Table of Contents

- Key Takeaways

- 1. Revisiting Cap

- 2. Six Months of Change

- 2.1 The Institutionalization of Underwriters

- 2.2 The Expansion of Underwriting Capital: Ethereum Restaking, Bitcoin Collateral, and Even Money Market Funds

- 2.3 The Expansion of Reserve Assets

- 2.4 The Expansion of Demand: stcUSD Enters Payment Rails

- 3. Cap in Metrics: What Matters More Than Total Value Locked

- 3.1 The Diverging Paths of TVL and Borrowing

- 3.2 The Reversal in Reserve Composition

- 3.3 The Shift in Yield Sources and the Paradox of Capital Efficiency

- 3.4 What Matters More Than Yield

- 4. Cap's Final Component, $CAP

- 5. Looking Ahead

- 5.1 The Shift in Risk and the Paradox of Slashing

- 5.2 Cap's Competitiveness Will Come From Risk Disclosure, Rather than Yield

Researcher

Related Projects

Key Takeaways

- The core challenges that lingered at Cap six months ago, namely its heavy reliance on self-delegation and low capital utilization, have now been resolved to a meaningful degree. EtherFi and Bedrock have each stepped into independent underwriter roles backed by ETH and BTC collateral, moving the system away from self-delegation, and reserve utilization, which sat at just 5.3% in December 2025, climbed to roughly 60% by the end of the first quarter of 2026. The 100 million dollar revolving credit facility extended to Susquehanna Crypto also signaled that institutional borrowing has begun to move beyond the pilot stage.

- The number of registered underwriters grew from 12 to 22 and borrowers from 18 to 30, yet it remains unconfirmed whether an independent credit market, in which different underwriters price different borrowers differently, is actually functioning. It is still untested in practice how far operators' real strategies and legal agreements can be publicly verified, and whether the slashing and repayment paths will work as intended in the event of a large default.

- In terms of metrics, the borrowing utilization rate and the composition of yield sources now matter more than total value locked. TVL stands at around 250 million dollars, below its previous peak, but borrowed capital has grown substantially compared with before. The yield on stcUSD has also fallen from about 8.6% in December 2025 to the low 5% range today, yet its relative standing against comparable products has actually improved.

1. Revisiting Cap

In the article I wrote last December, I introduced Cap as a "verifiable yield-bearing stablecoin project." At the time, Cap put forward a structure in which the paths of lending, collateral, and liquidation could be traced onchain, and in which operator losses were automatically absorbed through the slashing of underwriting collateral via smart contracts. It was an attempt to address, through a verifiable structure, the failures that traditional finance and early DeFi had repeated because of opaque yield sources and reliance on trust.

Source: Cap

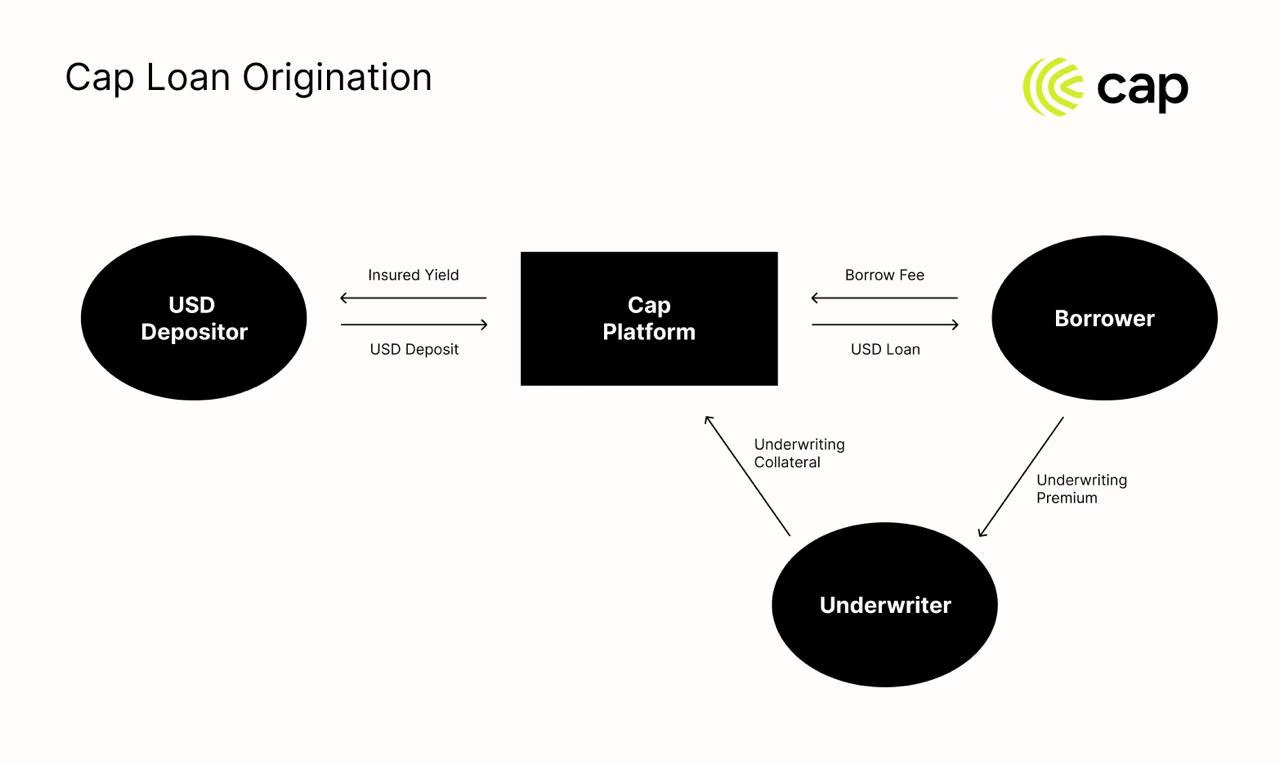

The heart of Cap's design lies not in yield but in the path of losses. As shown in the figure above, Cap's structure can be reduced to three actors.

- Depositor: When a user deposits dollar assets, cUSD is issued, and by staking cUSD the user can mint stcUSD, a yield-bearing stablecoin.

- Borrower: Borrows capital from Cap's reserves to deploy in external strategies, then repays principal and interest.

- Underwriter: Assigns assets such as Ethereum restaking collateral to a specific borrower, and if that borrower fails, the collateral absorbs the loss first. In return for providing this guarantee, the underwriter collects a premium from the borrower.

Where conventional yield-bearing stablecoins placed both the yield and the operational risk entirely on the user, Cap distributes these across three actors. Users supply dollar liquidity, borrowers execute yield opportunities, and underwriters take on credit judgment and loss absorption. The verifiability Cap speaks of comes from the fact that the relationships among these three ledgers can be traced onchain.

Cap does not directly control a borrower's strategy, nor does it permit only verifiable strategies. Its core principle is not that "every strategy is fully visible onchain," but that "the party who bears the loss when a strategy fails is decided in advance, and the path of loss absorption is written into code." If a borrower fails to repay or the collateral ratio reaches a dangerous level, the underwriter's collateral is slashed and used to repay debt and replenish reserves. This works on a principle similar to the way subordinated debt absorbs losses ahead of senior debt in traditional finance, and the fixed fee the underwriter receives is in effect compensation for taking on the borrower's default risk, giving it a structure similar to a collateralized credit default swap (CDS).

That said, a traditional credit default swap carries the risk that, when a default actually occurs, the party that sold the protection cannot pay the money it promised. That was precisely the problem exposed in the 2008 financial crisis. Cap, by contrast, locks up the underwriting collateral in advance and enforces slashing through code, so depositors bear only the question of whether the collateral locked within the protocol is sufficient, rather than the risk that an underwriter will fail to repay. In effect, the promise of loss absorption has been shifted from a person's willingness to perform to collateral and code, and liquidation too is carried out automatically by smart contracts through a Dutch auction, without governance votes or legal proceedings.

Now, six months after I first introduced Cap, the project is emphasizing this structure even more. In an article published in January 2026, Cap reintroduced itself as a credit platform backed by collateral, that is, "Covered Credit." It has, in other words, begun to explain the yield from its stablecoin as a product of credit backed by collateral. The names of the actors have been organized to fit this framing as well. Depositor, operator, and delegator became depositor, borrower, and underwriter, and the base supporting Cap's deposited assets shifted from dollar-based safe assets to crypto collateral.

How far has Cap kept its promise of verifiable finance over the past half year, and what new burdens has it taken on along the way? In this article, I review the changes and results at Cap over the past six months and consider where it is headed next.

2. Six Months of Change

2.1 The Institutionalization of Underwriters

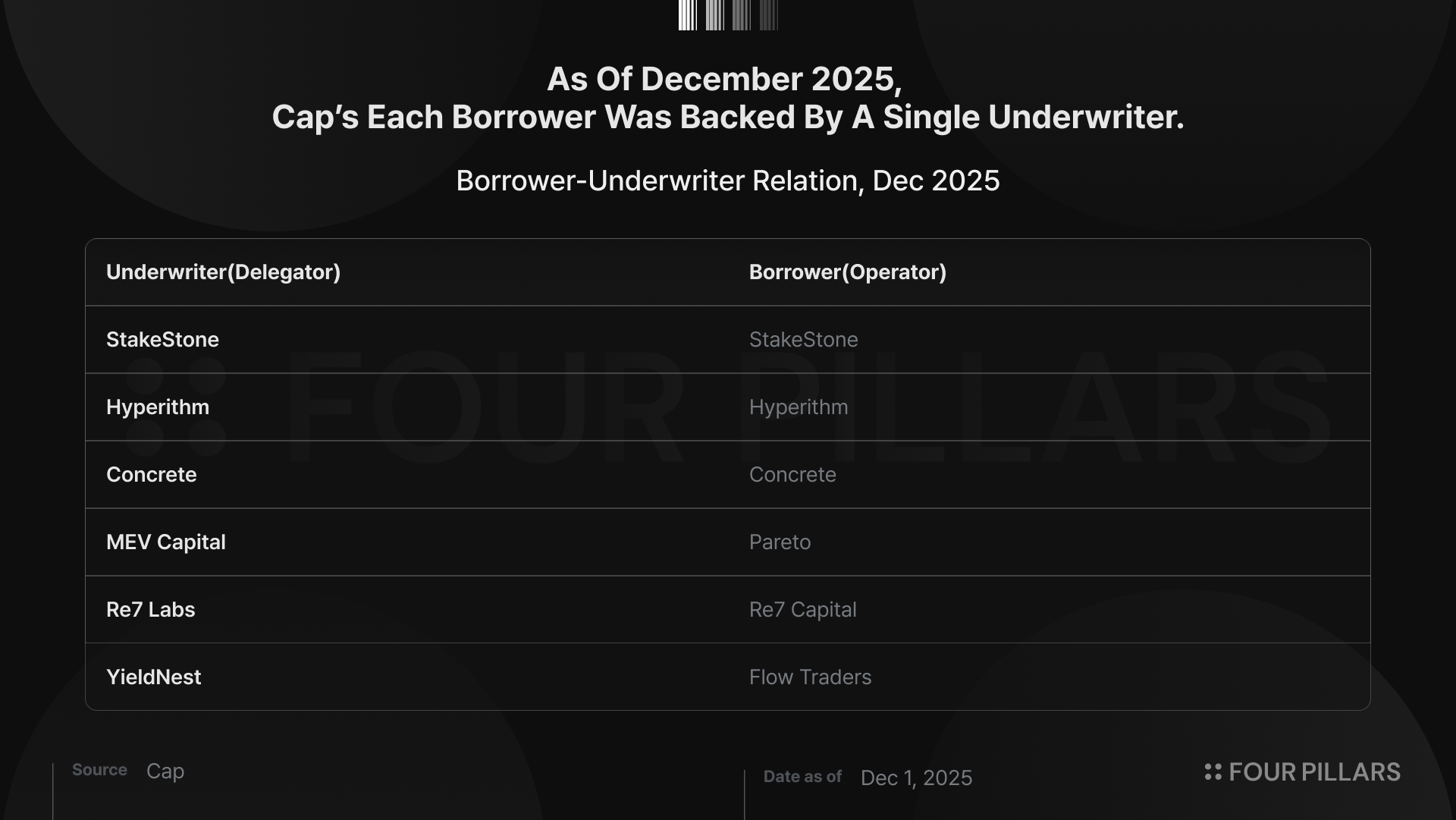

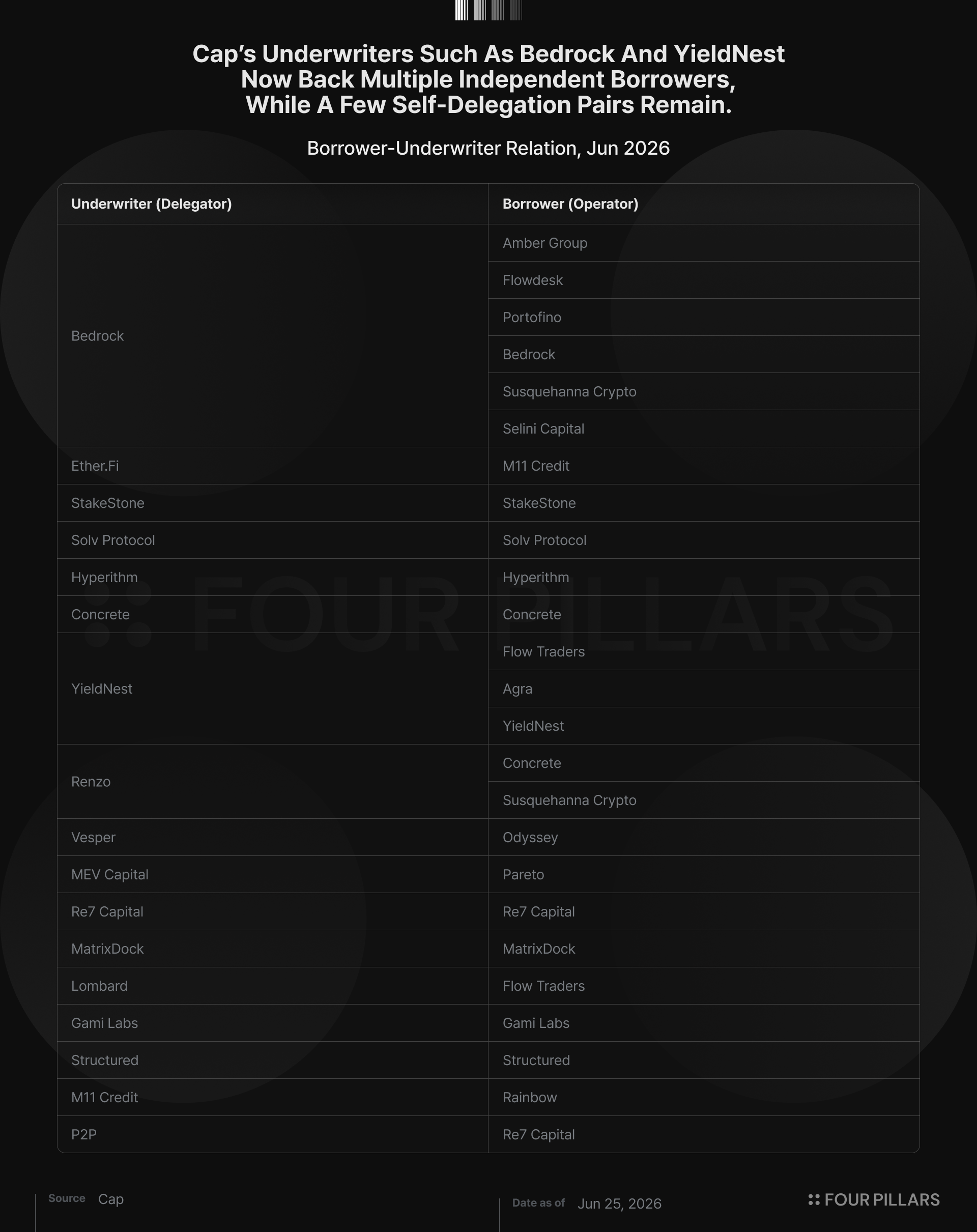

Six months ago, the most pressing task for Cap seemed to be the self-delegation of delegators. The delegators registered in the contract were varied, but most of the relationships that were actually active took the form of operators posting collateral to themselves. For Cap's core structure of market-based credit assessment to work, independent third-party underwriters appeared to be necessary.

Source: Cap, Data as of 2026.06.24

Six months later, laying out the same relationship map reveals a noticeably different picture. A many-to-many structure has taken hold, in which one underwriter handles several borrowers and a single borrower receives collateral from two or more underwriters. Not every self-delegating pair in which the underwriter and borrower are the same has disappeared, but cases like Bedrock, which underwrites several independent borrowers, are increasing, and the fact that both borrowers and underwriters have grown more diverse can be viewed positively.

Source: Cap

In addition, in March 2026 Cap announced an institutional restaking partnership involving four parties: Ether.Fi, Symbiotic, M11 Credit, and FalconX.

In that partnership, Ether.Fi serves as the underwriter that backs borrowing with restaked ETH collateral, M11 Credit acts as the borrower that draws capital on the basis of that collateral, and FalconX takes on the role of generating actual yield with the borrowed capital and managing the loan. It created a case of institutional division of labor in which the underwriter, the borrower, and the yield generator are split into separate entities. Here Ether.Fi's collateral is implemented as a separate token called weETHs, and because the delegated collateral takes on real credit risk and receives a credit spread in return, this can be seen as an onchain reproduction of the way a guarantor in traditional finance collects a guarantee fee and assumes default risk.

One issue remains in this structure, however: FalconX's yield strategy consists of offchain activity across exchanges that cannot be directly verified onchain. To address this, Cap and FalconX designed the arrangement to set up a dedicated special purpose vehicle (SPV), to operate all loans on an overcollateralized basis only, and to hold the collateral assets in a third-party custody structure. It appears that Cap's philosophy of placing the focus of verification not on the execution of the strategy but on whether the promised repayment is fulfilled applies equally to institutional borrowers.

2.2 The Expansion of Underwriting Capital: Ethereum Restaking, Bitcoin Collateral, and Even Money Market Funds

The second notable update is the broadening of the underwriting collateral. Cap's early underwriting structure was described as using collateral from Ethereum-based restaking protocols through shared security networks such as EigenLayer and Symbiotic.

Source: Cap

In March of this year, however, Bedrock joined as a Bitcoin liquid restaking protocol, adding a structure in which it underwrites borrowers with its own uniBTC and receives dollar-denominated yield. Bedrock's delegation has grown from an initial 1 million dollars to more than 155 million dollars as of June 2026.

This means more than the simple addition of one Bitcoin-class collateral. In Cap's structure, an underwriter backs borrowers who borrow dollars, but the underwriting collateral need not itself be dollars, so Cap can operate as a market that connects the borrowing demand for dollar assets with the cost-of-capital differences of non-dollar collateral. Until now, Bitcoin holders faced only two choices: hold Bitcoin and earn no yield at all, or sell Bitcoin to convert it into a stablecoin and give up their Bitcoin exposure. Bedrock allows holders to keep their Bitcoin exposure through uniBTC while receiving the yield generated by borrowers in dollars, creating a form of return, namely dollar yield layered on Bitcoin collateral, that had not previously existed at institutional scale. On top of this, on June 4 Solv Protocol's solvBTC joined as an underwriter asset alongside Bedrock's uniBTC, so that Bitcoin-class collateral no longer depends on a single type.

Source: Cap

The scope of underwriting collateral has expanded even to real-world assets. In June, Cap integrated Matrixdock's XAUm as a collateral asset. XAUm is tokenized gold backed by LBMA-certified physical gold, so Cap's underwriting collateral now extends beyond restaking assets to include gold, a traditional reserve asset.

2.3 The Expansion of Reserve Assets

Source: Cap

There were changes on the reserve side as well. WisdomTree's WTGXX was integrated as a reserve asset. With this, Cap took shape as a system that accepts tokenized dollar-like assets as reserves on one side and Ethereum and Bitcoin-class collateral as underwriting capital on the other, creating dollar-based credit in the process. Accordingly, Cap's risk is gradually shifting from simple stablecoin reserve risk toward credit-market risk, which involves coordinating multiple forms of collateral, multiple borrowers, and legal agreements.

Source: Cap

In June, Ondo Finance's OUSG was integrated into reserve management. OUSG is a tokenized RWA fund with onchain exposure to short-term U.S. Treasuries and money market funds, and through this integration Cap can now deploy idle reserves that are not being used for borrowing into U.S. Treasury yield via OUSG.

Source: Cap

The institutionalization of reserves recently advanced a step further, as Cap onboarded as a BENJI client, accepting Franklin Templeton's tokenized money market fund BENJI as a supported deposit asset. Launched in 2021, BENJI is the oldest tokenized money market fund in its category, an onchain share token of the U.S.-registered Franklin OnChain U.S. Government Money Fund (FOBXX).

Because BENJI is a permissioned asset that can be connected only with the direct approval of Franklin Templeton's digital assets team, it is striking that Cap passed Franklin Templeton's full compliance review to qualify for holding BENJI in a wallet. With BENJI added on top of WTGXX and OUSG, Cap's reserves are rapidly absorbing tokenized dollar-like and Treasury-like safe assets while at the same time building up a signal that it is a platform that has passed the due diligence of regulated institutions.

2.4 The Expansion of Demand: stcUSD Enters Payment Rails

Source: Cap

If the changes described above concerned the supply side, namely reserves and underwriting collateral, there was meaningful progress on the demand side over the same period. Through LayerZero, Cap made it possible to bridge cUSD and stcUSD to several chains including Ethereum mainnet, MegaETH, and Tempo, and in June RootsFi integrated stcUSD as a default yield source on Tempo. This means that balances on the RootsFi payment network automatically earn stcUSD yield, showing that Cap's yield-bearing stablecoin has begun to flow beyond trading and farming demand into a new source of demand, namely actual payment balances.

3. Cap in Metrics: What Matters More Than Total Value Locked

3.1 The Diverging Paths of TVL and Borrowing

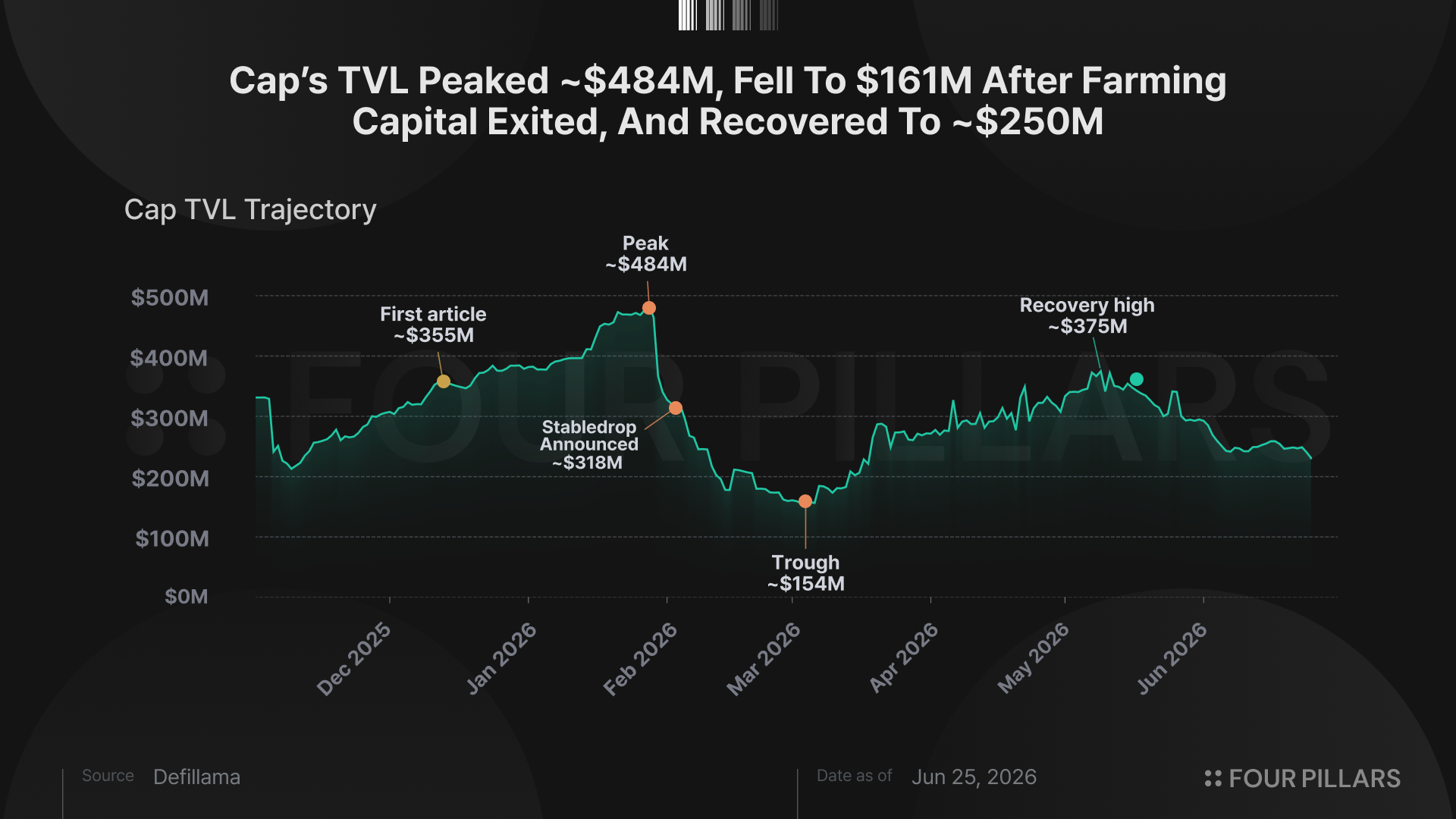

Cap's TVL has moved through wide swings over the past six months. After rising quickly soon after launch to a near peak of about 379 million dollars at the end of December 2025, TVL fell by more than half to around 160 million dollars in February 2026, then recovered to the current level of about 250 million dollars. The sharp drop in February may look like bad news on the surface, but it was the result of farming capital chasing short-term rewards exiting at a point that coincided with the period right after the Frontier program, the first incentive deposit program, and a broad downturn across crypto.

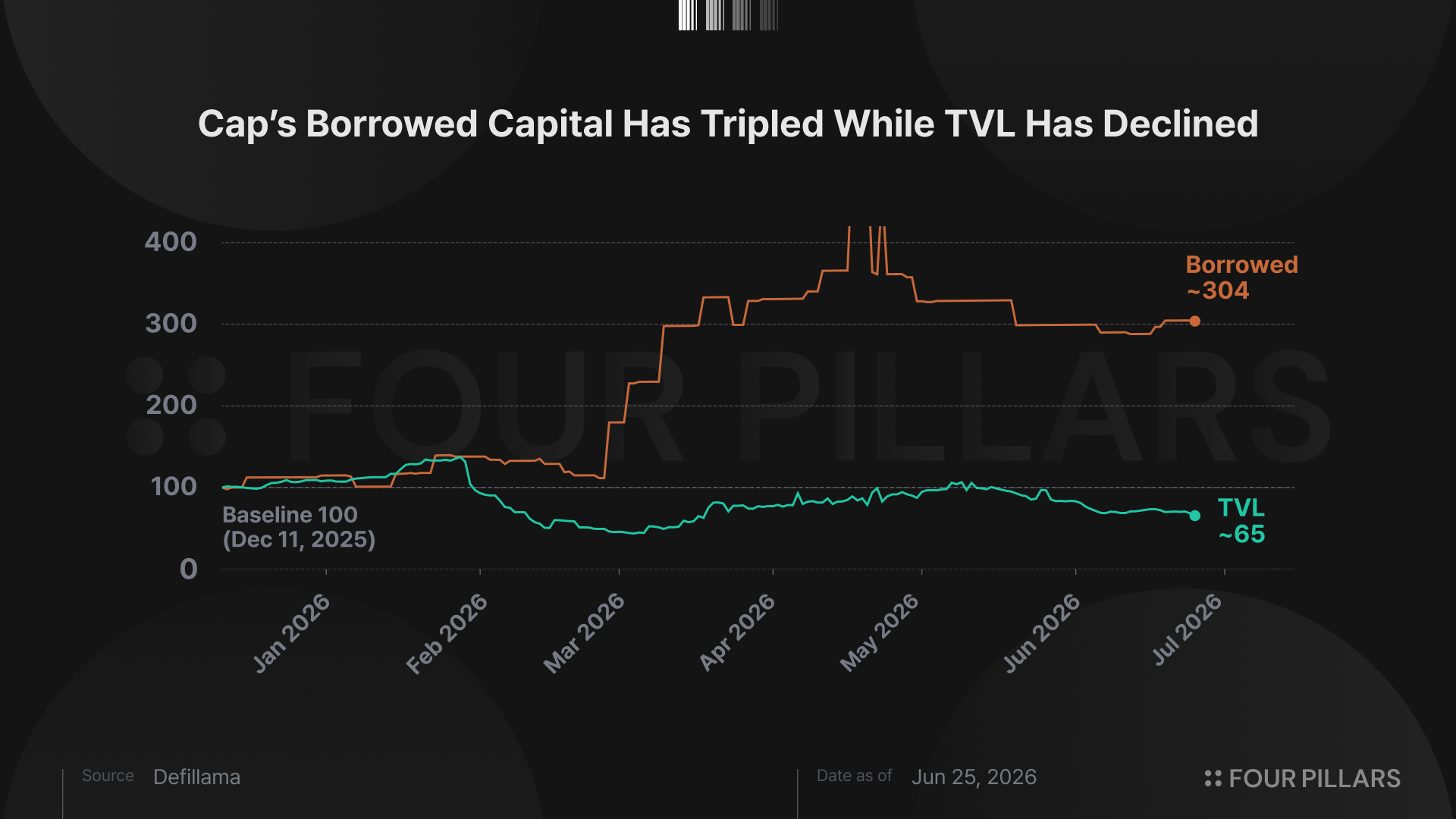

Meanwhile, borrowing balances over the same period traced an entirely different path. If we set December's TVL and borrowing both to 100 and rebase the two metrics, TVL rose to about 137 at its peak and has since come down to roughly 71, while borrowing surged to about 305. Even as the headline figure fell, actual credit activity grew threefold.

TVL can swing widely with prices and incentives, but borrowing balance is a metric driven by borrowers' real demand for capital. In March, when TVL dropped sharply due to a decline in short-term farming demand, borrowing demand surged instead, and Cap showed itself moving in earnest from a deposit product toward a credit market.

3.2 The Reversal in Reserve Composition

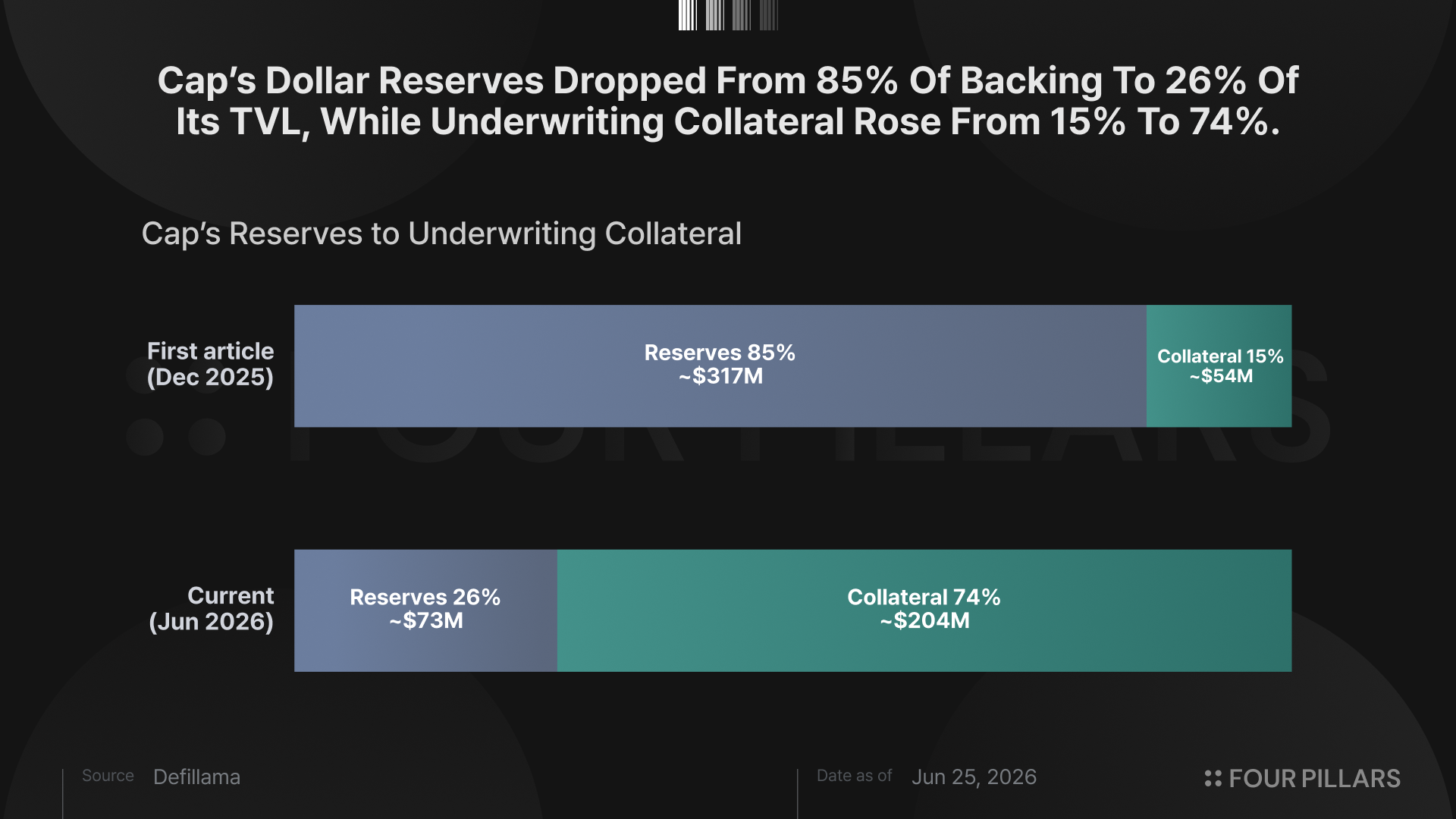

The most fundamental change in Cap's capital structure is that the balance between reserves (the total deposits of cUSD issuers) and the collateral posted by underwriters has flipped. At the time of the first article, in early December 2025, Cap had a structure in which about 45.6 million dollars of delegated collateral sat on top of roughly 277 million dollars of reserves. The deposited dollars were far larger, and the collateral layered on top was thin. Six months later, the opposite is true. Reserves have shrunk to somewhere around 80 million dollars, while underwriting collateral has become the large pillar supporting the entire pool of deposited assets. Underwriting collateral passed 170 million dollars over the course of the first quarter and currently holds at around 200 million dollars.

This reversal matters because the fact that reserves shrank while collateral grew means that the assets backing Cap's TVL have shifted from dollar-denominated safe assets to volatile collateral such as ETH and BTC.

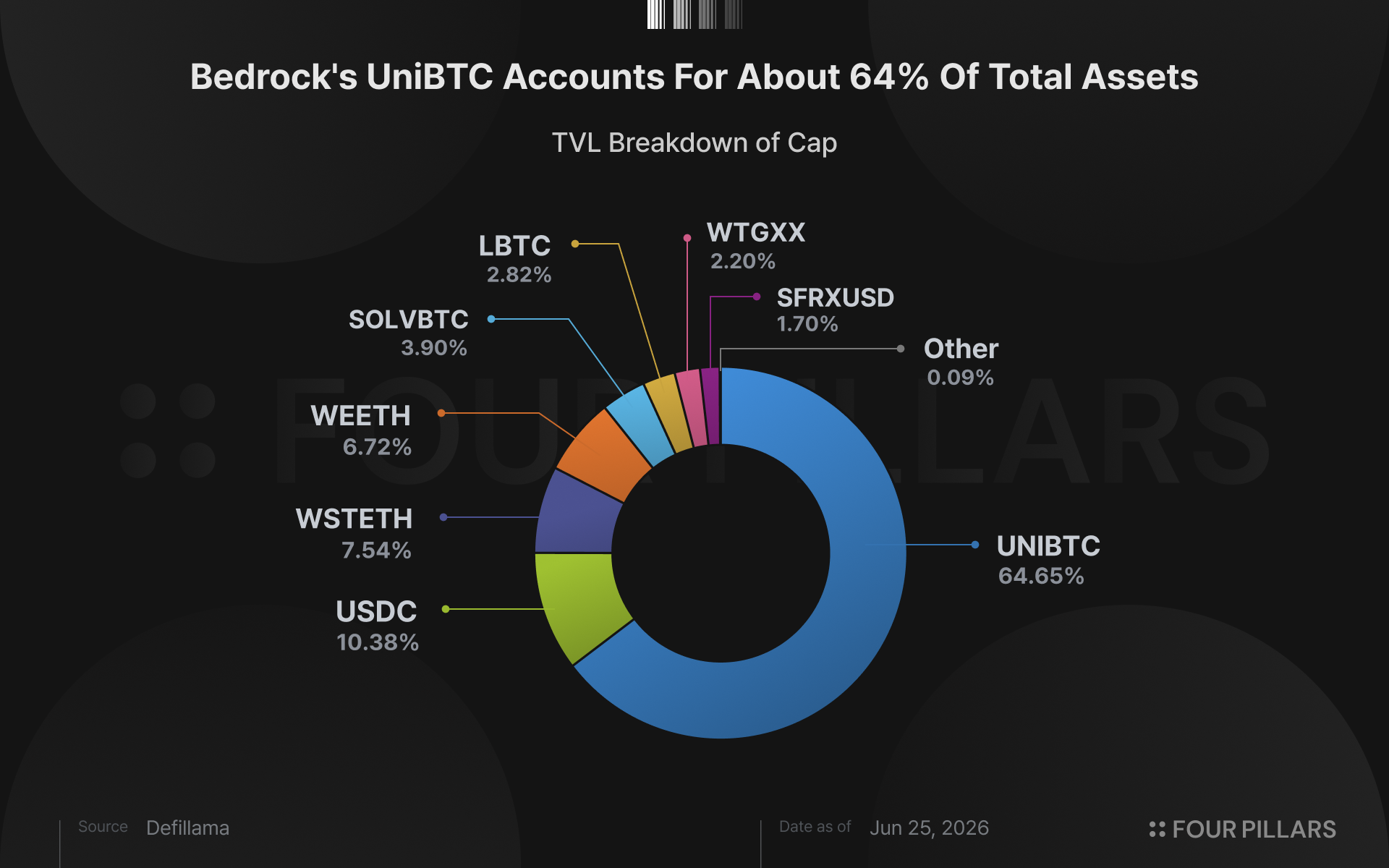

The concentration in Bitcoin-class assets is especially pronounced. Bedrock's uniBTC alone now accounts for about 64 percent of total value locked, so it is no exaggeration to say that Cap's asset composition effectively stands on Bitcoin collateral. The underwriting collateral that swelled quickly after March saw its valuation fluctuate along with crypto prices once those prices pulled back. Cap's lending business has settled in steadily, but the total value locked figure itself is taking on a form that is increasingly sensitive to crypto prices. As swings in collateral prices push up liquidation pressure as well, the risk from collateral-asset volatility is moving into actual territory.

3.3 The Shift in Yield Sources and the Paradox of Capital Efficiency

Cap's revenue is broadly divided into two parts: the base yield (DeFi yield) that idle reserves earn in external lending markets such as Aave and Morpho, and the borrowing interest that borrowers pay after borrowing reserves to execute strategies.

The important point is that the relative weight of revenue from DeFi yield versus borrowing interest is reversing. According to DefiLlama's profit-and-loss data, in the fourth quarter of 2025 DeFi yield was about 1.36 million dollars out of total revenue of roughly 2.86 million dollars, larger than borrowing interest (about 1.13 million dollars), and in the first quarter of 2026 DeFi yield (about 1.61 million dollars) was again the largest line item. In the figures for the second quarter of 2026 so far, however, borrowing interest reached about 600 thousand dollars out of total revenue of roughly 1.17 million dollars, surpassing DeFi yield (about 407 thousand dollars) for the first time.

This trend matters because the differentiation Cap claims lies precisely on the borrowing-interest side. Idle reserve yield is something other yield-bearing stablecoins can access too, but the credit spread that links borrowers, underwriters, and depositors only grows when Cap's structure is actually working. The fact that the first quarter's surge in borrowing showed up as a reversal in revenue composition only in the second quarter suggests that Cap's credit structure is only now revealing itself in the revenue.

A metric that is easy to misread here is protocol revenue. By DefiLlama's measure, Cap's 30-day fees come to about 420 thousand dollars, or roughly 8.07 million dollars annualized, but 30-day protocol revenue is only about 4,400 dollars, or roughly 53 thousand dollars annualized. This is because Cap passes its earnings through to stcUSD holders and underwriters rather than taking the revenue for itself. Looking only at the usual protocol-revenue metric makes it easy to undervalue Cap, but one needs to recognize that Cap's core metrics are not simple revenue but active loans, underwriting capital, borrower diversity, collateral buffers, and the composition of yield sources.

Finally, consider the utilization rates of reserves and underwriting capital. For dollar reserves, the utilization rate that stood at 5.3% six months ago has now risen to about 60%, meaning the idle buffer capital available for immediate repayment has thinned to that degree. Borrowing, meanwhile, amounts to only about 20% of underwriting capital, so underwriting capital is about 4.8 times the borrowed amount. From a safety standpoint the collateral buffer can be seen as thick, but from a capital-efficiency standpoint it also means underwriting capital is not being fully used. Cap's next bottleneck is likely to be not the supply of funds but creditworthy borrowing demand worth the risk that this underwriting capital is willing to bear.

3.4 What Matters More Than Yield

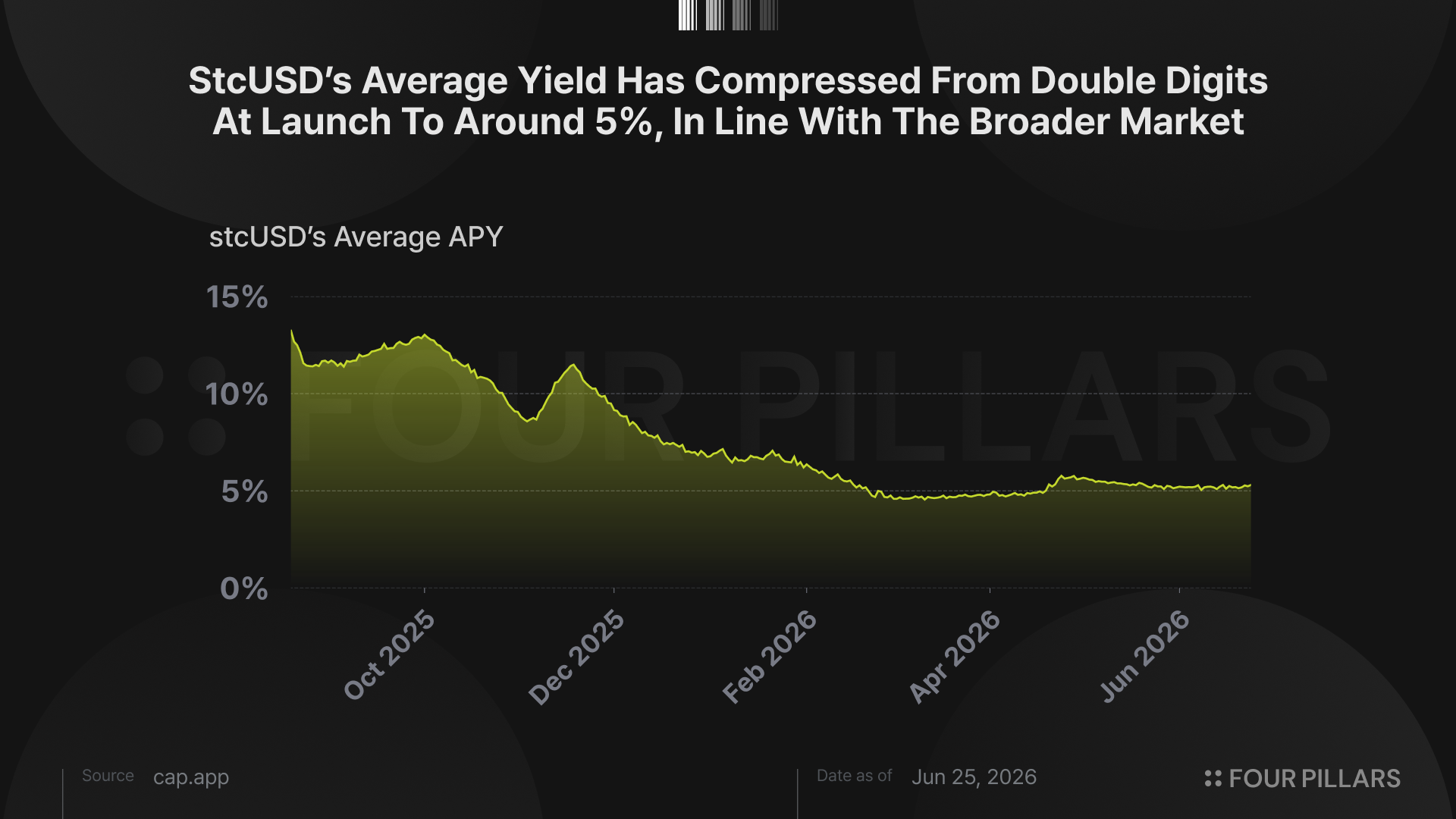

Looking at stcUSD's yield in isolation, Cap's yield is steadily declining. The stcUSD annual yield, which was about 8.6% at the time of the first article, currently sits at about 4.56%, holding at roughly 5.13% on a 30-day average. But the absolute figure alone cannot be the basis for discussing Cap's performance, because yields across DeFi as a whole compressed over the same period.

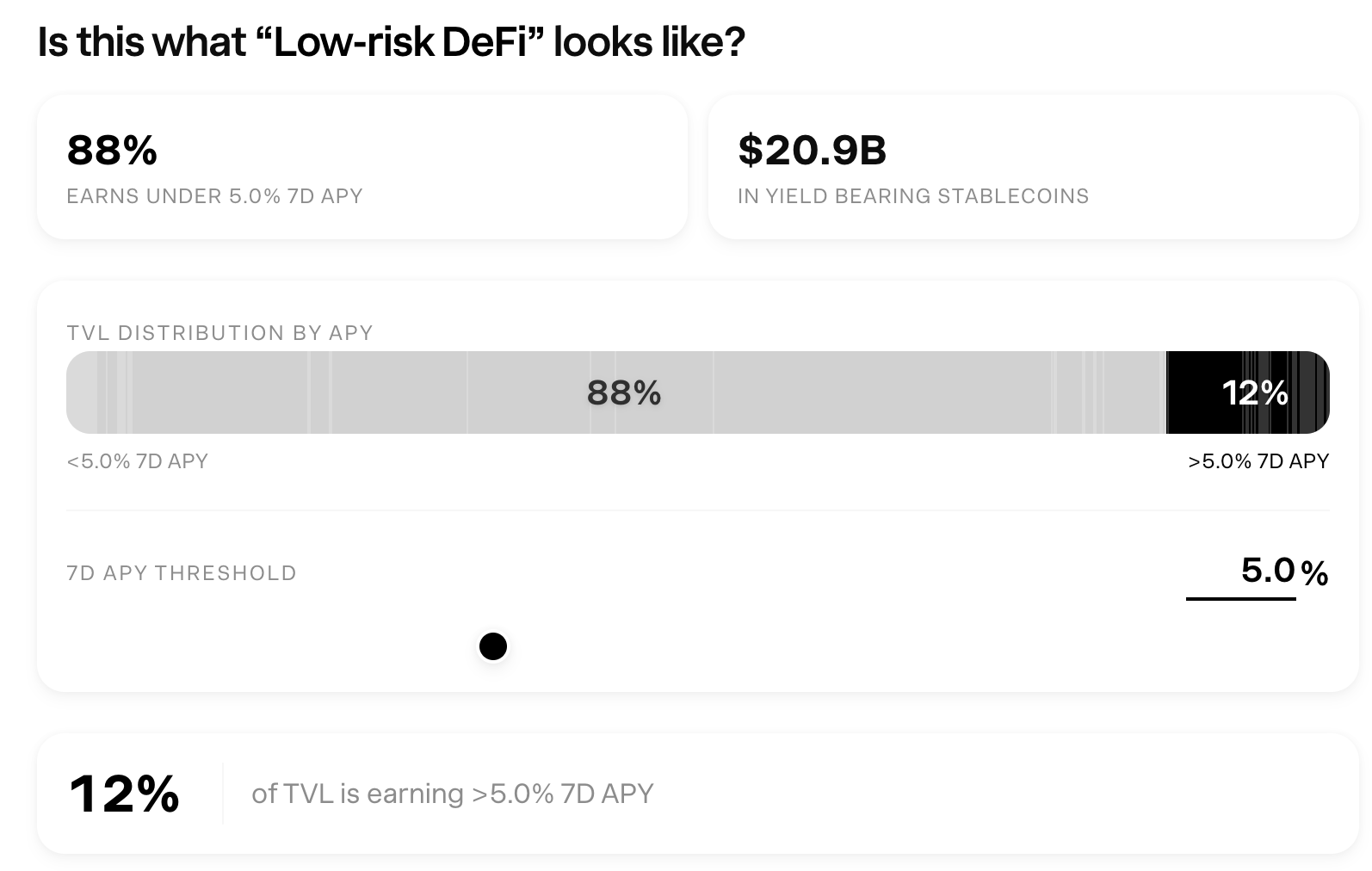

Source: stablewatch

According to data compiled by stablewatch, as of May 8, 2026, 88% of roughly 20.7 billion dollars in yield-bearing stablecoins sat below a 5% 7-day annualized yield. stcUSD is not a high-risk market chasing double-digit yields; it sits near the boundary of a market that aims to deliver dollar yield between 3% and 6% in a more transparent and predictable way. In this kind of low-risk DeFi market, who absorbs the loss first when a loss occurs matters more than an extra percentage point of yield. What matters more than temporary swings in Cap's yield is whether, when producing the same level of dollar yield, one can distinguish where that yield came from among idle reserves, external lending markets, institutional borrowing interest, and underwriter fees. If Cap is truly verifiable finance, the composition of the sources of its yield should be more important data than the annual yield number.

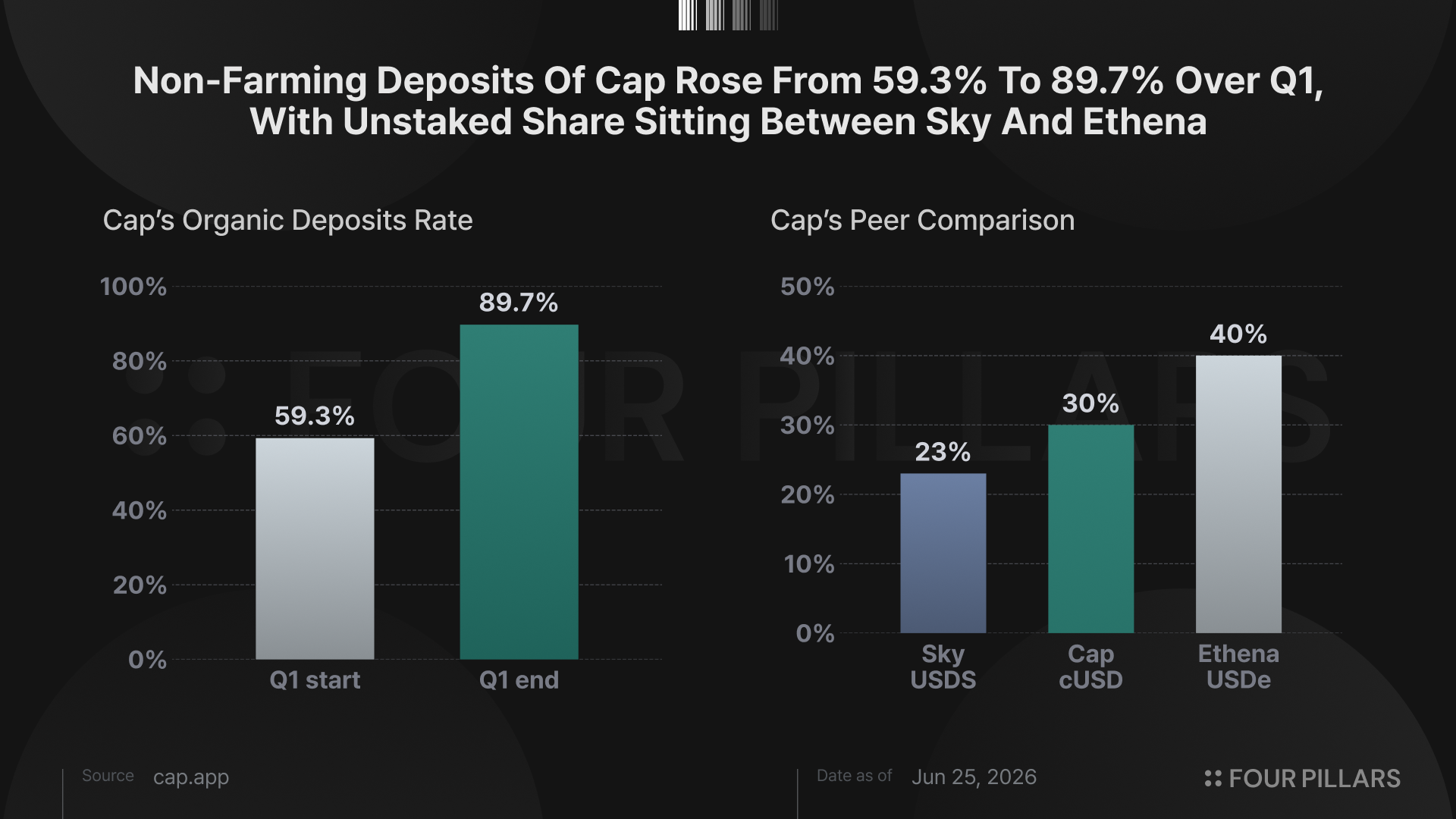

The character of the deposits points in the same direction. After farming capital temporarily exited in March, Cap chose to improve the quality of its deposits rather than force a recovery of the lost amount.

According to figures Cap reported in its investor update article, the share of funds that came in for actual use rather than reward mining (non-farming deposits) rose from 59.3% to 89.7% over the course of the first quarter. The TVL expressed as a size declined, but what remained within it was more stable capital.

4. Cap's Final Component, $CAP

One of the biggest unresolved tasks at Cap that I pointed out in the previous article was that running the project depended entirely on the team's discretion. Core parameters such as which assets to hold in reserves, which collateral could be used for underwriting, and where to set liquidation thresholds were left to the team's judgment rather than to code. $CAP is the token designed to fill exactly this gap. The total supply is fixed at 10 billion tokens, and token holders exercise voting rights over the protocol's core decisions, such as the following.

- Assets to include in or remove from the cUSD reserves

- Adding and removing collateral assets eligible for underwriting

- Liquidation thresholds for approved collateral

- The cUSD issuance fee

- The whitelist of institutions that may act as borrowers in the private credit market

- The maximum guarantee limit for surety exposure

In other words, $CAP exists to move the levers the team had been holding into token governance. It can be seen as the point at which Cap's promise of verifiable finance extends toward disclosing even who changes the protocol's rules and by what process. In addition, Cap allows the revenue the protocol earns to be used for discretionary token buybacks, tying the token's value to actual business results.

The most distinctive choice in the incentive design surrounding the token was the Stabledrop. The Frontier program covered in the first article transitioned at the end of January into the second incentive program, the Homestead program, which promised participants a reward distribution of about 12 million dollars. The decisive difference from a typical token airdrop was that the tokens promised as rewards were cUSD, a stablecoin, rather than $CAP.

This choice resolves two problems at once. First, it removed the initial selling pressure that arises from an airdrop conducted at the same time as a token generation event. In effect, it cleanly separated the early price formation of $CAP from the liquidation of rewards. At the same time, it hands participants real value that can immediately be redeposited into stcUSD and the like, so the incentive works for both the project and the airdrop recipients.

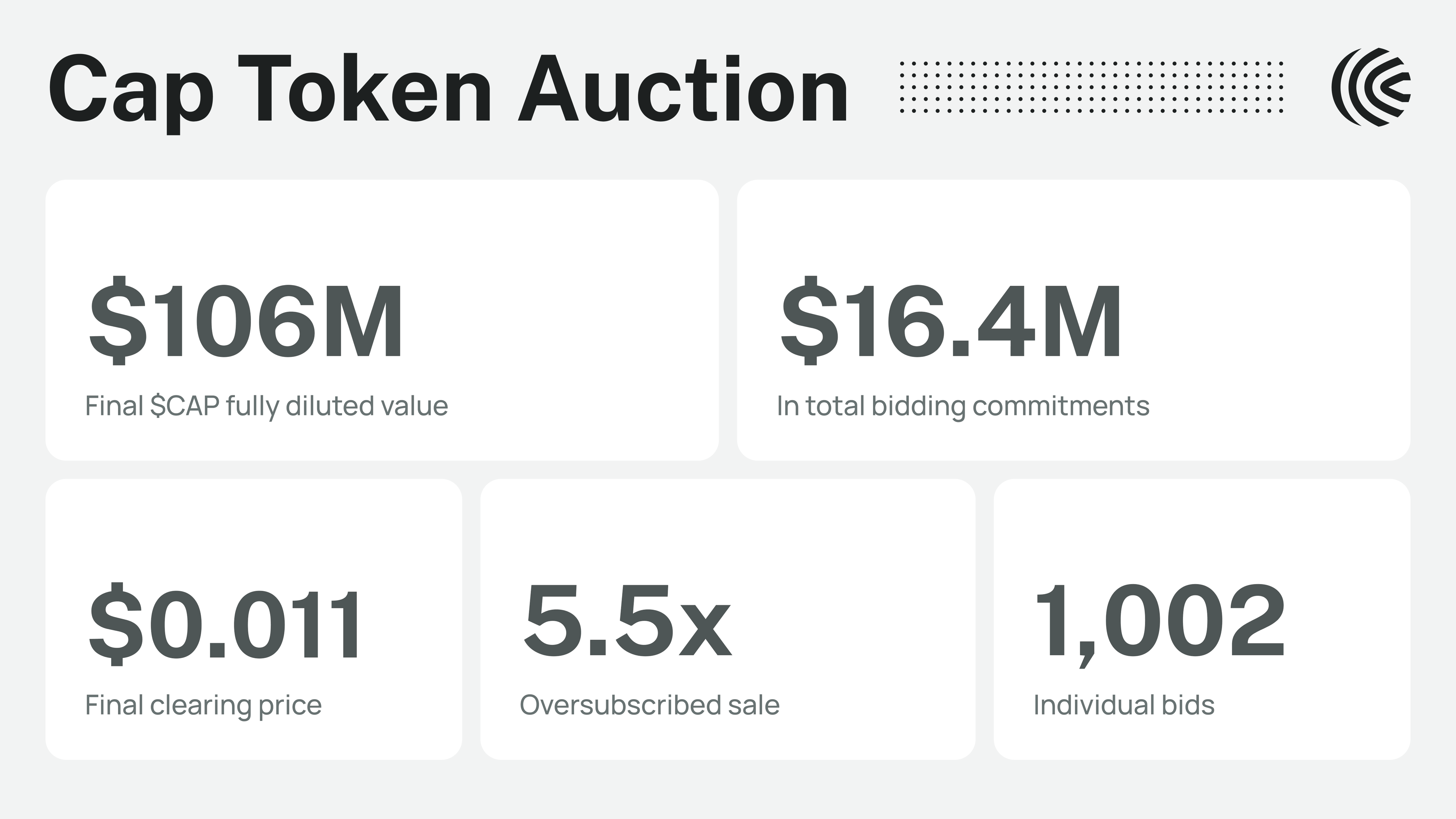

$CAP was sold to the public from June 13 to 18 through Uniswap's Continuous Clearing Auction (CCA). A CCA is a mechanism that generalizes a uniform-price auction into continuous time; auctions proceed block by block, a clearing price is set for each block, and price is discovered gradually according to demand. Because the sale supply is released in portions over time, last-minute sniping and gas-fee competition are neutralized, and participants compete on valuation rather than speed. When the auction ends, liquidity is automatically supplied to a Uniswap v4 pool at the discovered price, so a market price and liquidity are in place from the first day of trading. Cap's auction was run as a "Verified Auction" that combined 0xPredicate's verification module, handling the confirmation of eligibility onchain.

Source: Cap

In the end, the $CAP sale closed at about 106 million dollars on a FDV basis, gathering roughly 16.4 million dollars in bid commitments across 1,002 individual bids for a 5.5 times oversubscription. Cap's decision to conduct the token sale through a Uniswap CCA can also be read as an attempt to find as fair a value as possible for the token and thereby dampen early selling pressure.

5. Looking Ahead

Cap is passing one by one through major milestones: the institutionalization of underwriters, the reversal in reserve composition, the end of the early incentive program, and the launch of $CAP. Yet these achievements have not so much made Cap safer as changed the character of the risk Cap carries. As the tasks pointed out in the first article were resolved, the risk shifted from potential to actual, and the stage of verification likewise moved from design and documents to real market stress. For me, the questions that remain for Cap are as follows.

5.1 The Shift in Risk and the Paradox of Slashing

The fact that self-delegation and low utilization have been resolved does not mean Cap has become safer. A rise in utilization from 5.3% to 60% means the idle buffer available for immediate repayment has thinned, and as underwriting collateral became the large pillar of total deposited assets, the volatility of liquidation pressure tied to ETH and BTC prices grew. The items the first article identified as liquidity risk and fractional reserve risk remained merely potential while utilization was low, but they have now turned into actual risk. The stress tests Cap faces going forward will take place on top of a thinner buffer of capital.

In addition, while slashing is an event the protocol wants to avoid, from an analyst's perspective it is in fact the event that can best verify Cap's structure. So far, Cap's underwriting structure has been assessed mainly through design, documents, and limited operational data. But how slashing executes in an actual default or collateral collapse, how much loss is passed to whom, and how cUSD and stcUSD holders are affected have not yet been sufficiently observed. Whether Cap's loss-absorption structure moves as designed will ultimately be verified during a phase in which collateral prices fall sharply, and if it successfully holds its defense, this will remain a highly meaningful track record for Cap.

5.2 Cap's Competitiveness Will Come From Risk Disclosure, Rather than Yield

The last question that remains is what Cap needs to show next. Right now, underwriting capital is far larger than the borrowed amount. Good underwriting capital has been gathered, but if there are not enough borrowers worth the risk that capital is willing to bear, Cap's revenue structure could drift back toward idle reserve yield. So what Cap needs to show next is not "how many institutions have come in" but "whether different prices are being attached to different borrowers." In a credit market, the rate each borrower receives differs. If underwriters are actually pricing risk, Cap's data should show a dispersion of rates across borrowers, differences in premiums across underwriters, and differences in recognized value across collateral types.

On this point, the data Cap would do well to publish going forward is not a TVL chart. It is more important to bundle, almost like a disclosure document, each borrower's loan balance, underwriting capital, collateral type, loan-to-value ratio, interest rate, maturity, repayment history, liquidation threshold, and yield-source composition. In addition, the launch of $CAP has made governance another point to watch closely. The $CAP token is a unit of authority that can influence items such as the collateral list, borrower approval, fees, and liquidation parameters, while at the same time these are items for which regulated institutional underwriters and borrowers require predictability. If a token vote can change eligible collateral or borrower qualifications, participants bound by legal contracts, such as large institutions, will find that uncertainty hard to accept. How to reconcile the demand for decentralization with institutions' demand for predictability appears to be the most delicate task Cap must solve.

In the end, the question to ask of Cap is not "is it safe" but "can users know in advance who bears the loss under what conditions." Every financial product is safe under certain conditions and risky under others. If the first article called Cap verifiable finance, then half a year later Cap has taken a few steps in that direction. Now it is time for Cap to prove its competitiveness as a credit market, and the next stage of that competitiveness will come not from more deposits or higher yields but from better risk disclosure.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.