Table of Contents

1. Hard Times for DATs

In August 2020, Strategy introduced the world’s first DAT strategy. Then, in 2024 and 2025, many DAT companies emerged, including BitMine, Twenty One Capital, Metaplanet, and SharpLink Gaming.

In the early stages, these companies operated in a fairly favorable market environment. They raised capital through common stock ATM offerings, PIPEs, SPACs, and other methods, then used that capital to buy digital assets. By using the flywheel created by the mNAV premium, they tried to acquire more digital assets and increase the number of digital assets per share.

But the world has changed. BTC, which once seemed like it would stay above $100K forever, has fallen below $70K. ETH has also dropped below $2K, and other alt tokens have seen major price declines as well.

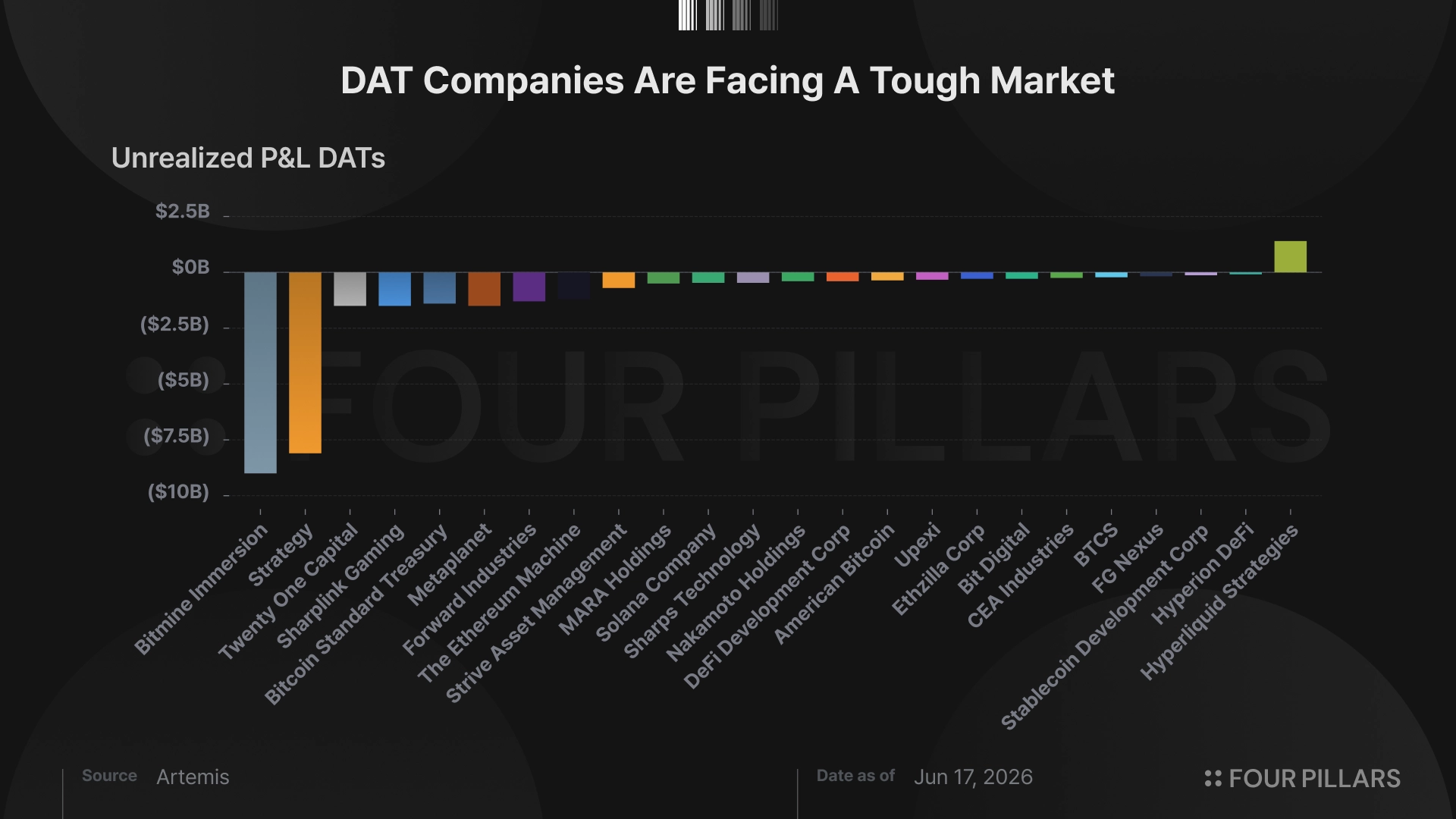

2. Current State of DATs

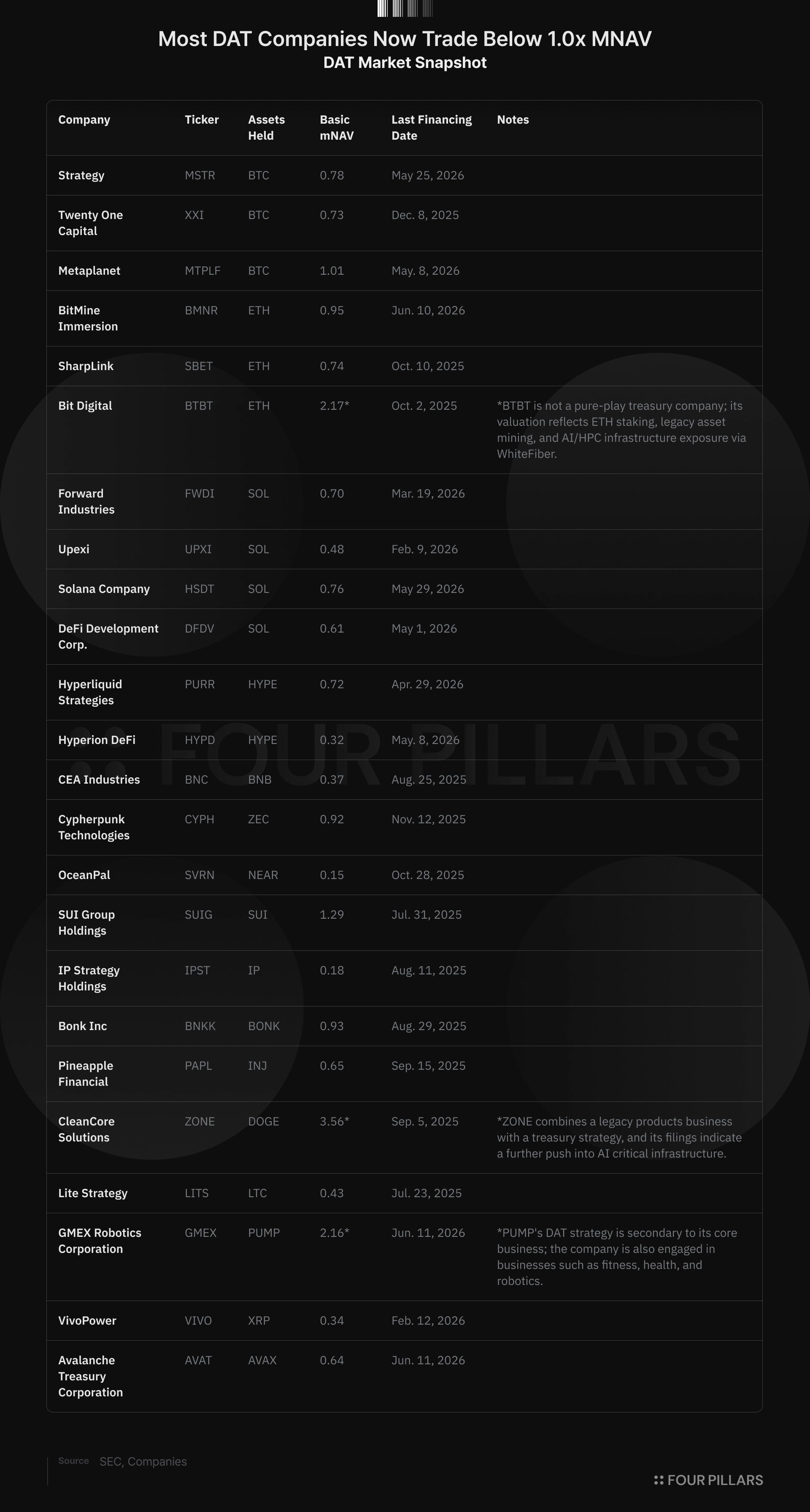

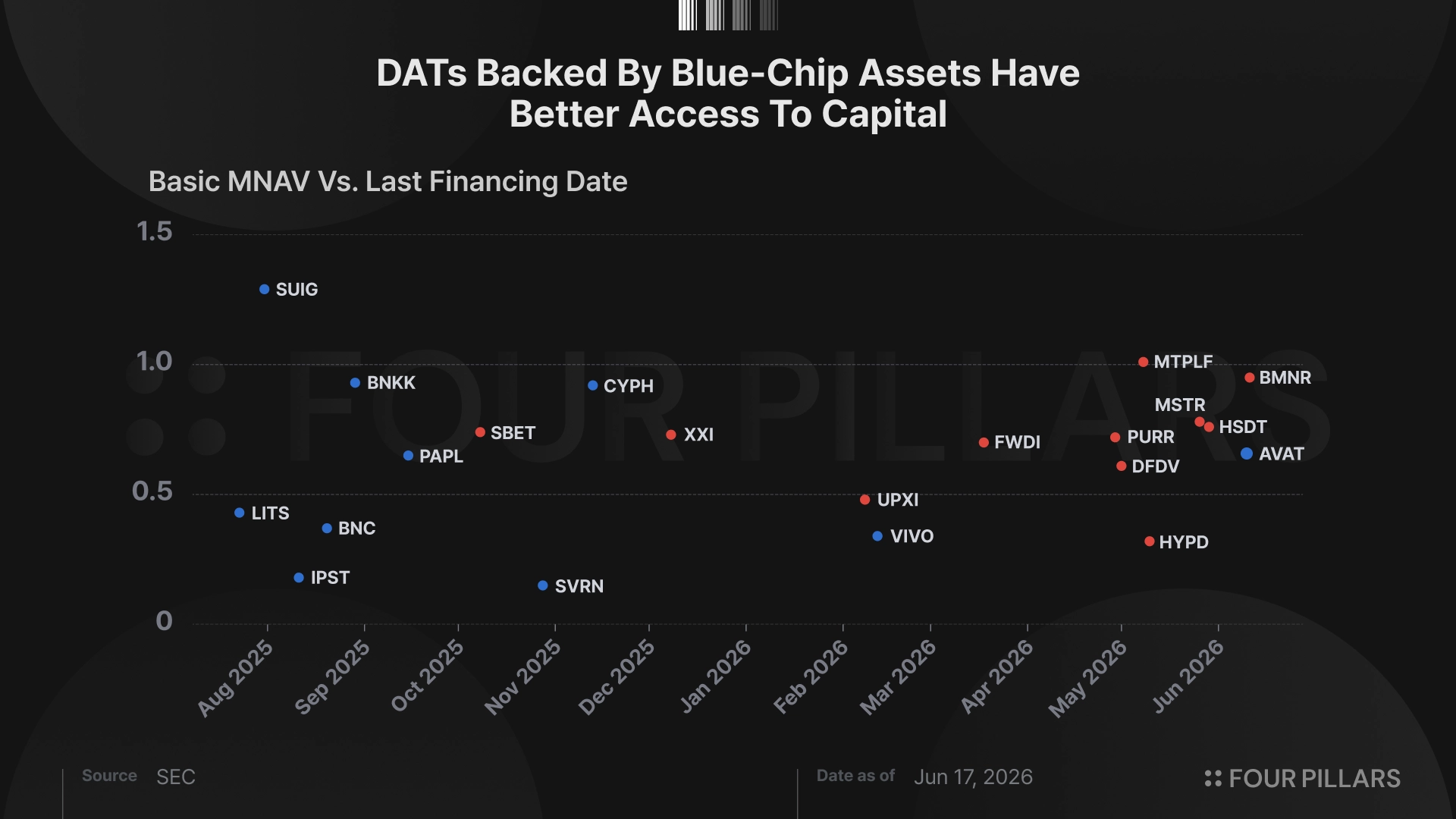

With the crypto market in poor condition, how are DAT companies doing now? I looked into the Basic mNAV of DAT companies based not only on BTC and ETH, but also SOL, HYPE, and various other alt tokens. I also checked when each company last raised capital.

(For reference, I calculated Basic mNAV by simply dividing each company’s current market capitalization by the size of its digital asset holdings. Since stock prices, token prices, and other inputs change constantly, and some calculations are based on disclosure data rather than real-time data, the numbers may be somewhat inaccurate.)

- mNAV < 1: The most noticeable data point is that the Basic mNAV of most DAT companies has fallen below 1. (For reference, a few companies where DAT is not the main strategy and that still actively operate other businesses, such as BTBT, ZONE, and GMEX, are exceptions.) This is basically because DAT stocks, unlike ETFs, cannot be redeemed. As market conditions worsened, an additional negative premium was applied. Since the basic premise of DAT companies is to buy assets using the mNAV premium, this situation could become a major burden if it continues for a long time.

- Extremely low mNAV: The level of mNAV resilience also differed depending on the underlying digital asset. For BTC and ETH DATs, Basic mNAV generally stayed above 0.7. For DATs based on other alt tokens, however, Basic mNAV was spread across a much wider range. In particular, IPST and SVRN have fallen into the 0.1 range. This shows that the attractiveness of the underlying digital asset is important for a DAT company to receive a reasonable mNAV valuation.

- Correlation between last financing date and mNAV: Before analyzing the data, my hypothesis was that companies with lower mNAV would have a harder time raising capital, so their most recent financing dates would be further in the past. However, the data showed that there was no strong correlation. What did show a clear correlation was that DAT companies based on top-tier digital assets, such as BTC, ETH, SOL, and HYPE, tended to have more recent financing dates. This suggests that there is still fairly steady demand for capital raises among DAT companies based on top-tier tokens. On the other hand, for most alt token DATs, it also suggests that they raised capital once or twice in the early stage when the DAT narrative was popular, but did not see much demand for additional financing afterward.

3. Die or Survive

DAT companies once appeared one after another, almost overnight. Now, they are standing at a crossroads between surviving and dying. Companies based on higher-quality digital assets, such as MSTR and BMNR, are still managing to hold on by continuously raising capital through preferred share issuances and other methods. However, some DAT companies based on less attractive assets have seen their mNAV fall to levels that may be difficult to recover from.

The goal of DAT companies is to continuously buy digital assets through the mNAV premium. Recently, however, poor market conditions have led some companies to do the opposite. They have sold digital assets and used the proceeds for share buybacks and operating expenses. DAT companies such as HSDT, LITS, ETHZ, FGNX, and EMPD are examples of companies that have actually done this. There have even been cases like STAS.L, where shareholders demanded redemption, and GNS, which went as far as liquidation.

As interest in the AI market has grown recently, some DAT companies have pivoted into AI businesses. STSS, which used to be a SOL DAT, changed its ticker to SKYA and pivoted into an agentic finance company. ZONE, which used to be a DOGE DAT, pivoted into an AI data center company. These cases show that companies that once pivoted into DAT in search of opportunity are now pivoting again in search of new opportunities to survive.

A painful waiting period has arrived. If negative market conditions continue, we may see more digital asset sales and share buybacks. DATs, which once acted as catalysts for price increases, have now become potential catalysts for price declines. It will be worth keeping an eye on whether DAT companies can endure this painful period and shine in the next bull market, or whether they were simply a short-term narrative.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.