Researcher

Related Projects

Felix winding down, and now Ventuals, has had me thinking about HIP-3 dynamics a lot. It made me wonder if HIP-3's design is flawed, that it only ever produces winner-take-all, and that newcomers are cooked. The conclusion I came around to is that we are looking at the wrong layer, and HIP-3 is doing roughly what it was always going to do.

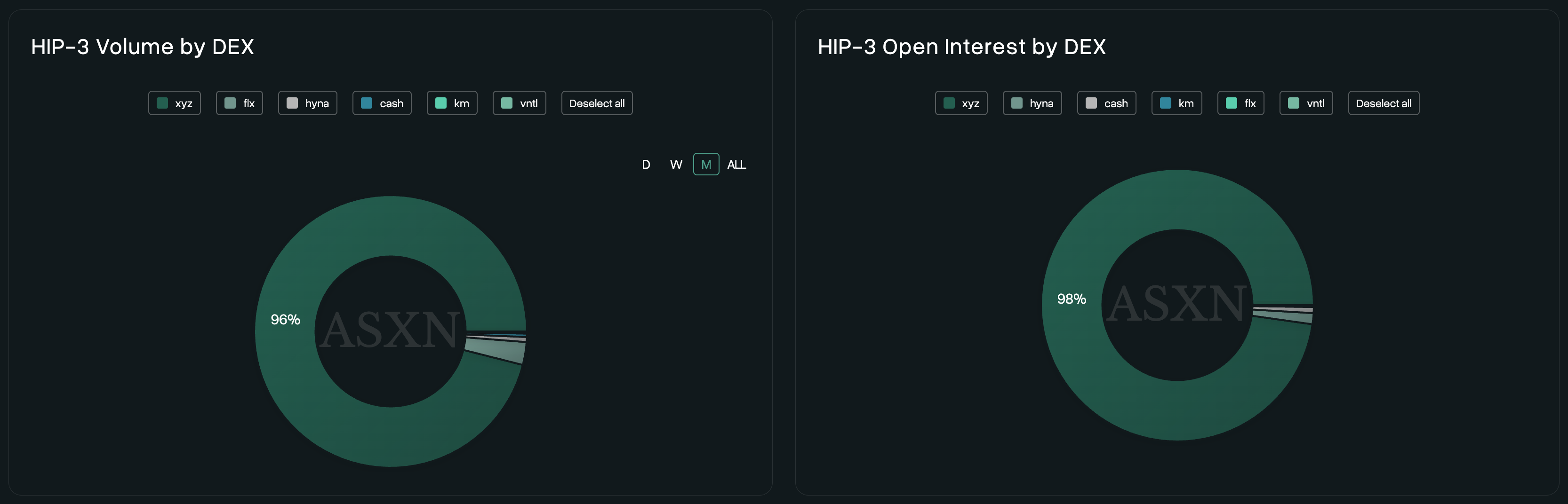

Permissionless entry and a near-monopoly outcome turned out to be completely compatible, which is strange, because we tend to assume the first produces competition. The reason it doesn't might be the feature everyone praises. Shared liquidity with no cold start is what makes HIP-3 magical for builders, and it is also what removes any niche protection. On a standalone venue a small listing survives because nobody will switch exchanges to trade it. On a shared book there is nothing to switch. The trader sees your market sitting beside a deeper clone in the same window and the flow drifts to the deeper book almost immediately. The door stays open to everyone and the room still ends up with one occupant.

If that is right, the concentration was never a flaw to fix. Liquidity begets liquidity is close to the entire logic of a trading venue. Splitting one name across ten deployers makes every book worse, wider spreads and worse fills, which hurts the very traders the venue exists for. A healthy perp market probably should look monopolistic at the level of any single contract. Measuring HIP-3's health by counting deployers is a little like measuring the health of the internet by counting independent implementations of TCP/IP. Seen that way, TradeXYZ's position at this layer is perhaps already irreplaceable.

Source: ASXN

So the question is probably not how to make the listing layer competitive, since it may not be able to be. The better question is where competition can live, and I think it lives at the demand layer, which has barely begun.

Demand for perps is no longer the open question, and Syncracy's “The Great Perpification” piece makes that case better than I could. Perpetuals are a cleaner instrument than options or CFDs for most retail, the derivatives complex they can absorb is enormous, and billions of people are still unbrokered.

The same piece is quietly unkind to the frontend layer. It describes user acquisition, localization and listings all pushed out to a swarm of frontends competing for the same flow, while the protocol scales like software toward very high margins. A swarm competing for flow has little pricing power. It is telling that HYPE appreciated sharply this month even as Ventuals wound down. The value those frontends compete away does not disappear, it settles a layer beneath them, in the protocol they all route through.

This is why another perpetuals app chasing the same crypto-native traders does not look like it wins much. Same CT audience, same airdrop-and-points playbook, same backend, the same converged terminal UI. Every lever is commoditized, so the only variable left is who burns the most incentive budget, which is a race to negative margin that ends in a points-funded death or an acqui-hire, with Ventuals folding into another team as the template, and that was one of the better outcomes. The standalone deployer version is the same trap with a higher entry fee. Niche means no demand, non-niche means TradeXYZ eats you, and the 500k bond plus auction cost makes both ends unprofitable. That's a value trap.

The way out is that TradeXYZ currently owns crypto-native demand and very little else. It does not yet own non-crypto demand, regional demand, community-owned demand, or new categories like HIP-4 outcome markets. The frontends that look viable are the ones bringing demand the swarm does not already have, whether that is regional or local-language distribution, a regulated wrapper offering protections the base layer can't, or an existing consumer app bolting perps onto users it already owns. Phantom switching on millions of wallets it already had is the clearest version so far. In each case they arrive already owning the demand and meter it through builder codes, agnostic about which backend they route to. The deployer economics that look fatal in isolation start to make sense for a team like that, because they deploy downstream of a crowd they already have rather than deploying first and hoping a crowd appears. That last part is the mistake Ventuals made. They got the category right (pre-IPO), but they owned the market without owning the audience for it.

Marketsxyz looks pretty smart to me for exactly this reason, because it is trying to do that one thing. It tries to goes after non-CT retail with a genuinely consumer product, simple UI, gamified mechanics, social feeds, and reward loops, building the audience first so the markets have somewhere to land.

So maybe HIP-3 did not fail to produce competition. It settled the listing layer, which was only ever going to settle one way, and the contest moved up a rung to the frontends and the builder codes, where protocol parameters cannot reach and most teams do not yet know how to play.

Deploying upstream of demand is a near-impossible fight at this stage. The edge, and most of the money, live downstream of it, where you choose between being a pure broker, builder codes only, lean, no bond, no slashing, and full vertical integration, builder codes plus fee split plus exclusive markets, richer and more defensible. Whoever owns the demand decides how far down to integrate. The right way to model one of these is as a fintech P&L with several revenue streams (e.g. Robinhood), then ask how far down the stack the team can push before the bond's capital cost and regulatory exposure stop being worth it. Whoever does not own demand has no good options, regardless of which fee line they chase.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.