Table of Contents

- Key Takeaways

- 1. The Paradox: The Most Licensed Market, the Least Profitable Operators

- 2. The 2026 Reform Makes Small Exchanges Un-Investable as Standalones

- 3. Why the License Is Worth More Than the P&L Suggests

- 4. Beyond Trading: One License, Several Businesses

- 5. SBI Already Wrote the Playbook

- 6. What Could Go Wrong

- 7. The Bottom Line

Researcher

Key Takeaways

- Japan has one of the world's deepest licensed exchange rosters, 30 registered CAESPs, yet the FSA itself acknowledges that roughly 90% of them operate at a loss under current compliance costs.

- The 2026 FIEA package adds disclosure handling, annual cybersecurity self-assessments, liability reserves of ¥2B-¥40B, and insider-trading surveillance on top of an already heavy cost stack, making sub-scale independence structurally unviable.

- Demand is about to inflect: the 20% flat tax from 2027, the 105-token FIEA whitelist, targeted 2028 spot ETF approvals, and institutional allocation intent (80% of Japanese institutions plan 2-5% of AUM in crypto within three years) all route through licensed venues.

- A license is no longer just a trading venue: embedded-finance "CaaS" distribution, gateway status for foreign stablecoins like USDC, and crypto card programs with rising usage each stack B2B and payments revenue on top of trading fees.

1. The Paradox: The Most Licensed Market, the Least Profitable Operators

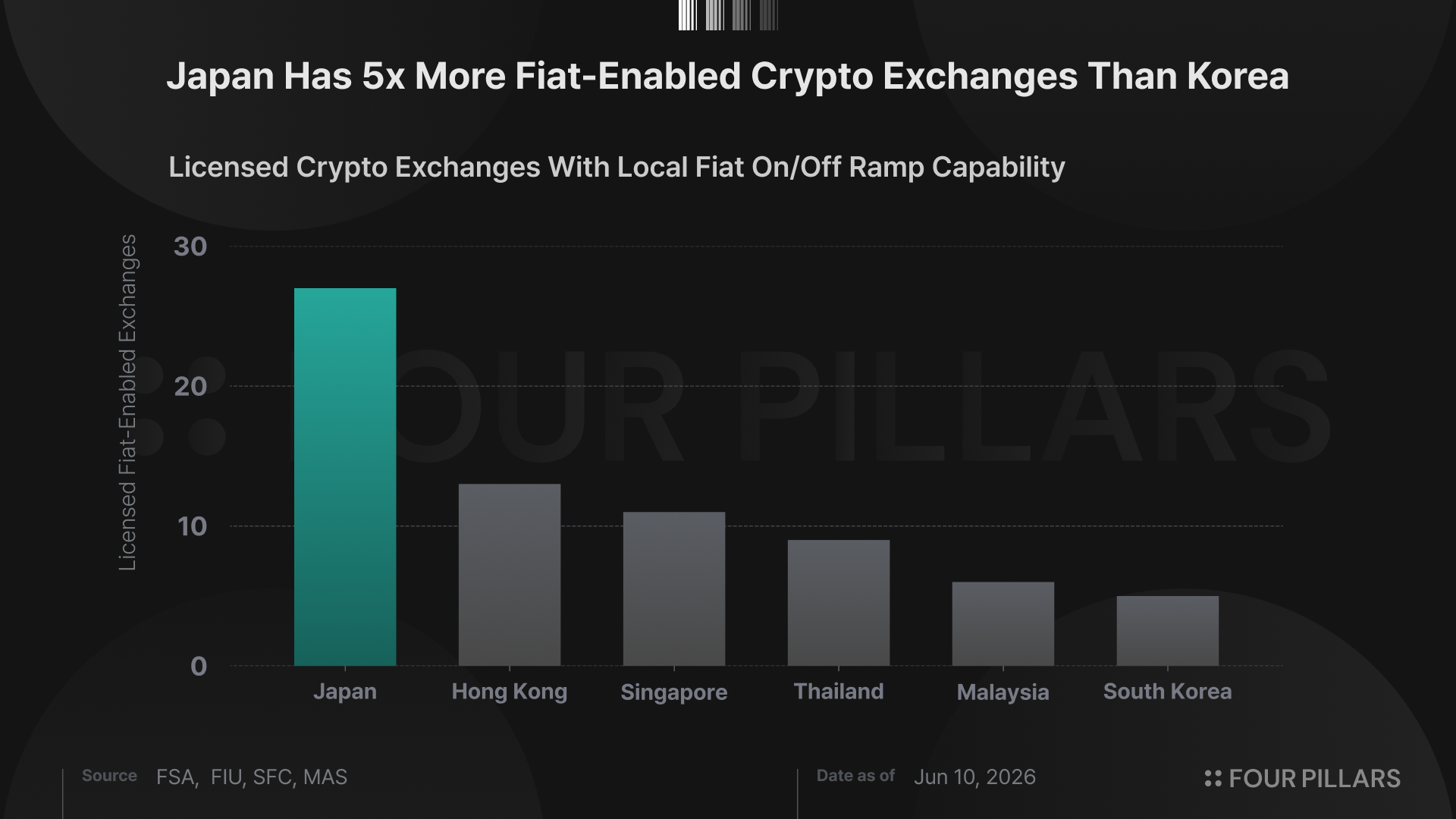

Japan's licensed exchange landscape is simultaneously one of the deepest in the world by registration count and one of the most challenged by operating economics. The FSA's registry lists around 30 Crypto-asset Exchange Service Providers (CAESPs), a count exceeding Hong Kong's, Singapore's, and Korea's licensed venues combined. Yet volume concentrates in a handful of platforms: bitFlyer, Coincheck, SBI VC Trade, and bitbank account for the dominant share of domestic spot trading.

The result is a long tail of venues holding the single most valuable asset in Japanese crypto, an FSA registration, while bleeding cash. The FSA has publicly noted that roughly 90% of Japanese crypto exchanges operate at a loss under current compliance costs. The cost stack runs through registration fees, AML/CFT compliance, JVCEA membership dues, cybersecurity infrastructure, and segregated custody, and against that base, only the highest-volume venues earn sustainable margins. This has been true since the 2017 PSA registration regime, and it is about to get worse before it gets better.

2. The 2026 Reform Makes Small Exchanges Un-Investable as Standalones

The April 2026 FIEA package layers four new cost drivers onto every licensed venue:

- Disclosure handling. Tokens on the 105-asset FIEA whitelist carry issuer-disclosure obligations that exchanges must operationally support.

- Cybersecurity Self-Assessment (CSSA). An annual, NIST-style assessment filed with the FSA, replacing the looser JVCEA-guideline regime, alongside mandates for 95% cold storage, penetration testing, and mandatory hack insurance.

- Liability reserves. Capital-style reserves of ¥2B-¥40B (~$13M-$255M) calibrated to user-asset balances, not revenue. This is the binding constraint: a small CAESP with a large but inactive user base faces the worst possible economics.

- Insider-trading surveillance. FIEA-grade transaction monitoring and STR filing to the SESC, an operationally non-trivial build comparable to FINRA-style market surveillance.

For the long tail of loss-making venues, the strategic options narrow to three: raise capital to fund a compliance build with no revenue offset, hand back the license, or sell. The first is unattractive, the second destroys the one asset of value, which leaves the third.

3. Why the License Is Worth More Than the P&L Suggests

The acquisition case rests on the gap between what these businesses earn today and what their regulatory position is worth tomorrow.

The demand side is inflecting. The 2027 shift of crypto gains from ~55% miscellaneous-income taxation to a 20% flat rate removes the single largest reason Japanese traders migrated offshore. Repatriated retail flow has to land somewhere, and it can only land on licensed venues trading the 105-token list. Japanese retail crypto holdings already hit a record ~¥5T in 2025 before the tax cut even took effect.

Institutions are coming through the same gate. Nomura's 2026 institutional survey found roughly 80% of Japanese institutional investors plan to allocate 2-5% of AUM to crypto within three years, with interest concentrated in staking, tokenized assets, lending, and derivatives, all activities that route through FIEA-supervised intermediaries. SBI VC Trade's FSA-supervised USDC lending product shows the margin profile available to licensed venues that can manufacture regulated yield.

The 2028 catalyst. The FSA has targeted spot crypto ETF approvals for 2028. ETF creation and redemption, custody, and market-making all require licensed counterparties, and NISA eligibility for those ETFs would expose big household savings wrapper to crypto for the first time. Exchanges positioned ahead of that flow will not trade at distressed multiples afterward.

4. Beyond Trading: One License, Several Businesses

The strongest part of the acquisition case is that a CAESP registration now monetizes well beyond spot trading fees. Three adjacent business lines have opened up in the last twelve months alone, and each one runs through the license.

Embedded crypto (CaaS). Coincheck launched "Coincheck CaaS" in June 2026, an API layer that embeds account opening and trading inside partner apps, with Mercari as the first deployment. Mercari's crypto service passed 4 million accounts in roughly three years, and about 90% of its users are first-time crypto buyers. Crucially, the FSA's new intermediary regime, effective June 1, 2026, lets unlicensed apps distribute crypto only by partnering with a registered exchange, which turns every CAESP into a potential backend for Japan's super-apps, retailers, and fintechs.

The gateway for foreign stablecoins. Overseas stablecoins can reach Japanese users only through registered electronic payment instruments handlers, and SBI VC Trade was the first to qualify, bringing USDC onshore in March 2025. Circle has already lined up Binance Japan, bitbank, and bitFlyer as follow-on USDC distributors, and Ripple plans to route RLUSD through the same SBI rails. For any foreign issuer, owning or partnering with a licensed venue is the entry ticket to the yen market, and an acquirer captures distribution economics on both sides.

Cards and payments. Binance Japan's June 2026 report on its BNB-reward card showed active users' monthly transaction frequency running above the industry average, evidence that crypto cards are crossing into daily use in Japan. The trend is global: crypto card spending hit an $18B annualized run rate in early 2026. Interchange and conversion spreads convert a large-but-dormant registered user base, the very thing that makes small CAESPs distressed under the reserve rules, into recurring payments revenue.

5. SBI Already Wrote the Playbook

In April 2026, SBI Holdings announced its acquisition of bitbank, which would make SBI Group Japan's largest crypto-exchange operator by combined volume and complete a full-stack strategy spanning stablecoin issuance (JPYSC), exchange (SBI VC Trade + bitbank), STO infrastructure (ODX), and L1 rails (Strium). The follow-on candidates are visible: Coincheck and GMO Coin are widely expected consolidation targets over 2026-2028, while DMM Bitcoin's post-hack scope reduction makes it a natural seller of operations.

The buyer universe is broader than domestic financial groups. Megabanks building stablecoin distribution, foreign exchanges seeking compliant Japan entry (the Binance Japan route, buying or building onto a licensed entity, remains the only credible path), and gaming or super-app platforms following Mercari's Mercoin model all have strategic reasons to own a registration rather than spend 18-24 months pursuing one from scratch.

6. What Could Go Wrong

The risks are real but quantifiable. Implementation slippage in FSA sub-rule drafting could push the tax and disclosure regime, and therefore the demand inflection, six months or more into 2027. Liability-reserve calibration could come in at the high end and raise the effective price of any acquisition. And the 105-token whitelist is conservative by design: a venue whose volume depends on long-tail listings inherits a narrower product shelf than offshore competitors.

Finally, integration is not free. The acquirer assumes legacy security liabilities in a market where DMM Bitcoin's ~$300-470M Lazarus-attributed loss is recent memory. That is precisely why diligence on custody architecture should dominate the process.

7. The Bottom Line

Markets rarely hand over regulated infrastructure at distressed prices right before a demand inflection. Japan in 2026 is doing exactly that: 90% of licensed exchanges lose money, the 2026-2027 compliance wave forces the long tail to sell, and the 20% tax cut, institutional allocation cycle, and 2028 ETF window guarantee that the surviving licenses carry far more flow than today's P&Ls reflect.

There is also a softer asset that never shows up on the balance sheet: localization. Japan is a market where regulator relationships, Japanese-language disclosure and customer support, and JVCEA process know-how cannot be imported, and building them from zero takes years. Buying an exchange is therefore an acqui-hire as much as a license purchase: the bilingual compliance officers, security engineers, and FSA-facing staff come with the deal, precisely the talent a foreign entrant cannot recruit quickly in Tokyo's thin crypto-compliance labor market.

As 90% of the exchanges are not profitable, The consolidation clock is running, and the cheapest entry into one of the world's most rigorously regulated crypto markets is to buy the license someone else can no longer afford to operate.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.