![License Is All You Need [FP Weekly 27]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Ft4v9kemqys40d1.png%3Fv%3D2&w=1920&q=75)

Table of Contents

- 1. Major News

- [Asia] SBI Holdings Acquires Bitbank for About $288.6 Million

- [Institution] European Parliament Approves Digital Euro Bill and Begins Trilogue Negotiations

- Others

- 2. Data Spotlight

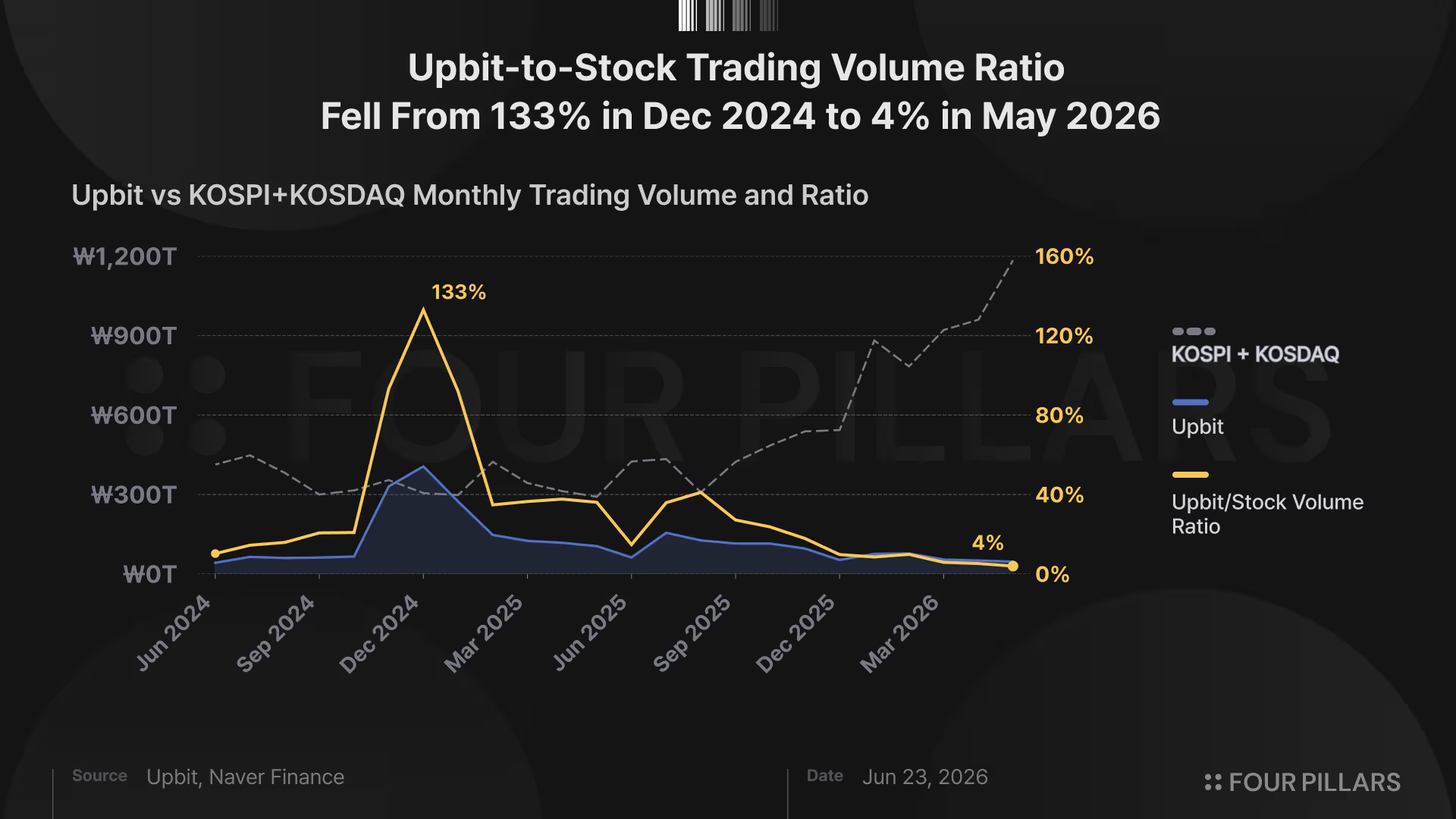

- Korean Exchanges Facing a Volume Plunge. Is It Really a Crisis? (Link)

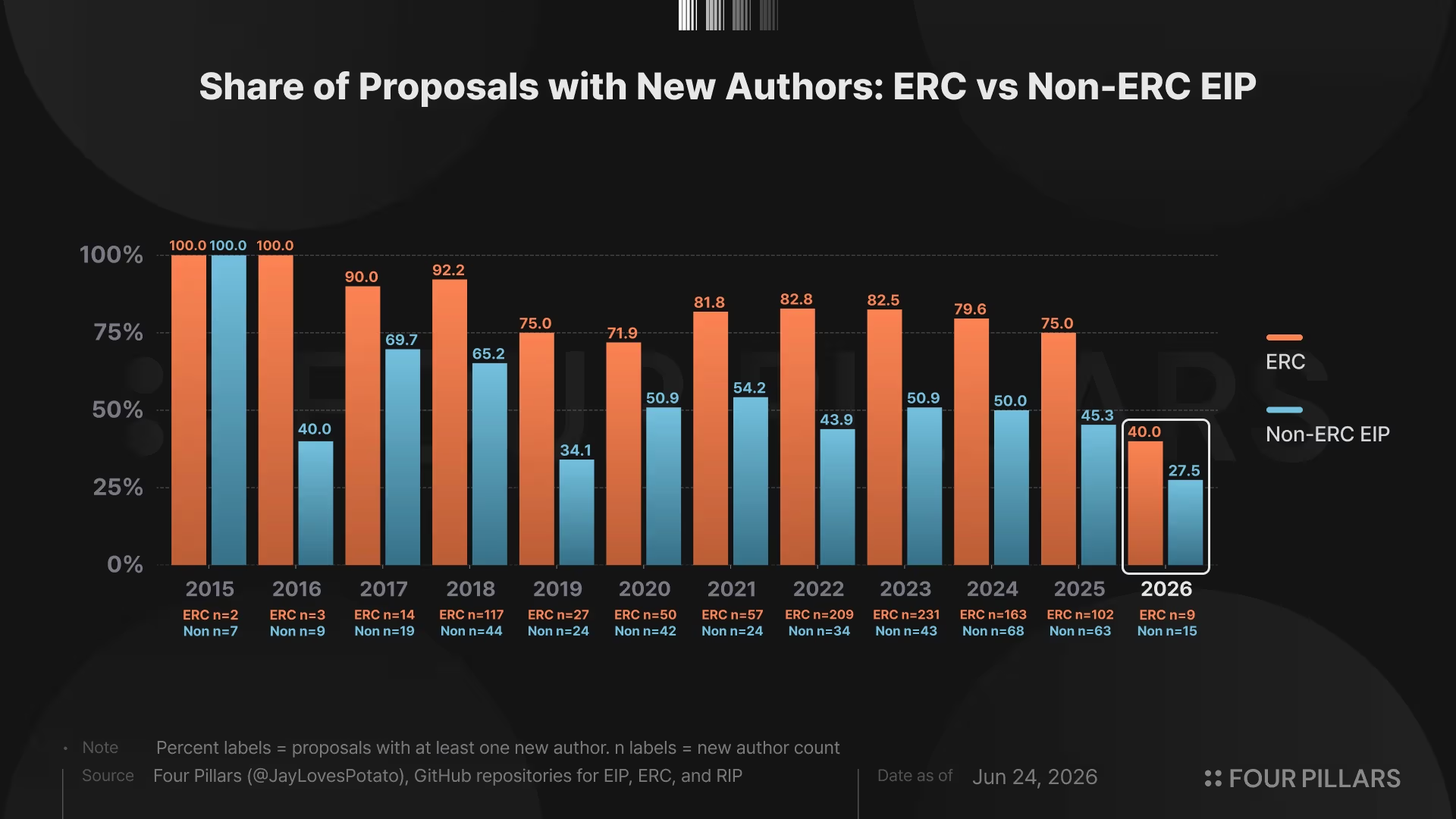

- Ethereum Decentralization Through the Lens of New EIP Author Share, and a Warning Signal from 2026

- 3. Four Pillars Weekly

- : : How Distributed Trust Absorbs Shocks: Lessons from the KelpDAO Incident and stETH's Resilience (Link)

- : : What Should Exist on HyperEVM? (Link)

- : : Code is Not Law: Legal Context Protocol (Link)

- Comments

- 4. Macro & Onchain Metrics

Researcher

1. Major News

[Asia] SBI Holdings Acquires Bitbank for About $288.6 Million

What Happened?

On June 25, SBI Holdings agreed to acquire the Japanese crypto exchange Bitbank for 46.7 billion yen (about $288.6 million). The transaction is carried out through SBI's wholly owned subsidiary SBICAH LLC, and upon completion Bitbank becomes an indirectly held, wholly owned subsidiary with 100% voting rights.

Completion of the deal is expected around October 2026, subject to conditions including a merger review by the Japan Fair Trade Commission (JFTC). After SBI first disclosed in May that it was in talks to acquire Bitbank, this announcement formalizes the acquisition terms and the deal timeline.

Through this acquisition, SBI plans to combine its existing crypto business with Bitbank's customer base, service development capabilities, and security and compliance systems to expand trading services and strengthen the development of digital-asset-linked financial products including stablecoins.

The acquisition also has a large effect in terms of scale. According to the company, a simple aggregation of SBI VC Trade and Bitbank figures as of the end of April 2026 would bring the group's crypto customer assets to about 1.1 trillion yen (about $6.8 billion) and the number of accounts to about 2.92 million. This corresponds to first place among Japanese crypto exchanges by assets under management and a top position by number of accounts as well. In particular, Bitbank says it has had no hacking incidents since its founding in May 2014, which aligns with the security and compliance capabilities that SBI emphasizes.

Researcher’s Comment

The Japanese exchange market has a fragmented structure of small and mid-sized exchanges. GMO Coin, bitFlyer, Coincheck, and Bitbank are divided into similar weight classes, and no single player dominates the market. Moreover, while there are exchanges under large groups such as Coincheck and Rakuten Wallet, cases of operating multiple exchanges are rare.

SBI has taken that rare path, gathering the customer bases and liquidity of multiple exchanges under a single group. Once the Bitbank integration is complete, it becomes the top operator by assets under management. In that it grows scale not through simple new entry but by acquiring a licensed operator outright, this signals that competition among Japanese exchanges has moved beyond securing market share into a phase of mergers and acquisitions.

This move can be seen in the same context as Japan's regulatory shift. The Financial Instruments and Exchange Act (FIEA) amendment that passed the House of Representatives in June reclassifies crypto assets as financial products and repositions exchanges as capital-market-style businesses. As obligations such as disclosure handling, liability reserves, and insider-trading surveillance are added, the cost structure grows heavier, and independent survival becomes difficult for small exchanges with weak compliance capacity and capital.

Accordingly, with many of Japan's roughly 30 registered exchanges already operating at a loss, a licensed exchange gains value as an acquisition target. SBI's acquisition of Bitbank is closer to a preemptive move to secure a licensed operator before the tightening of rules begins in earnest.

Meanwhile, the division-of-roles structure in Japan's digital asset market has become clearer. The three megabanks including Mitsubishi UFJ do not directly operate retail exchanges. For a banking group, taking on retail trade intermediation carries heavy risk, and their strengths lie in corporate clients, trusts, and payment networks. Instead, the megabank camp is preparing for high-value interbank settlement and the issuance and settlement of tokenized assets through trust-type stablecoins. If SBI captures the retail investor space with exchanges and foreign-currency stablecoins, the banks capture the corporate space. As a result, this acquisition is a step for SBI to solidify its position on the retail gateway side.

Ultimately, this acquisition points to the reshaping of Japan's exchange market accelerating in step with the regulatory shift. As the FIEA amendment raises entry costs and a structure forms in which inflection points such as the 20% separate tax, a token whitelist, and spot ETFs all flow through licensed exchanges, the value of a license gets repriced. SBI moved before that repricing began in earnest. Whether further consolidation into large operators with capital follows in Japan's exchange market is the point to watch going forward.

[Institution] European Parliament Approves Digital Euro Bill and Begins Trilogue Negotiations

What Happened?

On June 23, the European Parliament's Economic and Monetary Affairs Committee (ECON) approved the digital euro bill and voted to begin final trilogue negotiations with member states. A matter over which central banks and commercial banks had clashed for three years over deposit outflows has moved to the final stage of legislation.

The bill opens the way to introduce both online and offline versions of the digital euro by 2029. The offline version allows direct phone-to-phone transfers without an internet connection and guarantees cash-like privacy. At the request of commercial banks, holding limits were set to prevent a mass exodus of deposits during a crisis, and the ECB plans to run a 12-month pilot with merchants and payment service providers.

ECB President Christine Lagarde has argued that a CBDC is needed to respond to the spread of dollar-pegged stablecoins such as Tether's USDT and Circle's USDC within Europe. The European Union cited the fact that about two-thirds of card transactions in the eurozone are processed through non-European companies such as Visa and Mastercard as grounds for pursuing the digital euro.

Researcher’s Comment

The rationale for the digital euro involves not only reshaping payment infrastructure but also a significant stake in monetary sovereignty. What the ECB worries about is a situation in which two levers of control, the payment network and money issuance, pass to operators outside the bloc. If payment infrastructure is tied to non-European card networks, fees, data, and outage response are governed by the policies of outside operators, and if dollar-pegged stablecoins encroach on payments and deposits within Europe, the monetary policy transmission channel and seigniorage weaken as well. The digital euro is an attempt to keep these two levers of control within the bloc by securing both a public payment rail that does not pass through card networks and a euro-denominated digital currency.

This rationale overlaps with the digital currency discussion in Asia. The shared problem awareness on both sides is viewing the spread of dollar stablecoins as a matter of monetary sovereignty and responding with digital payment infrastructure based on the domestic currency. However, the institutional conditions of the two regions differ. In Europe, the ECB, with a single currency and a single central bank, pursues one digital euro for the entire bloc, whereas in Asia, currencies and regulatory systems are divided by country, so the response is also scattered at the level of individual countries.

Even so, the Bank of Korea's Project Hangang, Japan's DCJPY, and the Hong Kong Monetary Authority's Project Ensemble all point in the same direction in that they have tested regulated digital payment instruments such as deposit tokens and wholesale CBDCs. Across the non-US world, the move to lower dependence on dollar stablecoins and secure infrastructure based on the domestic currency is growing.

The same week, Europe also tightened rules in the private sector. On June 26, Spain's securities regulator (CNMV) said there would be no exceptions or extensions for operators that have not obtained authorization ahead of the July 1 MiCA licensing deadline. Just before, Binance withdrew its license application in Greece, and customers in some member states began receiving fund withdrawal notices. If the digital euro is the work of building public payment infrastructure, MiCA enforcement is the work of deciding who remains in that market under which rules. Europe is moving in the direction of reducing dependence on the US in both money issuance and market regulation.

That said, the effect of the digital euro appears with a time lag. With a 2029 introduction target accompanied by holding limits and a 12-month pilot, it is closer to a long-term infrastructure move than to absorbing stablecoin demand right away. The holding limits set to ease commercial banks' fears of deposit outflows are themselves a device that constrains the pace at which the digital euro captures payments. While the digital euro takes time to settle into the payment network, if the euro stablecoin market under MiCA grows first, the division of roles between public and private will be redrawn in a form different from what is now expected. Where Europe places the weight of payment sovereignty, between public and private, is the point to watch in the next stage.

Others

Crypto

- Polymarket trading volume jumps 300% on World Cup effect, and Kalshi also records all-time-high open interest

- Meta moves to develop a prediction market app, Arena, similar to Polymarket and Kalshi

- Tether's USDT0 surpasses $100 billion in cumulative volume

- Sophon shuts down its own L2 chain and pivots to developing a Base-based consumer app

Institution

- BIS reiterates that stablecoins fail to meet the basic requirements of money

- US Senate moves to advance crypto market structure legislation in July, but timeline uncertainty grows

- Spain's financial regulator stresses no exceptions or extensions to MiCA for Binance and other crypto firms

Tech

- Base normalizes after a roughly two-hour halt in block production

- Bitmine, SharpLink, and Joe Lubin back Ethlabs, an R&D nonprofit for institutional Ethereum adoption

- Ethereum discusses a proposal to redirect up to 10% of validator rewards to ecosystem public-goods funding

Investment

- Kraken in talks to acquire a 15% stake in Aave Group with 35,000 ETH and 250,000 AAVE tokens

- The average IBIT investor enters a loss zone of about 40%

- Framework Ventures raises $400 million for its fourth fund

- Invesco files with the SEC to register an onchain fund targeting the stablecoin reserve market

- Allium raises $40 million in Series B amid rising demand for onchain data infrastructure

Asia

- Chainlink joins Project Pangea, involving 47 banks in Korea and Europe

- Ripple's RLUSD begins offering in the Japanese market through SBI VC Trade following Japan FSA approval

- SBI Group launches a pre-release version of the trust-type yen stablecoin JPYSC with Startale

- Toss Bank pursues a stablecoin-based cross-border remittance PoC with the Solana Foundation

- Kyobo Life completes a PoC for insurance premium collection and claims payment using a Korean won stablecoin

2. Data Spotlight

Korean Exchanges Facing a Volume Plunge. Is It Really a Crisis? (Link)

Ethereum Decentralization Through the Lens of New EIP Author Share, and a Warning Signal from 2026

3. Four Pillars Weekly

: : How Distributed Trust Absorbs Shocks: Lessons from the KelpDAO Incident and stETH's Resilience (Link)

- In April 2026, ~$292 million worth of assets were stolen from KelpDAO. The incident marked the collapse of a structure that had concentrated trust at a single point. Over the same period, Lido's staking token stETH, which sat outside the direct path of the damage, felt the shock of the incident but recovered quickly.

- stETH was not a target of the theft, but as the broader market turned to risk aversion, its exchange ratio against ETH drifted by as much as roughly -59 basis points, and execution costs widened temporarily. Even so, trading remained possible throughout the stress period. The direct foundation for this absorption lay in liquidity spread across many venues and in onchain data that could be verified in real time.

- Behind the depth and trust that stETH came to hold lies Lido's design, which avoids placing trust at a single point through measures such as validator decentralization, halting mechanisms that cannot move funds, exit rights at the governance level, and onchain treasury operations. This incident illustrated how a structure that concentrates trust and one that distributes it diverge when faced with the same shock.

: : What Should Exist on HyperEVM? (Link)

- HyperEVM should be evaluated as the smart contract layer that lets applications read and use HyperCore’s trading, collateral, positions, and risk.

- The right way to judge a HyperEVM app is to ask two questions. Why does it need EVM, and why does it need Hyperliquid?

- Basic apps such as swaps, lending, and asset wrappers are necessary, but the real differentiation comes from products that cannot work the same way without HyperCore.

- The long-term end state is an integrated account where one balance can move across trading, borrowing, yield, hedging, and payments.

: : Code is Not Law: Legal Context Protocol (Link)

- On June 24, a consortium that includes the American Arbitration Association and Integra Ledger unveiled the Legal Context Protocol. The standard begins from a single concern: as transactions in which agents pay and accept terms on behalf of people grow, the layer that records which terms applied, under which jurisdiction's law a deal took place, and what procedure to follow when something goes wrong has been left empty.

- LCP is not a standard that proposes new technology, but one that standardizes where terms are placed. It asks every service to put a JSON file containing the address of its terms document at a fixed path, then layers hash verification, signed consent, and dispute resolution links on top of that as optional steps in a four-tier structure. LCP does not require blockchain; it works with any web server that supports HTTPS.

- The interesting part is that, instead of settling agent transactions on-chain, LCP routes them back to the existing human legal system. The standard does not require any particular chain, but the upper tiers that build toward verification, signing, and storage rely on methods such as hashing and content addressing, which blockchains can provide in a more trustworthy form. Many of the chains that joined as founding contributors have long aimed at real-world assets and payments, and among them Sui is positioned to connect its own storage and encryption stack directly to those upper tiers.

Comments

- BitMine Can’t Own the Ethereum Network

- Korea, Taxation, and DAT

- This July is an Important Moment for Korea RWA Market

- STRC Has No Reason to Trade at $100

4. Macro & Onchain Metrics

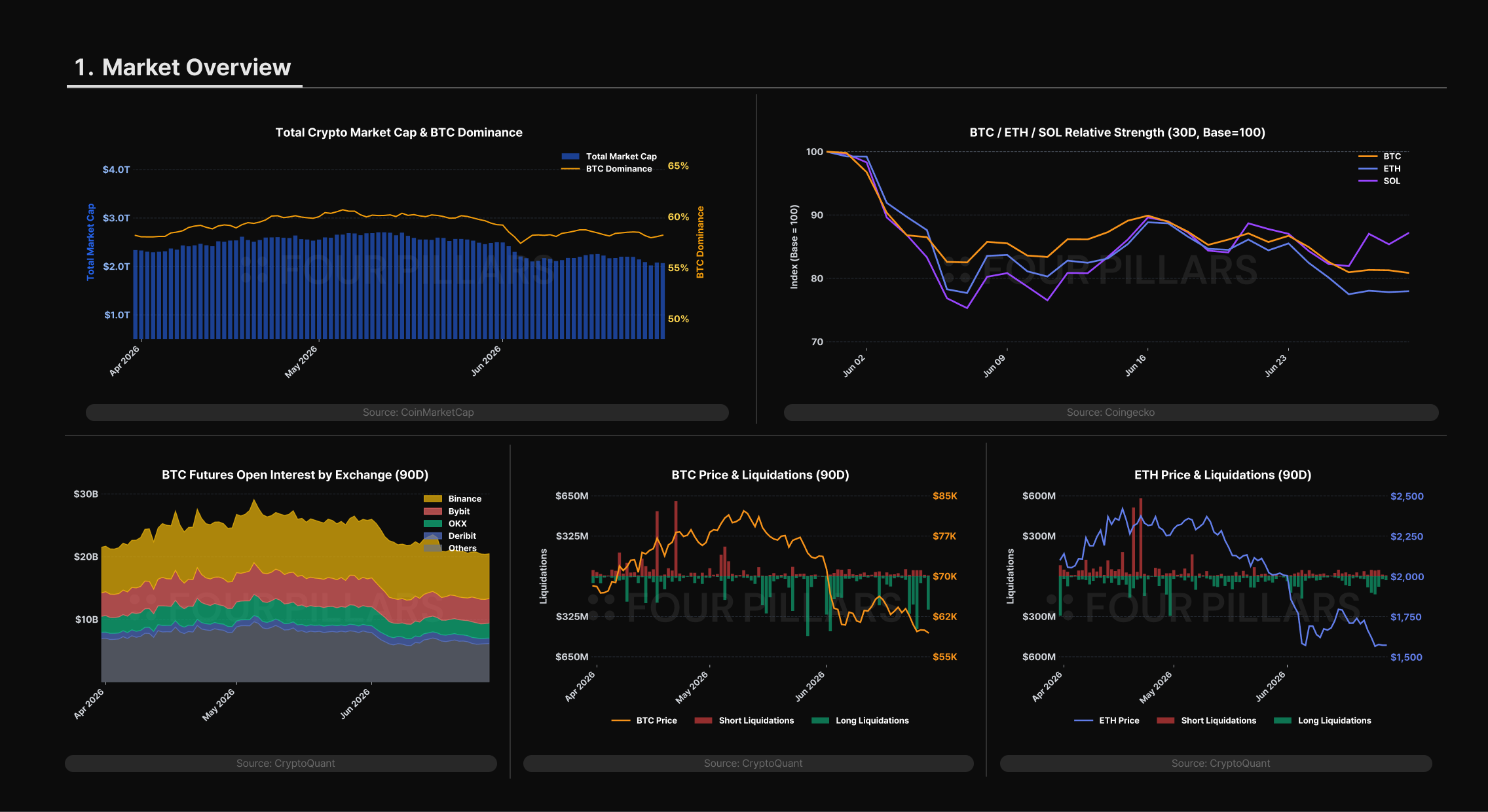

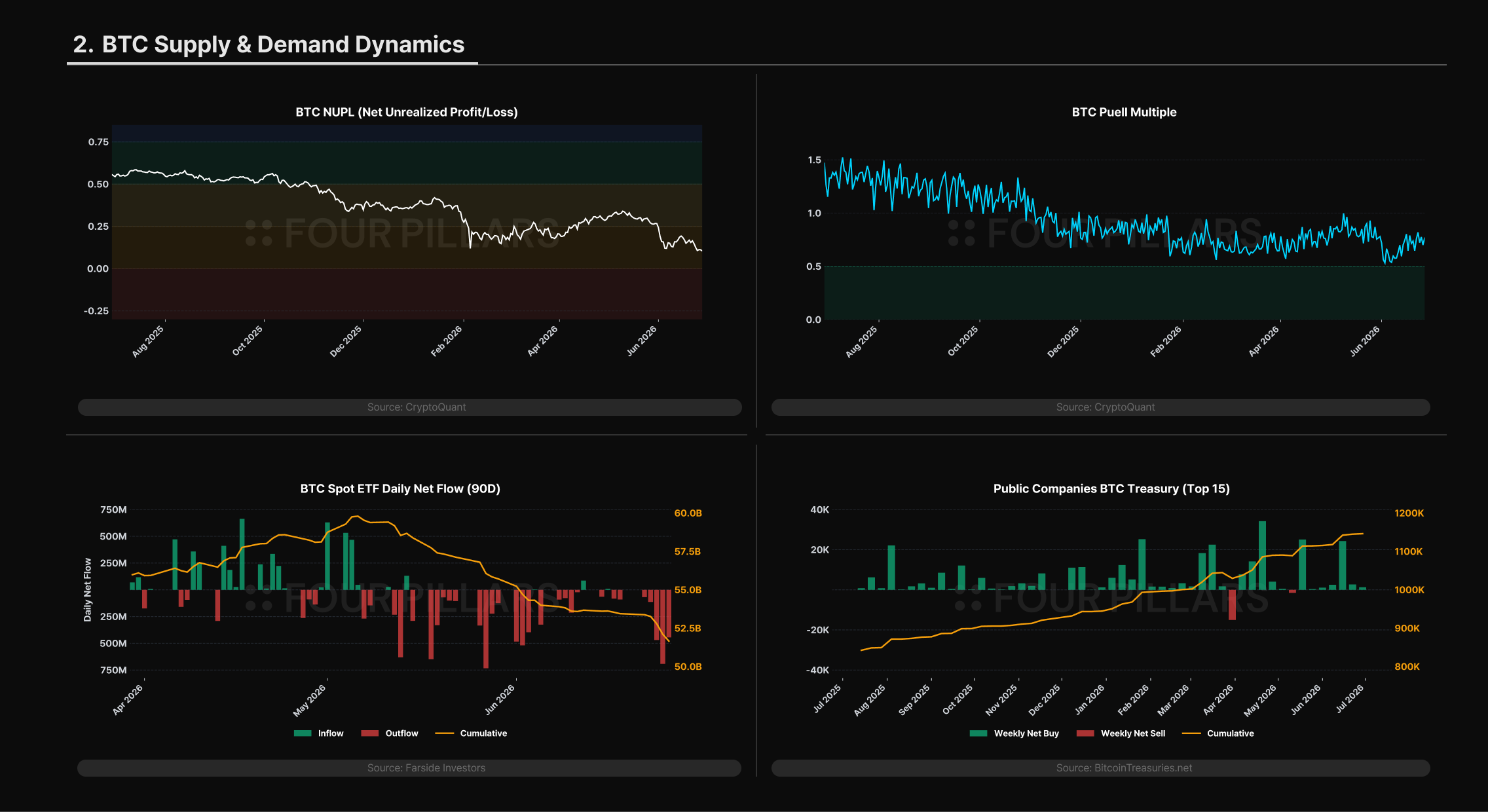

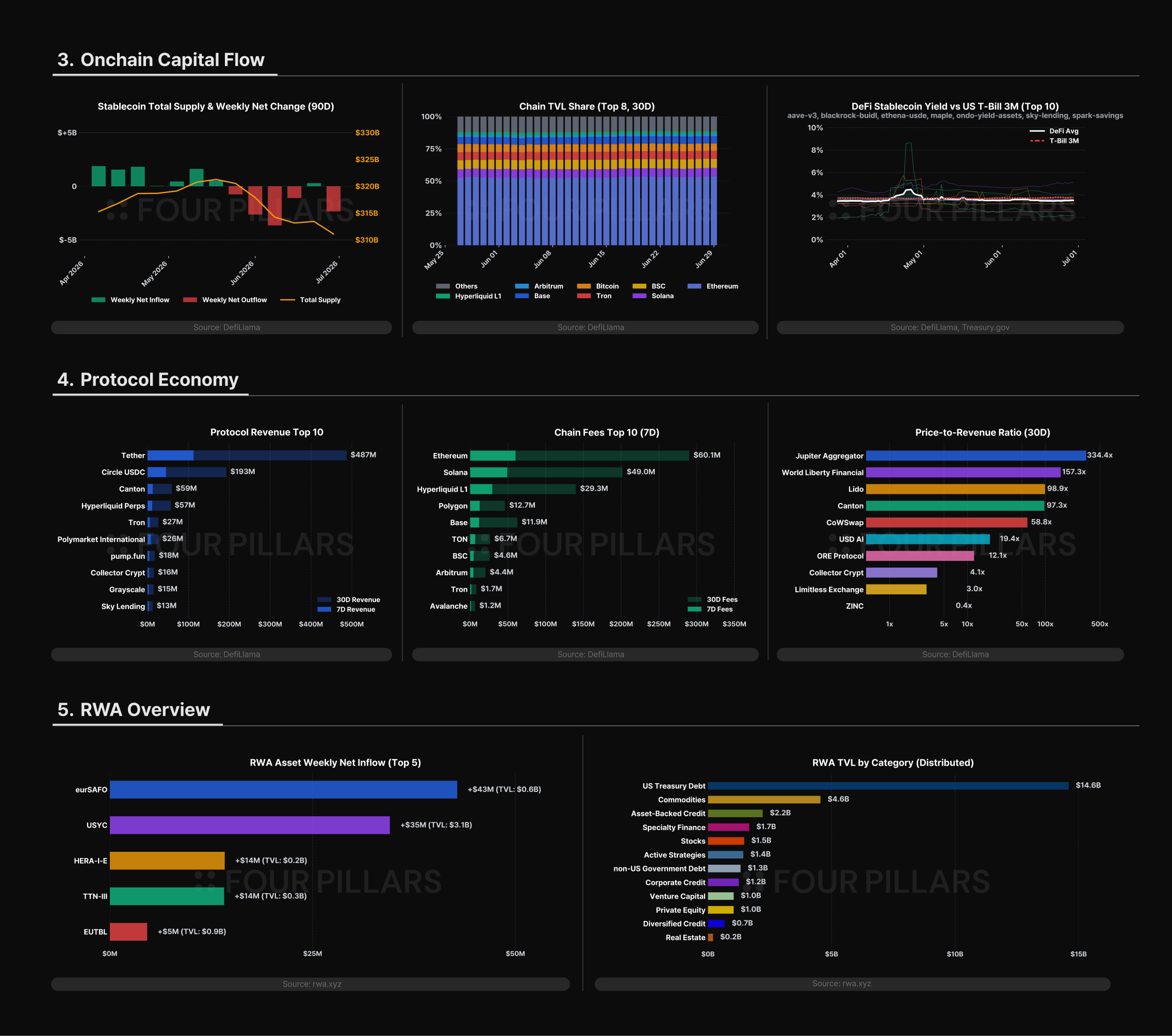

Some of the charts below are powered by CryptoQuant. For those interested in exploring the underlying data in greater detail, CryptoQuant provides access to a comprehensive suite of onchain and market analytics used by institutional participants.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![MSTR and COIN [FP Weekly 26]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F6ivhjsmqq8e3w1.png&w=1920&q=75)

![Signals from Wall Street and Japan's Securities Industry to the Crypto Market [FP Weekly 25]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fuh58gemqes9azi.png&w=1920&q=75)

![The Fall of Two Worlds: MSTR and ZEC [FP Weekly 24]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F9w86bhmq4oqczw.png&w=1920&q=75)