Table of Contents

Researcher

Related Projects

Key Takeaways

- Korean retail net bought ₩32.4 trillion in equities through early June, with Samsung and SK Hynix absorbing 73% of that flow and accounting for 42% of the KOSPI, the most concentrated semiconductor bet in a generation.

- Perpetual contracts on Samsung (10x), SK Hynix (10x), Hyundai (10x), and EWY (the MSCI Korea ETF, 20x) already trade 24/7 on Hyperliquid.

- Markets by Kinetiq has generated $3.75 billion in cumulative volume from 9,278 users since launching in January 2026, averaging $404K per user.

- Markets builds trading as a social product. Every position posted carries a verified onchain PnL history and copy trading/counter-trading are each one tap.

- Every trade on Markets earns kPoints toward KNTQ allocation, with Season 2's final snapshot on September 29, 2026. 100% of platform revenue flows to sKNTQ staker buybacks.

1. The KOSPI Frenzy

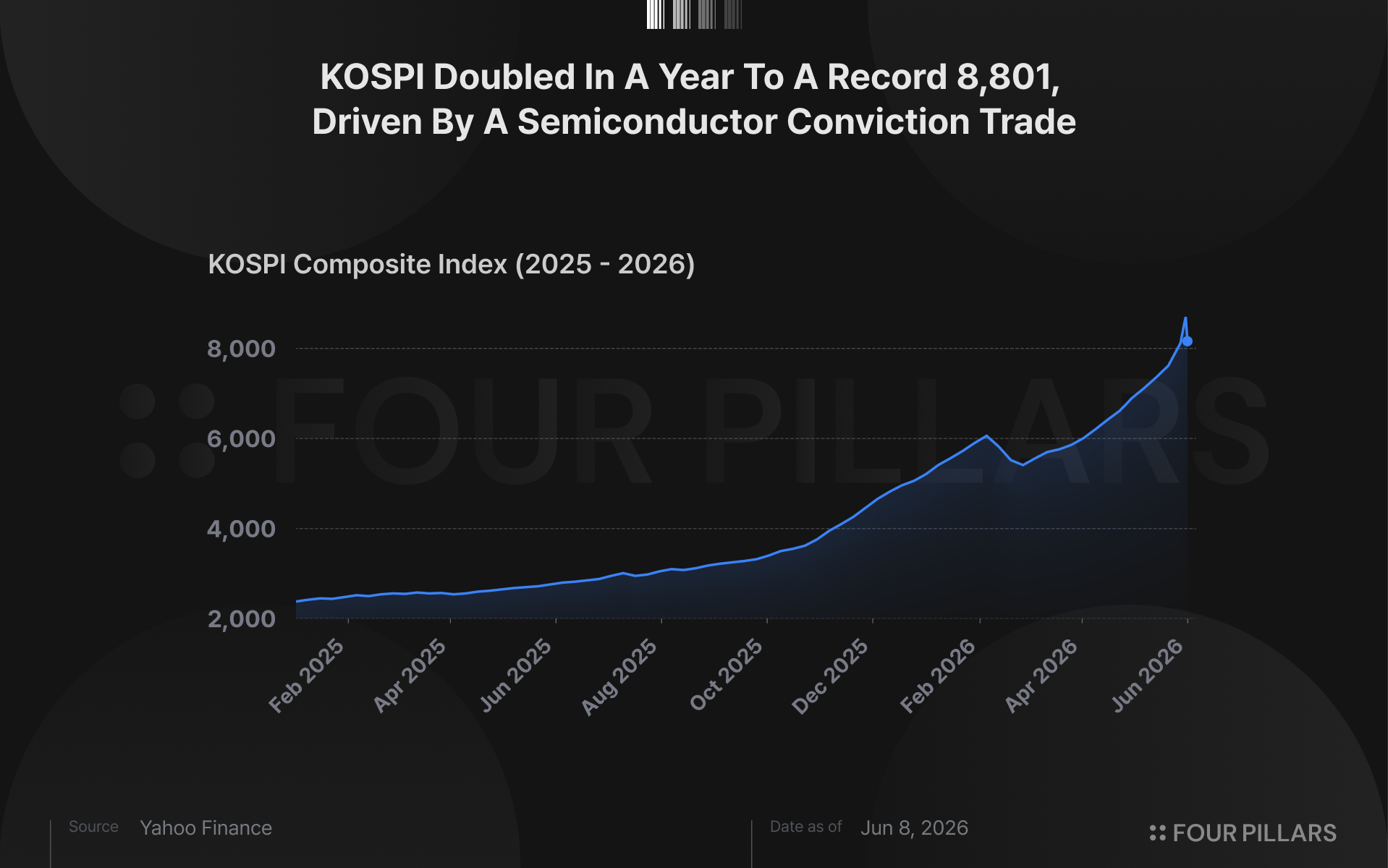

Korean retail is in the middle of the most aggressive equity frenzy in a generation. KOSPI doubled in 2026 to a record 8,801 on June 4, driven by a semiconductor conviction trade that has pulled the entire index upward on the back of AI demand for memory chips. Samsung touched ₩349,000 on a 10.9% single-day surge. SK Hynix peaked above ₩2.4 million.

Korean retail net bought ₩32.4 trillion in equities through the first week of June alone, with Samsung absorbing ₩9.36 trillion and SK Hynix another ₩14.26 trillion of that total. Together, the two names now account for over 42% of the KOSPI, a record concentration not seen since the semiconductor supercycle of 2021.

The appetite for leverage is just as concentrated. Single-stock leveraged ETFs are doing ₩9 trillion in daily volume. But the instruments Korean traders rely on to express this conviction have a fundamental constraint. The market closes at 3:30pm, leveraged ETFs cap at 2x, and weekends are completely dark. On June 4, Broadcom reported earnings that disappointed after Wall Street’s close, triggering a semiconductor rout that rippled across Asia the next morning.

Samsung opened down and closed at ₩329,000, a 6.4% single-day loss. SK Hynix fell to ₩2.08 million, down nearly 10%. Korean retail had zero ability to hedge overnight because the market was closed when the catalyst hit. After-hours earnings calls, geopolitical events, weekend macro developments — all of these move the value of Samsung and SK Hynix in real time, but Korean retail cannot respond until the opening bell. The semiconductor momentum does not pause at 3:30pm. The instruments do.

2. Samsung 10x Leverage, Saturday 3AM

Perpetual contracts on Korean equities with real leverage, tradeable around the clock, already exist onchain and are already trading with meaningful volume. SAMSUNG-USDC is live on Hyperliquid at 10x leverage with $16 million in open interest. SKHYNIX-USDC trades at 10x with $65.9 million in open interest, making it one of the deeper HIP-3 markets on the platform, deeper in fact than many crypto-native perpetuals that launched years earlier. HYUNDAI-USDC trades at 10x with $1.4 million in open interest. EWY, the MSCI Korea ETF, offers 20x leverage on the broader index.

The catalog extends well beyond Korea. The S&P 500 trades at 50x leverage, NVDA at 20x, TSLA at 10x, AAPL at 20x, gold at 25x, crude oil at 20x, EUR/USD at 50x. Across eight independent HIP-3 deployers, the full catalog spans 188 assets doing $3.0 billion in daily volume against $3.0 billion in total open interest. All of it settles in USDC on Hyperliquid’s L1 with no market close.

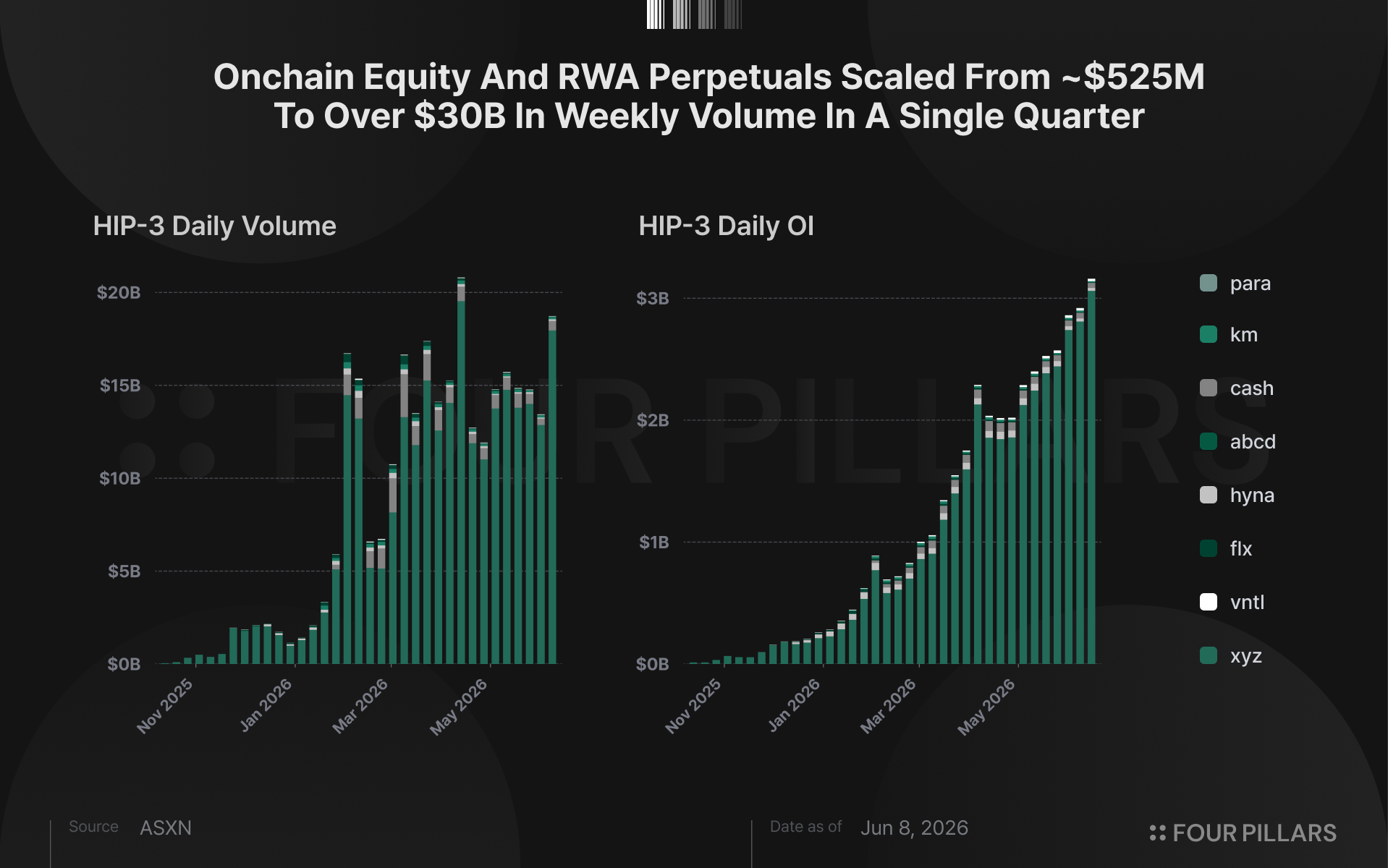

These are not synthetic tokens or prediction market proxies. They are perpetual contracts with real orderbooks, real leverage, and real liquidation mechanics, running on the same infrastructure that processes Hyperliquid’s core crypto perpetuals. The equity perp market itself barely existed a year ago. HIP-3 went from $525 million in weekly volume to over $30 billion in a single quarter, growing from a curiosity to a market segment that at its peak represented 45% of all Hyperliquid activity. The instruments are live and the volume is organic. With the instruments established, the question becomes how a Korean retail trader actually accesses any of this from their phone.

3. The Markets App

3.1 The Billion-Dollar Frontend

Hyperliquid built the backend. The missing piece has always been the frontend. The existing interfaces to HIP-3 markets are designed for traders who already hold USDC in a wallet and understand how perpetual contracts work. That is the core audience, but it is not the audience that explains a billion-dollar opportunity. Hyperliquid co-founder Jeff Yan framed it directly in November 2025 that “there is a billion dollar opportunity to build a mobile app for non-crypto users. The two keys is seamless fiat onboarding + a mobile UX that non-crypto users love.” The onchain instruments described in the previous section are accessible to anyone with a wallet, but wallet-first distribution excludes the vast majority of potential users.

Markets by Kinetiq is a mobile-first perpetual futures app built on HIP-3 that routes to all deployer markets, not just its own, giving users access to the full asset catalog from a single interface. The platform launched in January 2026, with the iOS app following on April 21 and Android arriving the week of June 9.

The mobile app was developed together with the Dexari team. Dexari has built a Hyperliquid-based mobile trading app that lets users trade perps, equities, gold, forex, and indices from a self-custody wallet experience. Dexari is led by Chuck Bradford, the former Senior Director of Growth at Binance US, who brings a Stanford MBA and direct experience scaling a retail crypto exchange in a regulated market. Dexari raised a $2.3 million seed at a $22.5 million valuation from Prelude and Lemniscap.

3.2 Institutional-Grade Architecture

The execution quality beneath the consumer interface is institutional-grade, and the spread data makes the case more directly than any product claim. The US500 market runs at 0.36 basis points in spread, with $1,000 in slippage at 0.62 basis points and $10,000 at 2.20 basis points. USBOND sits at 0.54 basis points. USTECH at 1.85 basis points. The deeper markets are tight enough to trade with real size.

Jun 7 2026 snapshot, Source: https://markets.xyz/stats

The oracle architecture is built with Kaiko and runs three layers deep. Institutional-grade feeds from NYSE, NASDAQ, and major forex venues update at one-second frequency, with EMA pricing during off-hours to maintain continuous mark prices even when the underlying exchanges are closed. Mark price is calculated as the median of the oracle price, orderbook sentiment, and last trade, bounded within a defined range. Execution routes through the Hyperliquid L1 orderbook, with automated dividend adjustments and stock split handling so that positions are never manually disrupted by corporate actions. The HIP-3 standard itself requires deployers to stake 500,000 HYPE as a security deposit, subject to slashing for bad oracle behavior, earning up to 50% of trading fees in return. The security deposit creates economic accountability for price feed quality that no centralized exchange replicates.

Fees reflect growth-stage priorities. Markets runs a 90% discount on Hyperliquid’s base fee during its current growth mode, bringing the effective taker fee to 0.81 basis points. The builder fee sits at 3.5 basis points for takers and scales down with volume tiers. sKNTQ stakers receive up to an additional 30% discount on top. There are no gas fees at the user level. The architecture is entirely non-custodial, with USDC collateral backed by cash and US Treasuries held in JPMorgan Chase custody. Four independent security audits have been completed by Spearbit, Zenith, Pashov, and Code4rena, covering both the smart contract layer and the deployer infrastructure.

3.3 Trading as a Social Product

The differentiation that separates Markets from other perpetual futures interface is not the instruments or the infrastructure, but the decision to build trading as a social product. Crypto trading has always been social in practice, with Telegram groups, CT threads, and screenshot culture driving a significant share of retail flow, but the signal-to-noise ratio is terrible because none of the performance claims are verifiable. Markets takes the social impulse and anchors it to onchain truth. Every position posted on the platform comes from a real onchain account with a verified PnL history. Traders share positions with their thesis, reasoning, and setup attached, and others watch those trades play out in real time. There are no demo accounts, no hindsight calls, no simulated screenshots.

Source: X (@0xOmnia)

Copy trading and counter-trading each take a single tap. If a trader posts a Samsung long with a compelling setup, one button replicates the position. If the thesis looks wrong, one button opens the opposite side. Social conviction with skin in the game, flowing in both directions. The mobile UX is simplified for the audience it targets: up/down instead of long/short, pick a multiplier, one click to execute. Markets also offers a web frontend at markets.xyz with limit orders, stops, TWAP, and scale orders for power users who want more control, but the mobile app is designed for someone who has never touched a DEX.

Gamification reinforces the trading core. XP accrues from trades, check-in streaks, referrals, and leveling up. PnL and XP leaderboards run separately, with weekly competitions and a $200,000 incentive program that includes a Rolex Datejust 41 and FIFA World Cup tickets for Brazil vs. Scotland on June 24. A curated social feed lets traders follow the largest onchain accounts, build a personalized feed, and compete against friends. Fiat on-ramping runs through Stripe’s Bridge with cross-chain support from ETH, Arbitrum, Base, and Solana, plus credit card deposits. Sign-up accepts email or wallet connection. The comparison is not other DEXs. The comparison is Kiwoom Securities and Robinhood, except with 10-50x leverage, a verified social feed, and token earnings on every trade. Korean brokerages offer none of this.

The product stands on its own as a trading interface. But there is an additional reason to start now.

4. KNTQ Incentives

Every trade on Markets earns kPoints, which convert to KNTQ tokens. The program distributes 800,000 kPoints weekly, with snapshots on Tuesdays and distributions on Thursdays. kPoints accumulate through trading activity on Markets as well as broader ecosystem participation, with the exact earning formula kept private. Season 1 distributed 24% of total KNTQ supply to kPoints holders. Season 2 has been live since November 13, 2025, with the final snapshot set for September 29, 2026, roughly four months from now. An additional 30% of total KNTQ supply is allocated to protocol growth and rewards, meaning the combined allocation to users across both seasons represents a majority of the token’s distribution.

Source: X (@Markets_xyz)

100% of Markets revenue, 100% of Launch revenue, validator commissions, and 70% of staking revenue flow to buybacks distributed to sKNTQ stakers. sKNTQ staking tiers unlock up to 30% fee discounts and 15% referral commissions, creating a loop where heavier usage earns more tokens and cheaper trading simultaneously. The incentive structure is designed so that the users generating the most volume are the users earning the most favorable economics, and staking deepens that advantage further.

The deadline creates urgency that the product itself does not. Four months of Season 2 remain, and every trade between now and September 29 accumulates points toward an allocation with a fixed end date that will not repeat on the same terms.

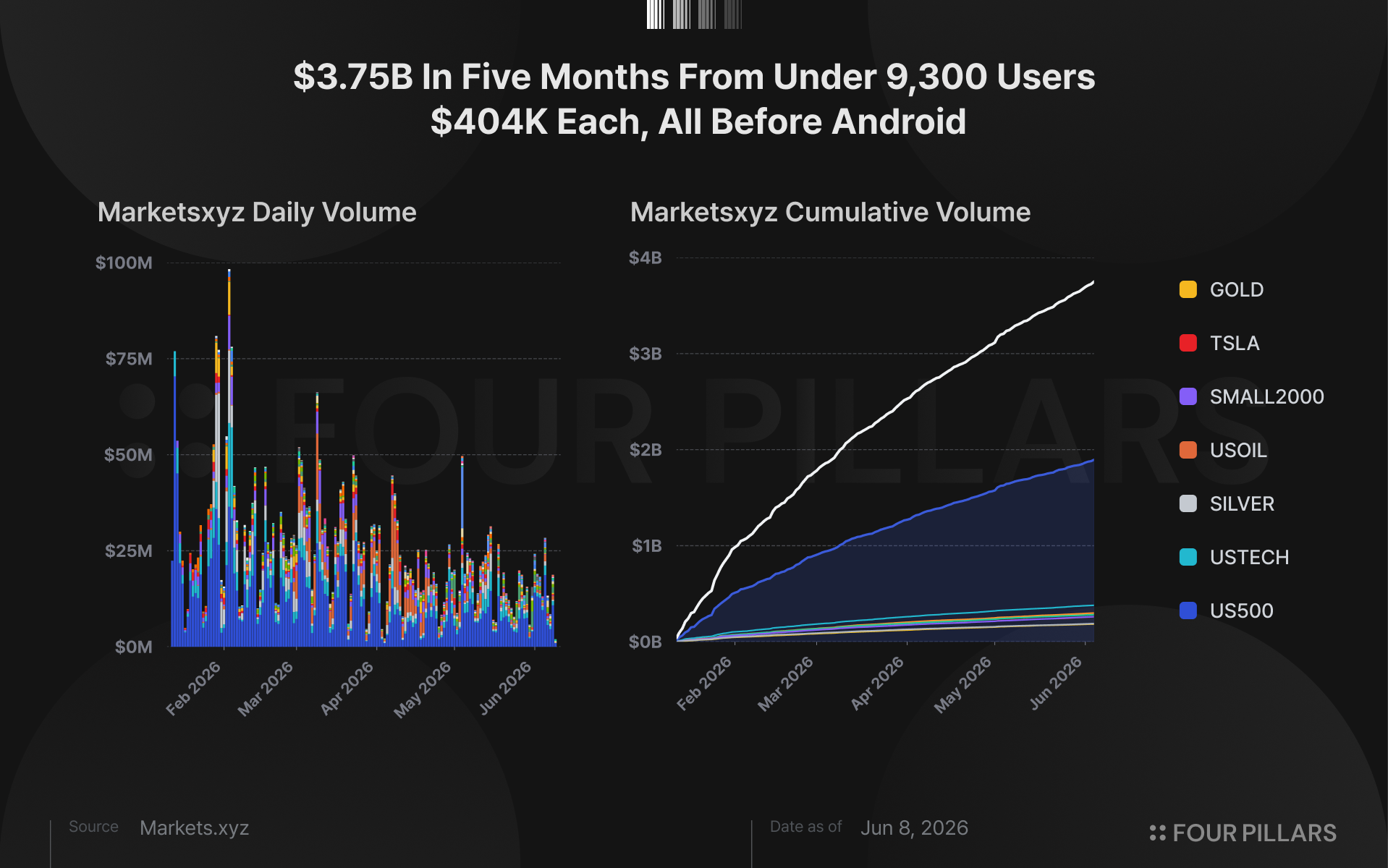

5. $3.75 Billion from +9,000 Users

Markets launched on January 12, 2026, and shipped its iOS app on April 21. In under five months, the platform has accumulated 9,278 users who have generated $3.75 billion in cumulative volume across 7.13 million trades. That works out to $404,000 in volume per user and an average trade size of $526. Markets has also deployed its own catalog of 23 markets on HIP-3, covering US indices, individual equities, commodities, and forex, with $15.6 million in total open interest and daily volume averaging $28 million through the first week of June.

For a platform that did not exist six months ago and only reached mobile (IOS) in late April, the early traction suggests that the product thesis is landing with the users it reaches.

6. Looking Forward

The infrastructure exists, and the instruments are live. The app is cross-platform, and the Android launch puts Markets in the hands of the operating system with the largest mobile user base. What is also worth noting is the primitive underneath it. A perpetual contract does not care whether the underlying is Bitcoin or Samsung. It uses the same margin, the same settlement, and the same orderbook.

The category lines between crypto exchanges and stock exchanges were always defined by what they listed. Crypto exchanges listed coins, brokerages listed stocks. But once equities, indices, commodities, and FX can all trade as onchain perpetuals, that boundary starts to dissolve.

For Korean retail, this perpification of assets is not only about being able to trade Samsung onchain. The more important point is that positions can be opened or adjusted during windows that the traditional brokerage system does not cover: after-hours earnings, weekend macro events, or overseas semiconductor selloffs before the Korean market opens.

The semiconductor momentum does not stop at 3:30pm.

The report is based on the independent research of the author sponsored/funded by Kinetiq Research Pte Ltd. The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.