Table of Contents

- Key Takeaways

- 1. Background: Upbit and Bithumb's SPACE and SPX Listings, and the Korean Community's Shock

- 2. Where Korean Exchanges Stand Now

- 2.1 A Revenue Structure Dependent on Fees

- 2.2 The Regulatory Picture

- 3. A Comparison With Overseas Exchanges

- 3.1 Have Korean Exchanges Lowered Their Listing Standards?

- 3.2 As Overseas Exchanges Aim to Become Everything Exchanges, Korean Exchanges...

- 4. Implications

Researcher

Key Takeaways

- On June 16, 2026, Bithumb listed Spacecoin and Upbit listed SPX6900, after which Bithumb listed SPX6900 as well. The Korean community tied these listings to the SpaceX IPO, which had debuted on the Nasdaq four days earlier on June 12. A low-profile token and an aging meme coin were listed at this exact moment under names that bring SpaceX to mind, and many read the situation as the exchanges riding the hype to pull in trading volume.

- This reading gains weight against the backdrop of weak results at Korean exchanges. Dunamu's first-quarter revenue in 2026 fell roughly 55 percent from a year earlier, and Bithumb swung to a net loss. Both exchanges draw their income almost entirely from one source, trading fees, so when volume drops, earnings collapse with it.

- Korea classifies tokenized stocks as securities and bars crypto exchanges from handling them, and it does not permit crypto futures, derivatives, or spot exchange-traded funds (ETFs) either. Over the same period, Binance, Kraken, and Bybit expanded into tokenized stocks and direct trading of overseas shares, generating billions of dollars in related trades on the day SpaceX listed alone. The fact that a "similarly named spot token" is the only channel left for Korean exchanges to join a narrative the rest of the world has joined is a bleak one.

- Regulation designed to protect investors paradoxically pushes the exchanges into the market's most speculative corner. With revenue streams and product lines such as derivatives, tokenized stocks, and ETFs all closed off, the only lever left to an exchange is spot listing, and the drier volume becomes, the more it tilts toward higher-profile, and therefore more speculative, listings.

1. Background: Upbit and Bithumb's SPACE and SPX Listings, and the Korean Community's Shock

Source: New Listings Feed

On the morning of June 16, 2026, the biggest topic across the Korean community was Bithumb's listing of Spacecoin (SPACE) and Upbit's listing of SPX6900 on their won markets. One might ask whether this was just an ordinary token listing notice, but the reason it drew attention was not the listing itself.

What stirred the community was less the listing than the combination and the timing.

Four days earlier, on June 12, SpaceX had listed on the Nasdaq under the ticker SPCX. As everyone knows, SpaceX's IPO was the largest on record, and since stock-related topics now dominate the Korean crypto community, it had been the hottest name in those circles over the weekend.

After Upbit and Bithumb posted their listing notices, suspicion spread through the community that the two were listing tokens with names and tickers resembling SPCX in order to ride the hype and secure volume. The connection rests only on circumstance, but the fact that such a reading was accepted so readily says something about the position Korean exchanges are in.

The reaction soon turned to a self-deprecating one. While overseas venues such as Coinbase, Binance, and Bybit let users trade SpaceX and other foreign stocks directly inside the exchange, Korean exchanges cannot offer such products because of regulation, so perhaps the best they can do is list a coin that at least shares a name.

I do not think this episode is merely something to laugh off and move past. I see it as a case that shows just how harsh the environment is for Korean crypto exchanges trying to compete with their overseas peers. In this piece, I want to look at the market and regulatory conditions surrounding Korean crypto exchanges today, and at how those conditions diverge from the rest of the world.

2. Where Korean Exchanges Stand Now

2.1 A Revenue Structure Dependent on Fees

Source: FSS DART, translated via ChatGPT

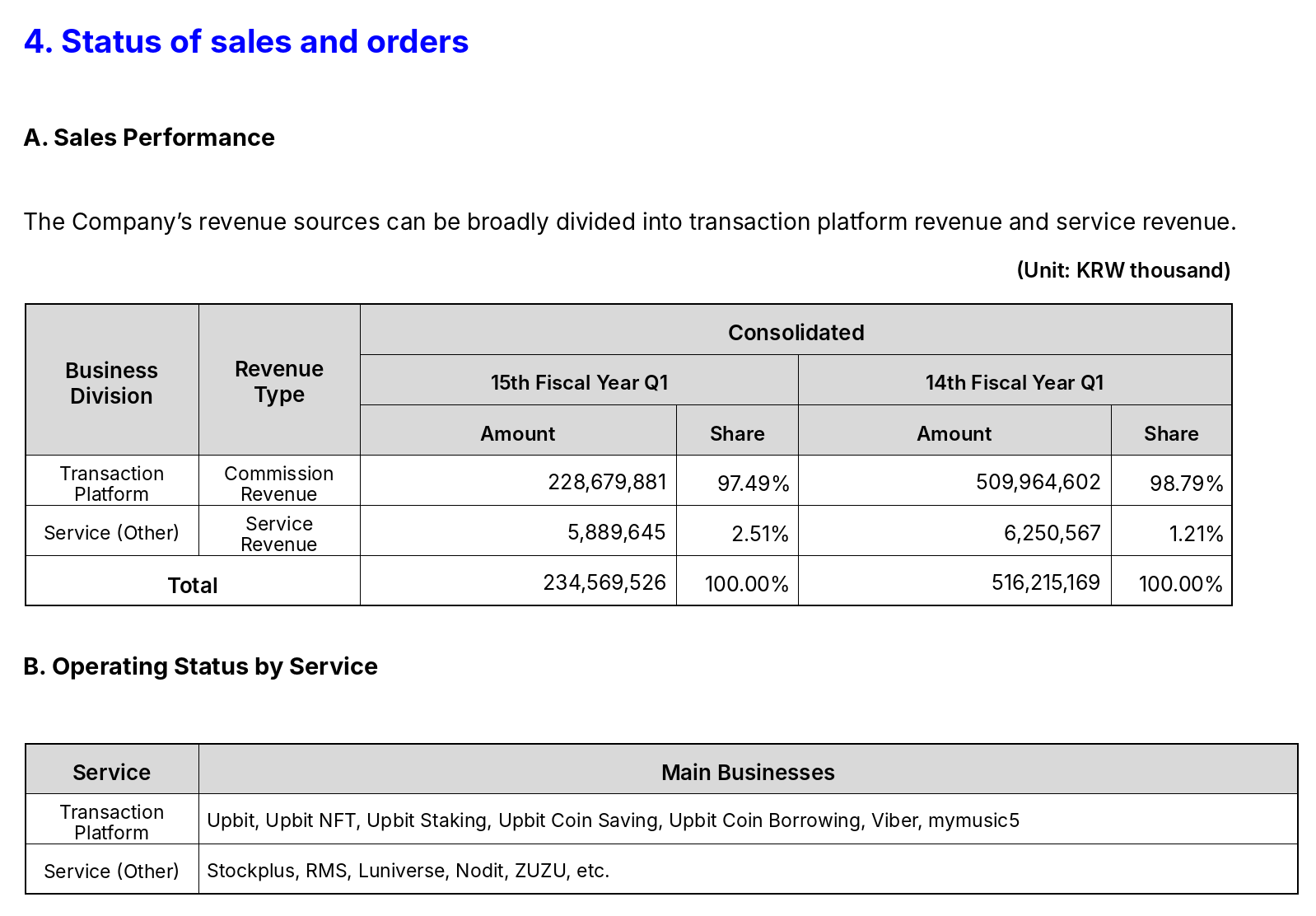

The first-quarter scorecard for 2026 was poor across Korea's major exchanges. According to quarterly reports released on May 15 through the Financial Supervisory Service's electronic disclosure system, Dunamu, which operates Upbit, posted consolidated revenue of 234.6 billion won, down 54.6 percent from a year earlier. Operating profit fell 77.8 percent to 88 billion won, and net profit dropped 78.3 percent to 69.5 billion won. Fee revenue from Upbit fell 55.2 percent, sliding into the 200 billion won range, while operating costs over the same period rose 22 percent, squeezing margins.

Source: FSS DART, translated via ChatGPT

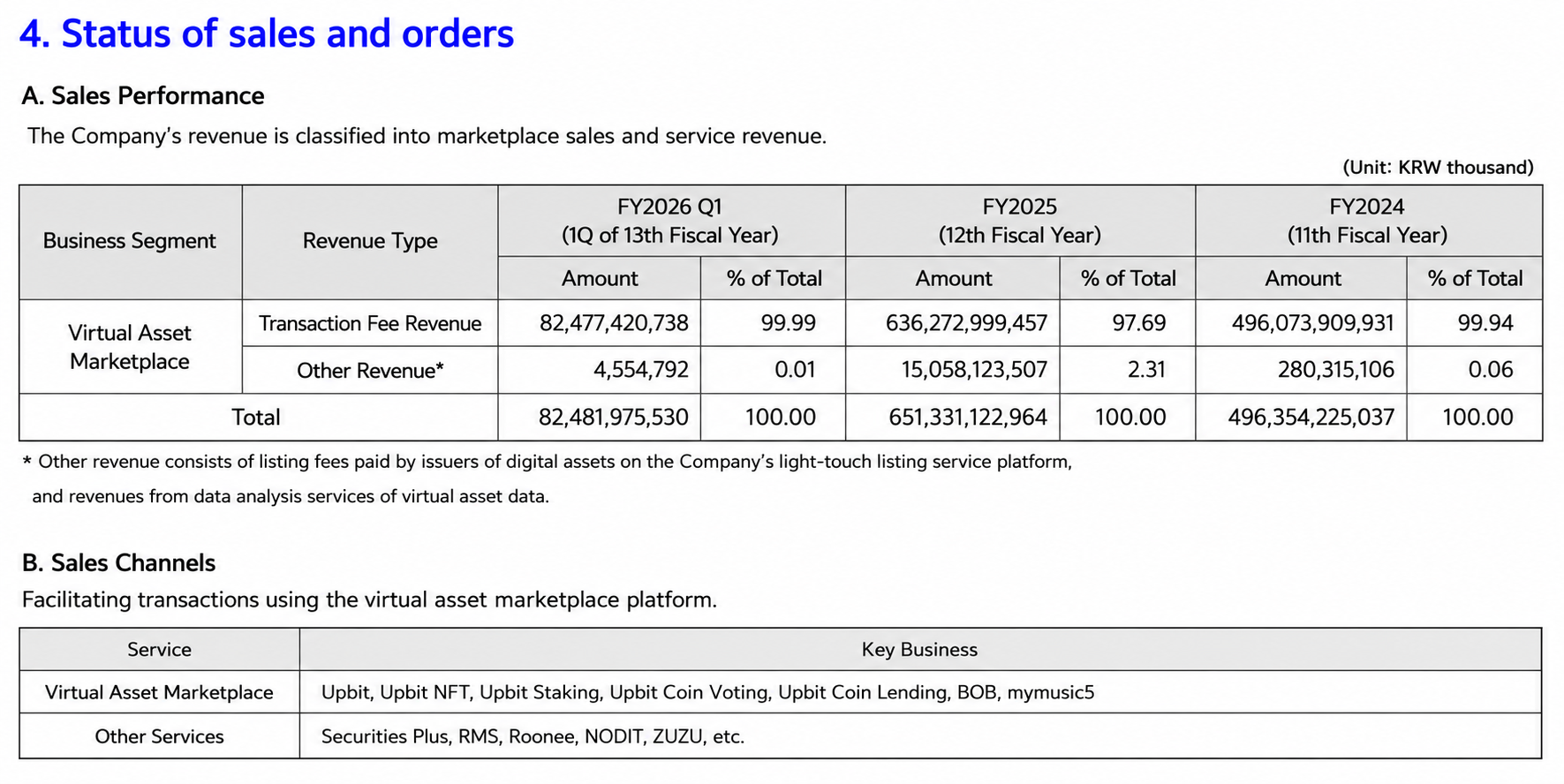

Bithumb's situation is harder still. First-quarter revenue fell 57.6 percent to 82.5 billion won, and operating profit plunged 95.8 percent to 2.9 billion won. The bottom line swung into the red with a net loss of 86.9 billion won, the second straight quarter of net losses after the prior one. The direct cause was an 87 percent drop in fee revenue as trading value shrank. On top of that, a six-month partial suspension of business and a 36.9 billion won fine imposed by the Korea Financial Intelligence Unit for violations of the Specified Financial Transaction Information Act were reflected in the first-quarter results.

The biggest problem is that the revenue structure of Korean exchanges leans almost entirely on trading fees. Trading fees account for about 97.5 percent of Dunamu's revenue and 99.99 percent of Bithumb's, so fees are effectively the whole of it. Yet it is more reasonable to attribute this structure to the regulatory environment Korean crypto exchanges face, discussed below, than to any negligence in how they run their business.

2.2 The Regulatory Picture

What a Korean crypto exchange can actually handle is, in practice, the crypto spot token and little else. Most other areas are blocked, whether by explicit rule or by tacit avoidance.

- Tokenized stocks: In June 2026, the Financial Services Commission and the Financial Supervisory Service moved toward classifying tokenized stocks as securities rather than virtual assets. Securities fall under the Capital Markets Act regardless of the form in which they are issued, and under the Electronic Securities Act, only a licensed electronic registration agency may carry out the electronic registration of rights. If a crypto exchange that is not such an agency issues or circulates security tokens, it amounts to operating without a license. In other words, tokenized stocks, which are growing fast abroad, are an asset that Korean crypto exchanges structurally cannot handle, and that is unlikely to change.

- Futures and derivatives: Korean crypto exchanges offer spot trading only and cannot provide derivatives such as perpetual futures or options to domestic users. This is less a clean prohibition in law than a hurdle left by a single attempt. Coinone, one of Korea's five major exchanges, ran a margin trading service with leverage of up to four times for about a year starting in December 2016. When regulatory moves by the government and a police investigation began in late 2017, it shut the service down entirely. In 2018, police treated the service as gambling on the grounds that it had operated without approval from financial authorities, referred CEO Cha Myung-hoon and others to prosecutors on charges of running a gambling den, and even booked 20 users who had traded more than 3 billion won as gamblers. The case closed about three years later, in 2021, with a no-charge disposition for lack of evidence, but since then no crypto exchange has had margin or futures trading on its radar.

- Tacit avoidance under self-regulation: Korean crypto exchanges are governed by self-regulation under the Digital Asset eXchange Alliance (DAXA), a body formed by the five major won-market exchanges. Its listing review criteria include opacity from de-identification, the likelihood of being a security, and the potential for use in money laundering. These criteria effectively push privacy coins that emphasize anonymity off the list and lead exchanges to avoid tokens that could be read as securities. Assets that might raise questions of being securities or gambling, such as exchange tokens or prediction-market tokens, are rarely seen on Korean exchanges for the same reason.

Taken together, nearly every new area that overseas exchanges are expanding into, that is, derivatives, tokenized stocks, and the listing of certain privacy and prediction-market tokens, is effectively blocked at Korean exchanges.

3. A Comparison With Overseas Exchanges

3.1 Have Korean Exchanges Lowered Their Listing Standards?

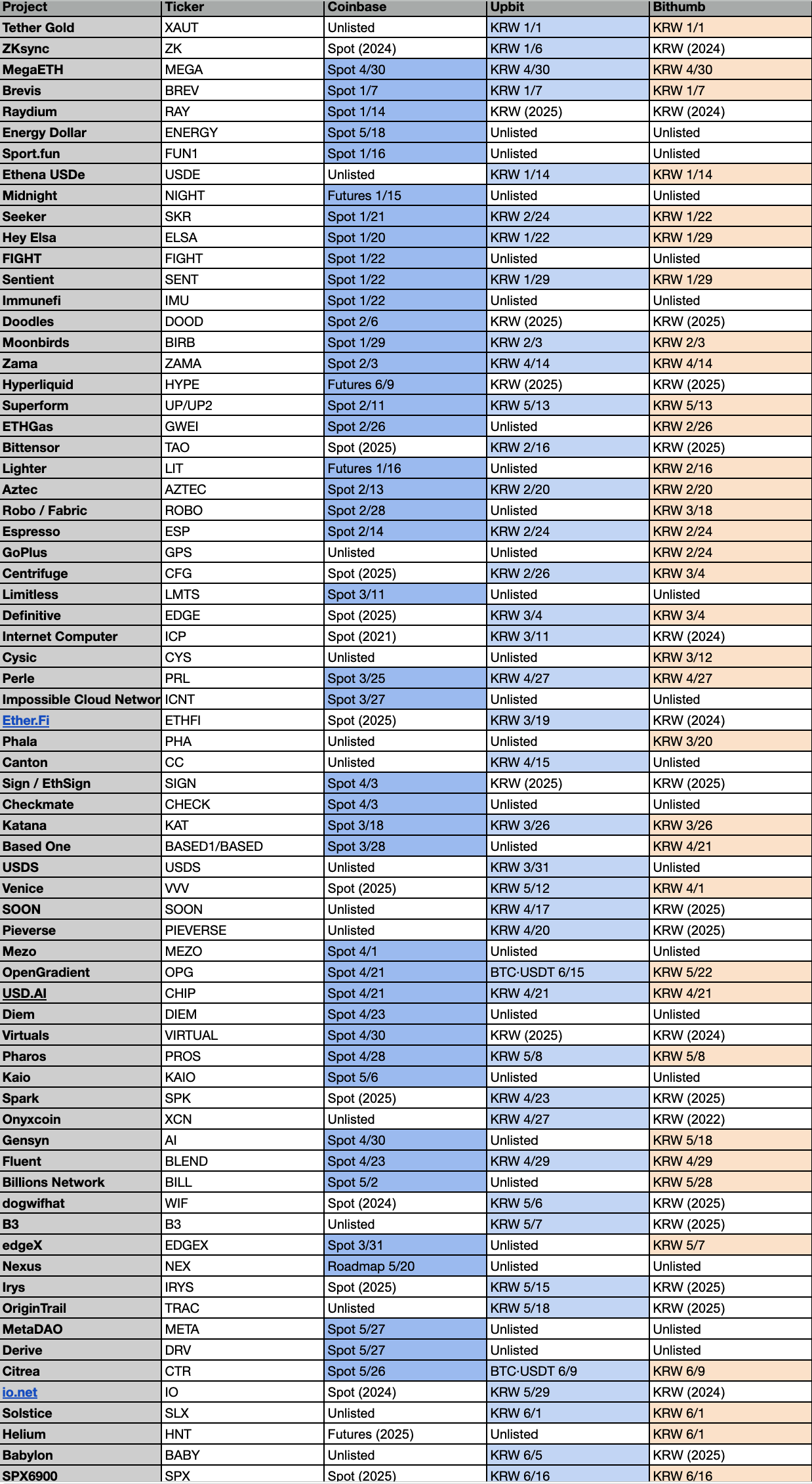

Source: Four Pillars (@c4lvin)

These listings prompted the charge that Upbit and Bithumb had loosened their review standards. The table here is my full survey of the tokens that Coinbase, Upbit, and Bithumb listed in 2026, and I want to examine that charge through the data.

On the raw number of listings, Coinbase leads. Coinbase listed many assets that the two Korean exchanges did not, and a large share of them were offered not only on spot but on futures as well, giving exposure earlier than other venues. On frequency and timing alone, Coinbase is in fact the more aggressive.

In 2026, a sizable share of the new won-market tokens Upbit listed were already on Bithumb. Bittensor (TAO), Internet Computer (ICP), Ether.fi (ETHFI), io.net, dogwifhat, Spark (SPK), and Babylon are examples, most of them names that had not traded heavily on Bithumb. Rather than newly unearthed assets, they were tokens that already existed in the market and were listed after the fact, which likely fed the sense that the listings felt less fresh.

The real source of that perceived decline in quality is less a fall in standards themselves than a fading of the volume effect that a listing used to create. In an environment where the volume drawn by a single listing dries up quickly and fresh assets worth listing grow scarce, exchanges keep their listing pace up by following Bithumb's existing tokens onto their own boards. The grumbling among Korean users is, in the end, less a complaint about any one name than a sense of the convenience gap they feel when comparing themselves with other markets that enjoy newer products like tokenized stocks.

3.2 As Overseas Exchanges Aim to Become Everything Exchanges, Korean Exchanges...

At the same moment, the path the large overseas exchanges are walking runs in the opposite direction. They are reaching beyond the fence of virtual assets toward what is called the "Everything Exchange," a single app in which every asset can be traded.

The most overt of them is Coinbase. In its fourth-quarter 2025 shareholder letter, Coinbase said it had begun trading stocks and ETFs inside the app on top of crypto and derivatives, opening roughly 3,000 names to early users, with the aim of binding traditional and digital assets into one portfolio experience. The same letter also stressed that it had become the first in the industry to launch a 24-hour U.S. perpetual-style product, lifting its share of the derivatives market.

Binance is more direct still. From June 1, 2026, it opened U.S. stock trading to eligible users, giving direct access to more than 7,000 U.S.-listed stocks and ETFs. On top of that, it rolled out bStocks, which tokenize U.S. stocks one to one, settle in stablecoins, can be withdrawn to a self-custody wallet, and trade around the clock.

Bybit, for its part, joined the xStocks Alliance, a coalition for tokenized stocks, and handles tokenized stocks created by a regulated Swiss issuer. These price-tracking tokens are backed by real shares and trade 24 hours a day using stablecoins.

Some venues have put tokenized stocks front and center. Bybit joined the xStocks Alliance and handles tokenized stocks created by a regulated Swiss issuer; backed by real shares, these price-tracking tokens trade around the clock using stablecoins. Kraken's tokenized-stock product, xStocks, holds more than 100 U.S. stocks and ETFs, has passed tens of billions of dollars in cumulative volume, and aims to grow to over 500 names by the end of 2026. Gemini offers fee-free, 24-hour tokenized stocks in some European countries, and Robinhood offers stock tokens in Europe that track the underlying shares.

The stage where this gap between the domestic and overseas trading environments showed most dramatically was the SpaceX listing itself. For overseas exchanges, this listing was a test of the tokenized-stock race.

Before SpaceX even began trading on the Nasdaq, four kinds of tokenized products were already running. Ondo Finance, Kraken, and Solana-based Backpack each put out a tokenized SpaceX, and Hyperliquid had pre-listing perpetual futures open. Bybit, too, chose SpaceX as the first product of its tokenized-IPO access service, opening spot trading in time for the listing day. In the 24 hours after listing, SpaceX-related trades across the entire crypto market reached about 9 billion dollars, of which 5.6 billion changed hands on Binance alone.

By contrast, there was no place for Korean crypto exchanges on this stage. Neither tokenized stocks, nor perpetual futures, nor any product tracking SpaceX was permitted at home. While the world's major exchanges traded billions of dollars on the same narrative, Korean crypto exchanges had effectively no channel to join the flow.

4. Implications

For an exchange that cannot compete on the range of products it offers, the remaining battleground is listing. Korean exchanges' income rests, in practice, on spot trading fees. In a structure where they can handle neither derivatives, nor stocks, nor tokenized securities, the only real way to lift volume is to list, at the right moment, the names that catch investors' eyes.

The strict regulation of Korea's crypto exchanges was designed to protect investors. It treated margin trading, where leverage magnifies losses, as effectively gambling and shut it out; it filtered out security tokens with opaque rights structures; and it pushed assets prone to money laundering or price manipulation off the listing review. Yet as this protective frame stripped the exchanges of revenue streams and product lines one by one, the only lever left to them became spot listing. And the drier volume becomes, the more that lever gets pulled toward higher-profile, and therefore more speculative, names. Protection at the product stage ends up, at the listing stage, encouraging a tilt toward speculative assets. What we saw this time is just one scene of that tilt surfacing.

The deeper problem is that even this protection does not fully work. Domestic investors who want perpetual futures or tokenized stocks do not simply give up the demand. They move to overseas platforms like Binance, Bybit, and Hyperliquid. In fact, every venue that ran tokenized products and pre-listing perpetual futures around the SpaceX listing was outside the country. In other words, regulation does not remove the risky trading itself; it pushes it out beyond a market that Korean authorities cannot supervise. When taxation and cross-border information exchange (CARF) take full effect in 2027, the scale of this offshore trading will show up in the data, but that will be closer to confirming after the fact what is already happening. In the end, investors take on the speculative exposure anyway while losing the domestic safeguards, and Korean exchanges lose the income those trades would have brought.

This structure also leaves the exchanges themselves frail. A single engine, where nearly all revenue comes from trading fees, is fully exposed to the volume cycle. While Coinbase spreads its income across custody, stablecoins, tokenized stocks, and derivatives to cushion the downcycle, Korean exchanges must absorb the same cycle head-on with one product. As this gap stacks up quarter after quarter, it turns into a difference in capacity to invest and in product competitiveness, and that burden returns, again, as the convenience gap domestic users feel.

Of course, the Korean government is also putting real effort into building out crypto regulation. The fact that the second phase of the Digital Asset Basic Act, the institutionalization of security token offerings (STOs), the approval of corporate trading, a won stablecoin, and spot ETFs are all on the table at once in 2026 shows this plainly. Yet even if these new products open, they are likely to be assigned not to today's crypto exchanges but to existing licensed institutions such as securities firms and electronic registration agencies.

Stock brokerage, that is, investment brokerage under the Capital Markets Act, is a licensed business in the first place, one that can only be carried out with a financial investment business license from the Financial Services Commission. Upbit and Bithumb are merely registered as "virtual asset service providers" under the Specified Financial Transaction Information Act and the Virtual Asset User Protection Act; they do not hold this license. For an exchange to broker stocks itself, it would have to pass a separate gate with capital requirements and a review of major-shareholder eligibility, and the so-called "separation of finance and crypto," the stance against mixing traditional finance and virtual assets within one company, has long blocked that entry.

So the convergence actually under way is not exchanges becoming securities firms, but securities firms and banks buying stakes in exchanges and pulling them under one umbrella. In 2026, Hanwha Investment & Securities raised its stake in Dunamu to 9.84 percent to become the third-largest shareholder, while Hana Financial Group took 6.55 percent and Samsung Securities, Samsung Card, and Samsung SDS took 4 percent. Korbit was acquired by Mirae Asset Group, and Korea Investment & Securities signed a strategic equity investment to take a 20 percent stake in Coinone, becoming its third-largest shareholder. With financial authorities turning cautious on, and leaning toward easing, the separation of finance and crypto, such alliances are multiplying fast.

Will Korea leave open the possibility, as seen abroad, of a crypto exchange growing into an "Everything Exchange"? I think that possibility is very slim. Stock and securities functions will flow to licensed securities affiliates, and the exchanges themselves are likely to stay within the fence of spot. That is why I believe that even if new products open, their channel is likely to be assigned to existing licensed institutions such as securities firms and electronic registration agencies rather than to crypto exchanges.

What I want to argue is not that regulation should be lifted right away. The problem is that a protective frame designed for one era is creating ever more invisible costs now, as the market moves quickly toward the convergence of assets. A crypto exchange operating in such a harsh environment will pass these costs on to users in a bear market like the present one, and that will lead, in the end, to the listing of short-lived tokens with one-off trading demand, just like today, creating more victims. I hope everyone recognizes this.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.