Table of Contents

- Key Takeaways

- 1. The Citrea Mainnet and the Launch of CTR

- 1.1 An Economy That Went Live Before the Token

- 1.2 CTR as a Coordination Asset and xCTR as Its Engine

- 1.3 Gauges and the Dual Treasury

- 2. The Capital Pathways CTR Coordinates

- 2.1 Exchange and Credit: Satsuma and Zentra

- 2.2 Vaults and Structured Products

- 2.3 Prediction Markets: Signals

- 2.4 Privacy: Crest

- 3. Closing Thoughts

Researcher

Related Projects

Key Takeaways

- Citrea reversed the usual sequence of issuing a token first and then waiting for an economy to follow. From the mainnet launch in January 2026 to the TGE in May, lending, trading, yield products, and prediction markets were already running on top of two assets, cBTC and ctUSD. CTR arrived to hand the community the wheel of an economy that was already in motion.

- CTR positions itself not as an ordinary governance token that merely sets a protocol's operating policy, but as a coordination asset that decides where capital flows, that is, one that selects the standard routes Bitcoin capital will travel again and again. The non-transferable xCTR that holders receive by staking CTR directs liquidity incentives through a vote-escrow model, gauges, and a dual treasury. Notably, the same structure recurs at the level of individual applications such as Satsuma, and the design of the coordination asset is becoming the shared grammar of this economy.

1. The Citrea Mainnet and the Launch of CTR

1.1 An Economy That Went Live Before the Token

In an earlier piece, I examined how Citrea built the rails to put Bitcoin to use without conceding trust. These were a zero-knowledge rollup that grounds data availability and settlement in Bitcoin, the Clementine bridge that operates on BitVM under a 1-of-N assumption, and ctUSD, a dollar issued within a regulatory framework.

Source: Citrea

The Citrea mainnet went live this January alongside applications spanning trading, lending, yield, and prediction, which it calls ₿apps, and its native token CTR was issued four months later in May. CTR was issued not as a token promising an economy yet to be built, but as one handing the community the wheel of an economy that was already running.

An ecosystem's economy does not run on its own simply because the routes for capital have been laid down. If the lending markets that set a benchmark rate for Bitcoin collateral and the yield-generating protocols that would serve as the default venue for deploying Bitcoin remain static and uncompetitive, then no matter how technically complete the infrastructure Citrea designs, Bitcoin will not become productive capital. In response, Citrea presents its native token CTR as a coordination asset that decides where capital on top of Bitcoin flows. This piece revisits the structure of CTR and xCTR, and then turns to the economy it aims to coordinate.

1.2 CTR as a Coordination Asset and xCTR as Its Engine

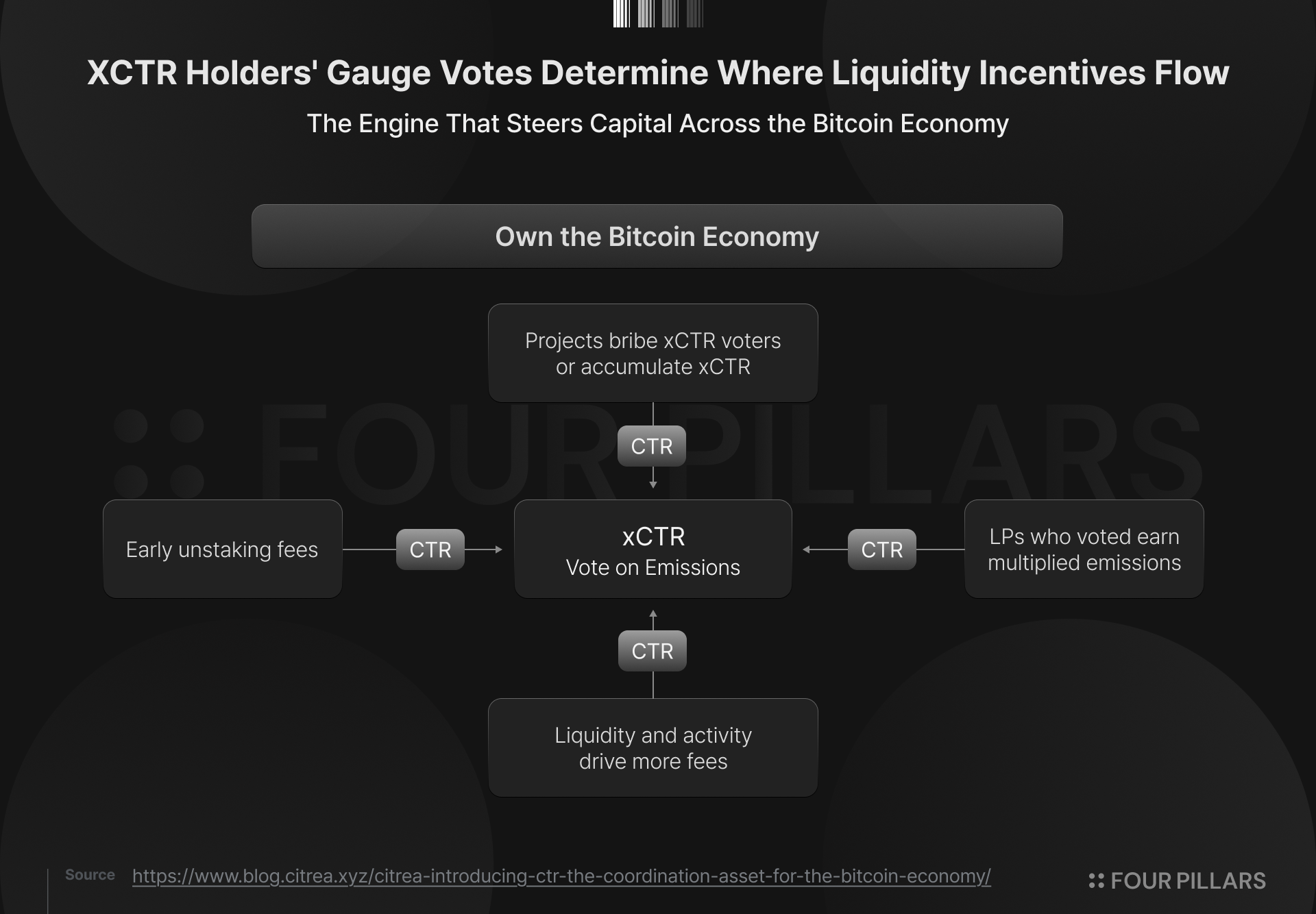

Citrea's token design centers on xCTR, a non-transferable token that holders receive by staking CTR. xCTR follows a modified vote-escrow model, in which a user's governance influence grows dynamically with their total xCTR balance. Beyond governance influence, xCTR also serves as the basis for receiving rewards. It exchanges for CTR at 1:1 at first, but as rewards flow in over time, that ratio rises past 1:1 and keeps climbing. In other words, the xCTR obtained with a given amount of CTR converts back into more CTR over time, and that difference is what the staker earns as a reward.

That said, simply staking CTR and holding xCTR yields only the base emissions and the automated unstaking-penalty rewards. For xCTR to earn the multiplied network rewards, the holder must actually take part in governance voting. Positions that stay staked without voting do not receive this substantial emission multiplier, which pushes holders to engage actively in the decision-making process. In this way, by tying capital to decision-making, Citrea has made it impossible to capture the full reward through token holding alone.

Unstaking carries a condition in a similar vein. Withdrawing CTR immediately incurs a penalty of about 50%, which decays to zero over roughly 90 days. Rather than being burned, this penalty is distributed pro rata to the remaining stakers, steering governance toward capital committed to the ecosystem rather than capital chasing short-term returns.

1.3 Gauges and the Dual Treasury

The governance influence gathered this way translates into actual capital allocation through an automated mechanism called the gauge. When xCTR holders vote for a particular liquidity pool, the liquidity incentives flowing out of the governance treasury are directed to that pool. In other words, token holders' votes decide where liquidity is laid more thickly. The gauge works as a self-adjusting mechanism in which the market sets the direction of incentives on its own. When liquidity crowds into a particular pool, that pool's incentives adjust naturally, and in the opposite case the market again finds a more efficient equilibrium.

Another mechanism supporting this is the dual treasury. On the governance side, Citrea has separated funds into two kinds: one is the governance treasury controlled by xCTR holders, the other is the foundation treasury managed by the Citrea Foundation. The governance treasury is used for market-facing activities such as liquidity incentives through gauges and the selection and compensation of committees and infrastructure providers. The foundation treasury is set apart for longer-horizon work such as research, grants, and operations, and it is explicitly restricted from being used for ongoing liquidity emissions. If the foundation wants to run a liquidity program, it must request approval from governance and present clear objectives and KPIs. In effect, control over short-term capital flows rests with token governance rather than a centralized entity. From the perspective of institutional capital, this separation means that the incentive flows affecting the liquidity they supply sit under the control of token governance rather than the foundation's discretion, which makes the sustainability of their capital commitment predictable in advance.

Once the gauge is running, it can give rise to a liquidity flywheel. When institutional liquidity, that is, cBTC and ctUSD, is supplied to lending markets, exchanges, and vaults, and gauge voting concentrates incentives where demand is forming, liquidity deepens, borrowing rates fall, and trade execution improves. The demand that grows from this raises fees, those fees lift the xCTR exchange ratio and flow back to stakers, and that in turn invites more staking and more voting toward productive pools. It is a structure in which capital supply, governance decisions, and the applications above them are aligned through a single asset. Through this structure, Citrea aims to leave capital allocation to a self-adjusting market mediated by the token, rather than to the decisions of a DAO or a foundation.

That said, in reading this flywheel, one should recognize that the rewards returning to xCTR holders split into two strands of different character.

One is the internal redistribution of CTR, which includes the emissions from the treasury, the 10 million CTR paid to early stakers over 90 days, and the penalties left behind by stakers who exit. These amount to CTR moving among holders within a fixed supply, so while they raise the exchange ratio, they cannot be seen as a flow that brings in cash from outside.

The other is the actual protocol fees generated in cBTC and ctUSD, that is, the revenue coming from trading, lending, and asset management. For the proposition that value created in the Bitcoin economy flows back to participants to hold fully, there must be a path by which the latter reaches xCTR through the governance treasury, but right now, just after issuance, that path is not yet fully in place. This is something to be established by the ecosystem projects discussed below, where trading fees are set to accrue to the liquidity providers of major decentralized exchanges (DEXs), and interest margins to lending protocols and their users.

2. The Capital Pathways CTR Coordinates

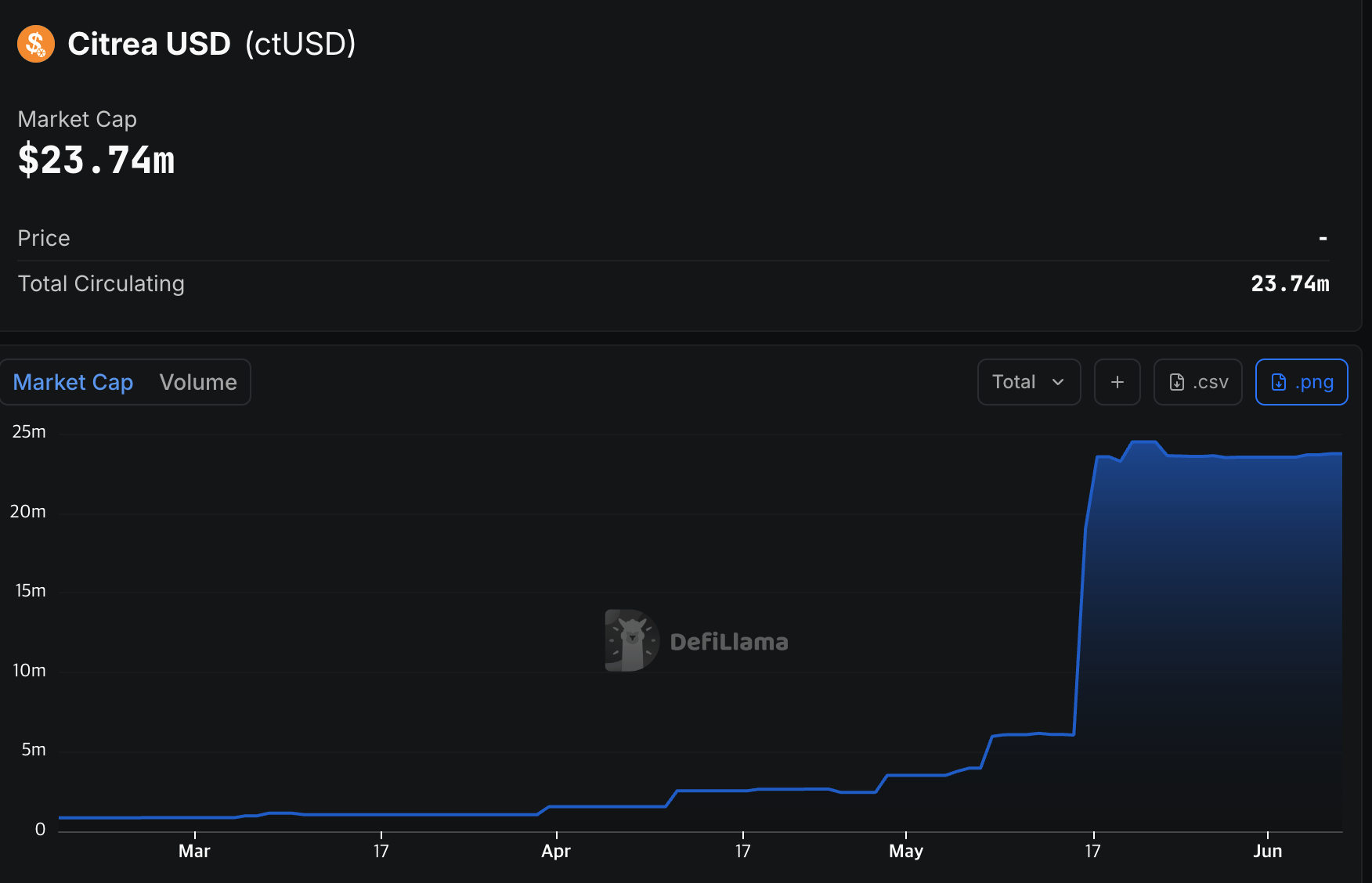

As noted earlier, Citrea's economy had been forming well before CTR launched. Just before CTR was issued, ctUSD supply stood at about $23 million, and the Clementine bridge had processed 140 BTC in total. The scale is small, but it is striking that these figures came from real user activity without fixed incentives.

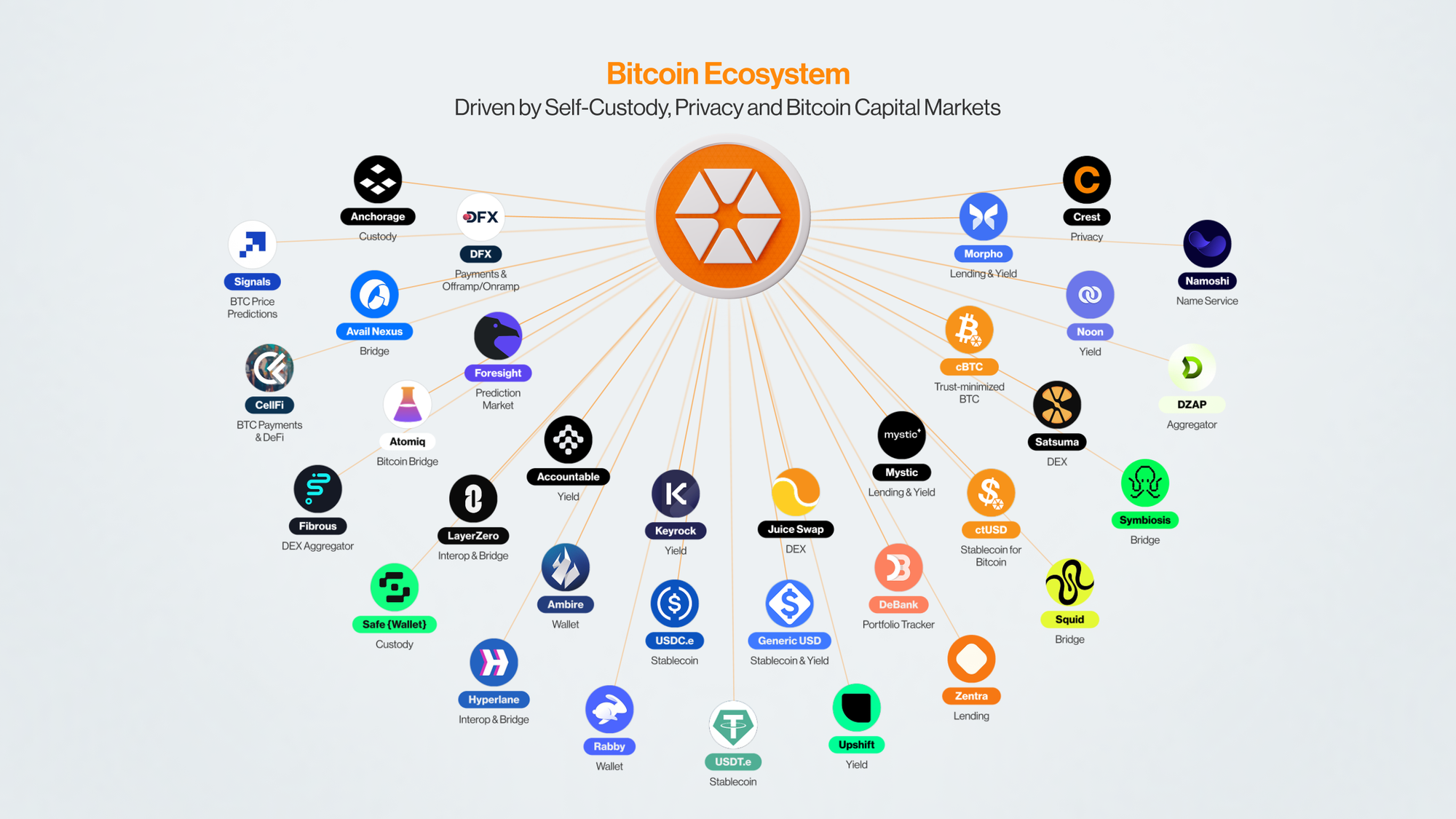

What binds Citrea's economy together is cBTC and ctUSD. If cBTC is the benchmark on the asset side, ctUSD is the benchmark on the liability and accounting side. Because these two tokens function as the common unit across every application, Bitcoin moves through exchanges, lending markets, and vaults without having to switch assets at each step. The Citrea ecosystem can therefore be read as a bundle of pathways that Bitcoin capital travels: entry, exchange, credit, and asset management. Each pathway is a place that shows what a Bitcoin holder becomes able to do with dormant Bitcoin. The sections that follow look at how Bitcoin is put to use through the projects in the Citrea ecosystem. These are applications built by independent teams on top of Citrea rather than by Citrea itself, while some being supported by the Citrea Foundation.

2.1 Exchange and Credit: Satsuma and Zentra

Satsuma is the flagship decentralized exchange supported by the Citrea Foundation, handling trading and liquidity allocation for cBTC, ctUSD, CTR, and others on the basis of concentrated liquidity. With about 167,000 cumulative trades and roughly 24,000 users, Satsuma is the most used application in the Citrea ecosystem and can be seen as the primary hub where the ecosystem's liquidity collects. Much like CTR, Satsuma chose a ve(3,3) structure with its own tokens SUMA and veSUMA, where governance votes set the direction of incentives, exit penalties are redistributed to the remaining stakers, and value accrues over time. In effect, the design for coordinating capital flows recurs not only at the chain level but also at the level of the applications above it.

Zentra is a lending protocol modeled on Aave, and the mechanism itself is the familiar overcollateralized lending structure, unchanged. What stands out is that its stage is Bitcoin. A user holding Bitcoin posts trust-minimized cBTC as collateral and borrows ctUSD without selling their Bitcoin, and the result settles in Bitcoin. If, as discussed in the earlier piece, Bitcoin-collateralized lending used to be a detour that required trusting a custodian or a multisig set each time, Zentra can be said to have rebuilt that trust on Citrea's decentralization through its infrastructure.

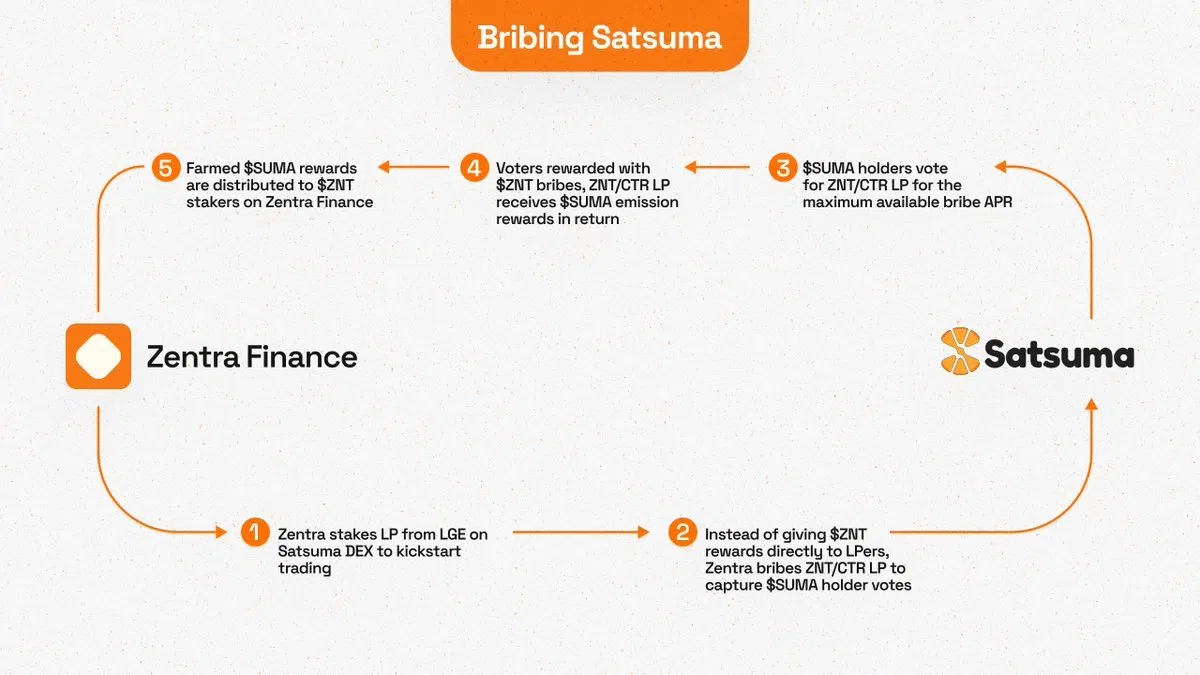

Zentra creates synergy with Satsuma through the design of its own token, ZNT. When Zentra started ZNT liquidity generation event on June 8, it put forward a model that returns about 90% of the protocol fees collected from interest margins, liquidation penalties, flash loans, and Satsuma rewards to stakers each week in ZNT or ctUSD, and it placed the entire team allocation in a permanent lock pool so that it cannot be withdrawn.

Source: Zentra Finance

As shown in the figure above, Zentra deposits the ZNT/CTR pool created through its LGE into Satsuma, and rather than handing ZNT directly to liquidity providers, it places a ZNT bribe on Satsuma's veSUMA voters to pull SUMA emissions toward that pool, then passes the SUMA farmed this way back to ZNT stakers. In effect, the gauge structure seen earlier in Citrea's CTR design has already been activated among the major liquidity players in the ecosystem, even before it has gone live at the chain level.

2.2 Vaults and Structured Products

The second is vaults and structured products that attach yield to Bitcoin itself, which grow in a form curated by professional asset managers. Keyrock's cBTC vault mixes on-chain and off-chain strategies to produce Bitcoin-denominated yield, while Noon's cBTC vault lets users keep their Bitcoin deposited while drawing out ctUSD liquidity to earn yield.

Citrea is driving the inflow of vault liquidity through two layers of different character.

One layer is institutional commitments. Citrea has said it secured more than $50 million in liquidity from asset managers including Galaxy Digital. This comes in not as dollars but as cBTC and ctUSD, and is deployed in stages into lending markets, exchanges, and cBTC structured yield products, keeping pace with the ecosystem's growth.

Source: Citrea

The other layer is community capital. This past May, to bootstrap ctUSD liquidity across the ecosystem, Citrea opened the ctUSD Pre-Deposit Vault curated by RockawayX on Upshift. The structure takes in USDC on Ethereum that users lock up for two months and pays out CTR as a reward. The public phase of initial $15 million cap filled in within seconds of opening, and an additional $3 million cap added afterward filled within minutes as well, bringing total deposits to $18 million and showing strong demand.

For early liquidity, placement matters more than scale. This is because where cBTC and ctUSD first accumulate in depth divides the later routes of liquidity allocation, and this capital can be seen as the seed money that the coordination mechanism will need to point in a direction. That said, since a fair share of this yield also comes from CTR rewards or points, how to retain the liquidity drawn in by the pre-deposit vault beyond the lock-up period, once incentives normalize, appears to remain an open challenge.

2.3 Prediction Markets: Signals

Source: Signals

The third is Signals, a prediction-market project centered on the Bitcoin market. Signals runs markets that predict the price of Bitcoin not as yes or no, but by range.

To build markets for betting on a continuously moving value like price, many prediction markets such as Polymarket typically slice the price range into several buckets and create a separate yes-or-no market for each bucket. This approach, however, has two weaknesses. Liquidity is fragmented across buckets so that each market grows shallow, and the probabilities assigned to each bucket do not line up with one another, so the whole becomes internally inconsistent.

Signals solves this with a pricing method called the Continuous Logarithmic Market Scoring Rule (CLMSR). It lays out the places where the price might fall on a fine-grained scale, but instead of splitting it into buckets, it binds the whole into a single curve and prices it. Any trade is priced along this one curve, and the cost of a trade is determined solely by how much that trade moves the curve. So whether you buy a narrow range or a wide one, it is priced by the same yardstick, and the total cost of moving the market to the same point is the same no matter what order the trades arrived in. Because liquidity gathers on a single curve, even large bets move the price only slightly, and a user can express the view that the price will close within a particular range in a single trade.

Another point worth noting in the design is the way it separates trading and settlement in time. Trading runs continuously over a set period, but settlement happens once a day. Prices form on a daily basis, that day's settlement finalizes the outcome, and payouts follow accordingly. At settlement, signed oracle data fixes the price observed that day as a single point on the scale, and the amount each position receives is calculated automatically from that point, the range it chose, and the size of the bet.

That settlement concludes cleanly and without dispute follows from what Signals chose as its object of prediction. It deals with a price objectively observed in the market, not an event open to differing interpretations. Unlike ordinary prediction markets, where subjective disputes often arise over judging the outcome, in Signals the question of where the price closed is settled on-chain as a single value according to fixed rules. On top of this, since the cost and the return of a trade are denominated in ctUSD, Signals too operates within the single economy that cBTC and ctUSD tie together.

2.4 Privacy: Crest

The fourth strand is privacy. Crest is a Bitcoin mobile wallet built on a zero-knowledge privacy pool on Citrea, adapting the open-source Nocturne protocol for Bitcoin. It works by following the familiar shielded-pool model. When Bitcoin is deposited into the pool, that deposit becomes a private commitment, that is, a note, and the user proves ownership with a zero-knowledge proof and spends this note privately. This makes possible encrypted balances, shielded addresses, fully private transfers, and private DeFi interactions. Crest is an early-stage project that opened its private beta in March 2026, but it is worth noting that a dimension of privacy is being added to the Bitcoin economy.

3. Closing Thoughts

The projects on Citrea are not a collection of unrelated applications but a single economy interlocked through cBTC and ctUSD as shared assets. A flow runs across a single chain: bringing Bitcoin in as cBTC to earn yield in a vault or to borrow ctUSD on Zentra, supplying that asset as liquidity on Satsuma, and settling a Signals position with the same ctUSD.

For now, Citrea's economy still looks like it is in an early stage. Much of the liquidity depth in each pool leans on incentives, and while DeFi liquidity has grown steadily since the mainnet launch, as of June 8, 2026, the time of writing, it stands at roughly $7 million in total, which is on the shallow side. The infrastructure is in place, but attracting and allocating liquidity is the gap the coordination asset aims to fill, and Citrea is preparing Citrea Gateway, a unified interface that lets users explore and allocate across liquidity pathways from a single screen.

CTR is not a token that promises an economy yet to come, but one that has taken over the wheel of an economy that was already running. Where a typical project floats a token first and waits for the economy to follow, Citrea ran lending, trading, and yield products first after the mainnet went live, and then handed control over to the token. This leaves a question of whether the inflow and allocation of ecosystem liquidity can be resolved through coordination by way of community participation.

What remains is a matter of proof. Whether the gauge actually runs and withstands many cycles and adversarial conditions, whether liquidity pulled in by incentives stays once the incentives are withdrawn and the pre-deposit vault's lock-up ends, and above all whether revenue generated in cBTC and ctUSD someday reaches xCTR through the governance treasury so that CTR actually captures the cash flow it directs, are all questions that time will answer. The on-chain traction that builds over the next few quarters, on top of the shallow liquidity just after issuance, will answer whether CTR is an asset coordinating a real economy or a temporary incentive program.

The report is based on the independent research of the author sponsored/funded by Chainway Ltd. The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.