![MSTR and COIN [FP Weekly 26]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F6ivhjsmqq8e3w1.png&w=1920&q=75)

Table of Contents

- 1. Major News

- [Crypto] Are MSTR and STRC Okay?

- [Institution] Coinbase’s Tokenized Stocks: Are They Really Tokenized Stocks?

- Others

- 2. Data Spotlight

- ALT DATs, Are They Still Alive? (Link)

- 3. Four Pillars Weekly

- : : A Look at Built-In Privacy on General-Purpose Chains (Link)

- : : Neutrl and the Fund Era of Stablecoin Yield (Link)

- : : Korean Stocks Now Trade 24/7: Markets.xyz and the Retail Opportunity (Link)

- : : SPCX, SPACE, SPX?: The Gap Between the Everything Exchange and Korean CEXs (Link)

- : : Collector Crypt Has No Collectors (Link)

- : : Monad Six Months After Launch (Link)

- : : Monthly EIP - May 2026 (ft. The Staking Issuance Debate and the Responsibility of Scale) (Link)

- Comments

- 4. Macro & Onchain Metrics

Researcher

1. Major News

[Crypto] Are MSTR and STRC Okay?

What Happened?

Source: Webull

STRC, Strategy’s preferred stock, fell to around $82 last Friday. Considering that STRC is designed around a reference price of $100, and that in the event of Strategy’s bankruptcy, each STRC share has a claim of $100 plus accumulated unpaid interest, this was a massive decline.

The whole incident traces back to Strategy’s sale of 32 BTC. In late May, Strategy sold 32 BTC to pay STRC dividends, and once this was disclosed through filings, the price of BTC dropped sharply from $72K to $59K. Strategy had mentioned during its Q1 2026 earnings call that it could sell BTC for MSTR’s BPS, but when this was actually put into practice, the market panicked.

One to two weeks after selling 32 BTC, Strategy instead raised funds through an MSTR ATM issuance, purchased 1,550 BTC, and also replenished the funding source for dividends. However, because the financing was done while mNAV was low, it resulted in dilution of MSTR’s BPS. Even though the company purchased far more BTC than it had sold, the market’s assessment remained harsh.

STRC recovered to around $88 by the close, but the fact that it is still far below $100 can be interpreted as a sign that the market has doubts about Strategy’s long-term sustainability. With Strategy’s current USD reserve size, it can withstand interest and dividend payments on debt and preferred stocks such as STRC for 7.7 months, and if it sells BTC, it can withstand them for about 31 years.

Researcher’s Comment

Strategy is a company that raises capital through various methods and purchases BTC in a way that does not dilute BPS. In order to raise capital without diluting BPS, MSTR’s mNAV needs to receive a premium of at least around 1.2 to 1.3. The breakeven mNAV for Q1 2026 was 1.22, but recalculating it based on current figures gives a value of about 1.29.

However, MSTR’s current mNAV is around 1.13. This means that if Strategy raises capital through MSTR ATM issuances to purchase BTC or pay STRC dividends, it could dilute the BPS that Michael Saylor has placed so much importance on. In fact, Strategy recently purchased an additional 1,550 BTC through an MSTR ATM issuance, but this resulted in BPS dilution and drew significant criticism.

Strategy has three scenarios left.

- Maintain the status quo: Continue raising funds little by little through MSTR ATM issuances, as it is doing now, to purchase BTC and pay STRC dividends. This is the best short-term approach if market conditions improve soon, but it could be extremely damaging if unfavorable market conditions persist over the long term.

- Sell BTC: This is the most rational decision. At the current mNAV level, selling the BTC it holds is more reasonable than issuing additional securities in order to reduce BPS dilution. However, considering the shock that the recent sale of 32 BTC brought to the market, I do not think this is a realistic option.

- Suspend STRC dividend payments: Since STRC is not a bond, there is no obligation to pay dividends. Therefore, in the worst case, Strategy could suspend dividend payments to STRC holders, but this would cause STRC’s price to collapse.

The easiest solution is for conditions in the BTC market to improve. If that happens, MSTR’s mNAV will naturally recover, STRC’s price will converge back toward around $!00, and Strategy’s capital engine will start running again. The worst-case scenario is that Strategy continues rescuing STRC at the expense of MSTR shareholders, as it is doing now, while poor market conditions persist for a long period of time. We should watch how Strategy manages to break through this situation.

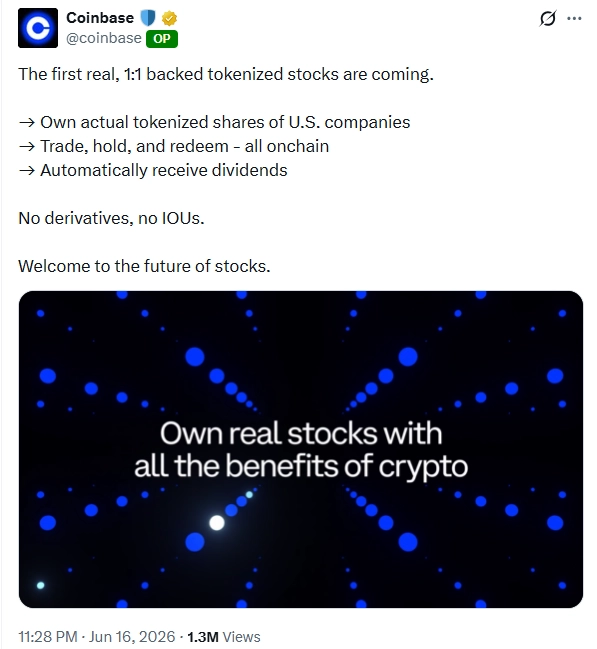

[Institution] Coinbase’s Tokenized Stocks: Are They Really Tokenized Stocks?

What Happened?

Coinbase previewed its tokenized stock service on June 16. Coinbase announced that its tokenized stock service is backed by actual shares, is not a derivative or IOU structure, and represents real ownership.

This service update aligns with Coinbase’s long-standing roadmap of becoming an exchange for everything. Coinbase is now aggressively expanding the range of tradable asset classes beyond simple digital asset spot trading to include futures, prediction markets, commodities, stocks, and more.

However, one thing stood out in the announcement: Coinbase’s tokenized stocks will not be offered in the United States. If stocks were tokenized in compliance with existing securities laws, they could have been offered to U.S. investors as well. Because of this, the community has had many discussions about whether Coinbase’s tokenized stocks are actually tokenized versions of real shares as Coinbase advertises, and what kind of structure is being used for the tokenization.

Researcher’s Comment

There are broadly four ways to tokenize stocks.

- The first is for a transfer agent, such as Securitize or Superstate, to directly tokenize shares. This complies with existing securities laws, and the token can inherit all rights attached to the shares.

- The second is to tokenize the rights to shares, as DTCC does. This is carried out by DTCC using a distributed ledger within its internal system.

- The third is the method used by Backed Finance, Ondo, and Robinhood, where shares are deposited and a derivative contract or security based on them is tokenized. This can provide investors with rights related to returns, such as price tracking and dividends, but it cannot tokenize ownership of the shares themselves.

- The last is perpetual futures trading that tracks the price of the stock.

Coinbase is highly likely to indirectly tokenize stocks through a method similar to Robinhood’s.

- The first reason is that directly tokenizing stocks requires a transfer agent, and Coinbase is not qualified as a transfer agent.

- The second reason is that Coinbase’s tokenized stock service cannot be offered to U.S. persons.

- The third reason is that Coinbase has repeatedly argued that the CLARITY Act hinders tokenized stocks, and it recently supported news of the SEC’s tokenization exemption. The CLARITY Act does not hinder tokenized stocks, and the SEC’s recent tokenization exemption enables indirect tokenization models like Robinhood’s to be carried out legally, rather than enabling direct tokenization.

The details of Coinbase’s tokenized stocks have not yet been disclosed, but we will need to watch closely to see how much of Coinbase’s claims are accurate and how much is exaggerated.

Others

Crypto

- Ethereum Foundation co-Exec Director and board member Hsiao-Wei Wang steps down

- Ventuals, the Pre-IPO Market on Hyperliquid, Is Shutting Down

- Altura winds down stablecoin vault after 'unprecedented level' of withdrawal requests

- Plasma One is live now.

Institution

- State Street launches GENIUS-compliant money market fund for stablecoin issuers

- Kraken Launches CFTC-Regulated Perpetual Futures for US Traders

- Coinbase Introduces Tokenized Stocks

- Zama, Morpho and Steakhouse launch first 'confidential DeFi yield' vault on Ethereum

- Fidelity launches GENIUS-aligned money market fund for stablecoin issuers

Tech

- Base targets June 25 mainnet launch for Beryl upgrade and new B20 token standard

- Nous Research’s Hermes Agent Integrates Stripe Skills for Autonomous Agent Commerce

Investment

- Paradigm leads $9 million round in LatAm payments app El Dorado

- Standard Chartered says Uniswap's UNI token could surge 40x to $100 by 2030

- BlackRock launches new Bitcoin ETF that generates income using a covered call strategy

- EarnOS launches anti-AI slop app, raises $6 million from 1kx, Circle and Coinbase

- Kalshi holds early IPO talks with investment banks

Asia

- Ondo teams up with Mirae Asset to tokenise its Global X ETFs lineup

- Toss Bank pursues global remittance PoC with Solana

2. Data Spotlight

ALT DATs, Are They Still Alive? (Link)

3. Four Pillars Weekly

: : A Look at Built-In Privacy on General-Purpose Chains (Link)

- Recently, Sui and Starknet each rolled out privacy features, Confidential Transfers and STRK20 respectively. Both chains put privacy front and center, but they made nearly opposite design choices on what to hide and who holds the authority to disclose.

- Starknet's STRK20 uses a shielded pool model that hides the sender, the recipient, and the amount, severing the transaction graph itself. Auditors are given only read access for tracing and cannot seize assets. Sui's Confidential Transfers, by contrast, hides only the amount while leaving the sender and recipient public, and it follows an issuer-centric structure in which the issuer holds the power to freeze, seize, and audit, all at the code level. Starknet set out to build user-sovereign privacy aimed at DeFi users who want to protect their assets, while Sui aimed for compliance-friendly privacy targeting stablecoin issuers and institutions that cannot give up compliance.

- Privacy is no longer the preserve of dedicated chains. It is becoming a standard feature of general-purpose L1s. As general-purpose chains begin to absorb privacy that is good enough to use, privacy-focused chains with only middling liquidity and technology are bound to lose ground. The space where they can survive will be the far ends of the spectrum that general-purpose chains struggle to reach by design, such as comprehensive privacy that also covers metadata and the network layer, or private computation.

: : Neutrl and the Fund Era of Stablecoin Yield (Link)

- Pure basis is losing its edge as funding rates compress and the trade commoditizes. The stablecoin yield set has now converged into a narrow band: Aave v3 USDC at 3.19%, Sky sUSDS at 3.6%, Syrup USDC/USDT at 4.5%, Ethena sUSDe / stcUSD at 5.02%, and Neutrl at 5.2%.

- The protocols that sustain premium yields from here will increasingly look like multi-strategy credit funds rather than single-strategy vaults.

- Neutrl’s liquid reserves provide the base, basis trades capture speculative demand, and OTC locked-token positions monetize forced selling. The edge sits in the active sleeve’s ability to access return streams that reserve-only products cannot.

- Basis and OTC are negatively correlated by construction. When basis compresses, OTC opportunities tend to expand. When OTC dries up, basis tends to be rich because speculative demand has returned.

- The next leg sits in distressed credit, a $190.5B market with no scaled onchain fund analogue. Neutrl has not built the product yet, but the skill-set transfer from its OTC desk is direct.

: : Korean Stocks Now Trade 24/7: Markets.xyz and the Retail Opportunity (Link)

- Korean retail net bought ₩32.4 trillion in equities through early June, with Samsung and SK Hynix absorbing 73% of that flow and accounting for 42% of the KOSPI, the most concentrated semiconductor bet in a generation.

- Perpetual contracts on Samsung (10x), SK Hynix (10x), Hyundai (10x), and EWY (the MSCI Korea ETF, 20x) already trade 24/7 on Hyperliquid.

- Markets by Kinetiq has generated $3.75 billion in cumulative volume from 9,278 users since launching in January 2026, averaging $404K per user.

- Markets builds trading as a social product. Every position posted carries a verified onchain PnL history and copy trading/counter-trading are each one tap.

- Every trade on Markets earns kPoints toward KNTQ allocation, with Season 2's final snapshot on September 29, 2026. 100% of platform revenue flows to sKNTQ staker buybacks.

: : SPCX, SPACE, SPX?: The Gap Between the Everything Exchange and Korean CEXs (Link)

- On June 16, 2026, Bithumb listed Spacecoin and Upbit listed SPX6900, after which Bithumb listed SPX6900 as well. The Korean community tied these listings to the SpaceX IPO, which had debuted on the Nasdaq four days earlier on June 12. A low-profile token and an aging meme coin were listed at this exact moment under names that bring SpaceX to mind, and many read the situation as the exchanges riding the hype to pull in trading volume.

- This reading gains weight against the backdrop of weak results at Korean exchanges. Dunamu's first-quarter revenue in 2026 fell roughly 55 percent from a year earlier, and Bithumb swung to a net loss. Both exchanges draw their income almost entirely from one source, trading fees, so when volume drops, earnings collapse with it.

- Korea classifies tokenized stocks as securities and bars crypto exchanges from handling them, and it does not permit crypto futures, derivatives, or spot exchange-traded funds (ETFs) either. Over the same period, Binance, Kraken, and Bybit expanded into tokenized stocks and direct trading of overseas shares, generating billions of dollars in related trades on the day SpaceX listed alone. The fact that a "similarly named spot token" is the only channel left for Korean exchanges to join a narrative the rest of the world has joined is a bleak one.

- Regulation designed to protect investors paradoxically pushes the exchanges into the market's most speculative corner. With revenue streams and product lines such as derivatives, tokenized stocks, and ETFs all closed off, the only lever left to an exchange is spot listing, and the drier volume becomes, the more it tilts toward higher-profile, and therefore more speculative, listings.

: : Collector Crypt Has No Collectors (Link)

- Of CC's $635 million in all-time gross revenue, 90.6% was returned to users as instant card buybacks, leaving $43 million in net revenue at a 6.7% hold rate.

- Secondary trading across every channel, eBay plus peer-to-peer marketplace, totals under $5 million, and the eBay share of gacha flow has fallen from 1.23% to 0.10% over six quarters.

- Total token value accrual across burns and buybacks amounts to $1.4 million, or 3.4% of net revenue, while the operational wallet has off-ramped $45.7 million in USDC.

- Net margins halved from 11.2% to 5.8% as volume tripled into high-tier packs where the house edge is thinnest, and each new denomination ladder step pulls the blended margin lower.

- The ~$535 million FDV prices CARDS at 7.3x net revenue for a margin-compressing casino with roughly 420 daily players, a 20.5% float, and 72% insider supply vesting through November 2027.

: : Monad Six Months After Launch (Link)

- Monad takes on the blockchain trilemma not by proposing a new model, but through extreme engineering. It keeps the EVM interface and redesigns consensus, execution, network propagation, and storage underneath to optimize each one. MONAD_NINE and MIP-3, MIP-4, and MIP-5 show that Monad is running a high-performance EVM variant, tuning resource pricing and execution rules to fit its own runtime.

- The price of high performance is complexity. Asynchronous execution, parallel execution, reserve balance, and the split between block states in RPC all create complexity specific to Monad. Monad works to abstract this down to a level developers and infrastructure can handle, using the MIP process, tooling, RPC specs, and precompiles. In other words, Monad's performance is the result of system engineering across execution, memory, storage, and network propagation together.

- Monad's next task is to move past the identity of "a faster EVM." The job ahead is not to be a fast chain, but to build a new identity that gives builders and users a reason to stay as blockchain demand keeps expanding, backed by a long-term vision.

: : Monthly EIP - May 2026 (ft. The Staking Issuance Debate and the Responsibility of Scale) (Link)

- The EIP landscape in May saw a wave of core and ERC proposals aimed at redefining long-held assumptions around transaction, asset, and authorization models, highlighting Ethereum’s continued evolution toward expanding and reshaping its design space.

- In May 2026, amid key personnel departures and growing external coordination efforts, Vitalik argued that the Ethereum Foundation should be viewed not as the center of Ethereum but as a purpose-driven node within a broader ecosystem, underscoring the need to redefine its role around long-term sustainability and core values.

- Meanwhile, the debate over Ethereum’s staking issuance policy, reignited by accelerating institutional capital inflows, ultimately raises a deeper question: how can Ethereum preserve its credible neutrality while managing the growing influence of large-scale staking infrastructure through voluntary norms and self-imposed constraints?

Comments

- Can the Ethereum Foundation Finish the Job Before Making Itself Obsolete?

- Are HIP-3 Newcomers Cooked?

- Why Mirae Asset Chose Ondo Finance

4. Macro & Onchain Metrics

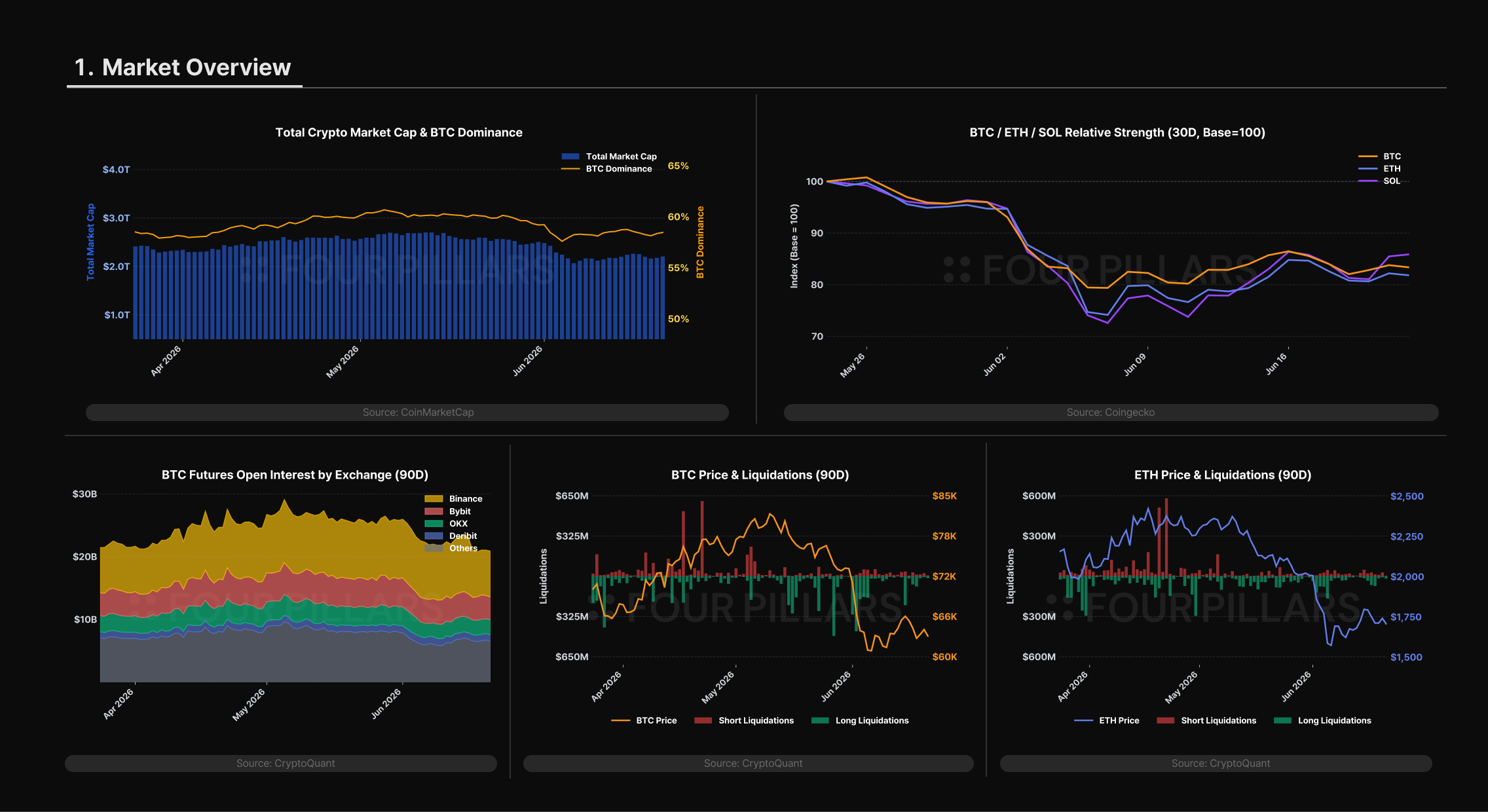

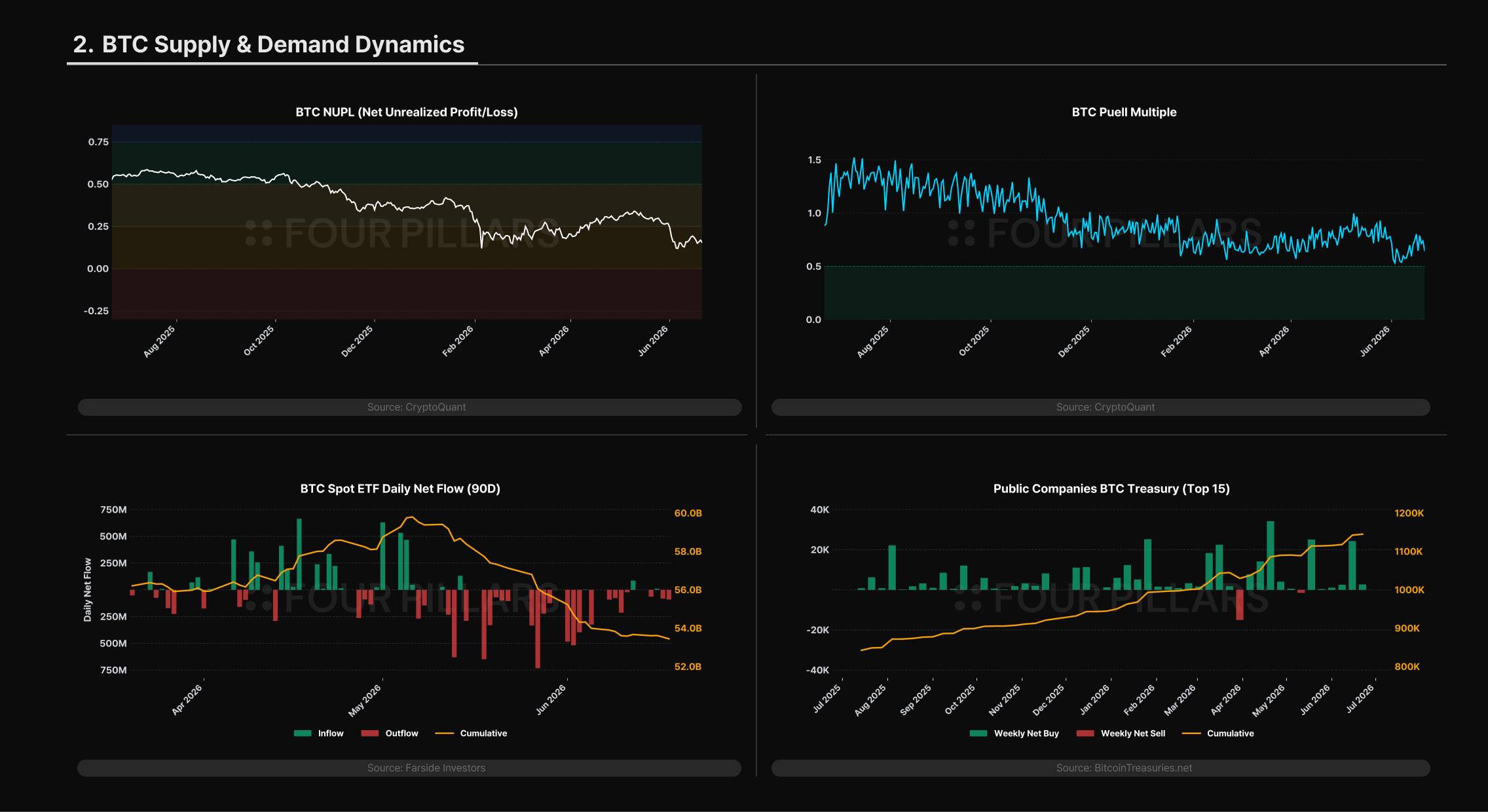

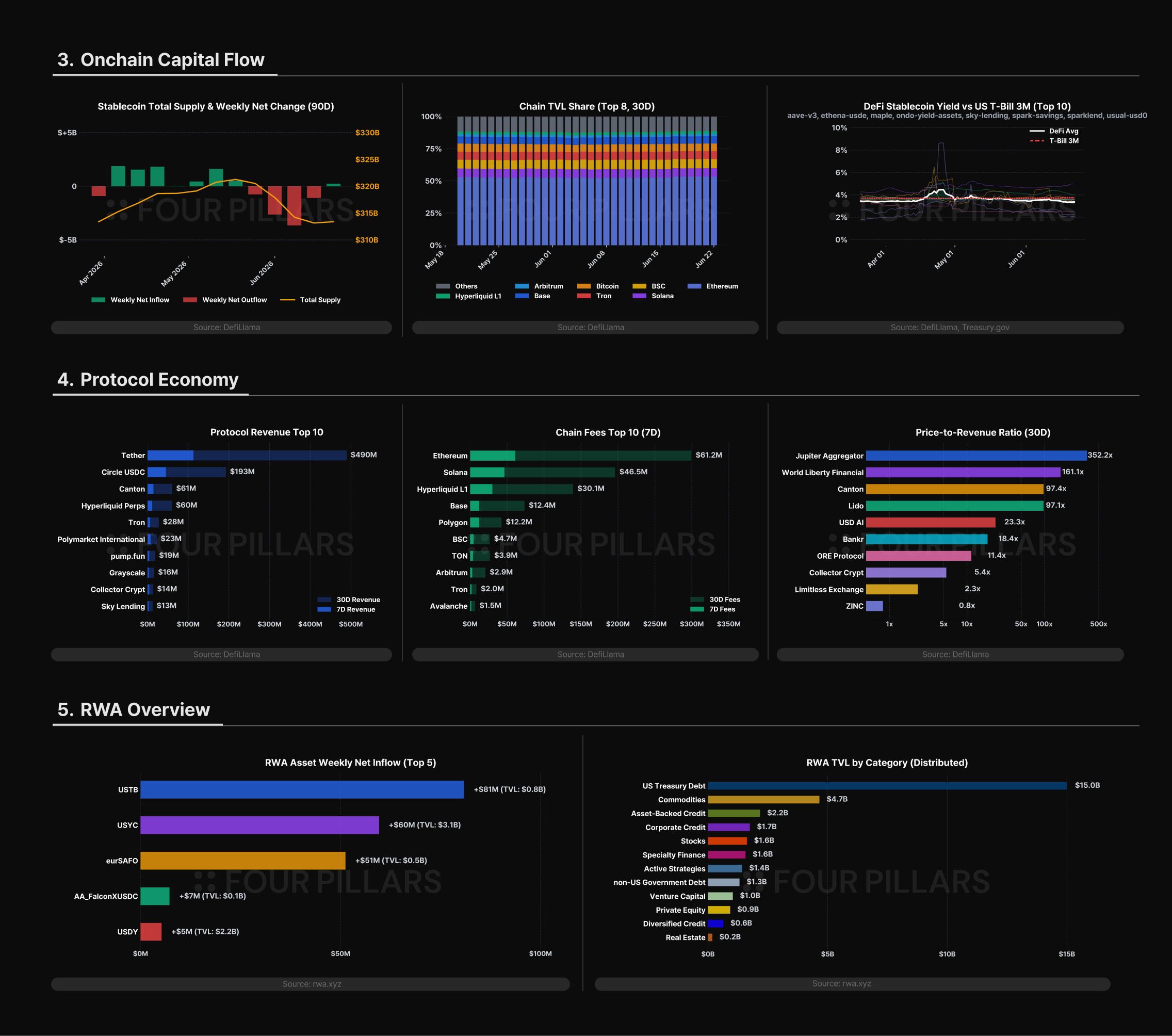

Some of the charts below are powered by CryptoQuant. For those interested in exploring the underlying data in greater detail, CryptoQuant provides access to a comprehensive suite of onchain and market analytics used by institutional participants.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![50% for Ethereum, 50% for Congress [FP Weekly 33]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F1cg9d7msn1d3j2.png&w=1920&q=75)

![Coldcard Got Burned, Coinbase Froze [FP Weekly 32]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fhv83s5msebytml.png&w=1920&q=75)