Table of Contents

Researcher

Related Projects

Key Takeaways

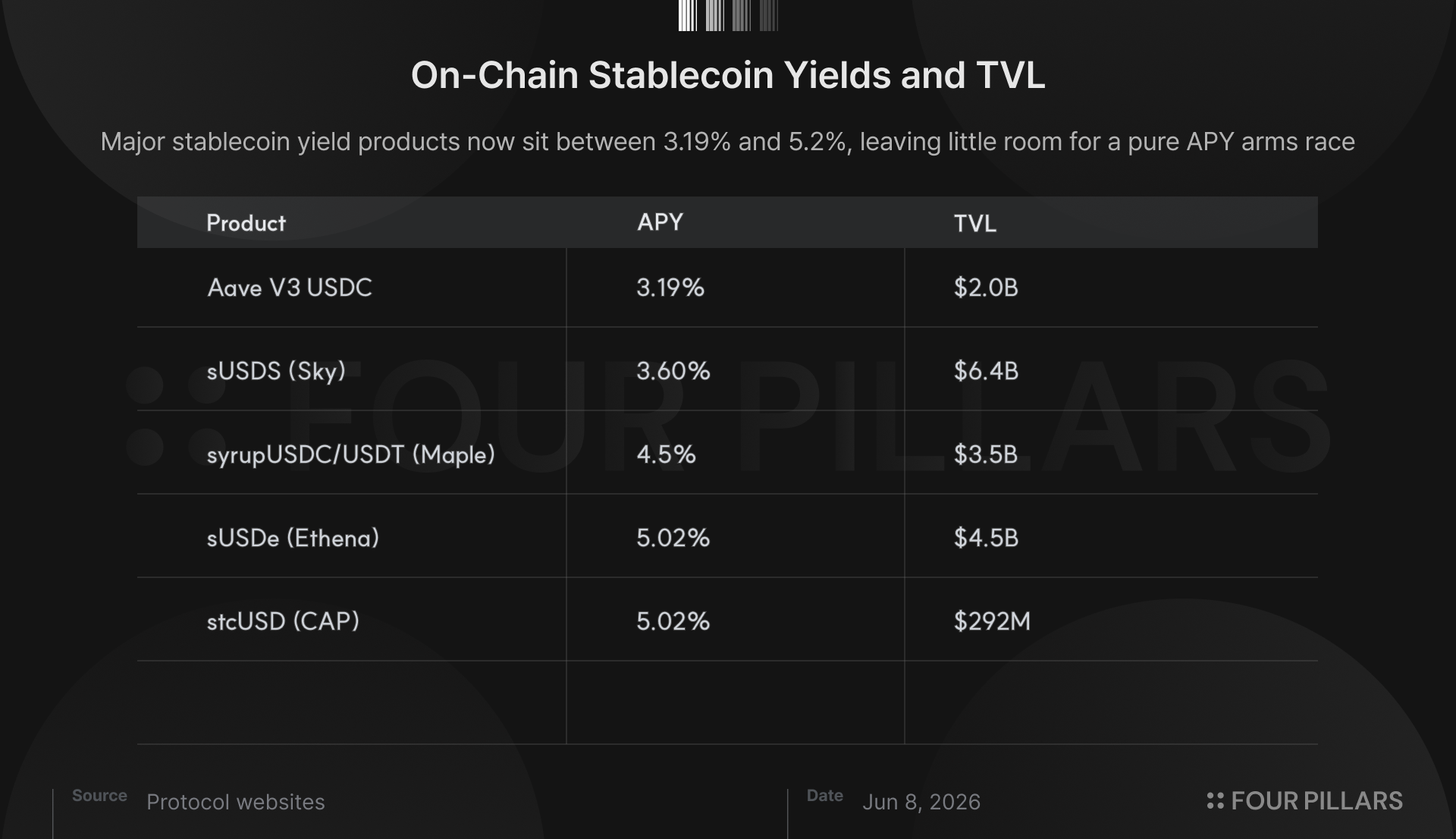

- Pure basis is losing its edge as funding rates compress and the trade commoditizes. The stablecoin yield set has now converged into a narrow band: Aave v3 USDC at 3.19%, Sky sUSDS at 3.6%, Syrup USDC/USDT at 4.5%, Ethena sUSDe / stcUSD at 5.02%, and Neutrl at 5.2%.

- The protocols that sustain premium yields from here will increasingly look like multi-strategy credit funds rather than single-strategy vaults.

- Neutrl’s liquid reserves provide the base, basis trades capture speculative demand, and OTC locked-token positions monetize forced selling. The edge sits in the active sleeve’s ability to access return streams that reserve-only products cannot.

- Basis and OTC are negatively correlated by construction. When basis compresses, OTC opportunities tend to expand. When OTC dries up, basis tends to be rich because speculative demand has returned.

- The next leg sits in distressed credit, a $190.5B market with no scaled onchain fund analogue. Neutrl has not built the product yet, but the skill-set transfer from its OTC desk is direct.

1. Yield as Moat

The onchain stablecoin sector has reached an inflection point.

A year ago, the leading delta-neutral vaults were printing yields several multiples above Treasuries. Funding rates were elevated, the speculative cycle was hot, and basis trades were the highest-conviction trade in crypto. Today the same market has compressed into a much tighter band. Aave v3 USDC yields 3.19%, Sky sUSDS 3.6%, Syrup USDC/USDT 4.5%, Ethena sUSDe / stcUSD 5.02%, and Neutrl 5.2%.

This compression has consequences. The stablecoin business has long been understood as a yield game, where the protocol with the highest APY captures the marginal stablecoin holder. That assumption is breaking. Not because the trade has failed, but because the category has matured. Five years ago, running a delta-neutral vault at scale was a differentiated capability. Today the trade is well understood, the infrastructure is replicable, and the funding rate is the binding constraint on returns rather than the operator’s ability to discover the trade.

Best-in-class operators can still earn meaningful spreads over median operators within basis. But those spreads now sit inside a ceiling set by the speculation cycle. When speculative demand is strong, perp funding rises and basis trades look attractive. When speculative demand weakens, funding compresses and basis converges toward cash. The trade remains useful, but it is no longer rare. For single-strategy products if the source of yield is public, crowded, and pro-cyclical, it eventually stops being a moat.

The alternative is a fund structure. A multi-strategy book can rotate capital across regimes, source non-public flow, underwrite assets pure basis cannot touch, and earn a spread from active allocation between strategies with different cyclical exposures. This is how the largest credit allocators in TradFi operate. Apollo, Oaktree, and Centerbridge are not durable because of any one trade. They are durable because they can move between liquid credit, private credit, distressed, and special situations as the opportunity set changes.

Neutrl is operating in that direction, and the sector is beginning to converge on the same architecture. On April 6, 2026, Ethena announced the diversification of USDe’s backing into institutional lending, expanded RWAs, equity and commodity basis trades, and prime lending. The protocol that defined the basis-trade stablecoin category publicly committed to becoming a multi-strategy book. When the sector incumbent changes the playbook, the playbook becomes the standard. Pure basis is no longer where durable yield lives.

Neutrl reached a multi-strategy structure earlier and from a different starting point. Its active sleeve has combined basis trades with OTC locked-token positions since launch, and the next potential extension sits in operational territory the rest of the sector has not yet entered.

This is the case for why.

2. Anatomy of a Premium

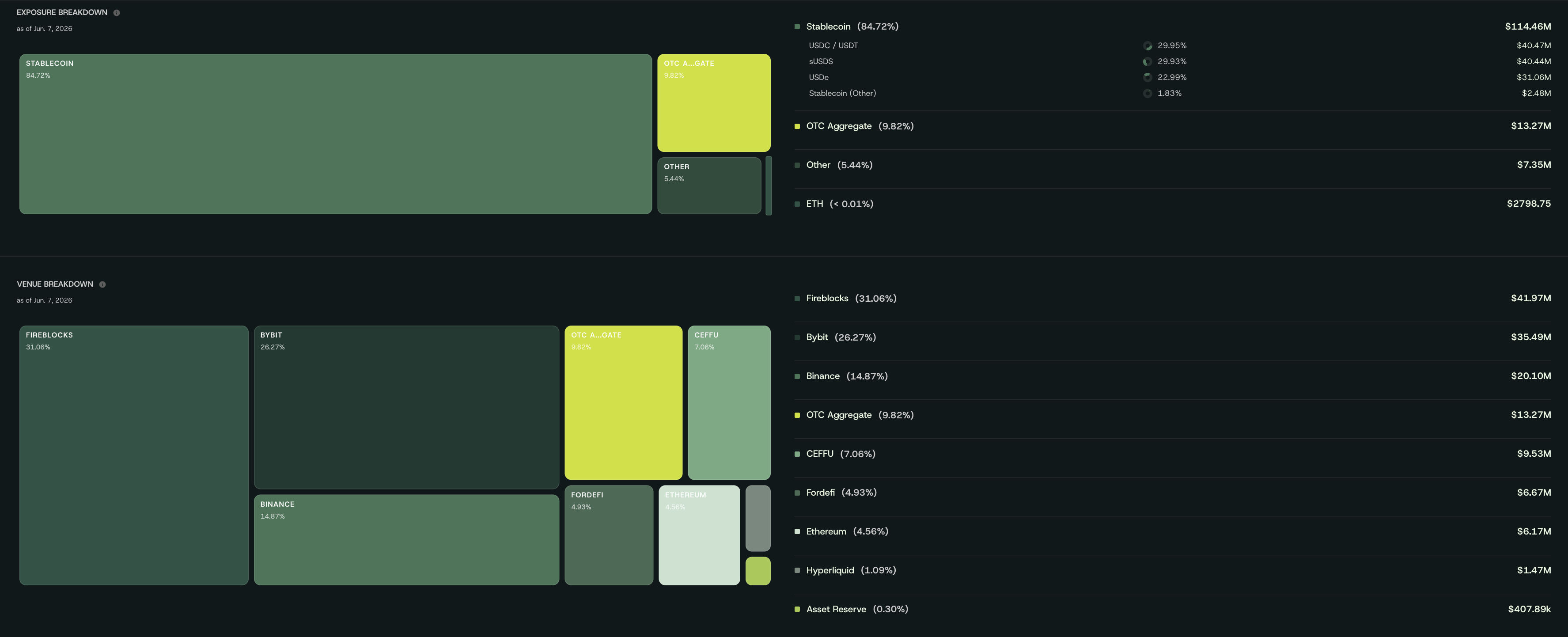

The premium no longer comes from a small active sleeve sitting on top of a mostly passive sUSDS book. Neutrl’s reserve composition has changed. As of June 7, 2026, total backing stands at $134.88M against $132.22M of NUSD supply, implying a 102.01% backing ratio. sUSDS now accounts for $40.47M, or 30.0% of reserves. USDC / USDT accounts for $40.91M, USDe for $31.07M, OTC Aggregate for $12.97M, Other for $7.34M, and Stablecoin Other for $2.10M.

Source: Neutrl

The original intuition still holds, but the portfolio has become less binary. Neutrl’s book now looks more like a diversified balance sheet across liquid reserves, exchange-deployed capital, USDe exposure, and OTC positions.

The venue breakdown makes the same point from a different angle. Fireblocks holds $41.99M, Bybit $35.50M, Binance $20.14M, OTC Aggregate $12.97M, CEFFU $9.55M, Fordefi $6.65M, Ethereum $6.17M, Hyperliquid $1.47M, and Asset Reserve $407.9k. This is a book distributed across custody, exchange venues, OTC exposure, and liquid reserve infrastructure.

The current headline APY is 5.2%. Against Sky sUSDS at 3.6%, the spread is roughly 160bp. Against Ethena sUSDe / stcUSD at 5.02%, the spread is only 18bp. That is why the premium cannot be read as a simple APY gap. The market has compressed too much for that. The relevant question is what part of the book is capable of producing returns above the reserve floor, and whether that return source can scale without becoming another crowded public-market trade.

A simple back-of-the-envelope illustrates the point. If the full $134.88M book earns 5.2%, Neutrl generates roughly $7.0M of annualized yield. The $40.47M sUSDS position, at a 3.6% yield, contributes roughly $1.46M. The remaining $94.41M of the book must therefore contribute roughly $5.56M, implying a blended yield of about 5.9% on the non-sUSDS portion.

The old version of the book made the active sleeve look like a small, high-octane engine carrying the yield premium. The current book looks more distributed. sUSDS provides a base rate, USDC / USDT and USDe provide liquid collateral and deployment flexibility. Exchange balances support delta-neutral strategies. OTC Aggregate represents the more differentiated private-flow component. The premium is now produced by the whole allocation framework rather than by one clearly isolated sleeve.

The decomposition itself is still the right place to start. The interesting part is what the book is becoming.

3. The Counter-Cyclical Engine

Basis trades are pro-cyclical. BTC perp funding has averaged 7.8% annualized historically, while ETH has averaged 9.15%, with bull-market prints running materially higher. When speculative demand rises, perp longs pay funding, spot-perp basis widens, and delta-neutral books earn attractive carry. When speculative demand fades, funding compresses toward zero. This remains the gravitational pull on single-strategy delta-neutral products.

OTC locked-token positions move differently. Discounts on locked tokens widen when capital becomes scarce. VCs, early investors, angels, and market makers often hold allocations they cannot immediately monetize through public markets. In strong markets, they can wait. In weak markets, they may need liquidity because of fund redemptions, LP distributions, margin pressure, portfolio rebalancing, or simple duration fatigue. A position that clears at a moderate discount in a healthy market can trade at a much steeper discount when the seller’s need for liquidity becomes urgent.

Source: Neutrl Blog

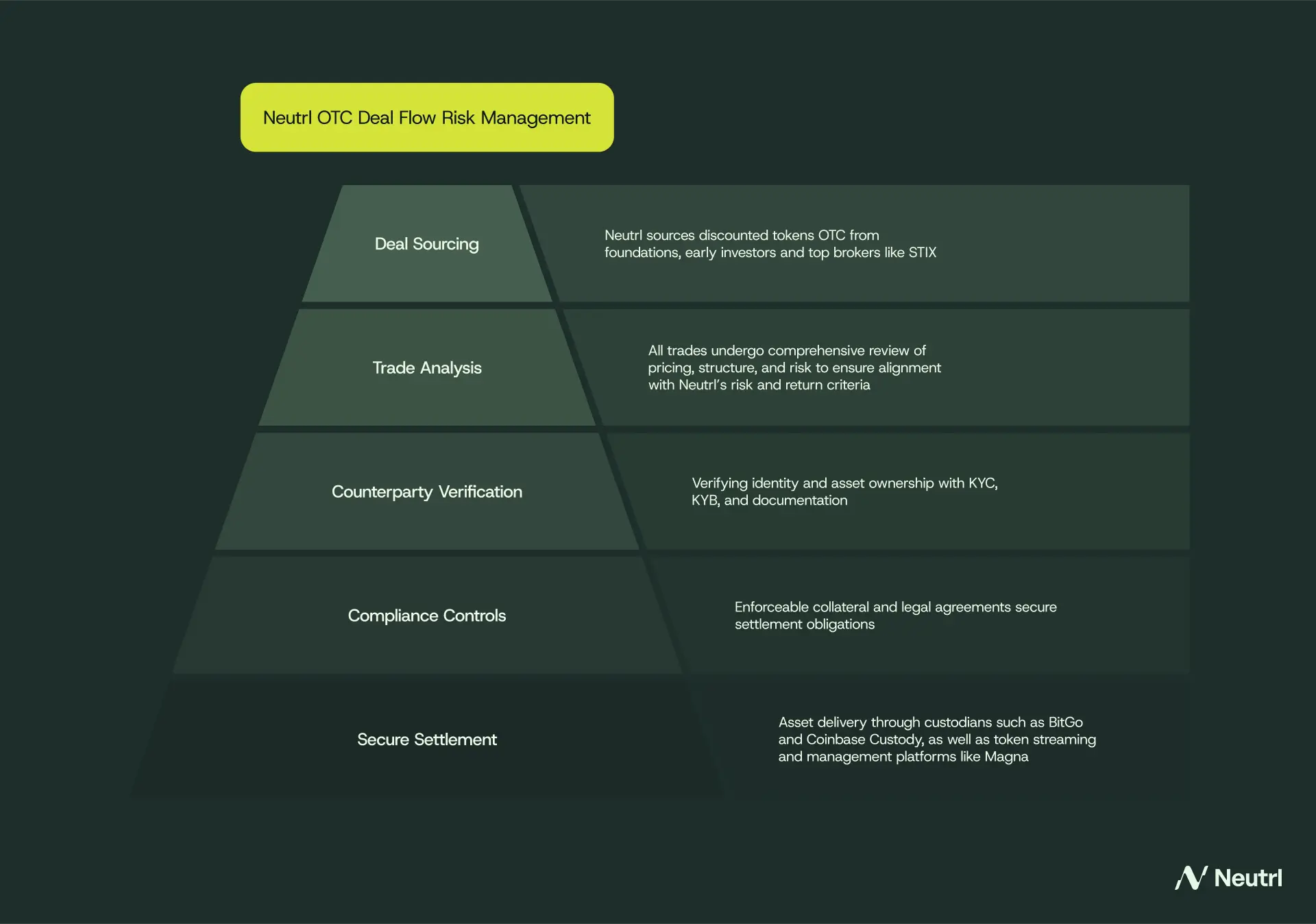

This is where Neutrl’s OTC desk operates. The trade is easy to understand in concept: buy locked-token exposure at a discount from a seller who values liquidity more than upside, hedge liquid market beta with perps where possible, and capture the discount as the position unlocks or liquidity normalizes. But the edge itself is not the complexity of the structure. It is access to flow, underwriting the quality of the locked asset, and having capital that can wait when the seller cannot.

The timing is what makes the strategy valuable inside the same book as basis. When basis yields compress, OTC discounts often widen because the same weak market that reduces speculative demand also increases liquidity pressure on private holders. When OTC discounts tighten because markets are healthy and sellers are not forced to transact, basis yields are usually richer because speculative demand has returned. The two engines are not perfectly hedged, but they are structurally counter-cyclical.

That gives Neutrl a different profile from a single-strategy vault. A pure basis product earns when funding is attractive. A pure lending product earns what public credit markets offer. Neutrl can move between liquid reserves, basis, and OTC depending on where the market is mispricing liquidity.

This is the operating logic of multi-strategy credit. Apollo, Oaktree, and Centerbridge do not operate as concentrated bets on a single trade. They build portfolios of strategies that complement each other across regimes. Neutrl is attempting the crypto-native version. The assets are different, but the underlying mechanic is the same. Forced sellers create discounts, duration earns a premium, liquidity has a price, and the allocator captures the spread.

4. The Distressed Frontier

Neutrl has not shipped a distressed credit product. What follows is directional. It belongs in this piece because the addressable market is the largest of the potential strategy legs, the operational adjacency to Neutrl’s existing OTC desk is direct, and the market has not yet priced this as part of the protocol’s franchise.

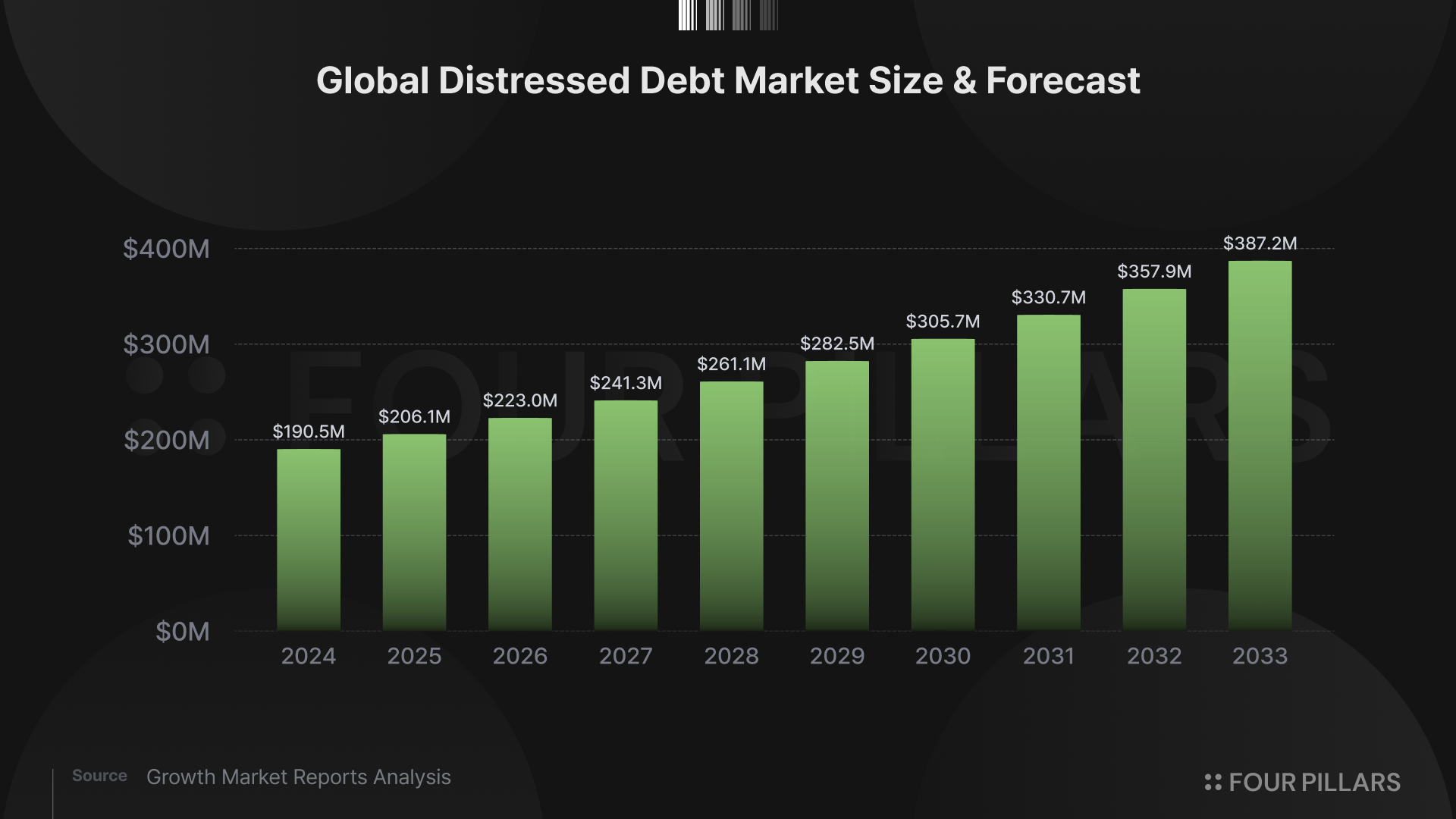

Begin with the market sizing. Global distressed debt was $190.5B in 2024 and is projected to reach $370.8B by 2033 at an 8.2% CAGR. $806B in US high-yield bonds and leveraged loans mature by 2028, providing the raw material for the next distressed cycle. The ten largest distressed funds in market are targeting $50B in aggregate. Oaktree raised $16B for its largest fund to date. Apollo launched a dedicated global distressed credit fund in April 2025 with a $40B-plus target focused on European distressed. Top-quartile distressed funds have historically earned 15% to 25% net IRR over fund lives, with yields running 800 to 1,500bp over Treasuries versus roughly 100bp for investment-grade credit. The asset class is one of the most consistently profitable categories of credit in TradFi, and it has no scaled onchain analogue.

Crypto-native precedent already exists. The 2022–2023 bankruptcy cluster produced more than $20B in claims across FTX, Genesis, Celsius, Voyager, and BlockFi. FTX claims went from distressed levels in early 2023 to above par by 2024, with final recoveries exceeding petition-date values. Genesis followed a similar path. The headline IRRs were materially inflated by crypto prices appreciating through the recovery period and should not be treated as a repeatable baseline. The more important structural point is that crypto distressed markets exist, trade at scale, and can produce return profiles that resemble TradFi distressed once the price-appreciation tailwind is stripped out.

Claims trading infrastructure also exists. Xclaim has processed more than $750M across over 10,000 creditors. What does not yet exist is a scaled onchain product that packages distressed exposure for crypto-native capital. This is where Neutrl’s OTC desk becomes relevant. Buying assets at deep discounts from liquidity-constrained sellers, hedging market exposure with perp shorts, and capturing the discount spread on unlock or recovery is close to what the OTC desk already does. TradFi distressed funds underwrite which situations will recover. Neutrl’s OTC desk underwrites which tokens will retain liquidity at unlock. The fundamental skill is similar: evaluating assets under forced-sale conditions where the seller’s marginal cost of capital dictates the discount.

The crypto-native variant also has a structural advantage. Perp hedges can make the position closer to delta-neutral, allowing the trade to capture discount compression without requiring outright appreciation in the underlying asset. In some cases, claims can also be tokenized, financed, or structured into onchain products. The market is still early, but the primitive is clear: buy impaired or illiquid exposure at a discount, manage duration, hedge what can be hedged, and monetize recovery.

5. Origin Season 2

Season 2 of Neutrl’s Origin Program is now live. Season 1 introduced NUSD, seeded integrations, built Pendle markets, and pushed the product into the market. According to Neutrl, Season 1 reached $230M in peak AUM, more than 1.1T Neutrl Points, 5,289 participants, an 80% staking ratio, $5.5M in yield distributed to sNUSD holders, and $3.2B in transfer volume.

Season 2 changes the focus from distribution to duration. The central product is Founders’ Lock, which lets users lock NUSD beyond the end of Season 2 in exchange for the highest point multipliers in the program. Founders’ Short locks through the end of Season 2 plus three months, earning 400x points per day per NUSD and the Sky Savings Rate. Founders’ Long extends the lock to six months after the season ends, earning 700x points per day per NUSD and base yield equal to the Sky Savings Rate plus up to an additional 2%.

Source: X (@Neutrl)

The design is asset-liability management in points-program form. Users give up liquidity, while Neutrl receives more predictable capital. More predictable capital can support longer-dated OTC deployments, and longer-dated OTC deployments can access deeper discounts. This is important because a protocol running OTC and other active credit-like strategies needs capital with duration.

Season 2 also adds new Pendle markets, higher lending market multipliers, and a 10% loyalty boost for wallets that earned at least 1M points in Season 1. It is the final Origin season before TGE, which makes the purpose clear. Neutrl is trying to convert early mercenary capital into longer-duration aligned capital before the token launches.

6. The Fund Era

The onchain stablecoin sector has crossed a threshold. Until now, capital mostly flowed toward products that could display the highest APY. That worked while basis was rich and the opportunity set was less crowded. But as yields compress into a narrow band, the market will need to evaluate these products differently. The relevant question is no longer which protocol has the highest headline yield this week. It is which protocol has the most durable return engine.

Neutrl is that protocol. Liquid reserves provide the base. Delta-neutral strategies monetize funding and basis. OTC locked-token positions target forced-sale discounts. Distressed credit could become the next extension. Origin Season 2 adds another piece by trying to lock in longer-duration capital before TGE. Together, these pieces transforms Neutrl into a crypto-native asset manager for market-neutral yield. That is the right game to play as the stablecoin sector moves out of the pure yield era and into the fund era.

gNeutrl.

The report is based on the independent research of the author sponsored/funded by Neutrl. The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.