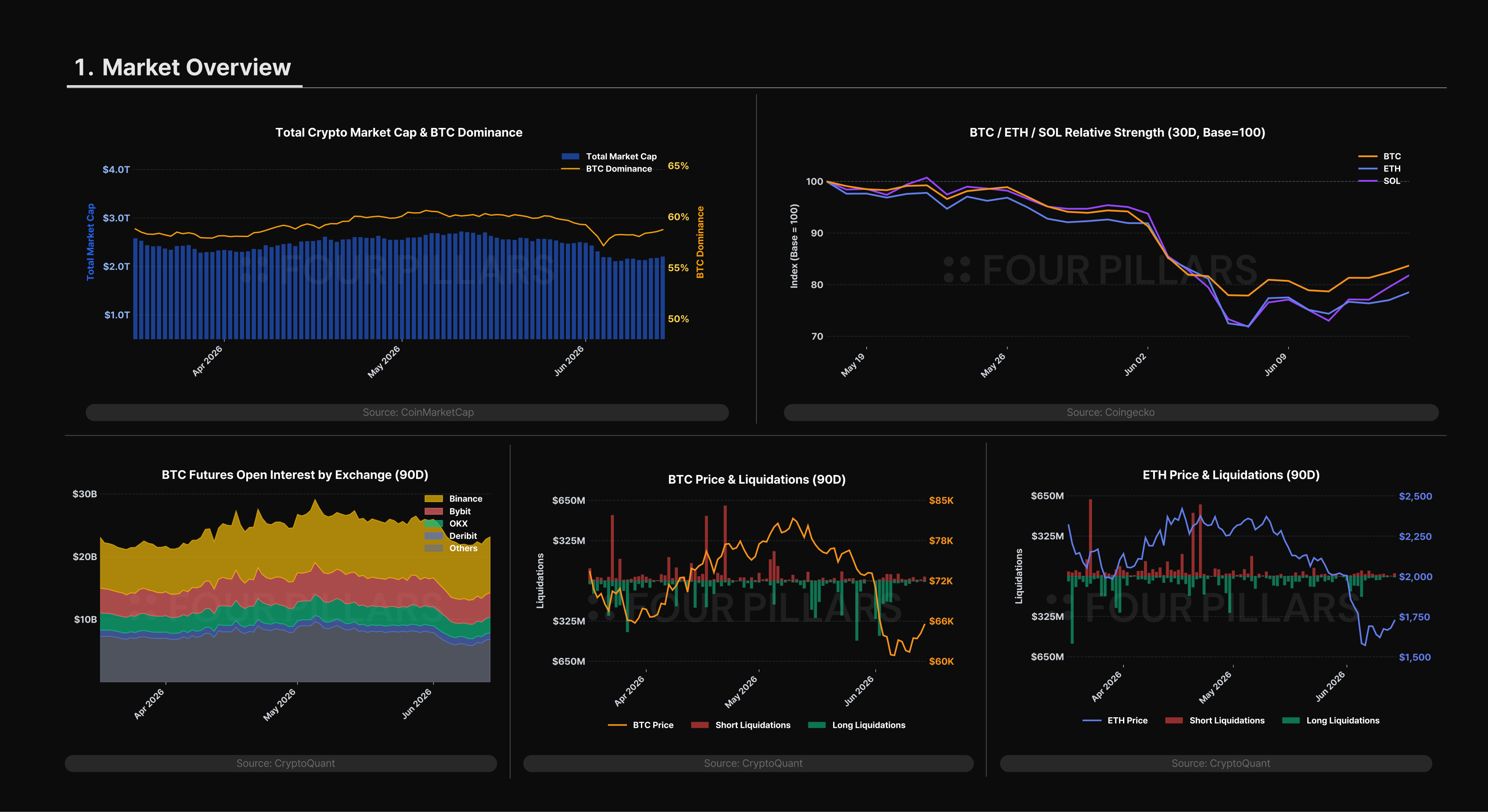

Some of the charts below are powered by CryptoQuant. For those interested in exploring the underlying data in greater detail, CryptoQuant provides access to a comprehensive suite of onchain and market analytics used by institutional participants.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![Onchain Vaults Head to the Regulator's Desk [FP Weekly 31]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fewmxa9ms2zo6jb.png&w=1920&q=75)

![Journey Toward Tokenized Stocks [FP Weekly 30]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fvlq144mrur6b4t.png&w=1920&q=75)