Table of Contents

Researcher

Key Takeaways

- Financial privacy may become more valuable, but that does not mean users will want exposure to a volatile privacy coin.

- Shielded supply and quantum-readiness are powerful narrative accelerants, not evidence of durable monetary demand.

- ZEC may work as a trade, but the multi-cycle monetary asset thesis remains unproven

ZEC is one of the hottest narrative trades in crypto right now.

It has Bitcoin-like scarcity, low relative market cap, famous endorsers (Barry Silbert, Mert, Ansem, Tushar Jain, Arthur Hayes, Raoul Paul, etc.), privacy/AI/quantum macro hooks, institutional breadcrumbs, rising shielded supply chart, low prior expectations, everyone underowned, and an easy “10% of BTC” upside meme. The setup is strong and the story is simple. Markets like simple stories.

The bull case is strongest when framed as monetary insurance, not payments adoption. The claim is not that everyone starts buying coffee with shielded ZEC. The claim is that private digital bearer money becomes a strategic asset in a world of onchain surveillance, AI-driven financial analysis, capital controls, debanking, and eventually quantum risk.

I still don’t buy it. The problem is value capture. Financial privacy may become more valuable, but that does not mean ZEC captures that value.

Users want private economic activity, not necessarily exposure to a volatile privacy coin. They may want private stablecoins, private wallets, private payment apps, private institutional rails, or private bank/tokenized-deposit systems. If privacy demand accrues to applications, stablecoins, wallets, or institutional rails, ZEC’s monetary premium is structurally capped.

The ZEC thesis asks the market to assume financial privacy becomes more valuable → ZEC captures that value. This is the leap I find hard to understand.

1. What is the Market Buying?

The sharpest ZEC thesis I can formulate is this:

“ZEC is a reflexive monetary-asset reboot where privacy, quantum-readiness, institutional accessibility, and Bitcoin fatigue converge into one scarce PoW asset. It does not need privacy payments to become mainstream immediately; it needs the market to reprice private digital bearer money from “dead niche” to “strategic monetary insurance.”

ZEC has three things that normally do not coexist.

- First, it has Bitcoin-like monetary packaging. Fixed 21 million supply, PoW issuance, long distribution history, no obvious new-chain VC unlock stink, and a simple “digital money” narrative.

- Second, it has a differentiated monetary property Bitcoin lacks: transaction privacy. Zcash shielded transactions can obscure sender, receiver, and amount, while transparent transactions remain available for exchange/custody/compliance flows. Bitcoin made digital scarcity credible, but not digital privacy.

- Third, it has an institutional-access path that Monero structurally struggles with. Optional privacy is politically weaker than mandatory privacy, but commercially stronger. Transparent ZEC can sit on CEXs, custody platforms, trusts, and potentially ETFs, while shielded ZEC can serve the private-money use case.

So theoretically ZEC is the privacy asset that institutions can touch, exchanges can list, miners can industrialize, and cypherpunks can still emotionally believe in. That combination is rare.

Bitcoin won scarcity, then became legible to the state. ETFs, corporate treasuries, sovereign holdings, custody, accounting, compliance, and Wall Street distribution made Bitcoin enormous. But that same success made Bitcoin less rebellious. Transparent UTXOs plus institutional custody mean Bitcoin is increasingly clean, monitored, and financialized.

ZEC enters as the “second monetary property” trade. Bitcoin is scarce public money. Zcash is scarce private money. This is why the “ZEC is what Bitcoin should have been” meme works. It is not technically perfect, but it is emotionally sharp. It lets people replay the early Bitcoin psychological trade: “Could you have held the weird cypherpunk money before institutions understood it?”

BTC’s success creates ZEC’s opening. The more Bitcoin becomes institutional reserve collateral, the more room there is for a parallel asset that carries the privacy/cypherpunk premium Bitcoin left behind.

2. The Core Flaw

The strongest counterargument is not “privacy does not matter.” Privacy obviously matters. The issue is that ZEC may be a bad way for the market to monetize that demand because privacy is not naturally captured by a scarce L1 monetary asset.

From first principles, users want private economic activity, not necessarily exposure to a volatile privacy coin. If someone wants confidentiality, they probably want private stablecoins, private bank rails, private payroll tools, private messaging payments, private wallets, or private exchange settlement. They do not obviously want to hold a high-volatility PoW asset.

Bitcoin captured scarcity because the asset itself was the product. You hold BTC because you want scarce, censorship-resistant, non-sovereign money. With privacy, the product may not be the asset. The product may be the privacy layer.

If so, ZEC’s monetary premium is structurally capped. The biggest privacy TAM may accrue to wallets, stablecoins, L2s, encrypted payment networks, private DeFi rails, compliance-preserving middleware, custodial apps, bank/tokenized-deposit systems, or even Bitcoin/Ethereum privacy upgrades.

3. Revealed Preference Is Weak

Markets price visible demand, not abstract virtue. People have known for years that public blockchains are surveillance machines. They still use them. They still buy memecoins from doxxed wallets, hold NFTs in public, bridge funds across traceable rails, and trade on CEXs.

The pain is obviously not immediate enough. Privacy behaves like insurance. Everyone agrees it is useful, but few people pay for it until after the disaster. ZEC is trying to monetize a future preference that users have consistently refused to reveal in the present.

A narrative can pump before adoption, but a monetary asset needs durable holders. If privacy remains mostly philosophical, ZEC remains a narrative trade rather than a structural repricing.

4. Optional Privacy is a Double Edged Sword

ZEC’s optional privacy is the reason institutions can touch it. Transparent ZEC can sit on exchanges, custody platforms, trusts, and potentially ETFs, while shielded ZEC preserves the private-money narrative. This is ZEC’s main advantage over Monero.

But it also makes the monetary thesis harder to underwrite. With Bitcoin, institutionalization did not weaken the core asset property. BTC became less rebellious, but it remained scarce. In fact, becoming legible to institutions strengthened the scarcity trade.

ZEC is different because privacy is not just the origin story. Privacy is the differentiation. If most institutional demand sits in transparent ZEC, the asset starts to look like Bitcoin-ish collateral with privacy optionality. If shielded usage becomes dominant, the same feature that gives ZEC its premium may become harder for exchanges, custodians, and allocators to support.

So the issue is that ZEC has to hold two narratives at once: compliant enough for institutions, private enough to deserve a monetary premium.

5. Weak Evidence

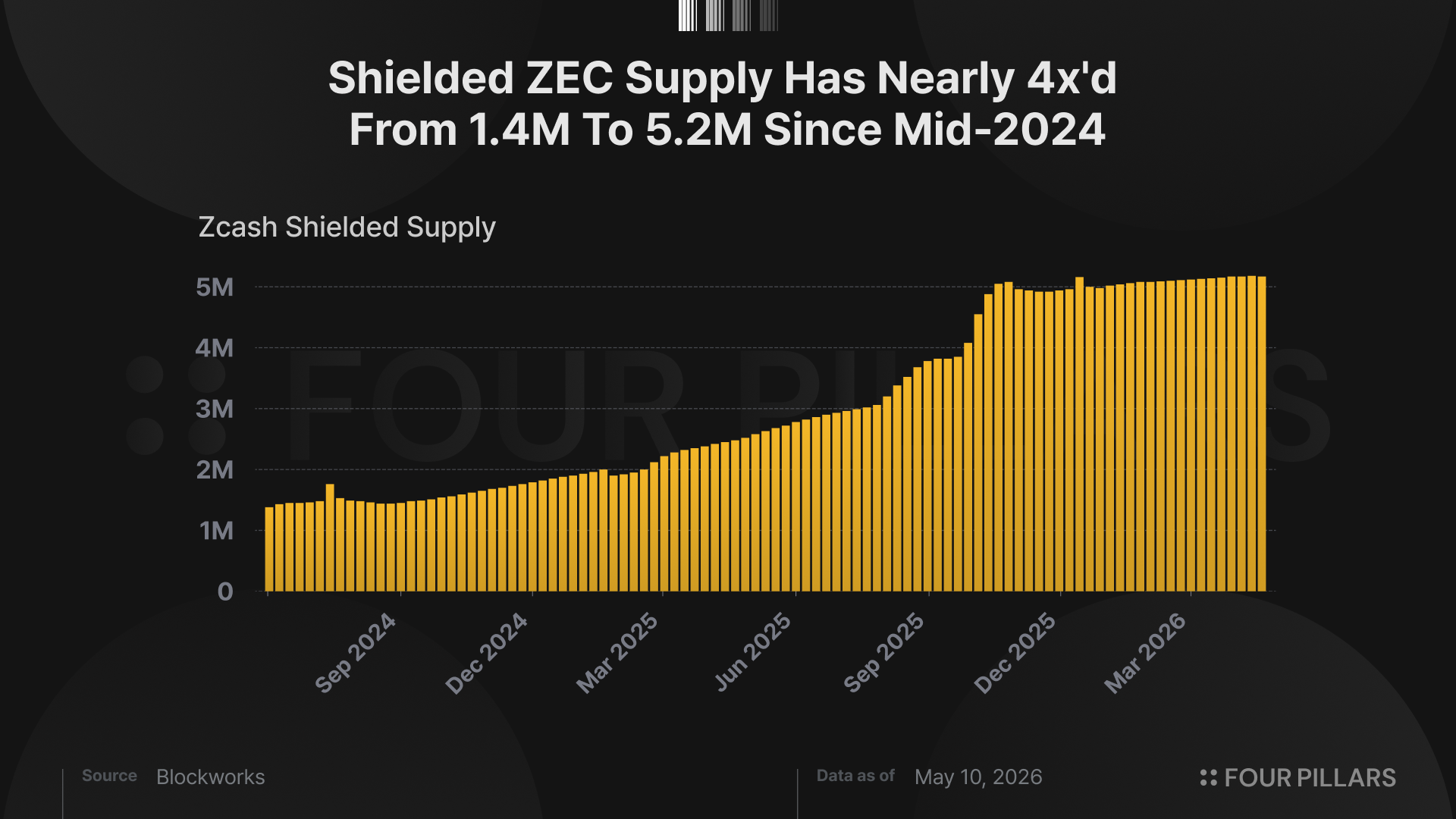

Rising shielded supply looks like proof that privacy demand is rising. But once CT tells everyone “shielded supply is the KPI,” rational holders will shield because it helps the narrative, signals ideological alignment, improves the chart everyone is watching, reduces visible float, and creates reflexive scarcity optics. That does not mean people are using ZEC as money. It may mean ZEC holders learned which metric pumps the asset.

Once a specific metric becomes a narrative target, it stops being so reliable. TVL, restaking deposits, DA blobs, bridged assets, active addresses, stablecoin supply, etc. all got gamed. So the question is: is shielded supply a revealed preference for private money, or coordinated holder behavior to support the trade?

Quantum is similar. It is easy to understand, scary, asymmetric, hard for Bitcoiners to dismiss completely, and tied to a visible roadmap.

It is a powerful narrative accelerant, but it is not yet a durable allocation reason. If quantum risk is too early, allocators ignore it. If it becomes imminent, the entire crypto market panics, and liquidity probably runs first to cash, gold, regulated custodians, and whatever Bitcoin migration path emerges.

If quantum becomes salient, every serious chain will accelerate post-quantum plans. Bitcoin is slow, but existential threats change coordination behavior. Ethereum, wallets, custodians, and institutions will also respond. Quantum gives ZEC a great story, but not necessarily durable monopoly value.

6. Conclusion

ZEC is a reflexive repricing of a real but over-abstracted problem. Financial privacy matters, but the market may be wrongly assuming that demand for privacy maps onto demand for a volatile scarce L1 asset. In practice, most users want private dollars, private payments, private wallets, and private institutional rails, not ZEC exposure.

Optional privacy gives ZEC exchange access, but it also weakens the purity of the monetary story. Rising shielded supply may reflect coordinated holder behavior rather than organic economic use. Quantum is a powerful narrative accelerant, but not yet a durable allocation reason. The current move may therefore be less “ZEC becomes private Bitcoin” and more “crypto found a perfect old-coin narrative with tight market structure and famous endorsers.”

As a narrative trade, ZEC is strong. As a multi-cycle privacy + quantum insurance asset, it is unproven. As a payments adoption thesis, it is weak.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.