Table of Contents

Researcher

Related Projects

Key Takeaways

- Ondo Perps is the first derivatives platform to enable the use of tokenized equities as margin, eliminating the forced-sell problem that fragments capital across every other platform. Traders can post SPYon and QQQon directly as collateral with the spot exposure stays intact while the capital becomes productive.

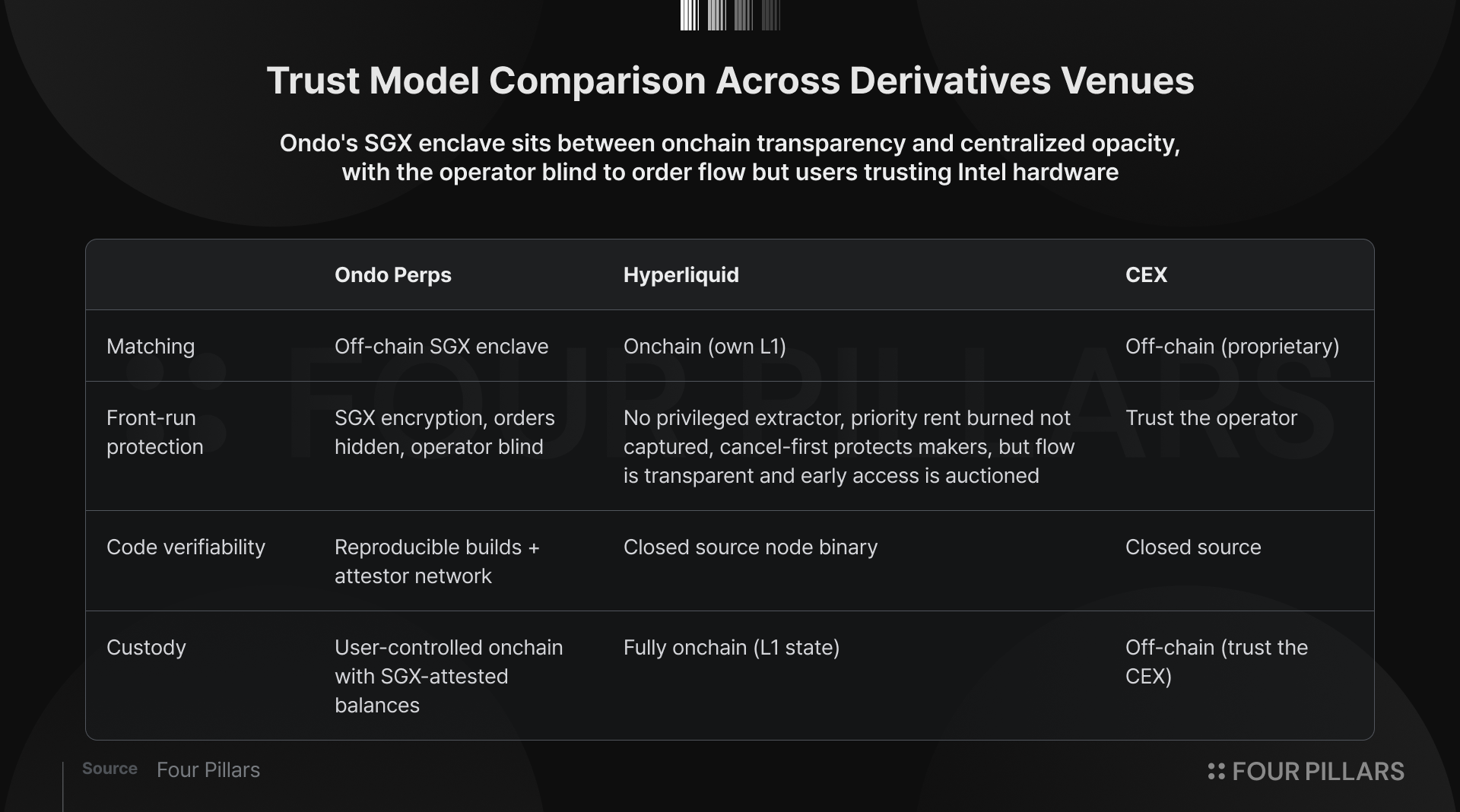

- The SGX enclave architecture is a deliberate trust midpoint between CEX and on-chain. Off-chain matching runs inside hardware-encrypted memory the operator cannot access, verified by an attestor network with split key material.

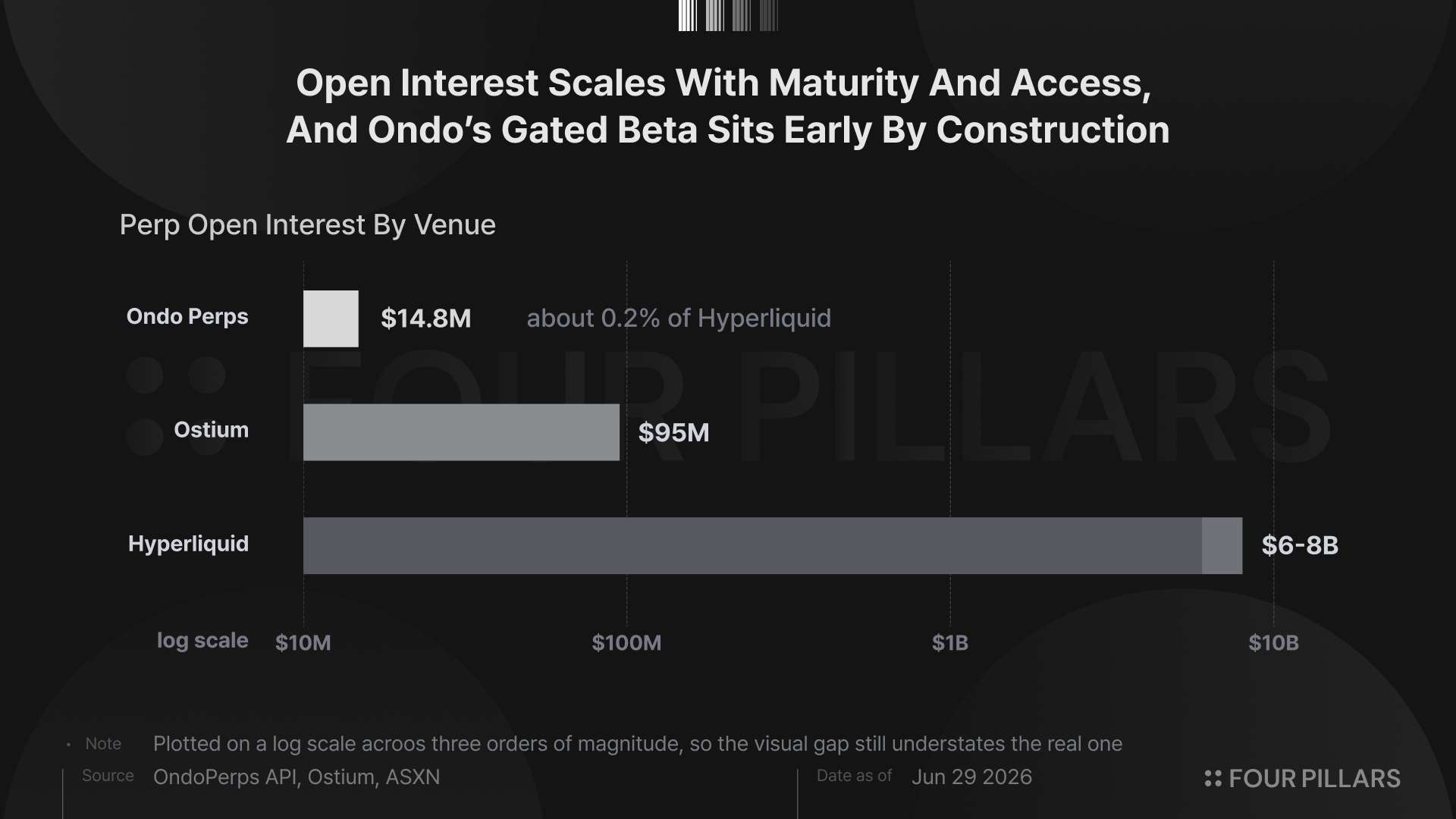

- $1.12B in cumulative volume and $14.8M in open interest within twenty days.

1. Productive Capital Thesis

The concept of onchain prime brokerage has been discussed for years, but nobody has shipped a product that gets close to what the term actually means. In traditional finance, a prime broker lets institutional clients hold a diversified portfolio of assets and trade derivatives against that portfolio as collateral, all within a single venue. In crypto, the closest equivalents only accept cash or stablecoins as collateral. If you hold tokenized equities and want to trade derivatives, you sell first, losing your spot exposure, and post USDC or USDT. The capital gets locked twice, once to buy the stocks and once to collateralize the trade. Goldman Sachs does not ask you to sell your equities before opening a futures position.

Ondo Perps allows traders to post SPYon and QQQon (Ondo’s tokenized S&P 500 and Nasdaq 100 trackers) directly as margin for perpetual futures, with a $100,000 per-asset cap. A trader holding SPYon can open a leveraged gold futures position without selling a single share. Hence, the spot exposure stays intact while the capital is productive.

For market makers, the implications are significant. A market maker running a hedged book can maintain both legs of the trade within a single collateral pool rather than splitting capital across platforms. This is how institutional desks have operated in traditional markets for decades, and it is the capability that has been conspicuously absent from every on-chain derivatives venue until now.

Today the implementation is pre-alpha, with general access to tokenized stock collateral coming soon. Two tokenized securities are accepted as collateral, with access limited to whitelisted wallets during the pre-alpha period, along with $100,000 cap limits. NVDAon, TSLAon, and GOOGLon and many more tokenized stocks and ETFs are planned additions. But the architecture is designed for generalization, and as Ondo’s tokenized equity universe expands beyond 430 assets through Ondo Stocks, the collateral pool can grow with it.

2. Enclave Architecture

Where Hyperliquid built its own L1 to run matching entirely onchain, and centralized exchanges like Binance run proprietary matching engines behind closed doors, Ondo Perps went in a different direction. The matching engine it routes to runs off-chain inside an Intel SGX hardware enclave verified by an independent attestor network.

The system has three components:

- The Engine handles all matching, position tracking, and liquidation logic off-chain, running inside an SGX enclave, an isolated region of hardware memory inaccessible to the operating system, the cloud provider, or even Ondo Perps’ own team. All orders are processed in fully encrypted form and trade history is only revealed after full processing, which means the operator cannot see, reorder, or front-run orders.

- Chain-Core sits on Ethereum and handles token transfers, acting as the settlement layer without any knowledge of internal account states.

- The Attestor Network, continuously verifies that the correct and unmodified codebase is running on genuine SGX hardware, with cryptographic key material split across the network so that no party can reconstruct the master secret or move funds. Any code modification requires an independent majority of attestors to audit and approve.

Fund flows are onchain, the matching code produces reproducible builds that anyone can verify against the deployed binary, and the attestor network provides external verification that does not exist in traditional venues.

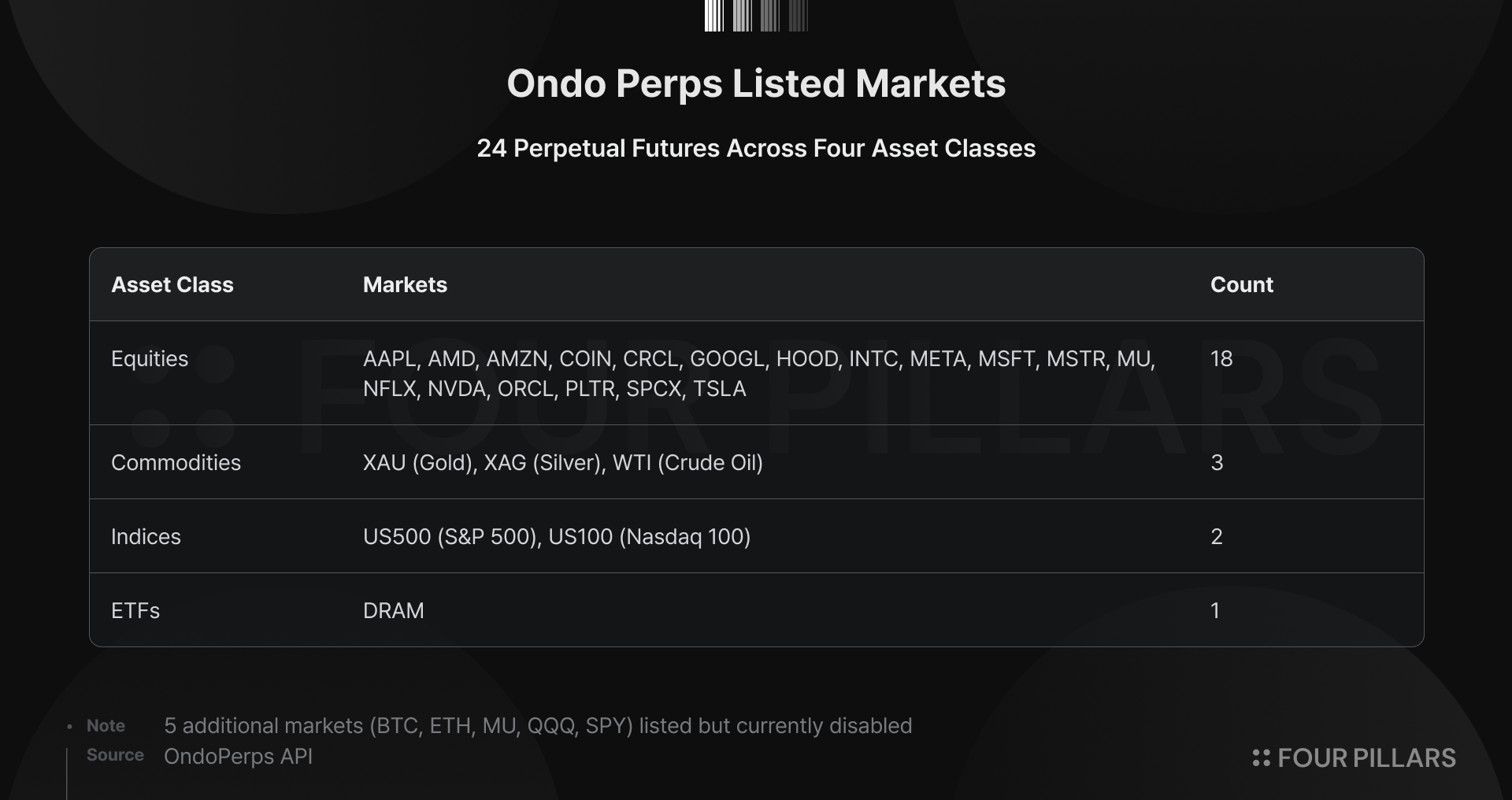

Ondo Perps currently lists 24 perpetual futures markets spanning four asset classes. 18 U.S. equities including AAPL, NVDA, TSLA, META, and MSFT (most at 10x max leverage, AAPL at 20x), two indices at 20x (S&P 500 and Nasdaq 100), three commodities at 20x (gold, silver, crude oil), and one ETF (DRAM). Pricing uses a dual oracle system that averages Pyth and Stork feeds during market hours and switches to an internal order-book-derived mechanism on weekends. Maker fees sit at 1.5 bps and taker fees at 3.5 bps.

3. Flywheel

Ondo Perps does not exist in isolation. It is the latest product in the Ondo ecosystem, and the strategic significance of each product becomes clear when you see where they connect.

Ondo Finance has developed the technology that powers three distinct financial products:

- USDY is a yield-bearing stablecoin backed by U.S. Treasuries and U.S. Treasuries funds with $2.15 billion in TVL across ten chains, earning approximately 4.65% APY.

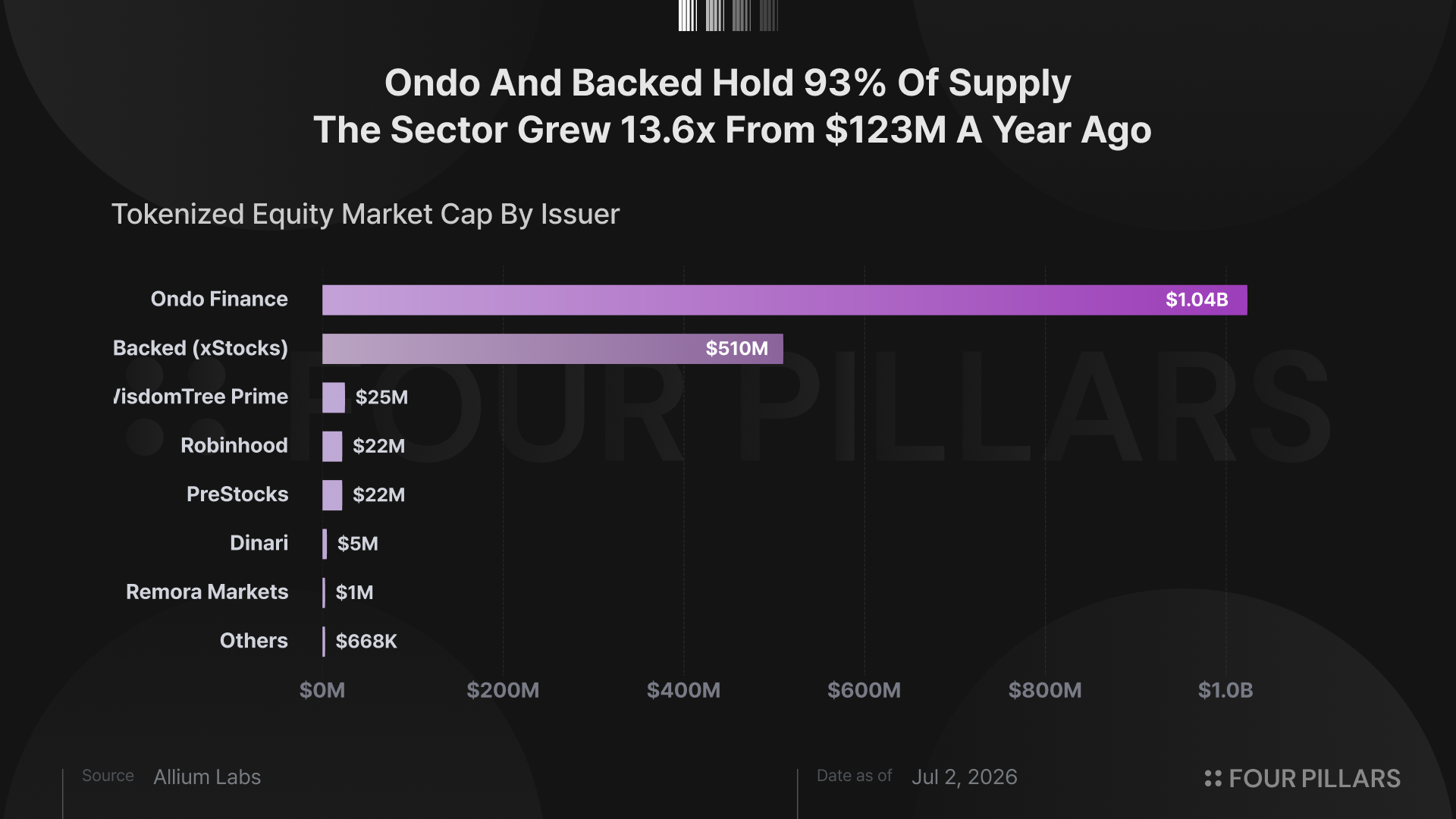

- Ondo Stocks issues over 430 tokenized U.S. stocks and ETFs, and has accumulated more than $1 billion in TVL, processed over $20 billion in cumulative trading volume, and holds over 62% market share by tokenized equity market cap.

- And now Ondo Perps, the derivatives layer.

Ondo Stock’s tokenized equities (SPYon, QQQon) can be posted as margin on Perps, which is what turns Ondo Stocks into the frontend of a prime brokerage because a trader’s equity holdings become productive. The more assets Ondo tokenizes through Ondo Stocks, the deeper the potential collateral pool available on Ondo Perps, and the more capital-efficient the overall system becomes. This is the flywheel.

What is not an open question is the institutional weight behind the Ondo ecosystem’s infrastructure. Franklin Templeton tokenized five of its ETFs through Ondo Stocks in March 2026. On June 16, Mirae Asset ($721 billion AUM, South Korea’s largest asset manager) signed an MOU to tokenize its Global X ETF lineup, starting with 10 U.S.-listed ETFs spanning AI, robotics, silver, defense, and covered call strategies.

On the distribution side, Ondo Stocks are already live on Bitget (first CEX listing, 100+ assets), Deutsche Borse’s 360X venue, Exodus Markets (200+ stocks on Solana), Felix Protocol (35 assets on HyperEVM), PancakeSwap, Titan, and Jupiter. Clearstream is integrating Ondo tokenized assets into its custody and settlement infrastructure. Broadridge enabled proxy voting for 250+ Ondo tokenized stocks in April 2026.

Most recently, all 430+ OGM tokens went live on Uniswap via UniswapX on Ethereum and BNB Chain.

None of this directly expands the Ondo Perps collateral pool just yet, but it tells you something about the caliber of institution that has decided to build on Ondo’s technological rails, and that institutional credibility is what separates Ondo Perps from every other new perps venue.

Meanwhile, what makes the Ondo ecosystem transformative beyond its technology and distribution is the regulatory infrastructure Ondo Finance and its partners have built around it. In October 2025, Ondo Finance acquired Oasis Pro, gaining a FINRA-member broker-dealer license, an SEC-registered Alternative Trading System, and transfer agent capabilities. Ondo Stocks filed a confidential SEC registration statement for transferable tokenized stocks and an SEC no-action letter in April 2026 regarding recording securities entitlements on Ethereum. It holds EU approval across 30 countries for tokenized stocks and ETFs.

These are not features you can fork. They are years of regulatory work that create a moat independent of the technology. With the CFTC having approved Kalshi’s perp listing in May 2026, signaling regulatory acceptance of onchain perpetual futures in the U.S., the Ondo ecosystem is positioned to expand if the domestic market opens.

4. $1.12B in Volume, $15M in OI in 20 Days

Ondo Perps crossed $1.12 billion in cumulative volume within its first twenty days of public beta, averaging roughly $56 million per day. A whitelist beta on crypto rails fills first with crypto-native traders, which is the cohort the collateral feature has to convert from spot holder into margin user, so an early book weighted toward commodities and one newsy name is a starting point.

Spreads are remarkably tight. Gold shows $612,000 of book at a 1.5 bps spread and silver carries $2.54 million at 3.5 bps, which is institutional-grade market-making quality. Funding has run close to flat, with 486 of 500 hourly gold samples at the base rate, consistent with a young and well-balanced book that has not yet developed a directional lean.

Open interest sits at $14.8 million against Ostium near $95 million and Hyperliquid in the $6 to $8 billion range, largely because the venue is still whitelist-only, still in beta, and capped per asset, so the size visible today is the size the design currently permits.

5. Looking Forward

Ondo Perps is three weeks old, still in beta, still whitelisted. Currently the volume is commodity-dominated, the open interest is comparatively thin, and the collateral feature that defines the thesis is capped at two assets and $100,000 each. By any conventional metric, this is an early-stage product.

What makes it worth watching is the infrastructure underneath. Ondo Finance has spent years building technological infrastructure, regulatory licenses, and institutional relationships that cannot be replicated on a short timeline. Franklin Templeton and Mirae Asset are not tokenizing their ETFs through Ondo Stocks because of the perps exchange. They are doing it because of the regulatory moat and distribution network. But the fact that Ondo Perps exists on the technology rails built by Ondo Finance means it inherits credibility and infrastructure that would take a standalone derivatives venue years to build independently.

The report is based on the independent research of the author sponsored/funded by Ondo. The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.