Table of Contents

Researcher

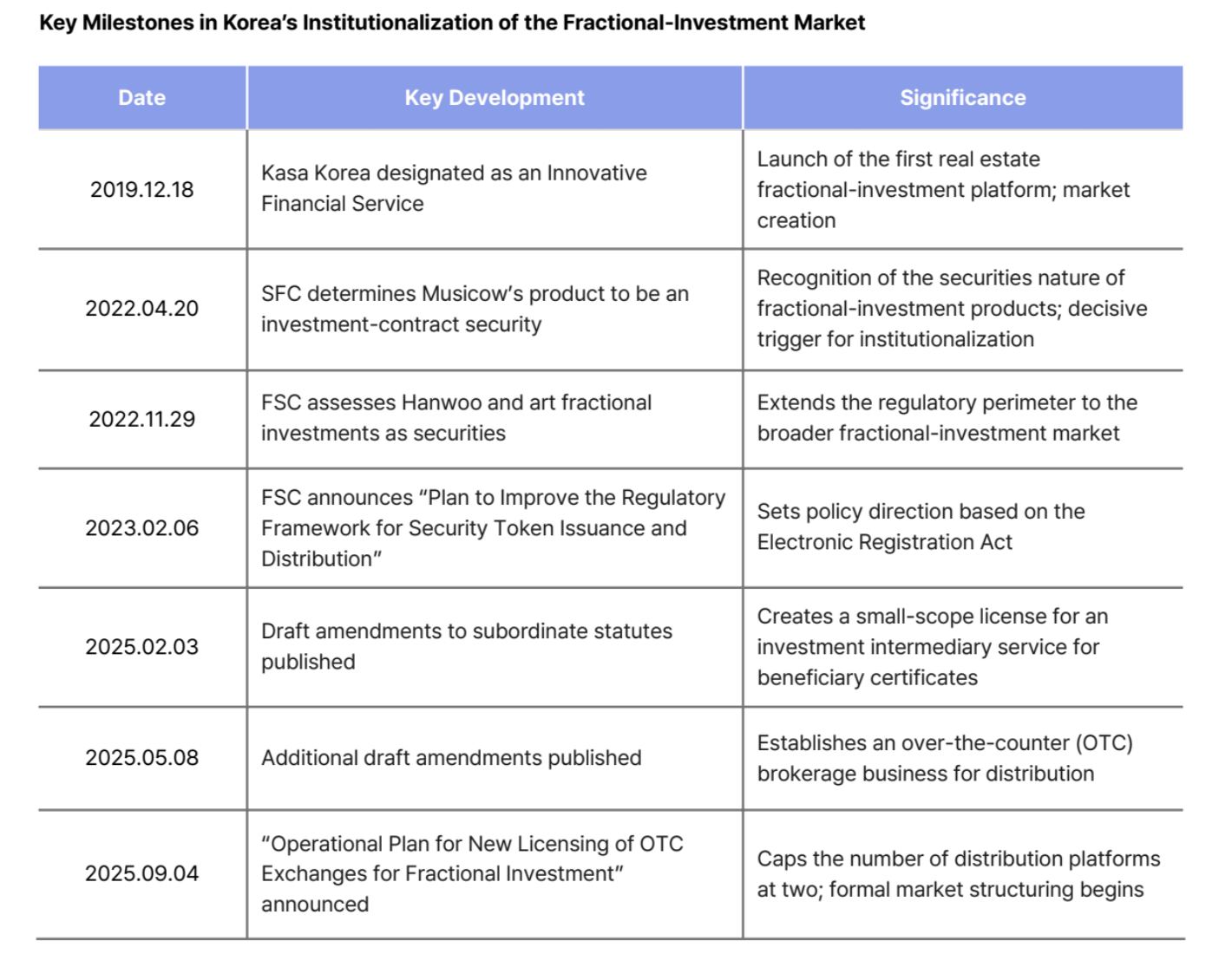

In Korea, the amended Electronic Securities Act and Capital Markets Act passed the National Assembly plenary on January 15, 2026, and they will take effect one year afterward, expected 4th Feb. 2027.

This would allow the issuance and trading of tokenized securities in Korea.

The FSC set up a joint consultative body (FSC, Financial Supervisory Service, Korea Securities Depository, KOFIA, plus industry and academia) that held its kickoff in February 2026. The detailed subordinate regulations these divisions produce (the issuance requirements, distribution structures, and infrastructure roles) are what the market has actually been waiting three years for.

The FSC has signaled it will publish its tokenized-securities guidelines in July 2026, ahead of the framework taking full effect.

In other words, January was the legal milestone, and July is the operational one. It is the most concrete digital-asset regulatory date Korea has on the calendar for all of 2026, and it will define whether the market opens wide or narrow.

1. What the Law Already Settled

Source: Press Releases - Financial Services Commission

Two structural decisions are locked in and won't change in July:

- Security tokens are a type of electronic security, not a new asset class. Blockchain-issued securities fall under the same legal regime as traditional electronic securities, so regulation attaches to whether something is a security, not to the token wrapper. This kills the legal-status ambiguity that stalled the fractional-investment (조각투자) market.

- Issuance and distribution are structurally separated. Asset holders and projects can issue tokenized securities, but trading and distribution must run through licensed securities firms or regulated OTC venues. The change in legislation also lets investment contract securities (currently art, livestock, etc.) circulate through licensed brokers for the first time, forming the investor-protection backbone of the regime.

2. The Caveat: Private Rails, Not Public

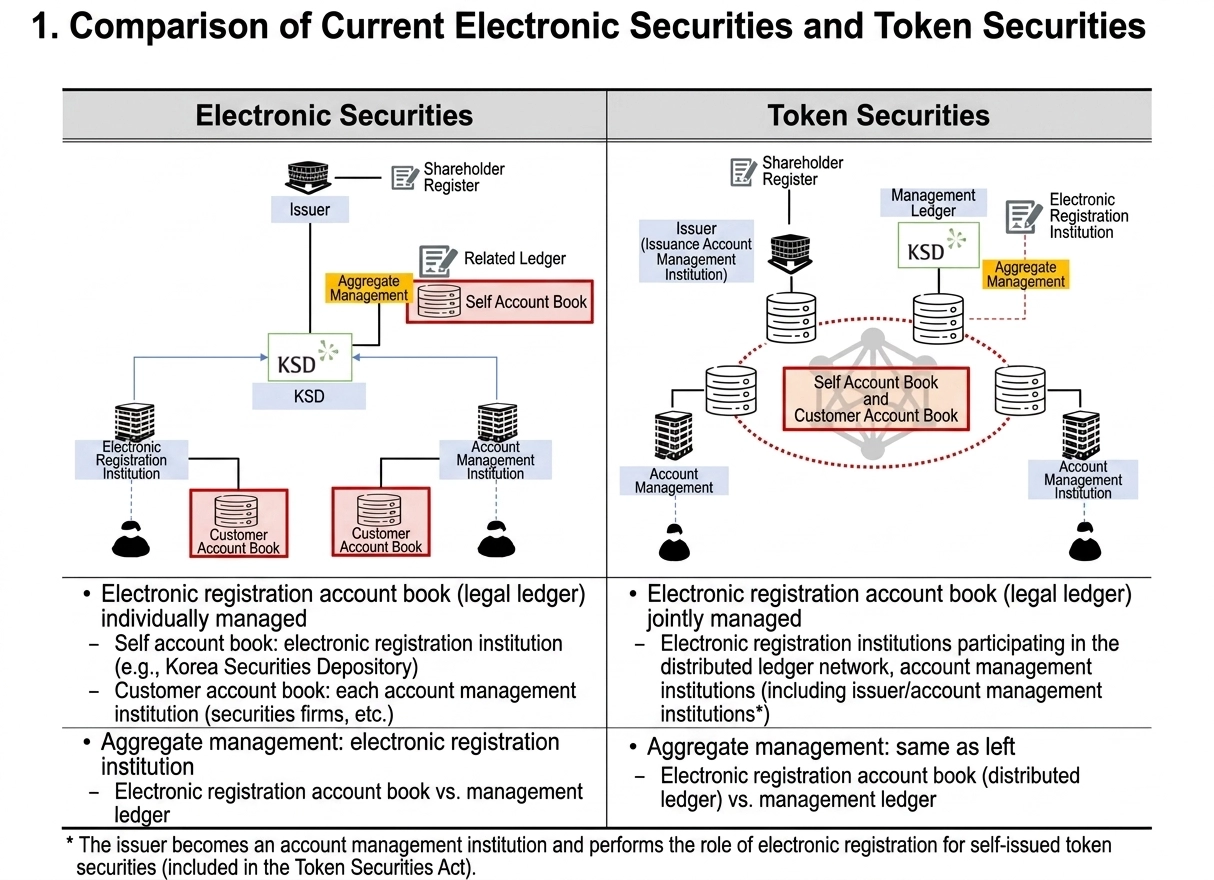

The most important thing to understand about Korea's model is that it is private, not public. The law's definition of "distributed ledger" prioritizes controllability and legal certainty over openness: "a ledger… jointly managed and protected from unauthorized deletion or retroactive modification." That is structurally different from a permissionless public chain, so securities will not be issued and traded directly on Ethereum the way the US is moving.

This has become a live controversy. The legislated framework requires issuers to link on-chain ledger records one-to-one with the KSD's aggregate management system, with KSD and Koscom sitting at the center for total-issuance control and capital-market stability.

Source: 한국예탁결제원, 토큰증권 테스트 베드 플랫폼 성공적으로 개시 - 머니투데이

For context, the Korea Securities Depository (KSD) is the country's central securities depository, the state-backed institution that registers, records, and settles virtually all of Korea's electronic securities. Koscom is the capital-market IT provider affiliated with the Korea Exchange, and it is expected to build and operate the blockchain infrastructure that links issuers to that registry. Routing every security token through KSD's master ledger and Koscom's rails is what gives regulators their total-issuance oversight.

Critics argue this routes "innovation back into the old mold," recreating the centralized depository structure on top of a blockchain, rather than letting distributed infrastructure do what it does best.

The July guidelines will have the details, and how much real distributed-ledger functionality survives the KSD linkage requirement, and how much smart-contract automation is actually permitted.

3. The Missing Piece: On-Chain KRW Settlement

Even a well-designed STO regime has a gap the July rules likely won't fully close: the settlement layer. If KRW-denominated bonds, funds, and private securities are issued on-chain but settlement still depends on off-chain bank transfers, the core benefits of tokenization, namely T+0 instant settlement, 24/7 trading, and programmable/atomic delivery-vs-payment, never materialize.

The answer isn't a KRW stablecoin first, either. Unlike USD stablecoins, a KRW stablecoin has limited utility without on-chain assets to settle against. The optimal path would be parallel development tokenizing KRW-denominated assets and standing up KRW stablecoins / tokenized deposits together, so the full issuance → distribution → settlement cycle runs on-chain.

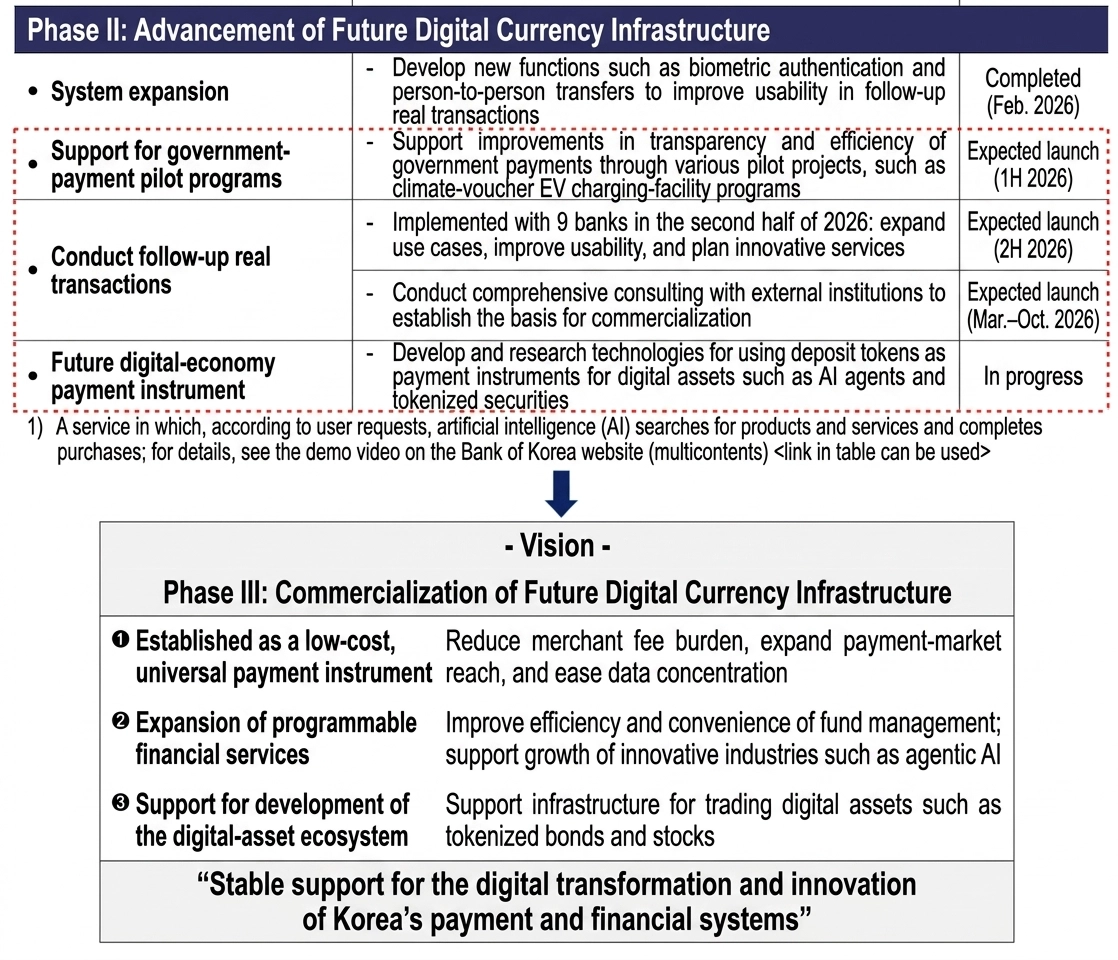

This is also where the Bank of Korea's Project Han River tokenized-deposit pilot could become strategically relevant to the STO timeline. In March 2026 the BOK launched Phase II of Project Han River, which explicitly investigates using deposit tokens as a settlement layer for tokenized securities such as digital bonds and stocks.

Source: [보도자료] 한국은행, 「프로젝트 한강」 2단계 본격 추진 | 기타 보도자료(상세) | 보도자료 | 뉴스 및 의사록 | 뉴스/자료 | 한국은행 홈페이지

If that link holds, the infrastructure question playing out around KSD could be answered on the payment side by regulated tokenized deposits rather than a KRW stablecoin.

4. The Distribution Battle: Who Runs the OTC Venues

One of the most consequential pieces of the framework is who actually runs distribution. The legislation created a new license, OTC brokerage business(장외거래중개업), as the regulated channel to solve the old fractional-investment problem where each asset could only trade on the app of its own issuing platform. Issuance and distribution must remain structurally separated.

The number of OTC platforms is capped at two. In October 2025, preliminary approval went to two consortium:

- KDX, led by the Korea Exchange (KRX) and Koscom with Kiwoom Securities, Kyobo Life, and Kakao Pay Securities (~45 firms, Busan-based)

- NXT, led by Nextrade with Shinhan Investment, Hana Securities, and Musicow.

Scope is initially limited to non-standard securities (i) investment-contract securities (투자계약증권) and (ii) non-monetary trust beneficiary certificates (비금전신탁 수익증권). Standard stocks and bonds keep running through existing infrastructure, though both consortia are already pushing to expand into bond and equity-fund tokenization.

The issue is that there would be a structural ceiling on the innovators. the fintech and platform players who actually built the fractional trading market are relegated to consortium members rather than venue operators, so the upside of the new license accrues to incumbents. For example like the sandbox appoved companies like Lucent block, Kasa Korea, etc.

How the July guidelines draw that scope line, and whether they leave room for a third entrant later, will decide whether distribution becomes genuinely competitive or simply re-concentrates around the existing order.

5. What to Watch in July

- Distribution licensing: Final licensing terms, capital, and technical requirements for the two OTC venues (see above).

- KSD linkage mechanics: How tight is the one-to-one ledger linkage, and how much does it constrain genuine on-chain functionality?

- Smart-contract scope: Which lifecycle functions (coupon payments, redemptions, transfers) can be automated on-chain, vs. which must mirror KSD?

- Eligible assets & issuer qualifications: What can be tokenized first, and who qualifies to issue? (I expect tokenized stocks will take time.)

- Settlement signal: Any linkage to tokenized deposits / KRW settlement rails or BOK pilots.

For the crypto industry in the short term, private-chain security tokens and the public-chain ecosystem will largely remain separate worlds.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.