Table of Contents

In its State of Tokenization Q1 2026 report, Pantera Capital frames today's tokenization market as a parallel to the early days of internet media. Publishers back then copied print articles onto websites, improving delivery and availability without changing the format itself. Tokenization, the report argues, is doing much the same. Existing assets have been distributed on chain, but the native financial instruments that will eventually define what tokenization actually becomes have yet to appear. Pantera labels this the "Newspaper-on-a-Website Phase." Every major bank, custodian, and asset manager now has a tokenization strategy, yet market activity alone does not reveal whether these tokenized assets are realizing blockchain's full potential or simply sitting as digital wrappers around traditional infrastructure.

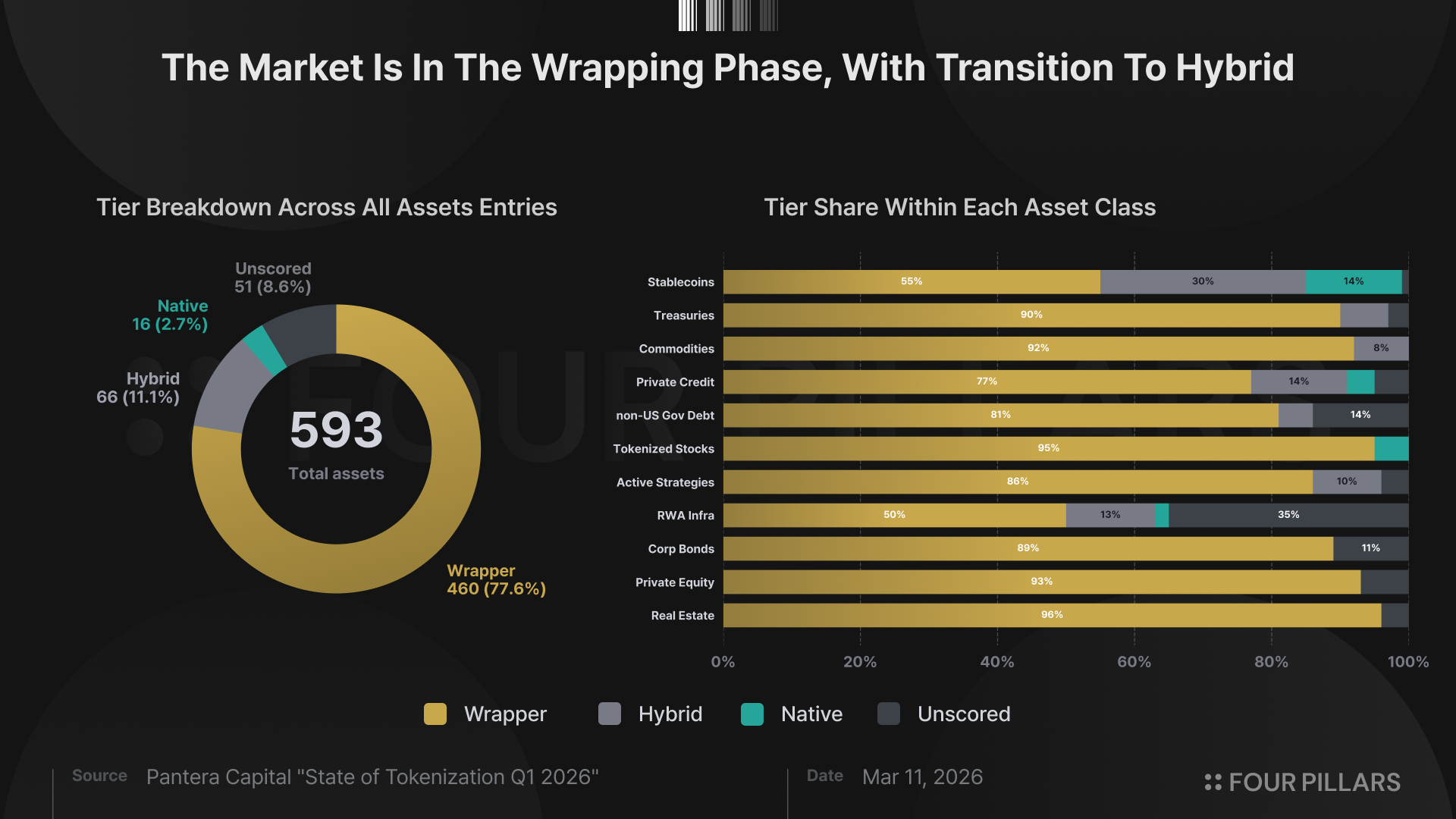

To put numbers behind this picture, the report examines 593 tokenized assets across 11 asset classes, representing roughly $320.6B in tracked market value. Of these, 542 are scored as live assets, while the remaining 51 sit in pilot or announcement stages and have yet to receive a score. To measure how autonomously those 542 assets actually operate on chain, Pantera built the Tokenization Progress Index (TPI), a framework built around three dimensions of on-chain maturity.

The Lifecycle of an Asset

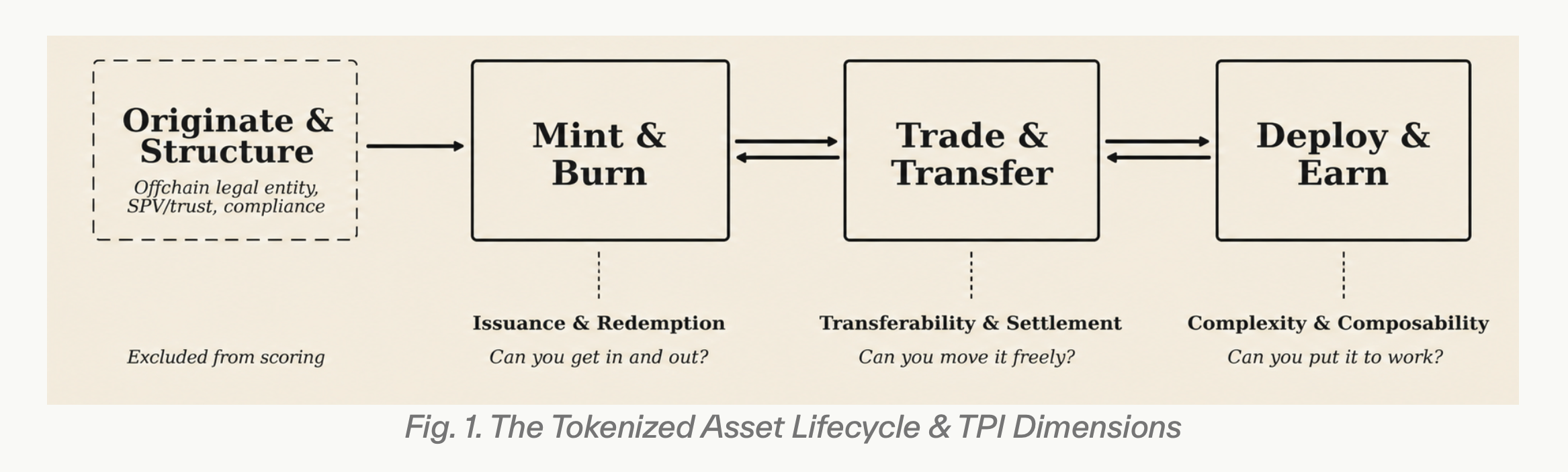

Pantera models the lifecycle of a tokenized asset as a linear flow of four stages. The first, Originate & Structure, covers the off-chain legal setup behind any tokenized asset, including entity formation, SPV and trust setup, and registration. This stage is excluded from scoring for now, not because it is unimportant, but because it remains too jurisdiction-specific and too unsettled to score consistently across the market today.

The remaining three stages, Mint & Burn (the token's birth and death), Trade & Transfer (how freely it moves and who holds the authoritative ledger), and Deploy & Earn (how much autonomous infrastructure backs it and how deeply it integrates into DeFi), map directly onto the three dimensions of the TPI.

Three Dimensions for the Tokenization Progress Index

Derived from these three stages, the TPI evaluates the autonomy and on-chain nativity of an asset across three aspects.

- Issuance & Redemption asks whether assets can be minted and exited through more autonomous and symmetrical on-chain mechanics.

- Transferability & Settlement asks whether the chain is the authoritative management and settlement layer, or just a mirrored record of an off-chain ledger.

- Complexity & Composability asks whether the asset can be put to work on chain through smart contract infrastructure, with composability for yield.

Each dimension is rated on a 1 to 5 scale, where higher scores indicate lower off-chain dependency and stronger on-chain autonomy. The dimensions are designed to be orthogonal, so a token can score high on transferability but low on composability, or vice versa. The composite TPI score is the arithmetic average of all three.

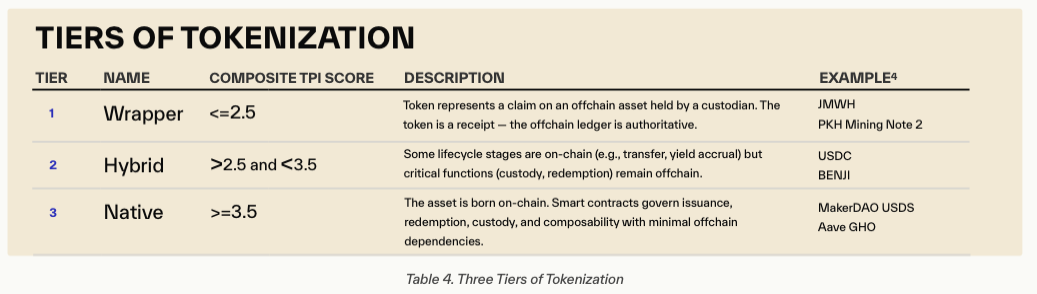

Three Tiers Based on Composite TPI Score (Wrapper, Hybrid, Native)

To make the TPI easier to interpret at the market level, Pantera groups assets into three tiers based on their composite score. The tiering is not a substitute for the underlying dimension scores. It serves as an interpretive layer that translates individual rubric scores into a more intuitive view of where each asset sits on the path from simple digital wrappers to genuinely native on-chain financial products.

At the bottom, with composite scores of 2.5 or below, sits the Wrapper tier. The token mainly functions as a digital receipt for an underlying asset that is still custodied, redeemed, and administered off chain. The chain may improve distribution or visibility, but it is not the authoritative operating layer. Justoken (JMWH) and PKH Mining Note 2 (PKH2), which is backed by bitcoin mining revenue, fall here.

One step up, between 2.5 and 3.5, sits the Hybrid tier. Some parts of the lifecycle have moved on chain, such as transfer or yield accrual, but critical functions like custody and redemption still depend on off-chain intermediaries, legal processes, or manual controls. USDC and BENJI are the canonical examples.

At the top, with composites of 3.5 or higher, sits the Native tier. The asset is designed to operate primarily on chain. Issuance, redemption, custody, and composability with other protocols are all governed by smart contracts, with minimal reliance on off-chain operational infrastructure. MakerDAO's USDS and Aave's GHO belong here.

That said, two assets can sit in the same tier for different reasons. One may be strong on transferability but weak on redemption, while another may be highly composable but still operationally constrained elsewhere. The tier labels summarize where an asset sits in the market, while the dimension scores explain how it got there.

Of the 593 tracked assets, 460 (77.6%) fall into the Wrapper bucket. Only 66 (11.1%) qualify as Hybrid and just 16 (2.7%) reach the Native tier, with the remaining 51 still in pilot or announcement stages. Tokenization has scaled quickly when it comes to distributing assets on chain, but it has barely begun the work of making those assets operate there autonomously. The market's center of gravity remains off chain, and only a small set of assets has crossed over.

By asset class, stablecoins lead the field. They post the highest Native share at 14% and the largest Hybrid share of any group. Actively-Managed Strategies and Private Credit follow next. Treasuries, Commodities, and Private Equity are only beginning to produce assets that reach the Hybrid range, with the vast majority still sitting in the Wrapper bucket.

RWA Infrastructure does not fit cleanly into the same comparison framework. Because it cannot be measured against market value in the same way, Pantera evaluates it as a separate category and assigns TPI scores within the limits of available information. The concentration of pre-launch pilots and announcement-stage projects in this category reads as a signal that the infrastructure and legal foundations the broader RWA market depends on are still being built.

Ultimately, the structural gap the report identifies is clear. The market has moved quickly to put assets on chain, but the work of creating financial products that are more useful because they are on chain remains in early stages outside of a handful of stablecoins and native assets.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.