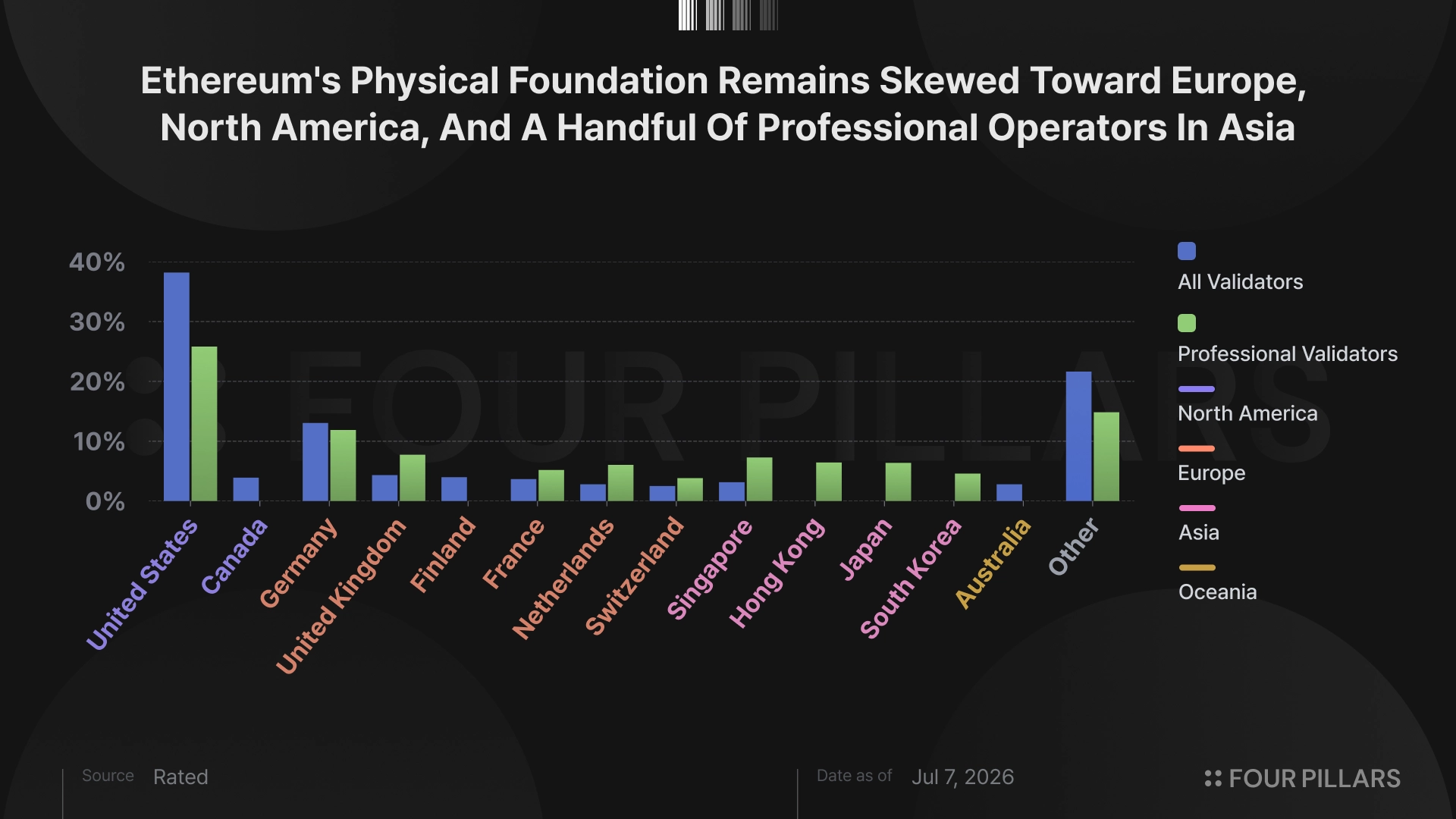

If Ethereum is to truly live up to the name "world computer," its nodes need to be spread across the world. Let's look at the distribution of validator nodes, the physical backbone of the Ethereum network, from two angles. One covers all validators, the other professional operators only.

1. All validators

By the all-validator count, the United States holds 38.19% and Germany 13.04%. Two countries account for more than half of the network. Among the top 10 countries, Singapore (3.15%) is the only Asian entry.

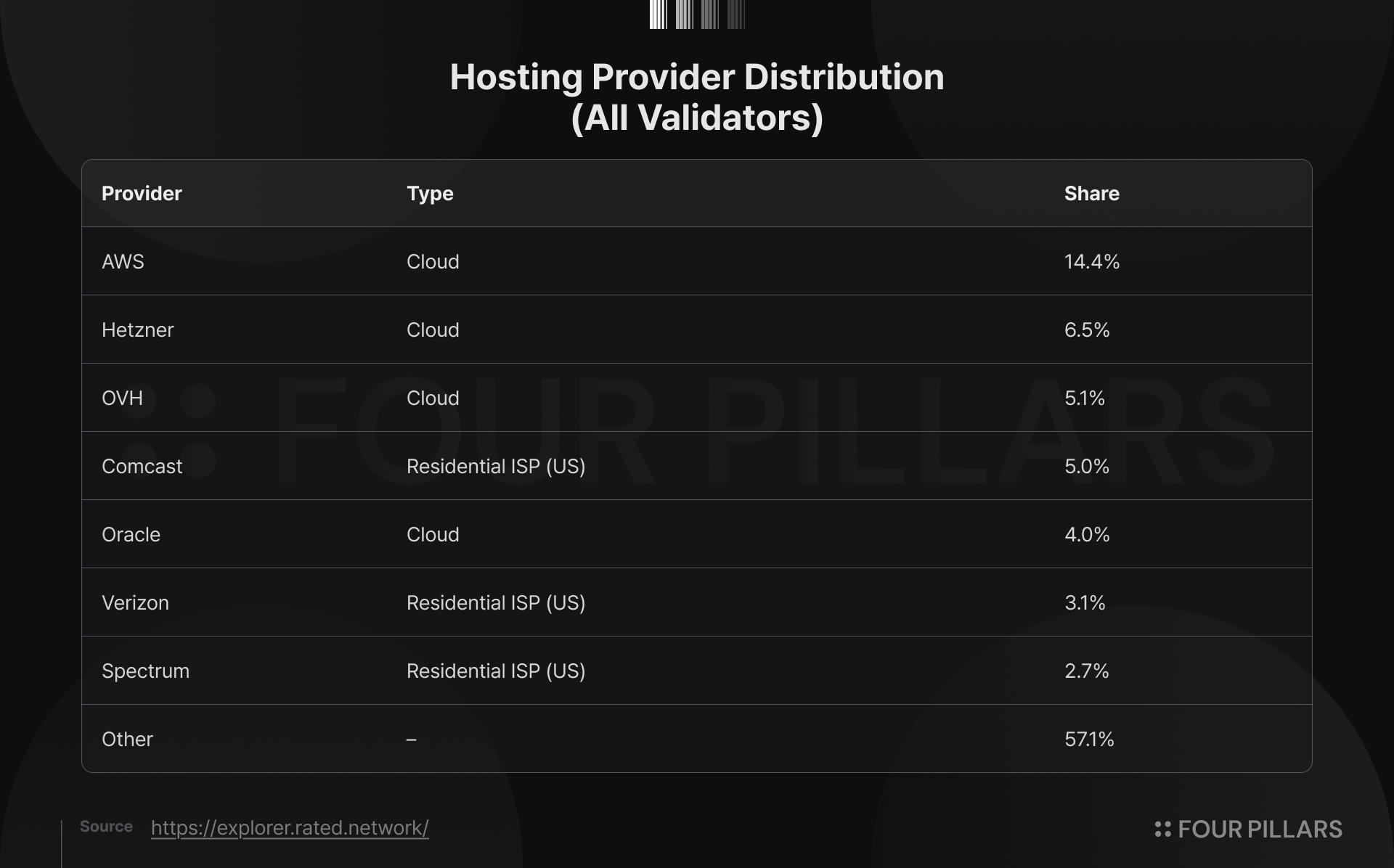

Finland (3.98%) and Canada (3.9%) also make the list, and the likely driver is cloud hosting rather than any particular Ethereum affinity in either country. Germany and Finland host Hetzner regions, and Canada has a large OVH region. Hetzner and OVH are the hosting providers blockchain node operators reach for most. The host distribution backs this up. Hetzner runs 6.5% of all validators and OVH 5.1%.

Another detail stands out in the host distribution for all validators. Comcast holds 5%, Verizon 3.1%, and Spectrum 2.7%. These are US residential ISPs (Internet service providers), which means more than 10% of all validators are home nodes running out of American households, not data centers.

2. Professional validators

The picture changes when you isolate professional validators. The US share drops to 25.81%, and major Asian countries climb. Singapore 7.28%, Hong Kong 6.44%, Japan 6.38%, South Korea 4.59%. Together the four reach about 24.7%. The share of professional validators operating out of Asia has risen to nearly the same level as the US.

This shows that institutional infrastructure is more evenly distributed geographically than the overall validator set. Professional operators face the same conditions as everyone else. The US and Europe are the cheapest, most convenient options. That they placed nodes in Asia anyway, whether to meet institutional clients' jurisdictional requirements or as a latency diversification strategy, shows the Asian deployment is a strategic choice.

3. The problem, and the opportunity

South America, the Middle East, and Africa appear in neither top 10. The Middle East is the notable case among them. Centered on the UAE, regulatory frameworks are taking shape while exchanges, funds, and custody businesses move in, making the region one of the industry's growing hubs. Yet from an infrastructure standpoint, the Middle East remains a periphery. Capital and industry are arriving, but the physical foundation of the network the region relies on still sits in Europe, North America, and Asia.

The P2P layer of Ethereum's consensus structurally disadvantages regions with low node density. A node that receives messages late gets a lower peer score, and a lower score pushes it out of the center of propagation, so it receives messages even later. A vicious cycle. The way to break it is to raise node density within a region. The problem is that conditions aren't cooperating. Large-scale staking by DAT companies and staking ETFs keeps growing around the US, so this gap may widen further.

Then again, this is also an opportunity. If Ethereum truly becomes a settlement layer spanning the globe, a world computer, institutions in each region will look for staking infrastructure that runs within their own jurisdiction. Operators who claim validator infrastructure in the Middle East, South America, or Africa first will likely find themselves with few substitutes at the negotiating table with local institutions. If only a handful of providers in a region can satisfy jurisdictional requirements, regulatory compliance, and latency locally, this becomes a matter of preemption rather than price competition.

The geographic distribution of validators is not a state that holds once achieved. The choices of large operators and the pull of capital can reopen the gap at any time. Decentralization is a verb. Whatever the current state, what matters is that the network keeps its destination clear and keeps making the best choices toward distribution.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.