Table of Contents

- 1. Ondo Finance Signs Tokenization MOU with Mirae Asset Global Investments

- 2. Why Tokenized ETFs Cannot Work Like “Tokens" in Korea

- 3. Mirae Asset's Tokenization Timeline: Built on a Global ETF Franchise

- 4. Ondo Finance's Timeline: From Treasuries to Equities to Onchain Prime Brokerage

- 5. What Does the Mirae Asset and Ondo Finance Collaboration Signal for the Market?

Researcher

Related Projects

1. Ondo Finance Signs Tokenization MOU with Mirae Asset Global Investments

Source: Ondo

Ondo Finance announced that it has signed a memorandum of understanding (MOU) with Mirae Asset Global Investments, Korea's largest asset manager. Through Ondo Global Markets, a tokenized securities platform, the two firms plan to tokenize the ETF product lineup of Mirae Asset's Global X unit.

The collaboration starts with Global X's U.S. ETFs and then expands to funds listed in major markets including Europe, Hong Kong, Japan, Canada, and Australia. The division of roles is also clear. Mirae Asset continues to handle the asset management of the underlying ETFs, while Ondo provides the tokenization infrastructure and onchain distribution.

The notable partner here is Mirae Asset Global Investments, an unfamiliar name in the crypto market. Mirae Asset is Korea's largest asset manager. Including its management subsidiaries, it runs about $410B in AUM and around $190B in overseas investment assets. It is also the second-largest player in Korea's ETF market and, through Global X, the world's 12th-largest ETF issuer, running ETFs across 10 countries.

This unusual pairing raises important questions for both Korea's tokenized securities market and the global onchain market:

- In Korea, the amended Electronic Securities Act enabling tokenized securities issuance is set to take effect in 2027. The framework has barely opened, but an attempt to put global ETFs onchain is difficult to launch within Korea's regulatory perimeter. As a result, even the largest asset manager, the one that has prepared its tokenized securities business most aggressively, skipped its home market as the first stage.

- In the offshore onchain market, traditional asset managers already use tokenization as a distribution channel, and large managers' products have come onto Ondo's rails one after another. Mirae Asset's entry shows that this trend is spreading to Asian asset managers. The next competition narrows to who captures the standard onchain distribution rail for the Asian market first.

2. Why Tokenized ETFs Cannot Work Like “Tokens" in Korea

The reason Mirae Asset sought the stage for ETF tokenization outside Korea becomes clear once you look into Korea's tokenized securities framework. Korea's tokenized securities framework was built out along two broad tracks, issuance and distribution:

- Issuance: Tokens recorded on a blockchain distributed ledger are now recognized as formal securities. Until now, issuance had to go through existing institutions such as brokerages, but now an issuer that meets certain requirements can issue tokenized securities directly.

- Distribution: Centered on non-standardized assets that had been hard to trade, such as fractional investment in real estate or art, it opened a new over-the-counter trading venue where multiple investors can buy and sell.

In this structure, Korea's tokenized securities sit closer to a supplementary ledger system for absorbing unlisted, non-standardized securities. Listed standardized securities such as listed equities, listed depositary receipts (DRs), and derivative-linked securities have effectively been pushed to lower priority.

Standardized securities are not excluded as a matter of regulation. The Korean government also keeps the tokenization of standardized securities open as a long-term agenda item, but realization remains distant. Listed securities are already fully electronically registered, and the financial authorities judge that a distributed ledger would struggle to handle the scale of the listed market.

For this reason, the path to issuing ETFs, which are listed securities, as tokenized securities within Korea's regulatory perimeter has not opened in earnest. One reason Mirae Asset set the starting point for ETF tokenization in the U.S. and Hong Kong is a reasonable workaround for this constraint.

3. Mirae Asset's Tokenization Timeline: Built on a Global ETF Franchise

Mirae Asset's offshore first-mover move was not implausible to begin with. Mirae Asset's ETF franchise has grown cross-border from the start. It first brought the U.S. Nasdaq 100 to Korea, and it is also the only Korean asset manager to have established ETF bases overseas.

Mirae Asset's global operations have already grown at a 34% CAGR over the past decade, close to double the 18% average for global ETF managers. ETF tokenization is the next step in moving this cross-border approach onchain.

The collaboration with Ondo also connects to Mirae Asset's digital asset moves. Since last year, Mirae Asset has been taking the preparatory steps for digital asset expansion one by one.

In September 2025, it partnered with Ava Labs to secure a technical foundation. The same year, it acquired the Korean exchange Korbit, adding a distribution channel.

Entering 2026, it aligned its direction around ETFs, AI wealth management, and digital assets under the Mirae Asset 3.0 vision, and in the same month entered the productization stage through the collaboration with Ondo. It is a move that filled in technology, distribution, and product in succession.

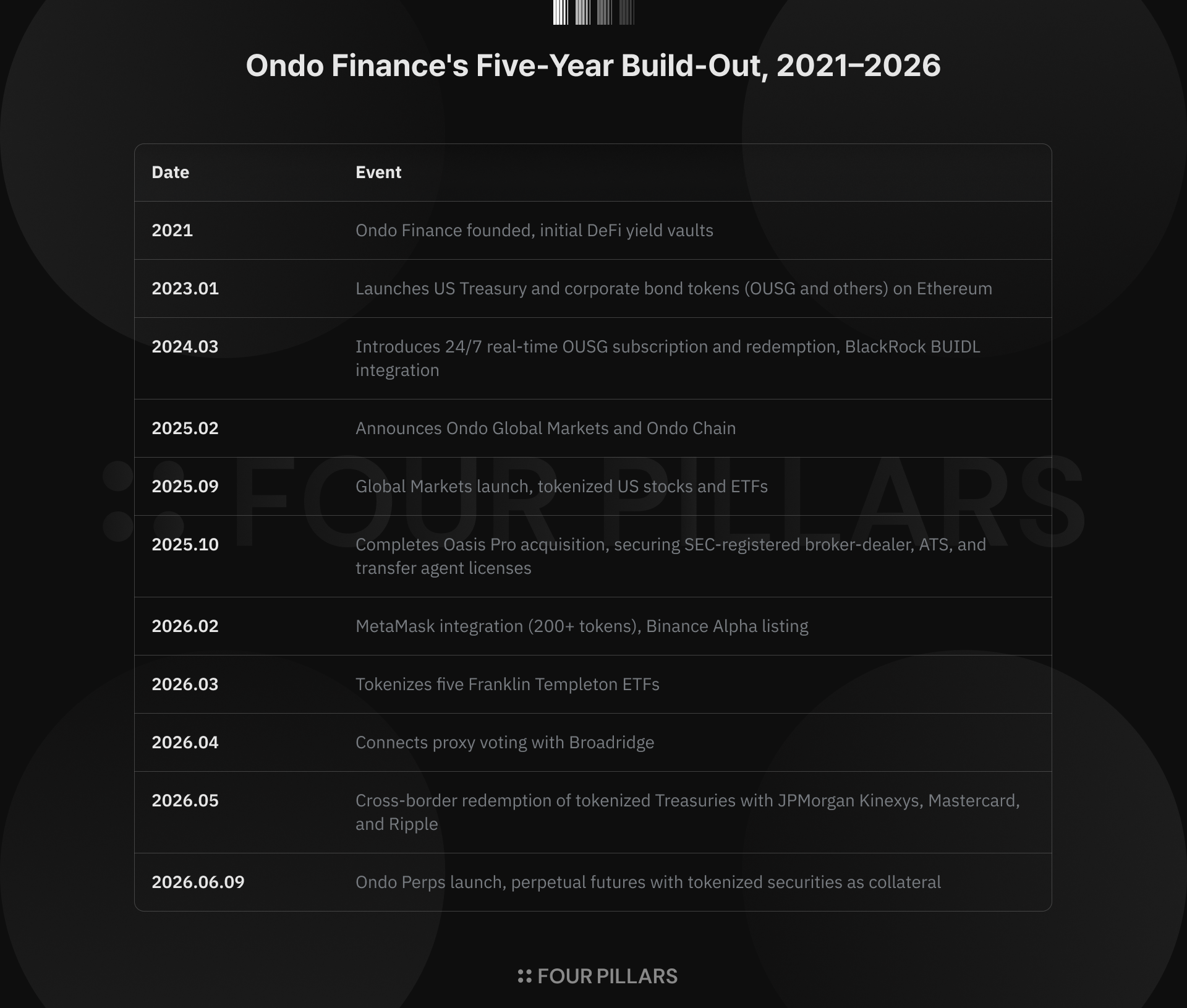

4. Ondo Finance's Timeline: From Treasuries to Equities to Onchain Prime Brokerage

The missing piece for Mirae Asset is the onchain distribution rail. The rail Ondo has built over five years plays that role.

Ondo has tokenized funds and ETFs from traditional asset managers such as BlackRock and Franklin Templeton, and distributed them to more than 250 wallets and exchanges including MetaMask and Binance. Having built up this track record, it currently holds about 60% of the tokenized equity market by RWA.xyz data.

Source: X(@OndoPerps)

Entering 2026, it expanded beyond tokenization into trading infrastructure. Ondo Perps offers perpetual futures collateralized by tokenized securities. This is a departure from existing exchanges that accepted only stablecoins as collateral. The idea is to gather tokenized spot, lending, and leverage into the same capital infrastructure to build an onchain prime brokerage.

Alignment with institutional finance also strengthened during this period. Ondo acquired Oasis Pro, securing SEC-registered broker-dealer, transfer agent, and ATS licenses. With this, it gained the capability not only for SPV-based tokenization but also to register tokenized securities directly and manage transfer records.

The collaboration with Broadridge sits in a similar context. Ondo enabled holders of tokenized equities to view corporate disclosures from a crypto wallet and submit voting intentions on each shareholder meeting agenda item. It is an attempt to fill the shareholder-rights gap often noted in tokenized securities.

5. What Does the Mirae Asset and Ondo Finance Collaboration Signal for the Market?

Through this collaboration, the two sides share what each brings: Mirae Asset's roughly $60B Global X ETF lineup, and the tokenization rail Ondo built over five years.

This setup makes visible the changes and market currents spanning the global tokenization market, the revenue models of tokenization platforms, Asian asset managers, and Asian regulated finance as a whole.

- The Tokenized ETF Playbook: First-generation tokenized equities had the tokenization platform buy stocks such as AAPL, TSLA, and NVDA directly in the market and issue them as SPV-based linked securities. ETF tokenization reduces the burden of liquidity management. The asset manager runs the ETF as before, and the platform manages only the tokenization and the onchain distribution rail. The Ondo and Mirae Asset collaboration shows a model that moves index exposure onchain as is while separating management from distribution.

- A Revenue Model Made Visible Through Brokerage: Issuance and distribution alone leave tokenization platforms with thin margins. Redemption fees and the management fees on tokenized treasuries are low, and the scale falls short of traditional finance. Ondo Perps is a move toward thicker revenue sources: trading fees, margin, and liquidation. The platform economics hold once tokenized ETFs and equities become the basis for derivatives rather than just held assets. This is why exchanges including Backpack are heading in the same direction.

- The Empty Non-U.S. Asset Pie: Tokenized equities formed around U.S. assets because of the difference in demand scale, and the market has already entered saturation. The inclusion landscape at major exchanges such as Binance and Bybit is already settled, and HIP-3-style perpetual futures have taken part of the trading pie. Non-U.S. assets, by contrast, sit empty. As SK Hynix and Samsung Electronics have shown, global demand for Asian assets is clear. This is why Mirae Asset placed Asian underlyings such as the Hong Kong HSCEI covered-call ETF among its tokenization targets. The next market is forming in the flow of Asian managers putting their domestic and regional assets onchain.

- Asian Regulated Markets Are a Different Game: Korea's tokenized securities and Japan's Progmat rails are closed markets where the assets eligible for tokenization, and even the methods of issuance and distribution, are set by domestic regulation. Both Korea and Japan restrict issuance and distribution to licensed trusts and licensed operators. By contrast, the offshore market that the likes of Ondo occupy is an open market based on Reg S. Neither the settlement infrastructure nor the investor pools overlap. Mirae Asset is building a track record offshore before its home framework opens, but the two markets will likely remain separate going forward.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.