Table of Contents

- Key Takeaways

- 1. Introduction

- 2. What the $635 Million Is

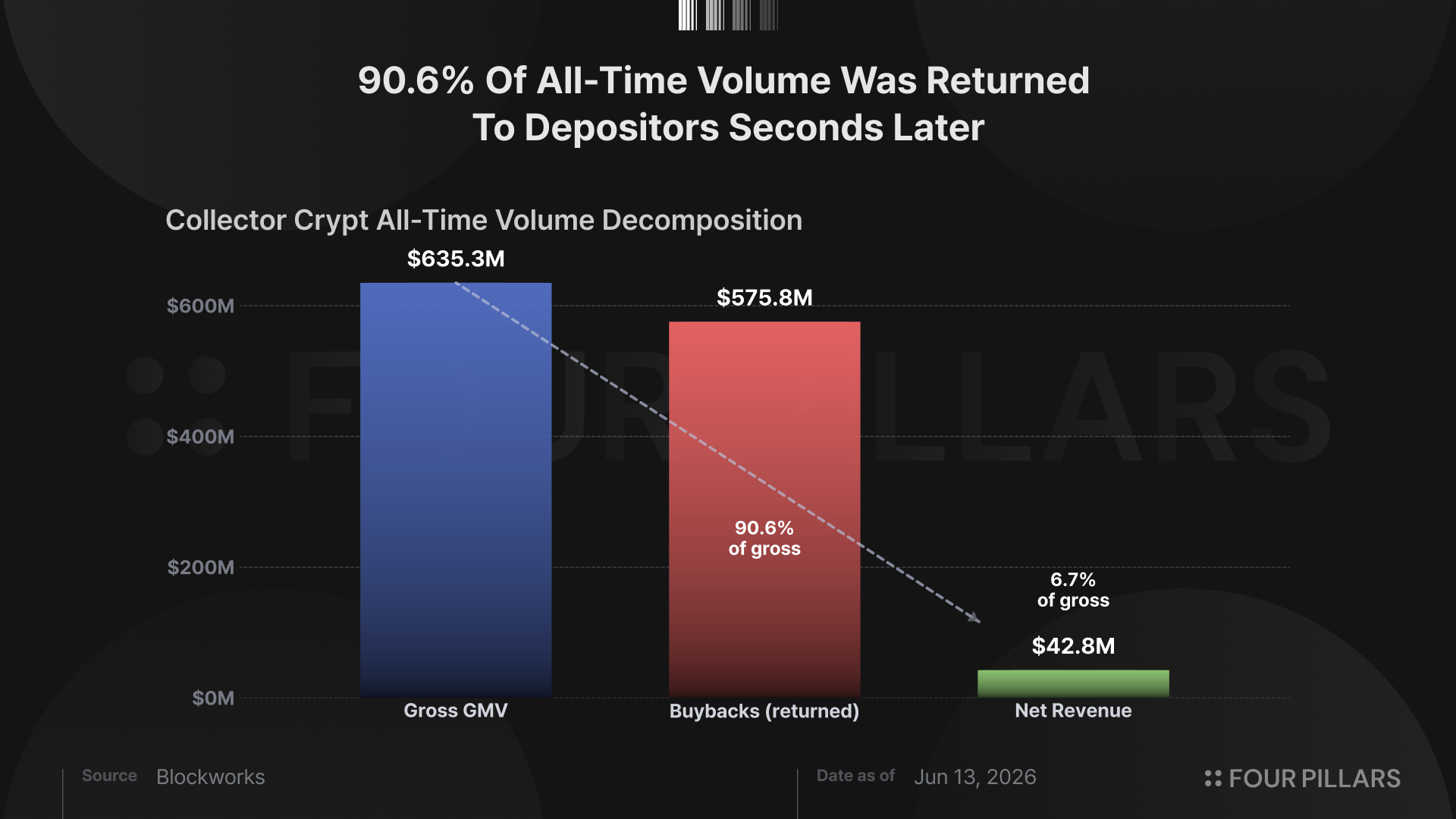

- 2.1 90.6% of All-Time Volume Was Returned to the Users Who Deposited It, Seconds Later

- 2.2 The Volume Is Concentrated in a Few Dozen Wallets

- 3. The Collector Market Hasn’t Arrived

- 3.1 The Bull Case

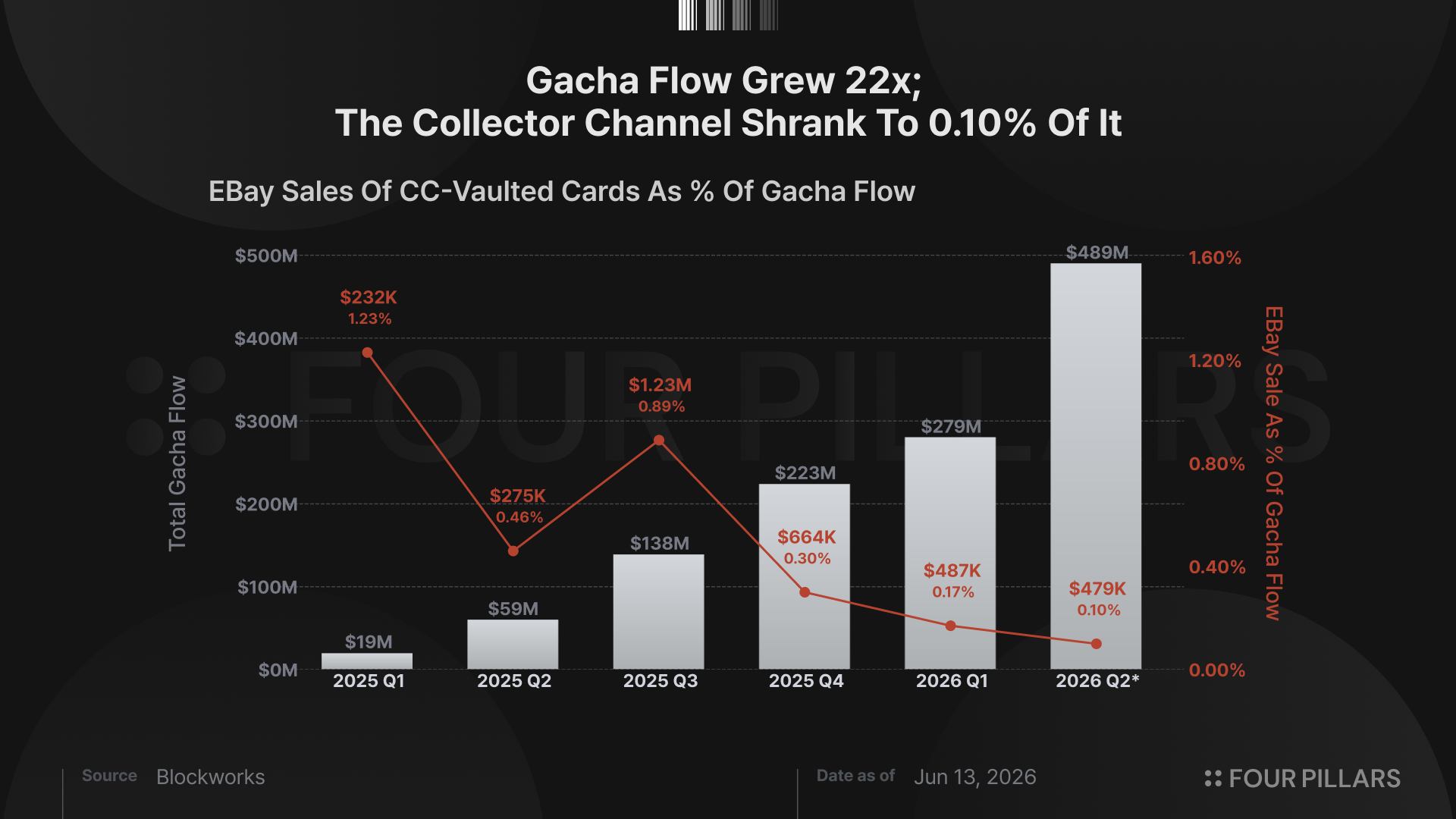

- 3.2 Secondary Trading Below 1%, eBay Share Down 12x

- 4. What the Token Gets

- 4.1 Margins Halved as Volume Tripled

- 4.2 Token Value Accrual Totals $56,000 in Burns and an $887,000 Buyback

- 5. Conclusion

Researcher

Related Projects

Key Takeaways

- Of CC's $635 million in all-time gross revenue, 90.6% was returned to users as instant card buybacks, leaving $43 million in net revenue at a 6.7% hold rate.

- Secondary trading across every channel, eBay plus peer-to-peer marketplace, totals under $5 million, and the eBay share of gacha flow has fallen from 1.23% to 0.10% over six quarters.

- Total token value accrual across burns and buybacks amounts to $1.4 million, or 3.4% of net revenue, while the operational wallet has off-ramped $45.7 million in USDC.

- Net margins halved from 11.2% to 5.8% as volume tripled into high-tier packs where the house edge is thinnest, and each new denomination ladder step pulls the blended margin lower.

- The ~$535 million FDV prices CARDS at 7.3x net revenue for a margin-compressing casino with roughly 420 daily players, a 20.5% float, and 72% insider supply vesting through November 2027.

1. Introduction

You deposit $1,000 into Collector Crypt, open a Grail pack, and receive a tokenized Pokémon card the platform values at $1,015. It looks like you came out ahead. Turbo mode fires automatically, selling the card back to the protocol at the 93% buyback rate, and $944 lands in your wallet. The whole cycle takes seconds.

That loop, repeated at industrial speed by a few hundred wallets, has generated $635 million in gross volume and a ~$535 million fully diluted valuation for the CARDS token. This piece breaks down what that volume consists of, whether the collector economy priced into the token is arriving, and what share of the revenue the token has claim on.

2. What the $635 Million Is

2.1 90.6% of All-Time Volume Was Returned to the Users Who Deposited It, Seconds Later

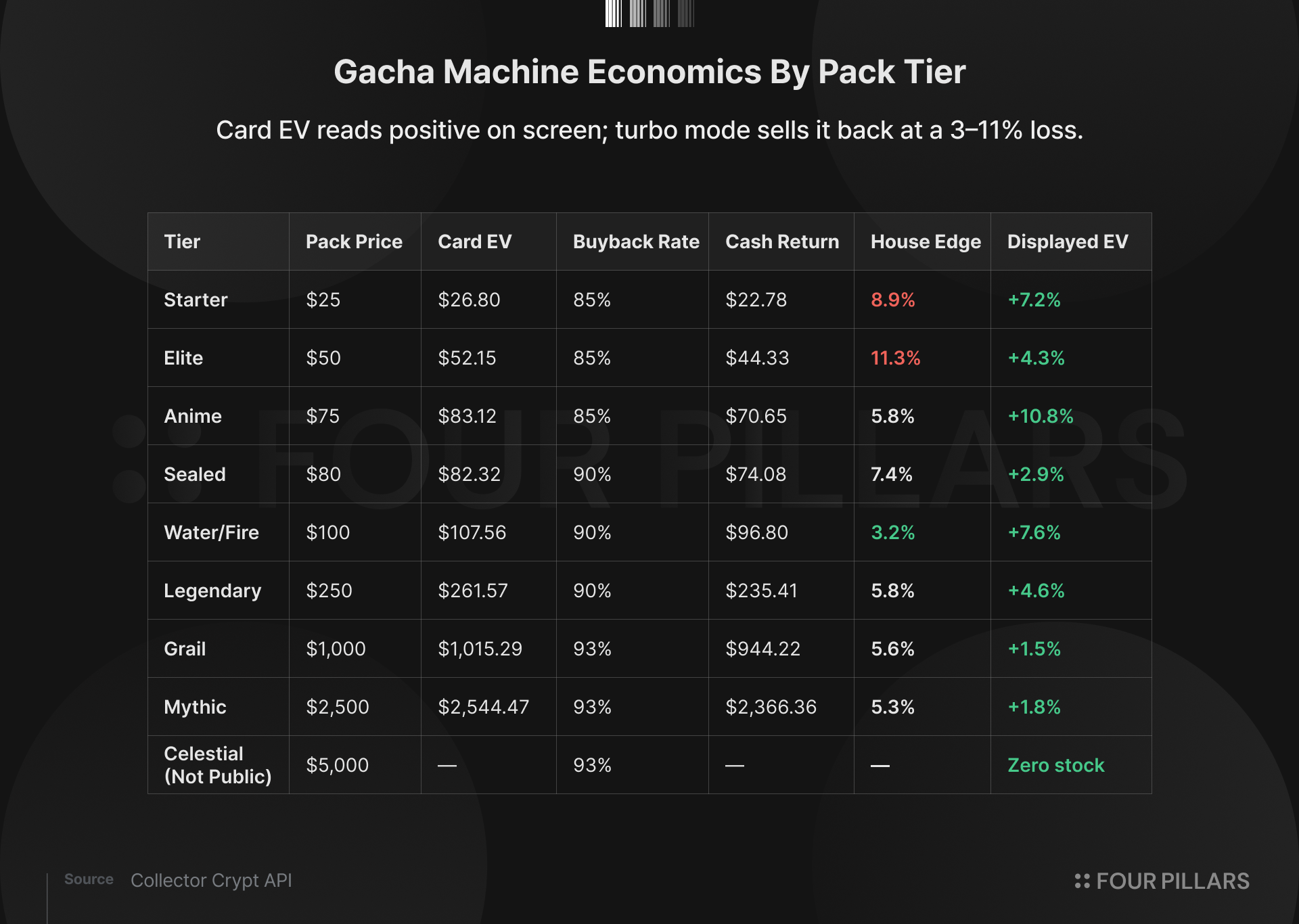

CC’s core product is a gacha machine. Users deposit USDC, buy a randomized pack ($25 to $2,500, with a $5,000 tier in the API but not yet public), and receive card NFTs backed by physical graded cards in vault custody. Each card carries an “insured value,” and the platform offers instant repurchase at 85 to 93% of that value.

The repurchase is the default, not the exception. All 33 machine configurations in CC’s API carry turboMode: true. Cards are sold back to the protocol automatically, and the user receives USDC back minus the haircut, typically within seconds.

Per Blockworks daily data through June 13, all-time gross revenue totals $635 million, of which $576 million was returned to users as card buybacks, leaving $43 million in net revenue at a 6.7% hold rate. “Buyback” here does not mean token buyback. It means the platform repurchasing the cards it just sold, recycling the same deposits into the next spin. On the ATH day of June 11, the machine processed $10.6 million gross and retained $881,000, an 8.3% hold.

The DeFiLlama adapter source code confirms the decomposition. It defines dailyFees = pack_purchases + royalties - buybacks, meaning the ~$52 million annualized fee figure on DeFiLlama’s dashboard is already net of buybacks. It also defines dailyVolume = pack_purchases, which is gross spend before recycling. This is the number that appears on protocol volume leaderboards.

2.2 The Volume Is Concentrated in a Few Dozen Wallets

Blockworks counts 23,333 cumulative users all-time. In May 2026 the platform averaged about 420 daily active users against $3.3 million in average daily volume, roughly $7,800 per active user per day. Even if 400 of those 420 each spent $1,000 daily, the remaining 20 wallets would still account for $2.9 million, or 87% of total volume. Extreme concentration is a mathematical necessity of the averages.

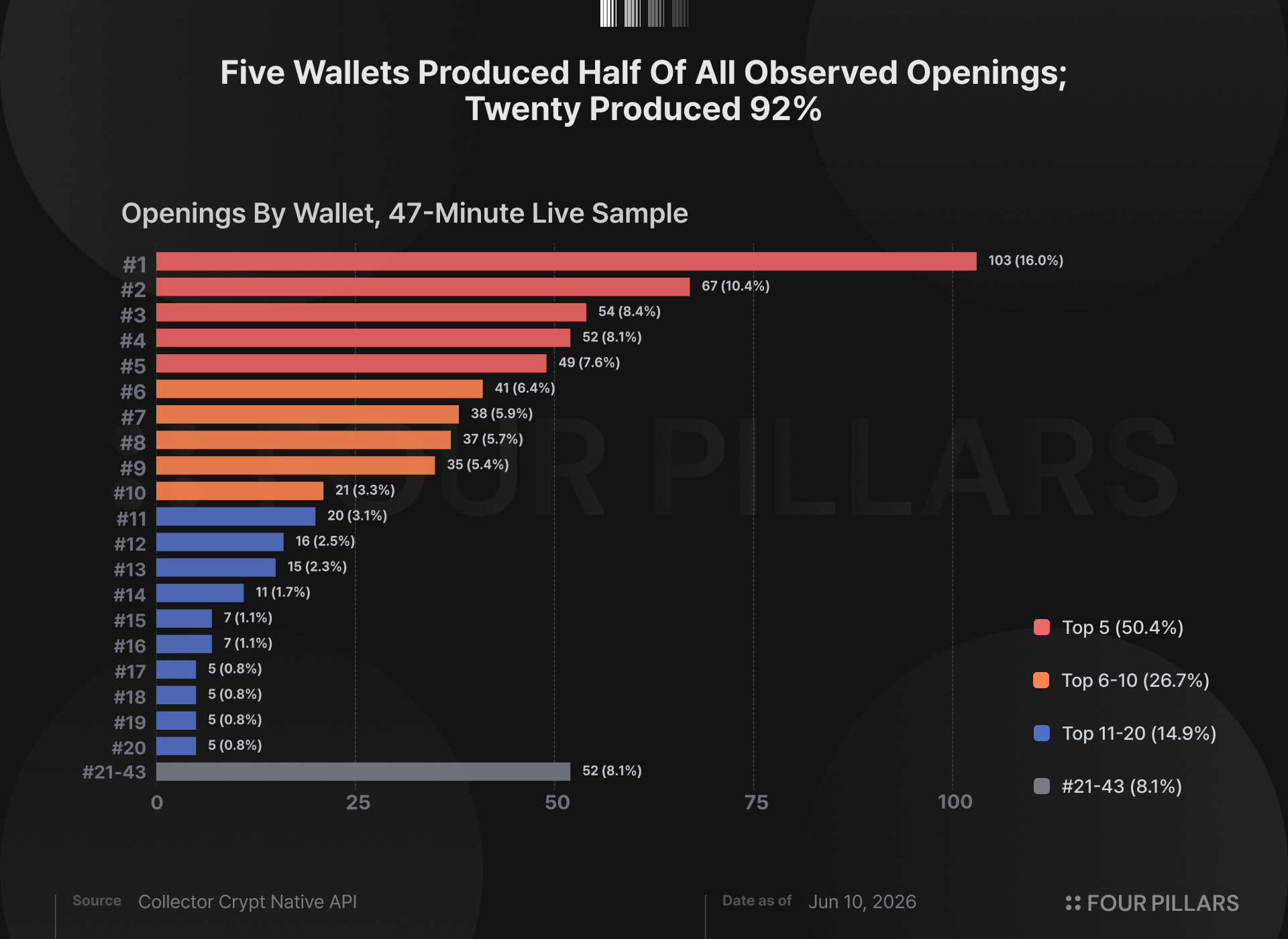

Observed activity matches. We polled CC’s public winner feed 20 times over 47 minutes on June 10, deduplicating by NFT address. The sample contains 645 pack openings from 43 wallets. The top five wallets produced 50.4% of openings, the top ten 77.1%, and the top twenty 91.9%. The most active wallet alone produced 103 openings, 16% of the total.

This is a 47-minute window, not an all-time distribution. But the averages and the sample point the same direction. The $635 million is a casino with a 6.7% hold, fed at industrial speed by a few dozen high-velocity players.

3. The Collector Market Hasn’t Arrived

3.1 The Bull Case

The strongest version deserves stating. The buyback cycle is the product. Like pachinko, the spin itself is the entertainment, the 85 to 93% return rate means users lose slowly, and instant liquidity on vaulted physical cards is a product innovation. As consumer design, this is defensible.

That said, the machine configurations show what the design optimizes for. CC controls two variables independently, the insured values assigned to cards and the buyback rate at which turbo mode auto-sells them back. The tier ranges and stock in the vault are configured so the probability-weighted expected card value lands above the pack price. The buyback rate then haircuts that value below it. For example, A $1,000 Grail pack displays an expected card value of $1,015, and the user sees a +1.5% proposition. Turbo mode fires at the 93% buyback rate, returning $944 in cash. Card EV sits above pack price, pack price sits above cash return, and the user sees the first comparison while the platform collects on the second. The same structure holds across all tiers, with realized edges from 3.2% to 11.2%.

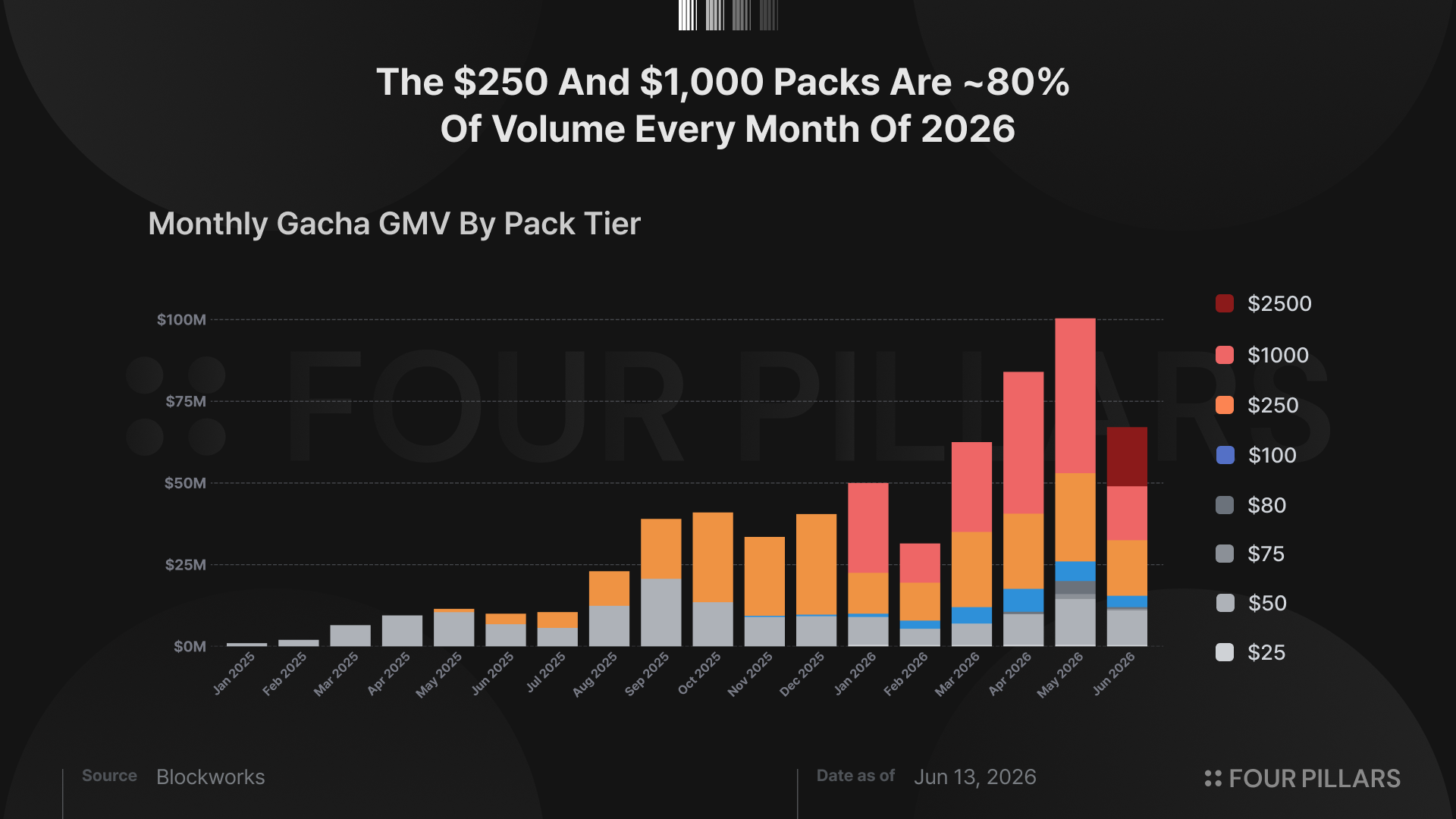

The spending mix confirms the user type. The $250 and $1,000 tiers made up about 80% of volume in every month of 2026 (79.4% in January, 80.6% in March, 79.4% in April). Collectors buy specific cards at specific prices to complete specific sets. A distribution dominated by $1,000 randomized packs is a high-roller distribution.

3.2 Secondary Trading Below 1%, eBay Share Down 12x

If collectors used this platform, they would trade with each other, and the cards would circulate into the broader market. CC’s data tracks both, and both read near zero.

On-platform, all-time marketplace royalties total $133,000. Of $6.9 million in lifetime marketplace volume, only $823,000 was actual peer-to-peer trading. The rest is buyback flow and legacy V1 volume.

Off-platform, Blockworks tracks eBay sales of CC-vaulted cards. The all-time total is $3.4 million, and the trend is the finding. As a share of gacha flow, eBay ran 1.23% in Q1 2025, 0.46% in Q2, 0.89% in Q3, 0.30% in Q4, 0.17% in Q1 2026, and 0.10% in Q2 2026. Gacha volume grew roughly twenty-five-fold over that period. The collector channel barely moved in absolute terms and collapsed twelvefold as a share.

Of the $635 million in card value generated by the platform, $18.5 million has been redeemed for physical cards, just 2.9%. The remaining 97% was sold back to the protocol through auto-sellback, most of it within seconds.

Combined, genuine secondary activity across every channel, eBay plus peer-to-peer marketplace trades, totals under $5 million against $635 million of gacha throughput. The standard bull rebuttal is “it’s early,” but the quarterly eBay series answers it. The platform is not early on a path toward collector behavior. It is six quarters into moving measurably away from it.

Turbo mode eliminates the dwell time that collector platforms monetize, the browsing and comparing and set-completing that builds a secondary market. The design optimizes for cycle speed, not discovery. These are different products.

4. What the Token Gets

CC's revenue flows through three layers. Users deposit USDC for gacha packs, receive randomized card NFTs, and in nearly every case auto-sell them back at the 85 to 93% buyback rate. The platform retains the 7 to 15% spread as net revenue. Minor additional lines include a 2% royalty on marketplace trades and a 2% fee when users redeem their NFT for the physical card. All net revenue flows to the operational treasury, which funds card inventory acquisition, USDC off-ramps, and as of June 2026, a small token buyback program.

4.1 Margins Halved as Volume Tripled

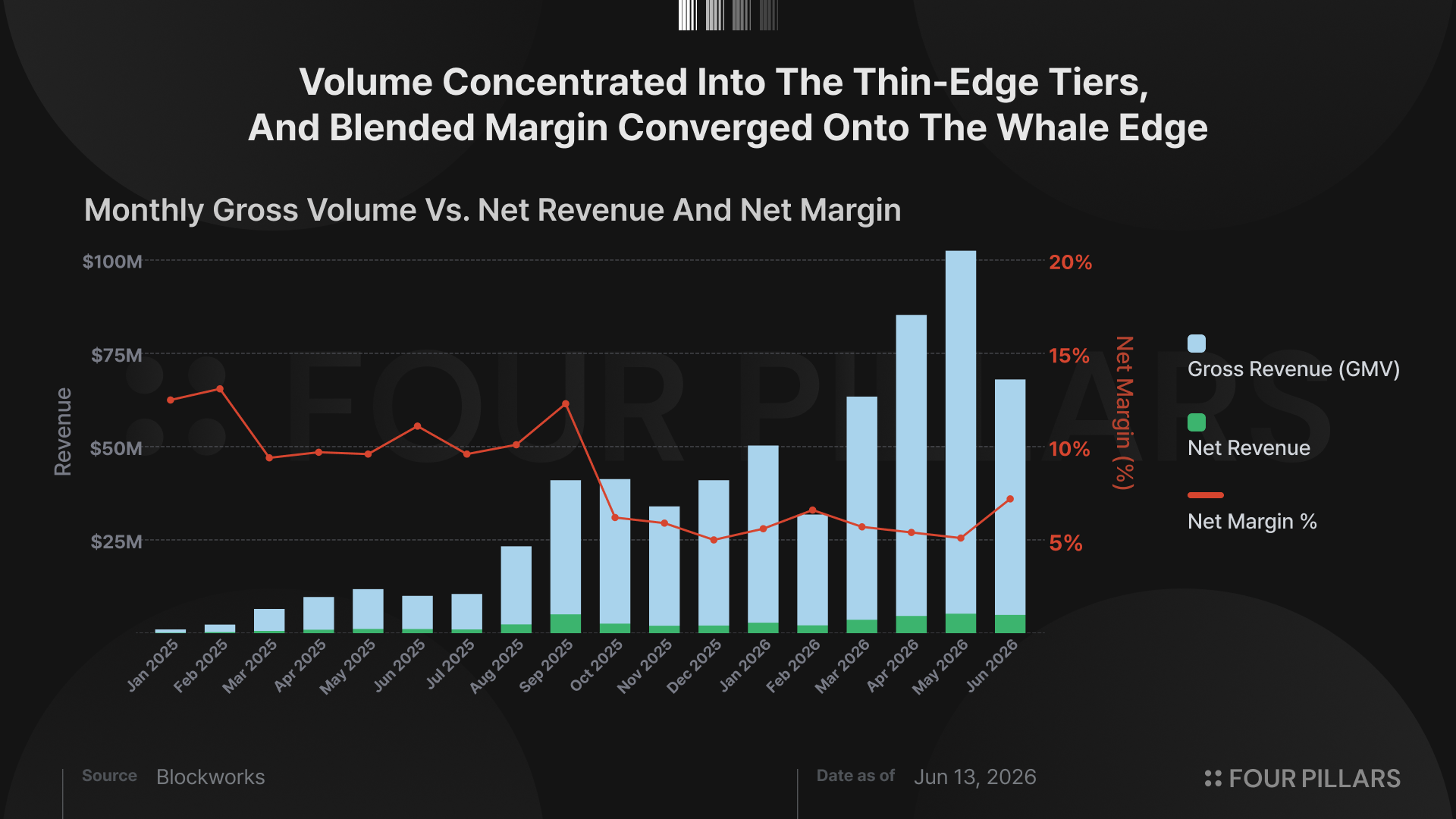

Per Blockworks daily data, Q3 2025 produced $75.0 million gross at an 11.2% net margin. Q4 2025 produced $116.3 million at 5.7%. Q1 2026 produced $145.9 million at 5.9%. Q2 2026 through June 13 produced $256.0 million at 5.8%.

The compression is structural. The house edge is thinnest exactly where the volume is, roughly 5% on the $250 and $1,000 packs versus 9 to 11% on the $25 and $50 tiers, because high-volume players will not cycle six figures at an 11% haircut. As volume concentrated into high tiers, the blended margin converged onto the high-tier edge. The marginal dollar of growth comes from the players the platform keeps the least of.

The $2,500 Mythic pack launched on June 10 carries a 6.4% house edge. A $5,000 Celestial pack already sits in the API at zero stock. Each step up the denomination ladder keeps gross volume growing while pulling the blended margin toward the high-tier floor.

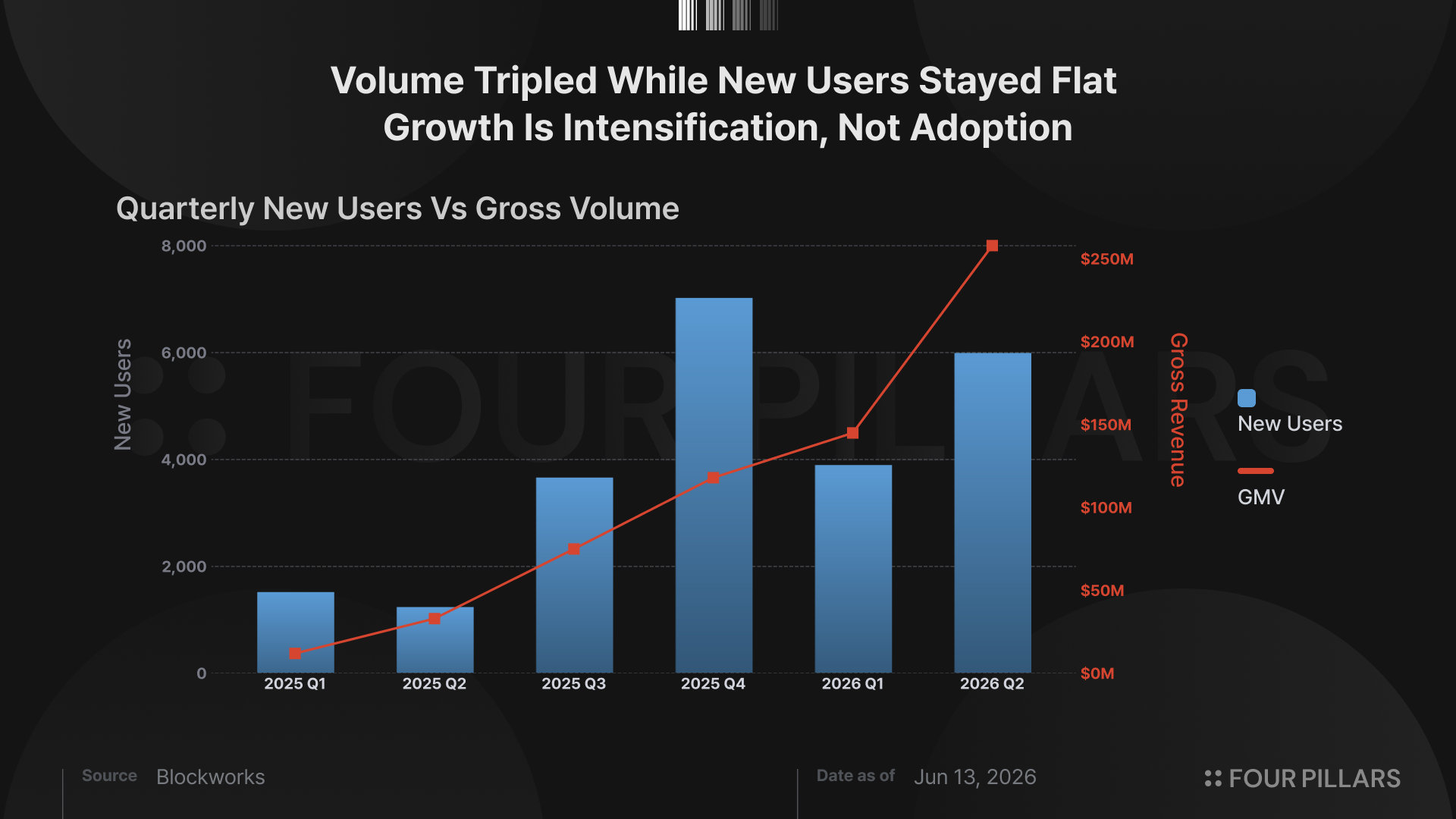

User data confirms the growth is intensification, not broadening adoption. New users across the last four quarters ran 3,668, then 7,013, then 3,886, then 5,982 (Q2 through June 13), roughly flat while volume more than tripled. May 2026 added 2,593 new users, but average daily active users rose only from about 280 in April to 420 in May. Most newcomers churned within days.

4.2 Token Value Accrual Totals $56,000 in Burns and an $887,000 Buyback

294,203 CARDS tokens have been burned since launch, representing 0.015% of supply and worth approximately $55,900 over 9.5 months. CC's documentation does not specify the mechanism that triggers these burns, and the decline tracks the collapse in marketplace activity. May 2026 burned 372 tokens. June has burned 21, worth $4.

On June 13, Lukas Ruppert from Maelstrom published on-chain evidence linking token purchases to wallets connected to CC’s operational infrastructure. Ruppert traced a wallet chain from CC’s known operational hub (DFEst) through Kraken to a DCA bot, and identified connected wallets with pack-opening history. He stops short of confirming team control, writing that “if these wallets are indeed team-controlled, the significance extends beyond the purchases themselves,” but the circumstantial case is strong.

The on-chain trail shows two events. On May 12, the CARDS Aggregator wallet paid $500,000 through a Fireblocks escrow to settle with pre-seed investor GSR, receiving 4,045,013 CARDS at roughly $0.124 per token. Then on June 10 and 11, a newly created wallet funded through Kraken began market-buying CARDS via a DCA bot with two parallel clip streams at roughly $625 and $587 every two to six minutes. By June 12 the bot had deployed $159,000 and accumulated 599,104 CARDS, with $728,000 in remaining budget.

Counting every form of token value accrual, burns ($55,900), the GSR settlement ($500,000), and the full DCA budget including undeployed funds ($887,000), the total comes to $1.4 million, or 3.4% of the platform’s $43 million in all-time net revenue. At the current Q2 run rate of ~$73 million annualized, the entire DCA budget represents 1.2% of one year’s net revenue.

The wallet Ruppert identifies as CC’s operational hub has off-ramped $45.7 million in USDC over the platform’s life, with $8.5 million since May 2026 alone. Whether or not these wallets are team-controlled, the disproportion is worth noting. $1.4 million directed toward the token, $45.7 million directed away from it. The buyback could be the start of sustained value accrual, but at the same time nothing in the program is on-chain, automated, or committed, so it could also stop tomorrow.

At 5.8% net margin, scaling token buybacks meaningfully is zero-sum with the operational wallet’s revenue. The buyback rate (85 to 93%) determines the player’s cost per cycle, and lowering it loses volume, so the total margin is set by player tolerance. Within that margin, token buybacks and operational off-ramps compete for the same dollars.

Even at face value, roughly $73 million annualized off the Q2 run rate, the ~$535 million FDV prices CARDS at 7.3x net revenue for a margin-compressing casino with about 420 daily players and a revenue base concentrated enough that a single wallet’s exit can move daily volume by double-digit percentages.

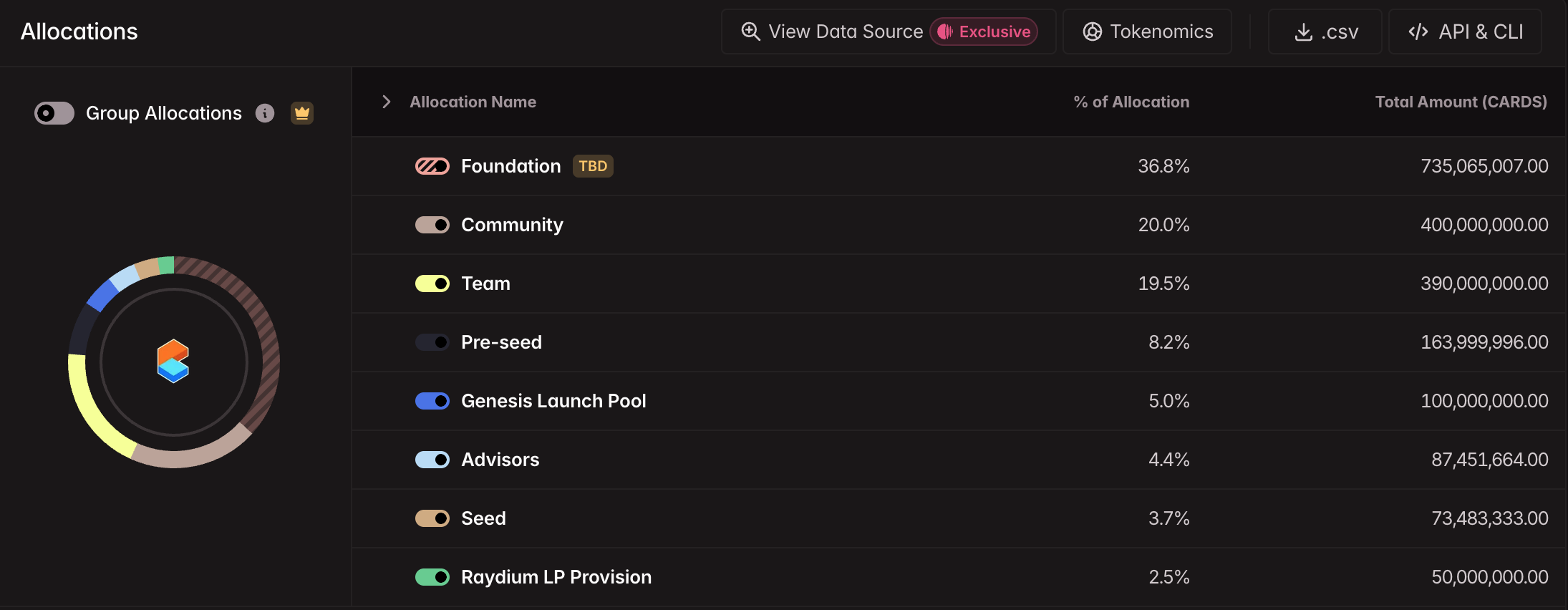

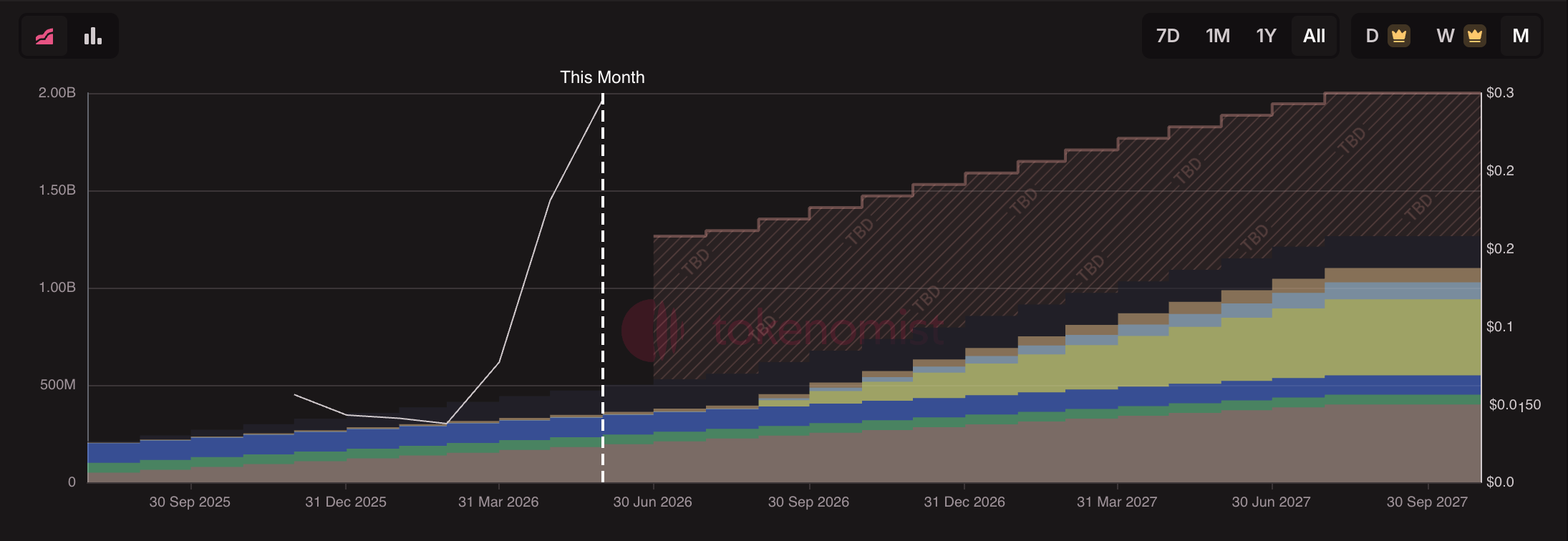

The ~$110 million circulating market cap reflects a 20.5% float, with 410 million of 2 billion total supply in circulation. The remaining 79.5% vests on a public schedule running through November 2027, with the next unlock on June 29 releasing 28.84 million tokens across four allocations. Insider allocations total 72% of supply across Foundation (36.75%), Team (19.5%), Pre-Seed (8.2%), Advisors (4.37%), and Seed (3.67%), with Community (20%), Genesis Launch Pool (5%), and Raydium LP (2.5%) making up the rest.

Source: tokenomist.ai

5. Conclusion

CC built a working product with physical cards in insured vaults, and it found product-market fit with a small number of high-velocity gamblers. Our view would change if marketplace royalties inflected toward genuine peer-to-peer trade, if the eBay share reversed its six-quarter decline, or if the buyback program scaled beyond 3.4% of net revenue. None of these is visible yet.

What is currently visible is total token value accrual of $1.4 million, 3.4% of all-time net revenue, against a $110 million market cap ($535 million FDV). An operational wallet that has off-ramped $45.7 million through the same infrastructure that funds the $887,000 buyback. A collector channel that has shrunk every quarter since launch. And above the 20.5% float, insider allocations totaling 72% of supply vesting through November 2027.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.