Table of Contents

- 1. Polls (Oh: 23¢)

- 2. Exit poll projects Jeong ahead (Oh: 3¢)

- 3. The vote gap widens between Jeong and Oh (Oh: 0.8¢)

- 4. A changed trend, the gap narrows as counting continues (Oh: 71¢)

- 5. A close race, followed by Oh’s final reversal (Oh: 100¢)

- 6. The underlying factor behind the reversal: Counting order

- 7. The factor that amplified the reversal: The price structure

- 8. Conclusion: The appeal of a binary structure and the remaining inefficiency

Researcher

Related Projects

Polymarket is a platform with growing regulatory risk in Korea because of questions over whether it constitutes gambling. Since there have been reports that the Korea Communications Standards Commission is reviewing possible gambling-related violations, as well as reports of investigations into domestic users, this article does not recommend Polymarket as an investment vehicle. It is a retrospective review of how election information was reflected in prices.

In the 9th nationwide simultaneous local elections held on June 3, 2026, public attention naturally turned to the Seoul mayoral race, the largest battleground.

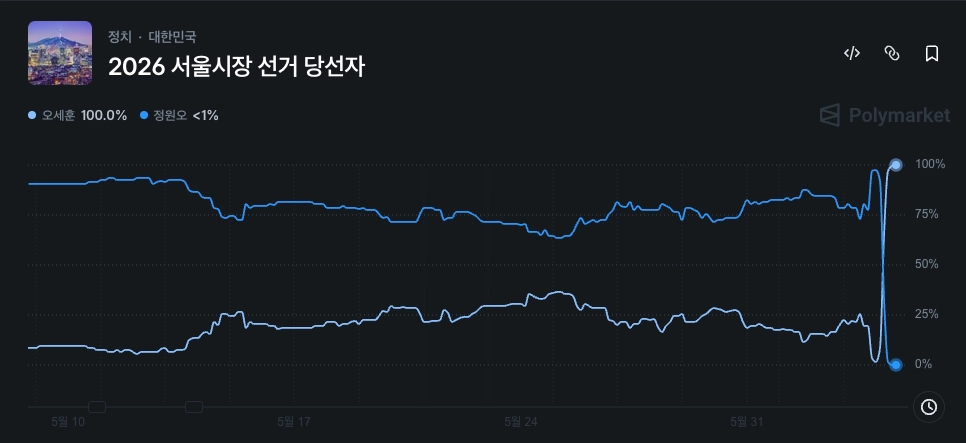

Source: Polymarket

The most volatile graph that day did not come from election-night broadcasts. It came from Polymarket, the global prediction market. Prices moved sharply as the market responded to forecasts that diverged from the exit poll and to the vote count as it unfolded.

Although access to Polymarket is legally blocked in Korea, prediction markets with large trading volumes have been cited by Korean media as useful secondary indicators because they can reflect public information quickly.

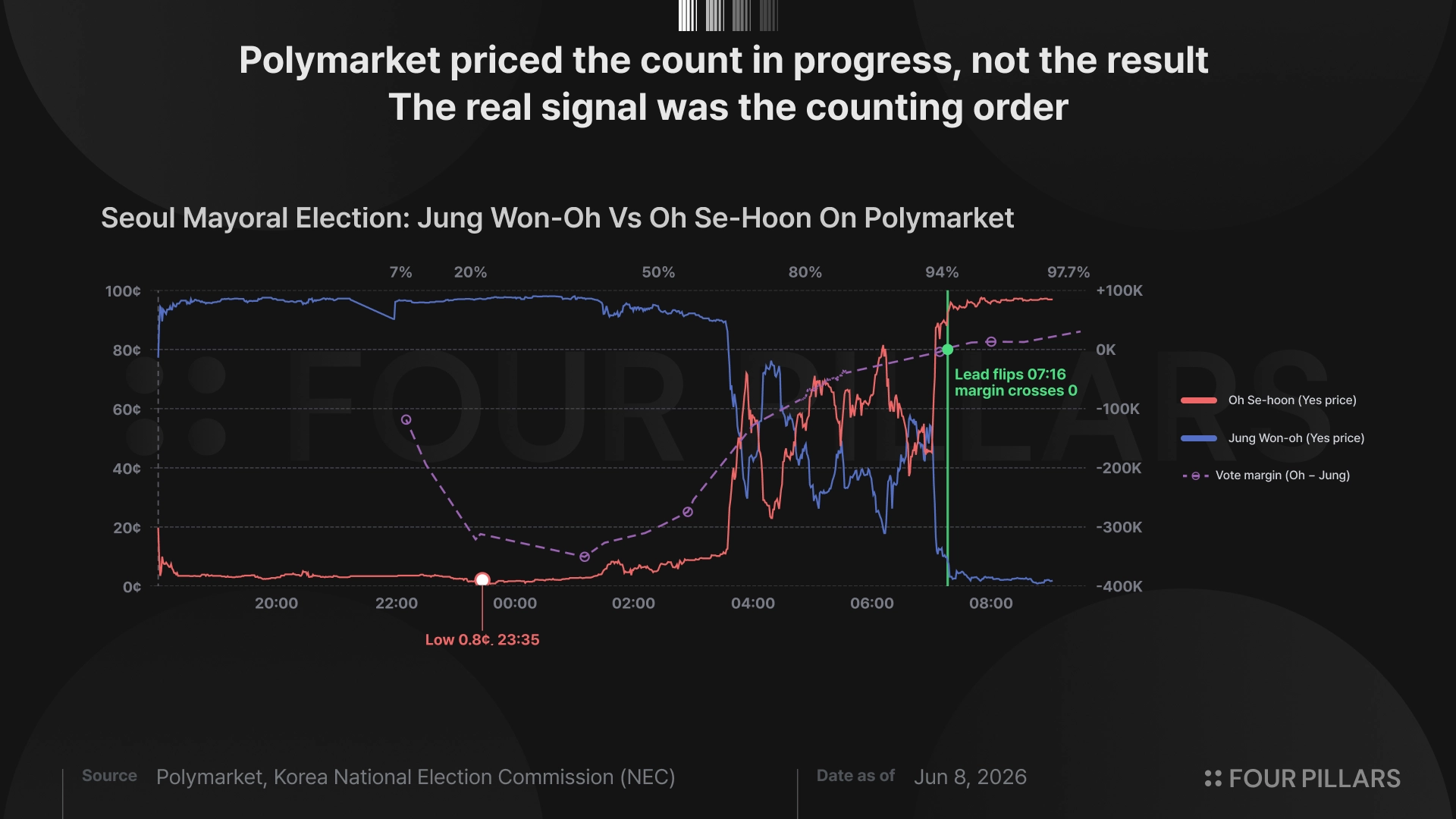

At the time, total trading volume in the Seoul mayoral market exceeded $52 million. With global attention on the race, the price of Candidate Oh Se-hoon’s winning token once fell to 0.8¢, which implied that the market was close to pricing in his defeat. Yet the market reversed sharply in the later stages of the count and eventually closed at 100¢.

This article follows the path of the price as it changed over time and analyzes which variables and pieces of information created such an extreme swing.

1. Polls (Oh: 23¢)

Based only on the published polling trend, Candidate Jeong Won-oh was ahead. By the final stage of the campaign, however, the gap had narrowed. In a poll released on May 28, Jeong recorded 41% and Oh recorded 37%, which placed the race within the margin of error.

Polymarket reflected this trend to some extent. Jeong was ahead, but Oh’s chance of a reversal had not disappeared. The price of Oh’s winning token stood at around 23¢. The market saw Oh as the weaker candidate, while still leaving room for the race to turn.

2. Exit poll projects Jeong ahead (Oh: 3¢)

The joint exit poll by the three major broadcasters, released after regular voting ended at 6 p.m., was much more one-sided than the market had expected. Jeong was projected at 51.4% and Oh at 46.0%. Unlike the close race shown in the final polls, the exit poll pointed to a stable lead for Jeong.

The price reflected the news immediately. Oh’s winning token fell from around 23¢ to about 3.5¢, a decline of roughly 85%. The market treated the exit poll as the main piece of information, and Oh’s chance of a comeback was priced low.

3. The vote gap widens between Jeong and Oh (Oh: 0.8¢)

After the count began, the early trend still favored Jeong. At 10:10 p.m., when about 7% of ballots had been counted, the gap between the two candidates had widened to roughly 118,000 votes. At 1:10 a.m., when the counting rate had risen to around 34%, the gap had expanded to about 350,000 votes.

Around 11:30 p.m., the price of Oh’s winning token plunged to 0.8¢. Polymarket was effectively treating Oh’s defeat as a near certainty.

4. A changed trend, the gap narrows as counting continues (Oh: 71¢)

This trend continued for some time, but after 1 a.m., the gap between Jeong and Oh began to narrow quickly as counting progressed.

At around 4 a.m., as the counting rate approached 69.93%, Jeong had 1,844,874 votes and Oh had 1,717,382 votes. The gap had narrowed sharply to 127,492 votes. Considering that the gap had been about 350,000 votes three hours earlier, the direction of the race had changed.

Oh’s winning token rose almost vertically to 71¢, and expectations of his victory grew.

5. A close race, followed by Oh’s final reversal (Oh: 100¢)

The market then entered another volatile phase. As the actual vote gap narrowed to a close margin, Oh’s token price moved between 42¢ and 67¢ from 4 a.m. to 7 a.m. Even a small change in the vote gap was enough to shift the market’s judgment.

After 7 a.m., the race moved in Oh’s direction. About 13 hours after counting began, shortly after 7 a.m. on June 4, Oh began to move ahead of Jeong. As the count continued, Oh’s lead became firmer. At 7:16 a.m., when the counting rate reached about 94%, Oh led Jeong by roughly 2,000 votes, and the token quickly broke above 90¢ to 95¢. When the gap widened to around 30,000 votes and Oh’s fifth-term victory became effectively certain, the price converged to 100¢.

6. The underlying factor behind the reversal: Counting order

Why did this price movement occur? The answer lies in the difference between the voting patterns of early voting and election-day voting, and in the order in which ballot boxes were counted.

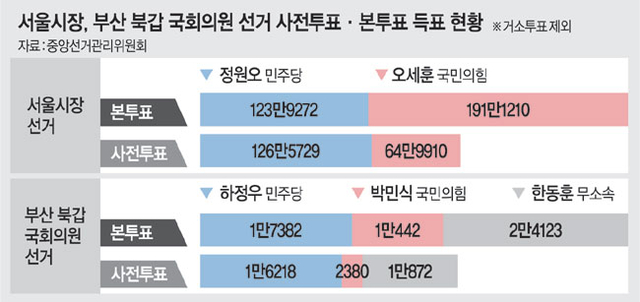

Source : The Munhwa Ilbo

In this Seoul mayoral election, early voting and election-day voting showed very different patterns by candidate. Jeong received 1,265,729 early votes, while Oh received 649,910. In election-day voting, by contrast, Jeong received 1,239,272 votes and Oh received 1,911,210. Early voting clearly favored Jeong, while election-day voting clearly favored Oh.

The important point is that these votes were not mixed and counted all at once. Due to the structural nature of South Korea's vote-counting system, many districts in this election once again saw early voting ballot boxes transported and counted first. As a result, votes favorable to Jeong were reflected early, while election-day votes favorable to Oh were reflected later in both prices and the counting rate.

The late counting in the three Gangnam districts, which lean conservative, also affected the final phase. This was especially true for Songpa District, which has many voters. Songpa’s count continued until late because of the controversy over a shortage of ballot papers, and this affected Oh’s late reversal and the consolidation of his lead.

For reference, anyone could check the real-time counting rates and vote tallies for all 25 districts of Seoul through the National Election Commission.

In brief, votes favorable to Jeong appeared first, and votes favorable to Oh appeared later. The market overread the early information as if it represented the entire electorate. As a result, Oh’s price fell too far, down to 0.8¢.

7. The factor that amplified the reversal: The price structure

If counting order created the reversal in the real vote count, the prediction market’s price structure turned that change into an extreme swing from 0.8¢ to 100¢. Two effects worked together.

The first was non-linearity. On Polymarket, a token price is generally interpreted as the market’s implied probability of the outcome. A price of 100¢ means that the market sees the outcome as almost certain.

The relationship between vote margin and probability of victory, however, is not a straight line. When one candidate is far ahead, a small narrowing of the vote gap does not move the probability of victory very much. When the race becomes close, by contrast, even a small change in the vote gap can move the probability sharply. In election models, this relationship often appears as a sigmoid curve.

The market also carried an implicit assumption. If many participants assumed that “the remaining votes will look similar to the votes counted so far,” then Jeong’s early 350,000-vote lead would appear to mean a likely Jeong victory. Under that assumption, Oh’s 0.8¢ price was not entirely irrational. The problem was that the assumption did not adequately account for counting order, which was the missing variable.

The second effect was variance collapse. Early in the count, many votes remain, so the chance of a reversal is also larger. As counting proceeds, the number of remaining votes falls, and uncertainty declines quickly. When the vote gap approaches zero while uncertainty is shrinking, one small change can push prices toward either extreme.

The price movement between 42¢ and 67¢ from 4 a.m. to 7 a.m. showed this dynamic clearly. The number of remaining votes was falling, the vote gap was narrowing, and the market was incorporating new counting data almost immediately. Once the actual vote count reversed, the price quickly moved close to 100¢.

In the end, counting order created the illusion of a Jeong victory, and the market’s price structure, shaped by non-linearity and variance collapse, amplified that illusion into a large price swing.

8. Conclusion: The appeal of a binary structure and the remaining inefficiency

This article is, of course, a retrospective analysis that looks back at the price path after the result is known. Such analysis should be careful not to label past prices as inefficient too easily simply because the final outcome is now known.

I do not think this case falls into that category. The counting order that most market participants missed was not future information. It was information that already existed at the time. Calling the 0.8¢ price inefficient is therefore not just hindsight. It is closer to a case in which existing information was underreflected in the price.

This type of inefficiency is unlikely to end as a one-off case. More events will be traded through prediction-market prices, and in each case, information will enter the market asymmetrically and sequentially. For that reason, the claim that “prices contain all information” does not need to be accepted without question.

In the Seoul mayoral election, the price was honest. It was not complete. The price existed only within the information held by market participants and the assumptions they made. What they missed was context outside the market: the order of the count.

Prediction markets are powerful tools. They are not perfect oracles. As important as what the price says is the ability to read which variables the price has not yet taken into account.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.