Researcher

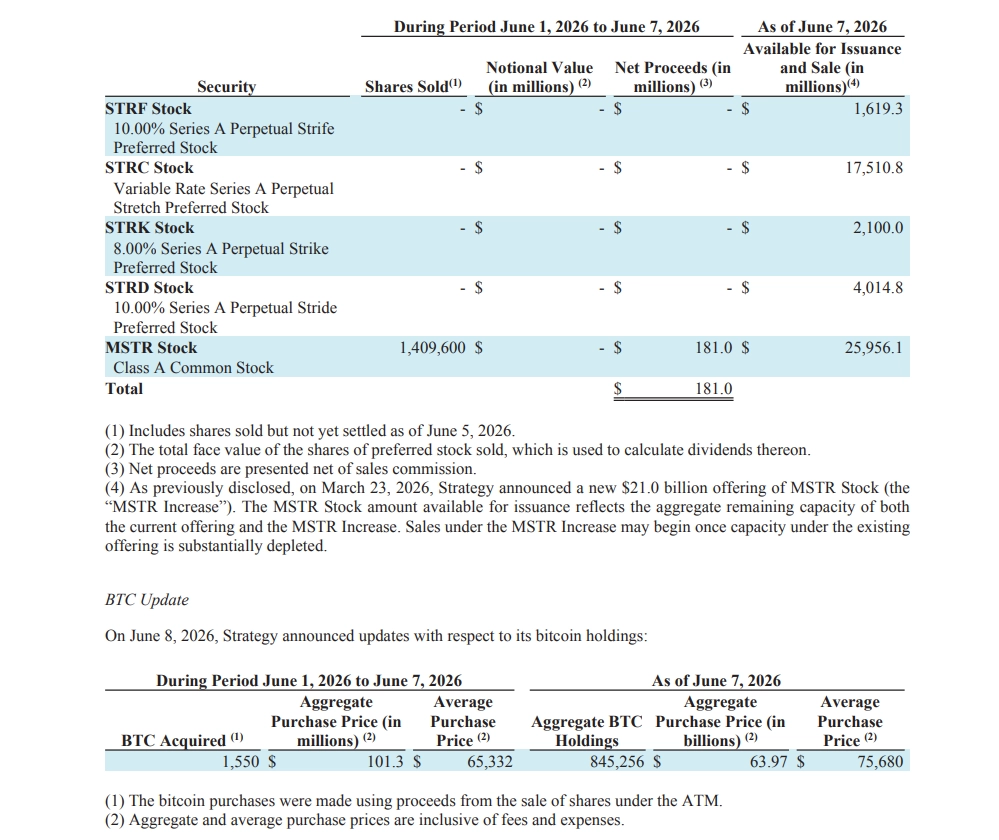

Saylor sold 32 BTC, then turned around and bought 1,550 BTC today.

I don’t want MSTR to fail. But someone has to say it.

This was one of the worst trades.

On the surface, it looks like an amazing trade.

Strategy bought a massive amount of BTC near the lows, and even increased its USD reserve for preferred dividends from $900M to $1B.

Is this the resurrection of Strategy?

If this feels bullish to you, you don’t understand Strategy.

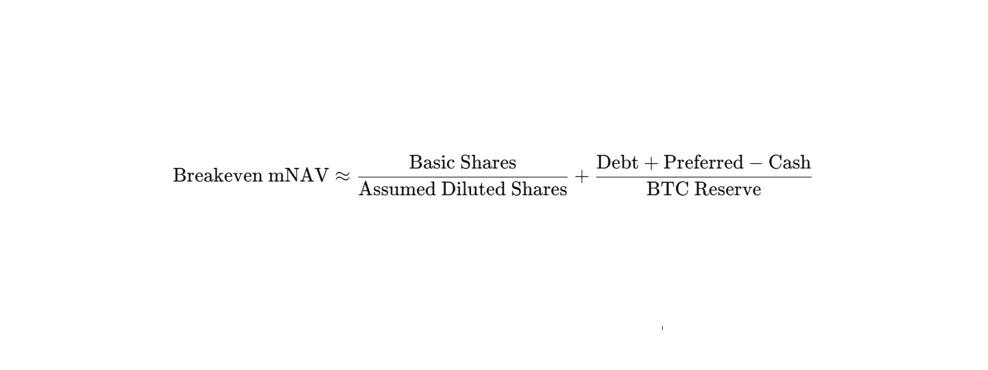

1. You need to understand breakeven mNAV

One of Strategy’s biggest goals is to increase BPS (BTC per share) for MSTR shareholders.

The way to increase BPS is very simple:

Sell common stock at a premium, then use the proceeds to buy BTC.

So how much of a premium does MSTR need for ATM issuance to actually increase BPS?

According to the Q1 2026 earnings call, mNAV needs to be above 1.22.

This is called the “breakeven mNAV.”

The idea starts from a simple condition:

The amount of BTC you can buy by selling 1 share of MSTR must be greater than the existing BTC per MSTR share.

For the full derivation, check my previous post.

But in the end, breakeven mNAV is calculated like this:

And by the way, the current breakeven mNAV is not 1.22 anymore.

Using the numbers before the 1,550 BTC purchase, I get 1.30.

2. The worst trade

Now let’s go back to Strategy’s 1,550 BTC purchase.

Strategy raised $181M through the MSTR ATM offering, then used $101.3M of that to buy 1,550 BTC.

There are two problems here.

- First, the MSTR ATM issuance seems to have happened below 1.30 mNAV. If you sell common stock below breakeven mNAV to buy BTC, you are not increasing BPS. You are decreasing it.

- Second — and this is the important part — not all of the ATM proceeds were used to buy BTC. The whole breakeven mNAV concept assumes that 100% of the capital raised is used to buy BTC. Even if mNAV is high, if only part of the proceeds goes into BTC, the trade can still reduce BPS.

Strategy appears to have added the unused proceeds to its USD reserve.

In other words:

Strategy sacrificed MSTR shareholders’ shares and BPS to support the sustainability of STRC.

In fact, Strategy’s BPS fell by about 0.19% compared to before the trade.

And what did they get for it?

The USD reserve runway increased from roughly 6.3 months to 7 months.

3. Strategy’s gamble

“We are here to drive Bitcoin per share up, and we are doing everything we can to drive Bitcoin per share up.”

That’s what Michael Saylor said on the Q1 2026 earnings call.

But with this trade, Strategy sacrificed MSTR’s BPS for STRC.

Strategy has rolled the dice.

If sacrificing BPS helps flip sentiment, restore STRC’s price, and recover mNAV, then Strategy can keep raising capital through MSTR and STRC ATM offerings.

But what if sentiment doesn’t turn?

Then Strategy may have no choice but to keep sacrificing MSTR.

And in the worst case, it either delays STRC dividends…

or slowly bleeds out.

Pray for BTC, MSTR, and STRC to recover.

Amen.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.