Table of Contents

Researcher

In the current situation, there is no reason for STRC to return to $100.

The original mechanism that was supposed to keep STRC trading near $100 is as follows:

- If STRC’s price is below $100, the dividend yield rises due to the price decline, and Strategy may also raise the nominal dividend rate above 11.5%.

- Since Strategy has the right to buy MSTR at $101 per share, price increases above that level are suppressed.

- If MSTR goes bankrupt, STRC has a claim of $100 per share plus accumulated unpaid dividends.

For STRC to return to $100, the mechanisms above need to work properly.

1. Dividend rate adjustments cannot be a fundamental solution

First, raising the dividend rate is unlikely to be effective for two reasons.

- A higher dividend rate becomes a financial burden for Strategy and may actually worsen its financial condition. From investors’ perspective, a high dividend rate in an unfavorable situation can also act as a negative psychological factor.

- Dividend rate adjustments and payments are not obligations of STRC. They depend on the board’s decision, so there is significant uncertainty from investors’ perspective.

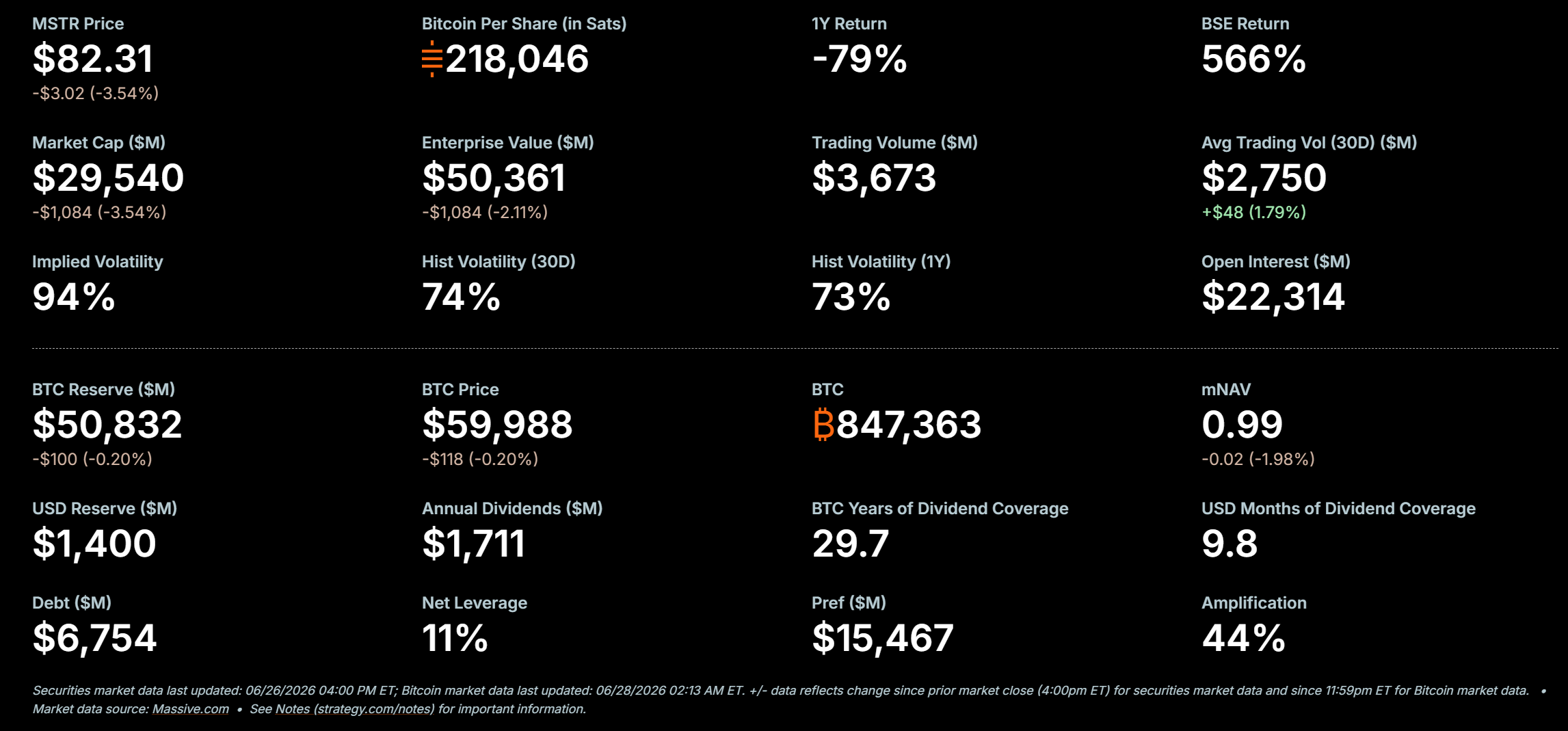

Because STRC pays a fixed dividend per share rather than a dividend proportional to principal, it is a product where dividend investors should not need to worry too much about principal. Even so, it is highly uncertain whether Strategy can continue paying STRC investors dividends at the current level.

Of course, Strategy can currently cover bond interest and preferred stock dividends for 9.8 months using its USD reserves, and for as long as about 30 years by selling the BTC it holds. However, this does not cleanly resolve dividend uncertainty.

The 9.8 months that USD reserves can cover is not a long period at all. To extend that period using USD reserves, Strategy would need to continue issuing MSTR through ATM offerings. But at the current mNAV level, this would inevitably dilute BPS, so it is absolutely not sustainable for Strategy.

Even if USD reserves are depleted and the company extends the life of both Strategy and STRC by selling BTC, that would fundamentally go against the purpose and essence of Strategy as a company. It would reduce the attractiveness of STRC and MSTR as investment products and accelerate a negative feedback loop.

2. Unless there is a redemption, the $100 per share claim is meaningless

If STRC’s price is simply guided through dividend rate adjustments, the $100 figure has no meaning. The fundamental reason STRC can be guided to trade near $100 is that if Strategy goes bankrupt, STRC has a claim on remaining assets equal to $100 per share plus accumulated unpaid dividends.

Put simply, STRC, currently trading at $75, may look like it is being sold at a huge 25% discount from its regular price of $100. Is that really the case?

The key point is that STRC is not a bond. It is preferred stock. Bonds have maturities, so if STRC were a bond, investors could receive $100 per share at maturity. In that case, this level of discount likely would not have occurred.

The only way STRC investors can get their money back, unless Strategy separately announces an STRC buyback, is for Strategy to fail.

There are two problems here.

- Contrary to what the community currently thinks, Strategy cannot easily fail. Strategy’s net leverage ratio is only 11%, and its amplification, which represents the ratio of bonds and preferred stock to its BTC reserves, is only 44%. For the company to truly go bankrupt, its leveraged position from bonds would need to collapse. That would be difficult unless the BTC price falls to 11% of its current level, or about $6,600. Even considering price declines caused by selling, this is unlikely unless BTC approaches around $10K.

- Even if it does go bankrupt, that is still a problem. If Strategy goes bankrupt, it would mean that a leveraged position of only 11% has collapsed. If a situation that severe occurs, preferred stock investors, including STRC holders, who have claims junior to bondholders, would already be in a difficult position to fully receive the remaining assets.

In other words, for STRC investors to receive $100 per share, 1) Strategy must go bankrupt, and 2) if a bankruptcy scenario actually occurs, it will likely be difficult to receive the full $100 per share.

3. STRC has no reason to trade near $100

Strategy set STRC’s dividend rate at 11.50% based on a $100 price. But STRC’s price is determined by the market. The $100 per share claim on remaining assets does not seem very meaningful in a worst-case scenario, and the long-term sustainability of dividend rate adjustments and payments is questionable.

STRC is currently trading at $75. At this price, the effective dividend yield is 15.3% per year. In other words, investors are demanding an additional 3.8% yield compared with the original dividend rate of 11.5%, due to risks such as bankruptcy risk and uncertainty around dividend payments.

If investors believe that a 20% dividend yield is appropriate given STRC’s risks, STRC could trade at $57.5. Since the fair price depends on market uncertainty and investor psychology, no one can know it with certainty.

In the current situation, there is no reason for STRC to trade at $100, and STRC’s price will converge toward the market price investors assign to it.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.