Table of Contents

1. Japan's Tokenized Securities Market: Why Real Estate Came First

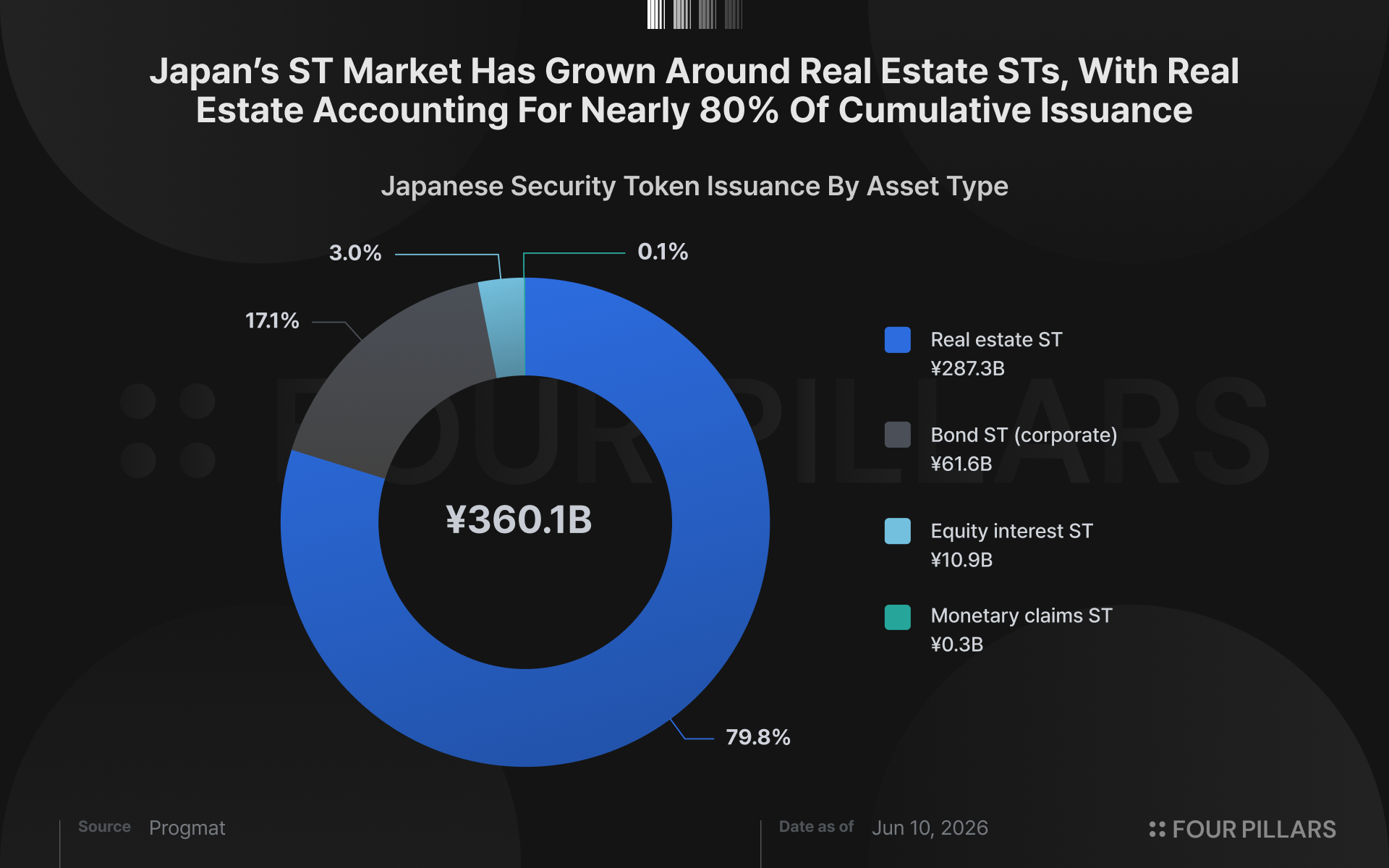

Japanese securities firms have shown intense interest in tokenized stocks recently. Japan's tokenized securities market, since being brought into the regulatory framework through two rounds of Financial Instruments and Exchange Act amendments in 2019 and 2020, has grown primarily around real estate. Three factors explain this concentration.

- An empty space with no established infrastructure to displace: Unlike listed equities, tokenized real estate securities had no central recordkeeping institution like Japan Securities Depository Center (JASDEC) to begin with.

- The product itself was new: Real estate STs combined the liquidity of REITs with the asset-by-asset selection of crowdfunding. They filled a gap in small-ticket real estate investment demand that existing products had not addressed, creating room for the market to grow.

- The regulatory framework aligned: Real estate STs could draw on the existing beneficiary certificate-issuing trust structure, which was already recognized, leaving little legal friction.

Stocks sit on the opposite side of these conditions. Japan Securities Depository Center (JASDEC) already operates as a central infrastructure.

The reason securities firms are still pushing to open the tokenized stock market is that there is unmet demand accumulating inside Japan's stock market that the existing infrastructure cannot absorb.

2. How the Trading Unit Barrier Made Half-Shareholders

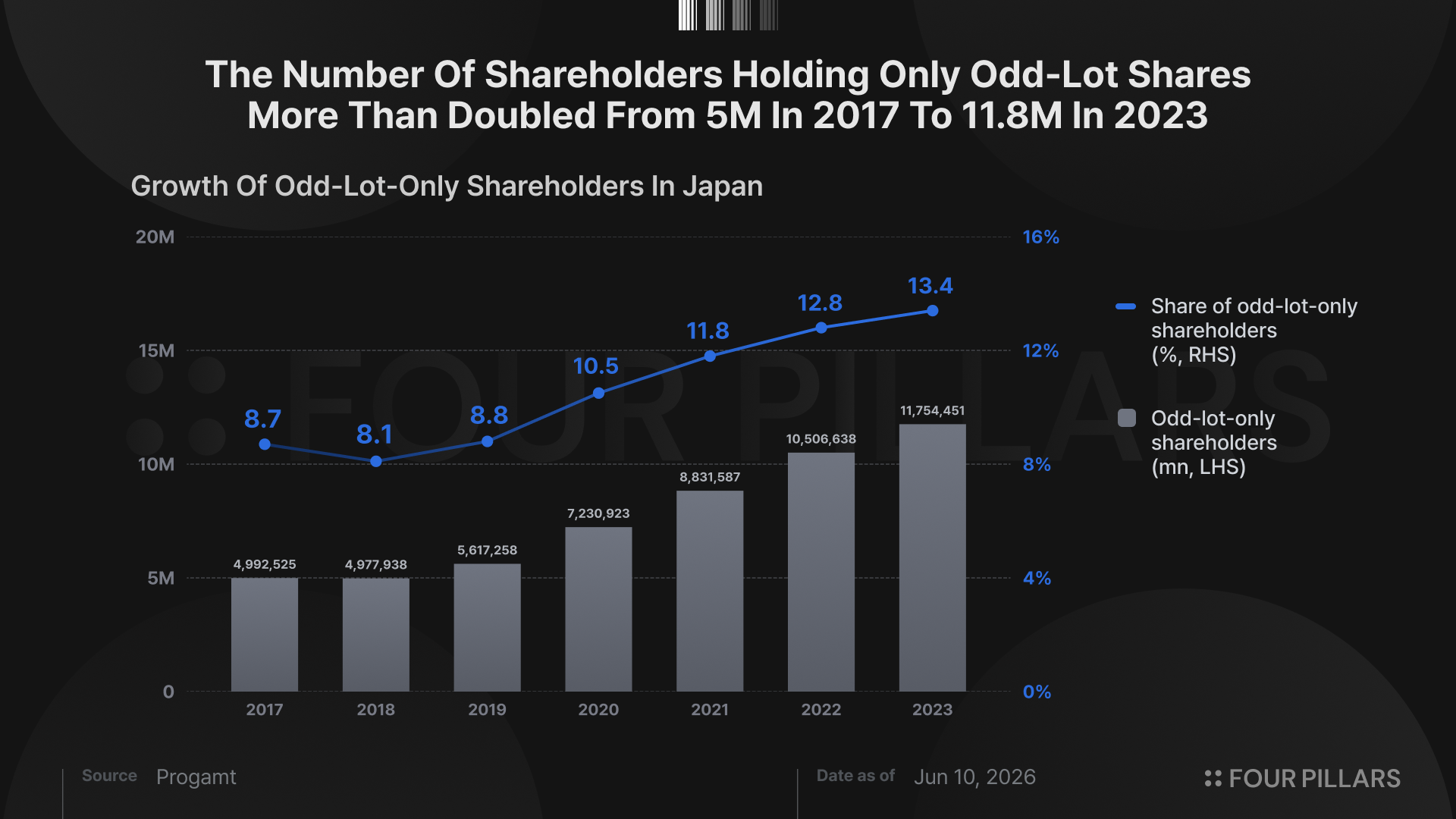

In Japan's stock market, shares are traded in "units" by default. Most listed companies set one unit at 100 shares, and exchange trading is only possible in unit increments.

A stock priced at 50,000 yen requires at least 5 million yen for a single exchange purchase. The median trading unit on the Tokyo Stock Exchange exceeds 130,000 yen, making the entry barrier for Japanese retail investors notably high.

Within these constraints, demand for sub-unit shares, meaning holdings below the 100-share threshold, has risen sharply. The number of holders of sub-unit-only shares grew from roughly 4.99 million in 2017 to about 11.75 million in 2023, a 2.4x increase over six years, with their share of total shareholders climbing from 8.7% to 13.4%.

These trades go through sub-unit share services offered by online brokers. SBI Securities, Monex, and others each operate their own sub-unit programs, but these transactions are OTC arrangements between the broker and the retail investor, not exchange trades. Order hours, eligible securities, and service quality differ from one broker to another.

The problem is that sub-unit shares come with legal restrictions: (1) no voting rights, (2) no exchange trading, and (3) no transferability in principle.

As of 2023, of the approximately 87.85 million total shareholders, 11.75 million (13.4%) held only sub-unit shares. The numbers have grown, but what has grown is a class of half-shareholders who hold no voting rights and cannot sell on the exchange. The share of "voting-rightless shareholders," whose circulation was never contemplated under the Companies Act, rises each year. This is the current state of Japan's stock market.

3. Japan's Securities Industry Tests 1-Yen-Unit Stock Investing

Retail demand is clear, but the infrastructure to absorb it has been missing. Securities firms' interest in tokenized stocks is aimed at opening exactly this empty market.

Recently, the digital asset infrastructure firm Progmat published a report on tokenized stocks. It compiles the findings of a working group that includes Nomura, Mitsubishi UFJ Trust and Banking, and SBI, and its objective is to draft a legislative proposal for the Tokenization Act required to actually issue tokenized stocks.

Stock STs work by placing 100 shares (one trading unit) of a listed company into a trust and issuing the beneficiary rights on a blockchain in units as small as one yen. The same beneficiary certificate-issuing trust structure used for real estate STs and JDRs is reused, with only the underlying asset swapped to stocks. This brings the previous entry barrier of millions of yen down to one yen.

The issuing company participates directly in the tokenization process. Unlike third-party stock-linked tokens that are issued without the issuer's consent, stock STs are bound by contract between the listed company and the trust. As a result, investors holding fractional beneficiary rights still receive proportional dividends and, as deemed shareholders, gain access to shareholder benefits and voting rights.

For property rights to the shares themselves, the report proposes keeping the JASDEC ledger as the legal record while synchronizing trade records on the blockchain. The scope also starts outside the main exchange, beginning with broker OTC transactions and PTS venues rather than exchange floor trading.

4. What Japan's Tokenized Stock Model Suggests

Japan's tokenized stock model is distinctive. Rather than copying global precedents, it is taking shape around domestic retail demand, existing financial infrastructure, and the country's Companies Act, building out a localized model.

Japan's stock ST draws a line against third-party issuance, in which someone creates stock-linked rights without the issuer's consent, and sits closer to the issuer-sponsored camp in that it presumes the issuer's consent.

That does not mean the blockchain becomes the shareholder registry or the token becomes the stock itself. Because unit shares are placed into a beneficiary certificate-issuing trust as an SPV and the beneficiary rights are tokenized, the token holder's legal status is that of a trust beneficiary, not a shareholder. Shareholder rights are exercised indirectly through the trust under deemed-shareholder status.

It also differs from DTCC’s rights tokenization. The DTCC model is closer to recording rights to DTC-held securities on a DLT, whereas Japan places unit shares into a separate legal vessel called a trust and tokenizes the highly fractionalized beneficiary rights.

From the perspective of Asian capital markets, Japan's precedent serves as an important reference point. As Korea is also pursuing STO legislation, markets with deeply institutionalized listed-share trading and a central securities depository structure will find it difficult to import offshore tokenized stock models as is. They are more likely to examine localized models closer to Japan's, built on top of their own securities law frameworks and depository infrastructure.

In the end, Asia's tokenized stock market is more likely to develop as a coexistence of differentiated models, each adapted to its own jurisdiction's legal framework and market structure, rather than as a single standard model unifying the region.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.