![CLARITY Act: Clearer Rules, Clearer Market Lines [FP Weekly 21]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Forosgimpbb0d59.png&w=1920&q=75)

Table of Contents

- 1. Major News

- [Institution] CLARITY Act Passes Senate Banking Committee: The Emerging Shape of the U.S. Crypto Market

- [Asia] Korean Financial Institutions Race for Exchange Stakes: Securing Distribution Channels Ahead of DABA

- Others

- 2. Data Spotlight

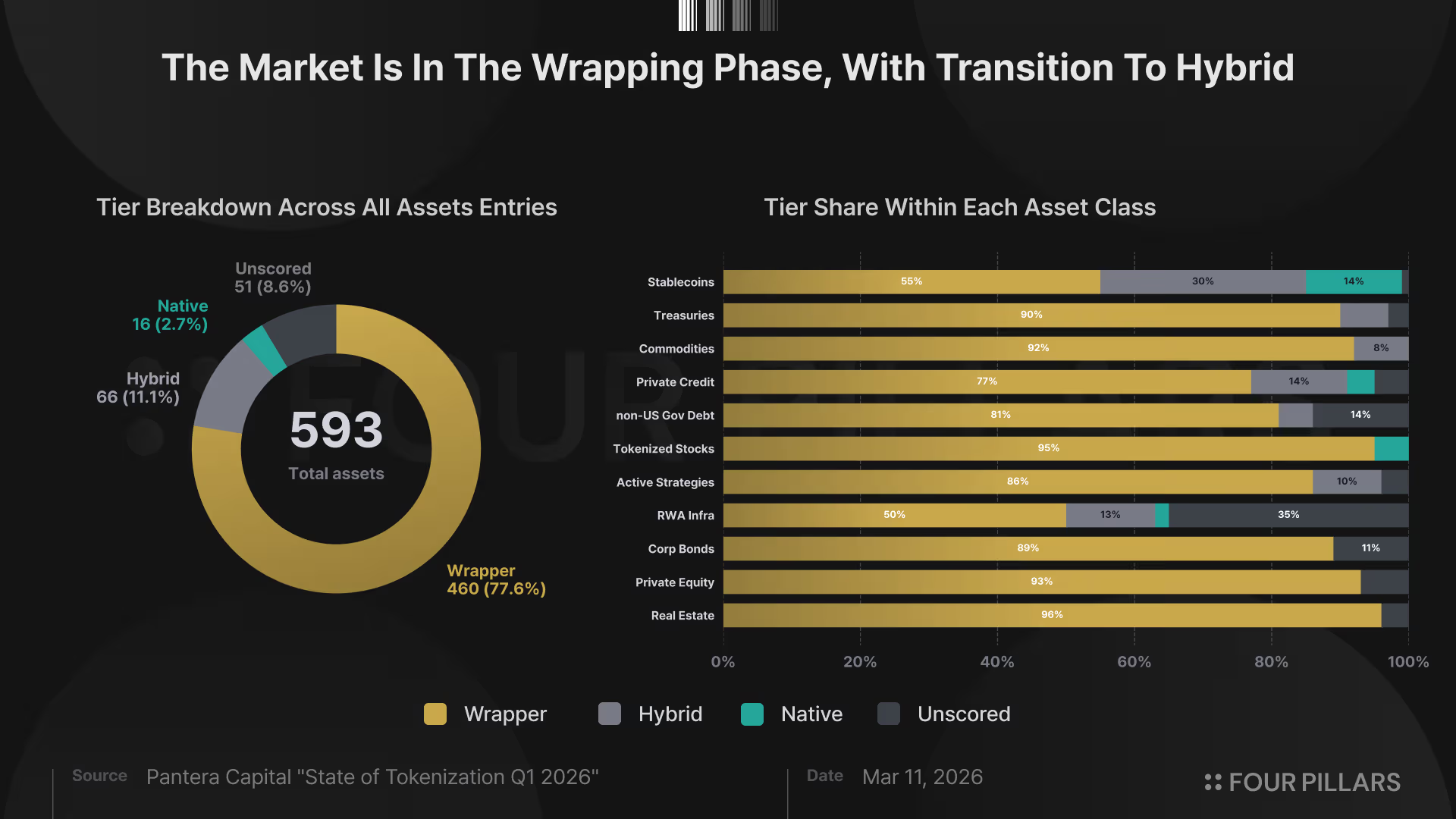

- The State of the Tokenization Market Through TPI (Link)

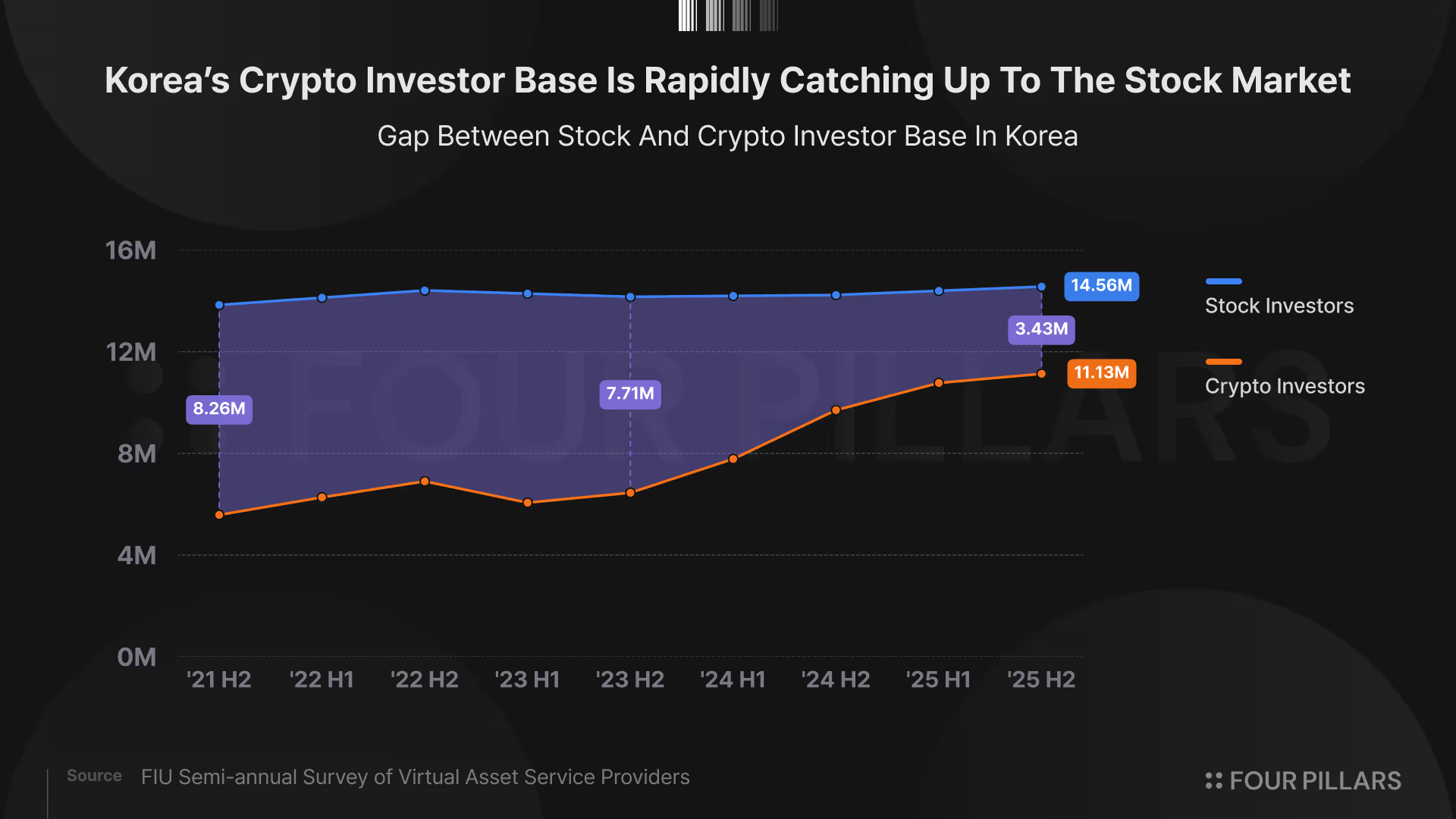

- The Korean Web3 Market In Data (Link)

- 3. Four Pillars Weekly

- : : 2026 Korean Web3 Market Report: Structure, Regulation, and Ecosystem (Link)

- : : Understanding Quantum Threats to Blockchain Security (Link)

- : : Trade[xyz] 2026 Q1 Report (Link)

- : : Monthly EIP - Apr 2026 (ft. Staked Assets at Work, The Prepared Win) (Link)

- : : Clear Signing: The Last Line of Defense Ethereum Rebuilds (Link)

- : : I Don’t Buy the ZEC thesis (Link)

- : : The New Frontier: The Application Ecosystem Blooming on Arcium (Link)

- Comments

- 4. Macro & Onchain Metrics

Researcher

1. Major News

[Institution] CLARITY Act Passes Senate Banking Committee: The Emerging Shape of the U.S. Crypto Market

What Happened?

The U.S. Senate Banking Committee passed the CLARITY Act, a comprehensive digital asset market structure bill, in a 15-to-9 vote on May 14. The bill establishes clear rules for digital assets. After clearing the committee, it moves to a full Senate floor vote.

The vote was led by Republicans but secured some Democratic support. All Republican members voted in favor, along with two Democratic senators, Ruben Gallego and Angela Alsobrooks. However, Democrats continue to raise concerns over anti-money laundering (AML) provisions, consumer protection, and crypto-related conflicts of interest among political figures.

The bill's primary objective is to clarify the jurisdictional boundary between the SEC and the CFTC over digital assets. It defines classification criteria for tokens as securities or commodities, and brings digital commodity exchanges, brokers, and dealers under the BSA (Bank Secrecy Act)-based AML/KYC regulatory framework.

The vote also sharpened the regulatory direction on stablecoin rewards. The updated CLARITY Act draft explicitly prohibits paying rewards on simple stablecoin holdings that are economically similar to bank deposit interest. However, rewards based on actual economic activity such as payments, transactions, and platform usage remain exempt.

Banks have argued that stablecoin rewards could trigger deposit flight, while crypto firms have contended that a blanket ban on rewards would be anti-competitive. The codified provision is effectively a compromise that restricts stablecoins to payment and transaction infrastructure rather than deposit-like yield products.

The CLARITY Act has not yet been finalized. A full Senate floor vote, coordination with the Senate Agriculture Committee on CFTC jurisdictional provisions, reconciliation with House bills, and presidential signature are still required. A key variable going forward is whether the bill can be processed within 2026. If it fails to pass Congress this year, the legislative momentum may weaken as the congressional composition shifts after the midterm elections.

Researcher’s Comment

The CLARITY Act does not deliver a uniform tailwind across the entire crypto market. The bill's effects specify the conditions under which exchanges, brokerages, stablecoins, DeFi, and onchain derivatives can each operate within the U.S. market. Regulatory clarity opens expansion paths for some firms, while models that previously operated in gray zones face greater compliance demands. If the bill is finalized, the following changes are expected:

First, the playbook for incentivizing stablecoin holders will change completely. Platforms will no longer be able to offer incentives to users simply for holding stablecoins. For example, Coinbase would no longer be able to pay rewards to USDC holders within its app, and PayPal likewise would not be able to offer rewards to PYUSD holders within its app. To offer rewards, platforms will need stablecoins to be used in activities such as payments, remittances, trading, or liquidity provision. This will require platforms to design more complex incentive structures.

Second, as crypto is incorporated into the regulated asset framework, new markets open up. In particular, once jurisdictional criteria are clarified, crypto firms will need to pre-design token structures, governance rights, issuance mechanisms, and the roles of foundations and operating entities to obtain classification as securities or digital commodities. After SOX, the internal controls advisory market grew significantly. After NSMIA, federal-state jurisdictional classification advisory services emerged. After the JOBS Act, demand for capital-raising pathway design surged. Similarly, post-CLARITY Act, an advisory market for token securities-digital commodities classification, SEC-CFTC jurisdictional determination, and the associated disclosure and registration requirements is likely to form.

Third, crypto assets expand from trading instruments to underlying assets for financial services. Once digital commodity exchanges, brokers, and dealers are brought under the BSA-based AML/KYC framework, traditional financial institutions can more easily treat crypto as an asset class for lending, collateral management, and custody. For example, a prime brokerage market where institutional investors can handle trade execution, custody, lending, collateral management, and clearing in an integrated manner is already forming in crypto. Cantor Fitzgerald's $2 billion bitcoin financing business, Ripple's $1.25 billion acquisition of Hidden Road, and FalconX's $8 billion valuation show that capital is already moving in this direction.

Whether the CLARITY Act is finalized this year remains uncertain, but the direction confirmed by this vote is clear. Stablecoins are positioned as payment infrastructure. Tokens enter the securities and digital commodities classification framework. Crypto brokers come under the BSA-based AML/KYC regime. Some will choose to enter the regulatory framework and connect with institutional capital, while others will strengthen decentralized, non-custodial, and offshore structures to remain in the onchain-native market. Regardless of direction, as regulatory clarity progresses, the crypto market is likely to bifurcate more sharply.

[Asia] Korean Financial Institutions Race for Exchange Stakes: Securing Distribution Channels Ahead of DABA

What Happened?

Hana Financial Group announced on May 15 that Hana Bank will acquire a 6.55% stake in Dunamu for approximately KRW 1.003 trillion. The acquisition target is 2,284,000 shares of Dunamu held by Kakao Investment. Upon completion, Hana Bank will become Dunamu's fourth-largest shareholder, after Chairman Chi Hyung Song, Vice Chairman Hyung Nyun Kim, and Woori Technology Investment. Dunamu operates Upbit, the largest virtual asset exchange in Korea, and this investment is exceptionally large among investments by domestic commercial banks in digital asset companies.

Hana Financial plans to link this investment to strategic business collaboration with Dunamu. The two companies announced they will jointly pursue blockchain-based overseas remittances, a KRW stablecoin ecosystem, and wealth management (WM) services combining digital asset capabilities. The structure secures an exchange stake while opening collaboration possibilities in remittance, stablecoins, and asset management.

Other financial firms are also moving to secure exchange stakes. Korea Investment & Securities is in discussions with global exchange OKX to jointly invest in Coinone. The two parties are reportedly considering acquiring approximately 20% stakes each. However, Coinone stated that while strategic investment and partnership discussions are underway, nothing has been finalized. Meanwhile, Mirae Asset Group has already entered the exchange stake competition. Mirae Asset Consulting agreed in February to acquire a 92.06% stake in Korbit for KRW 133.5 billion.

Taken together, Hana Bank's Dunamu investment, Korea Investment & Securities' Coinone investment discussions, and Mirae Asset's Korbit acquisition show that Korean financial institutions' interest has moved beyond exchange partnerships to equity acquisition. The backdrop is Korea's legislative environment, where the Digital Asset Basic Act (DABA) and security token regulation are being discussed simultaneously. DABA, in particular, is the central pillar of Korea's second-phase digital asset legislation, encompassing KRW stablecoin regulation and VASP regulatory reform. If National Assembly discussions begin in earnest in the second half of this year, the bill's specific contours are likely to emerge.

Researcher’s Comment

The race among Korean financial institutions for exchange stakes is less a short-term bet on the crypto price cycle than a move to secure distribution channels ahead of institutionalization. The Digital Asset Basic Act, KRW stablecoin legislation, and security token regulation all point toward digital assets being incorporated into the regulated market.

From the financial sector's perspective, the key to post-institutionalization commercialization narrows to where assets are traded and which distribution networks are occupied. Exchanges are already infrastructure equipped with VASP licenses, real-name account-based KRW on/off-ramps, a retail user base, and KRW market liquidity. If KRW stablecoins and crypto assets are permitted within the regulated framework, exchanges can function as the initial distribution network for KRW-denominated digital assets.

Korean exchanges hold a particularly strong position in crypto trading. Korea is the second-largest retail market for global crypto spot trading volume after the U.S., and Upbit alone ranks among the top exchanges globally in daily trading volume. As DABA takes shape and digital assets enter the regulated framework, exchanges with this retail liquidity and KRW settlement access become not just trading platforms but gateways for KRW-denominated digital asset distribution. Financial institutions are securing stakes to lock in options on this gateway.

Others

Crypto

- Jito Labs launches retail trading terminal JTX

- Chainlink CCIP gains over $2.5B TVL from LayerZero migration

- Coinbase joins as official USDC treasury deployer for Hyperliquid

- Starknet launches ZK-based strkBTC

Institution

- Boundary announces institutional verifiable stablecoin USBD

- U.S. Senate Banking Committee passes CLARITY Act

- JPMorgan pursues second tokenized money market fund on Ethereum

- Bank of England considers easing pound stablecoin regulations

Tech

- Ethereum Foundation unveils Clear Signing standard to prevent malicious transaction approvals

- THORChain halts trading after $10M cross-chain exploit

Investment

- Osero raises $13.5M led by Sky ecosystem

- Bitwise Hyperliquid ETF begins trading on NYSE

- Harvard exits ETH ETF position; Abu Dhabi sovereign fund expands BTC position

- Ledger shelves U.S. IPO plans due to market conditions

Asia

- Hana Bank acquires 6.55% stake in Dunamu for about KRW 1 trillion

- Korea Investment & Securities and OKX explore joint stake investment in Coinone

- Japan Blockchain Foundation plans B2B settlement JPY stablecoin EJPY

- Crypto.com obtains UAE license tied to Dubai government crypto payments

2. Data Spotlight

The State of the Tokenization Market Through TPI (Link)

The Korean Web3 Market In Data (Link)

3. Four Pillars Weekly

: : 2026 Korean Web3 Market Report: Structure, Regulation, and Ecosystem (Link)

- South Korea, with a population of 52 million, has more than 11 million cryptocurrency exchange account holders, making it one of the world's leading markets in terms of crypto investment per capita. Yet despite this enormous participation base, the energy of the Korean market is largely concentrated in short-term trading on centralized exchanges, while onchain activity and the builder ecosystem remain remarkably thin relative to the market's size.

- The enforcement of the Virtual Asset User Protection Act (Phase 1) in 2024, the announcement of the corporate participation roadmap, and the legislative push for the Digital Asset Basic Act (Phase 2) in 2026 are opening an opportunity to fundamentally restructure the Korean market. The introduction of a regulatory framework for won-pegged stablecoins, the launch of the STO market, and the full-scale entry of corporate investors could mark a turning point at which the Korean market, long stigmatized as a "hotbed of speculation," finally joins mainstream financial infrastructure.

- This report aims to quantitatively analyze the structure and regulatory environment of Korea's Web3 market as of April 2026, and to provide practical insights for global projects and institutions considering entry into the Korean market.

: : Understanding Quantum Threats to Blockchain Security (Link)

- Hash functions like SHA-256 and Keccak-256, and PoW consensus itself, are not realistic primary targets of currently known quantum attacks. The more direct risk is concentrated in addresses that have already exposed their public keys (such as Satoshi's), reused accounts, admin keys, validator keys, and the signing structures of bridges and oracles.

- Each chain faces a different version of the quantum problem. Bitcoin's bottleneck is legacy UTXOs and conservative governance. Ethereum's bottleneck is the complexity of its account model and smart contract permissions. Solana has to deal with the performance cost of post-quantum signatures. Cosmos SDK chains have to balance the flexibility of individual transitions against IBC interoperability.

- The exact date of Q-Day matters less than having transition options ready in advance. The arrival of CRQC is uncertain, but expert surveys and institutional reports point to 2030 to 2035 as the critical preparation window. Migration can take years, so the time to build transition paths and reach social consensus is now, while there is still time, not after the threat materializes.

- The quantum transition is not a security patch. It is a social transition. Blockchain set out to replace trust with code and consensus, but that code and consensus rest on cryptographic assumptions. When a technology like quantum computing breaks the underlying security assumptions, the code has to change and the consensus has to be rebuilt. Whether each network can carry out this transition in an orderly way will decide whether it can remain a sustainable piece of social infrastructure.

: : Trade[xyz] 2026 Q1 Report (Link)

- Q1 2026 answered the question that launched Trade[XYZ]: can perpetual derivatives on real-world assets function as serious market infrastructure, not just as a crypto novelty? The evidence in this report says yes.

- $112.87B in volume, 48 consecutive days of OI ATHs, spreads converging toward native crypto perps within a single quarter, and weekend prices that outperformed the Friday close as a TradFi reopen predictor in 76.6% of observations. Two macro stress events — a silver crash and an oil crisis — processed without a halt. These outcomes are measured, documented, and hold up to scrutiny.

- The growth rate is real but requires context. +857% QoQ against a peer group that contracted 40% reflects genuine share capture. But the fee environment is deliberately compressed, two discrete stress events drove the volume peaks, and monetization at 0.70 bps understates long-run earnings power significantly. How the volume base responds to eventual fee normalization is also a central unanswered question heading into Q2.

- Risks remain material. Regulatory uncertainty is the largest structural variable — U.S. retail access is restricted today, and the SEC-CFTC policy process will shape the addressable market more than any product decision. Competition will likely intensify as the revenue profile becomes visible.

- What cannot be taken back: the architecture held under stress, market quality improved faster than expected, and the S&P Dow Jones licensing agreement — awarded five months into existence — confirmed that institutional recognition has arrived.

: : Monthly EIP - Apr 2026 (ft. Staked Assets at Work, The Prepared Win) (Link)

- April's EIP activity, much like the first quarter, saw active new proposals at the core layer, with EIPs aimed at supporting a range of use cases at the signature scheme and application layers standing out in particular.

- Community discussions unfolded along two axes: "the safe structuring of the Glamsterdam and Hegota upgrades" and "strengthening the trusted network foundation for native applications.”

- Meanwhile, as the center of gravity in the staking asset market shifts toward solutions with high on-chain utilization, the protocols that will lead this market will be those that have quickly attained both Web3 scalability and Web2 accountability at once.

: : Clear Signing: The Last Line of Defense Ethereum Rebuilds (Link)

- On May 12, 2026, the Ethereum Foundation officially launched the Clear Signing standard. It is a structural attempt to address the long-standing problem of blind signing.

- The standard consists of three main components: ERC-7730, a JSON format that describes transaction intent in human-readable form; ERC-8176, which allows the accuracy of a Descriptor to be cryptographically verified by external parties; and a neutral registry that anyone can mirror. Because descriptors exist off-chain, the standard can be applied to existing contracts without redeployment, as long as wallets implement it.

- However, the standard itself does not guarantee safety. Coverage depends on voluntary participation by the protocols that write descriptors, and the responsibility for deciding which descriptors to trust is also distributed across wallets. UI-layer attacks such as the Bybit hack can only be blocked when verification is performed on the hardware wallet's own screen, and Clear Signing matters precisely because it provides the foundation for displaying genuinely meaningful information on that screen.

: : I Don’t Buy the ZEC thesis (Link)

- Financial privacy may become more valuable, but that does not mean users will want exposure to a volatile privacy coin.

- Shielded supply and quantum-readiness are powerful narrative accelerants, not evidence of durable monetary demand.

- ZEC may work as a trade, but the multi-cycle monetary asset thesis remains unproven

: : The New Frontier: The Application Ecosystem Blooming on Arcium (Link)

- The Arcium ecosystem is not a single application but takes the form of an application network, with 7 categories being built in parallel.

- Each application leverages different aspects of Arcium's multi-party computation (MPC). Examples include confidential balances based on Confidential Token Accounts, token launchpads built on sealed-bid auctions, prediction markets based on confidential betting, and asymmetric information market mechanisms. All of these are applications that were difficult to implement on existing transparency-based blockchains, or that proved unworkable from a user experience standpoint.

- In addition, Arcium's Confidential Token Standard (C-SPL) strengthens composability across applications in the ecosystem. This forms a new layer of capital markets on top of Solana, generating synergies that go beyond a simple sum of features.

Comments

- USDC becomes Hyperliquid’s aligned quote asset

- Lido EarnETH's First-Loss Activation: Notes on Revenue-Backed Vault Protection

4. Macro & Onchain Metrics

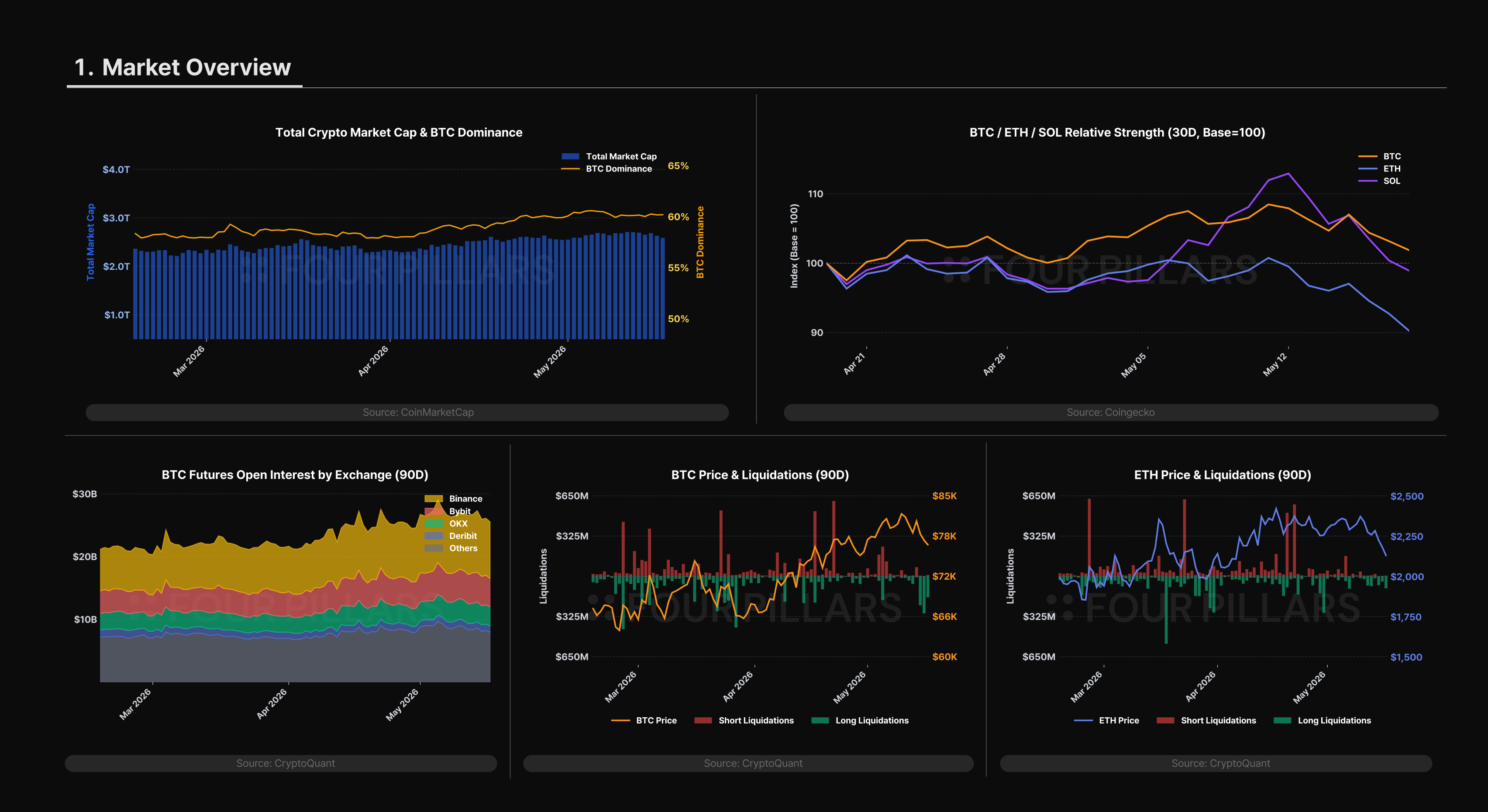

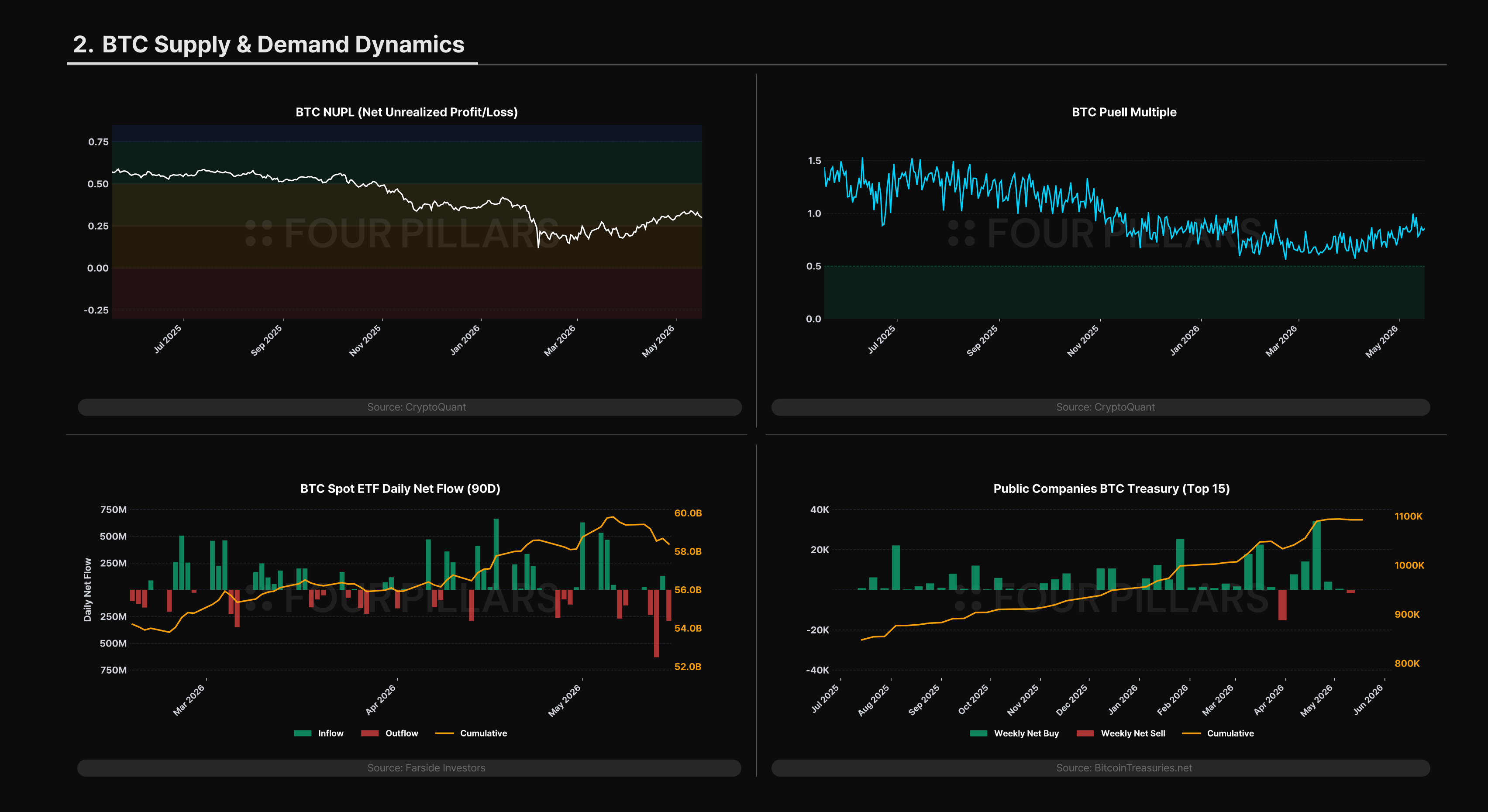

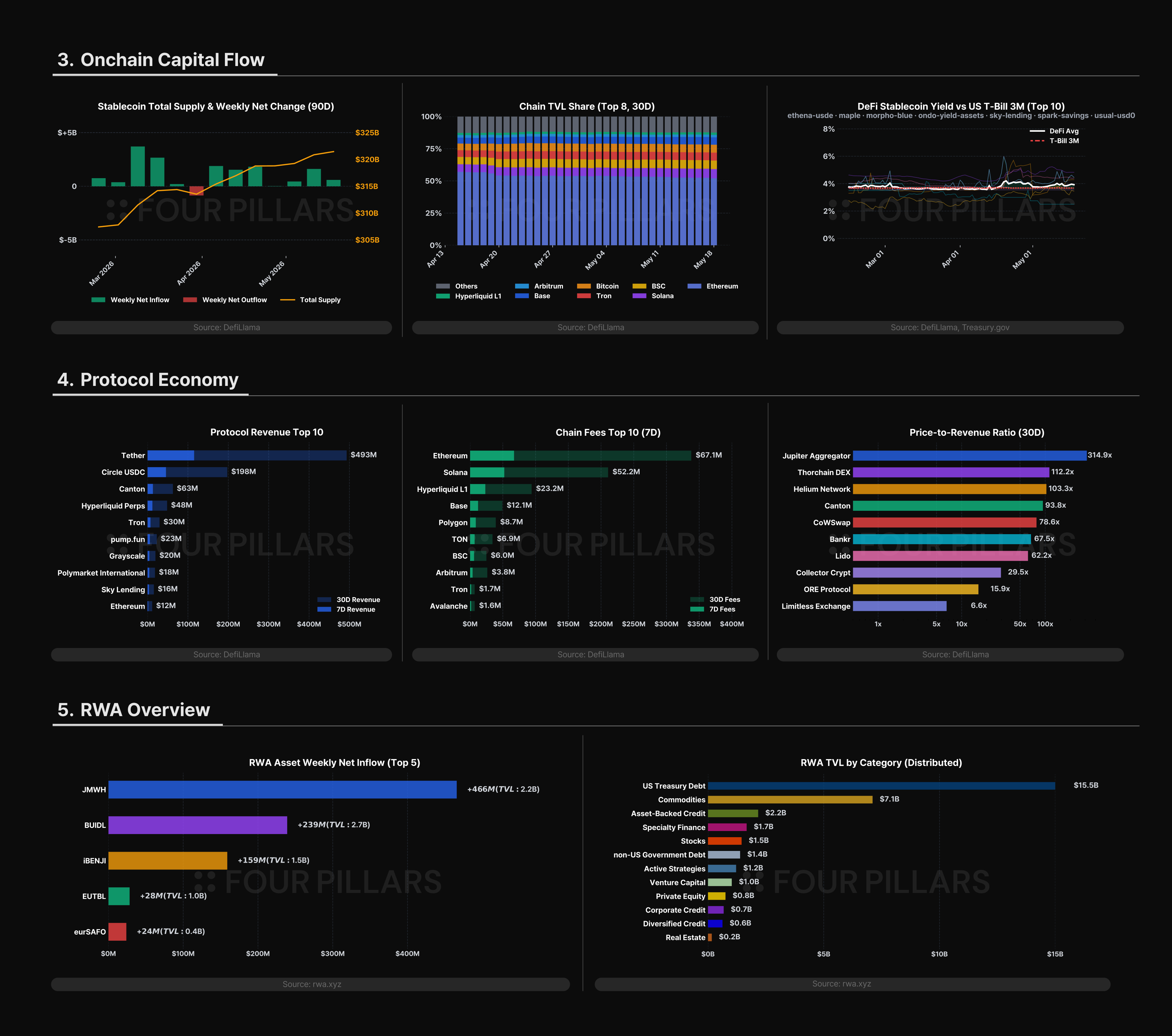

Some of the charts below are powered by CryptoQuant. For those interested in exploring the underlying data in greater detail, CryptoQuant provides access to a comprehensive suite of onchain and market analytics used by institutional participants.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![License Is All You Need [FP Weekly 27]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Ft4v9kemqys40d1.png&w=1920&q=75)

![MSTR and COIN [FP Weekly 26]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F6ivhjsmqq8e3w1.png&w=1920&q=75)