Table of Contents

c4lvin(Four Pillars) recently published the 2026 Korea Web3 Market Report, which lays out where the Korean Web3 market stands today. This piece revisits the report through a few data-driven keywords.

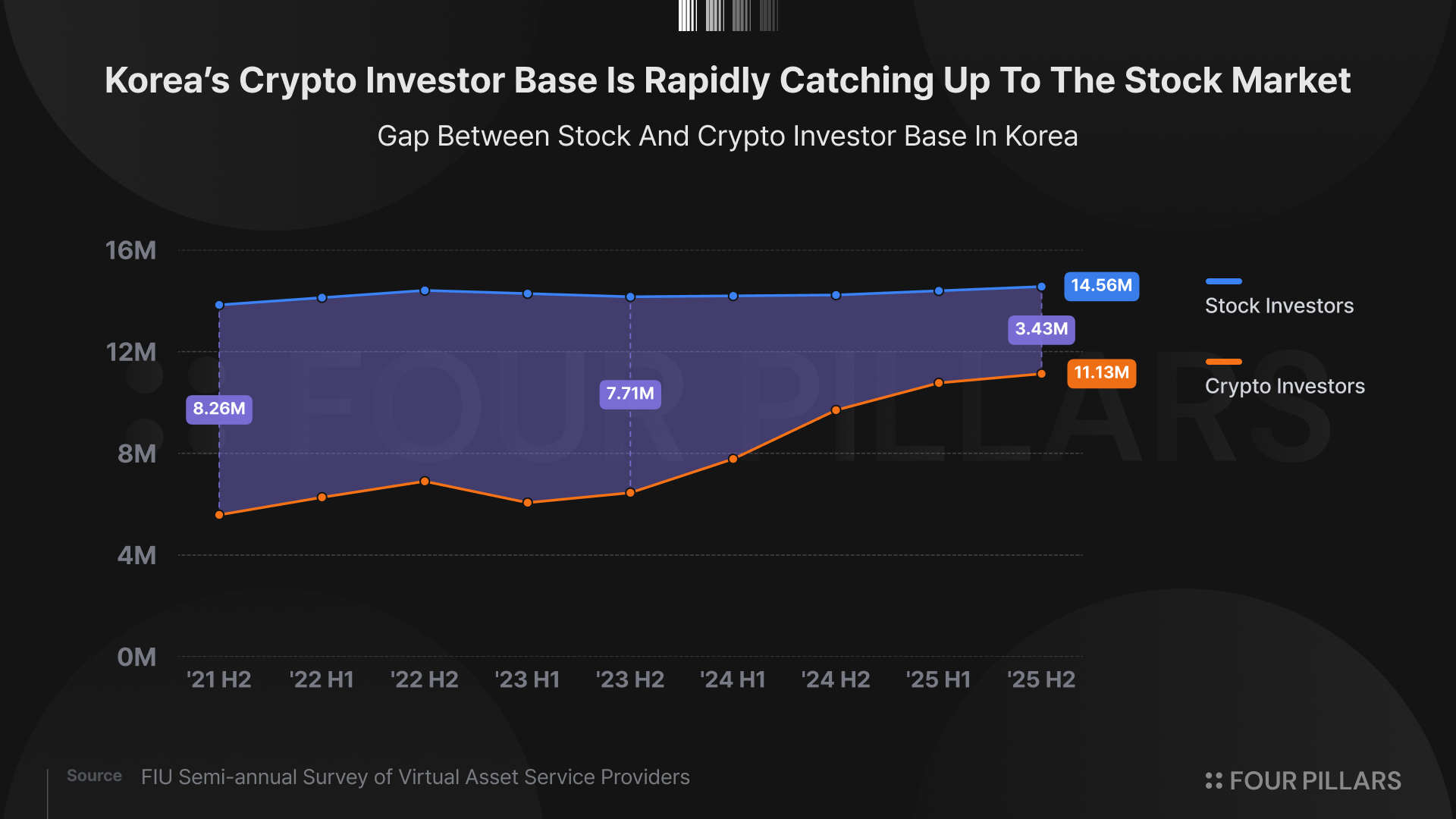

Korea has 11.13M crypto investors

On the investor-base front, Korea now stands on equal footing with any major global market. According to the Financial Intelligence Unit (FIU) and the Financial Supervisory Service's H2 2025 Virtual Asset Service Provider Survey, as of December 2025, the number of users on domestic exchanges reached 11.13M, or roughly 38% of Korea's economically active population. That figure is closing in on the country's stock investor count of about 14M. The catch is that accounts holding less than ₩1M make up 74.2% of the total (8.26M users), while accounts holding ₩10M or more sit at 10% (1.12M accounts), down 0.2%p from the end of June 2025. Accounts with ₩100M or more came in at 1.5% (170K accounts), narrowing by the same margin. Holders of ₩1B or more fell from 10,200 in H2 2024 to 6,900 by the end of 2025. New inflows are concentrated in small accounts while large holders are heading for the exit.

KRW market volatility hit 73%, 2.6x KOSPI.

Korea's trading behavior diverges from the global pattern as sharply as its scale does. The FIU's H2 2025 figures put Korean crypto price volatility at 73%, far above the same period's KOSPI Maximum Drawdown (MDD) of 28.3% and KOSDAQ MDD of 18.8%. The asset mix tells a different story too. As of December 2025, Bitcoin accounts for 58.4% of total market cap globally but only 34.9% in Korea. The starkest gap shows up in XRP, which ranks 5th globally at 3.7% but sits at 2nd in Korea with 26.5%, followed by Ethereum (13.1%), Solana (3.3%), and Dogecoin (2.9%). Turnover is high as well. With a market cap of ₩87.2T and average daily volume of ₩5.4T, the daily-volume-to-market-cap ratio comes out to about 6.2%. The market's assets rotate once every 16 trading days on average, pointing to a market dominated by short-term trading rather than long-term holding.

Of 11.13M users, only 588 are corporate accounts

One structural driver behind this volatility is what's missing from the market. As of the end of 2025, corporate accounts on exchanges numbered just 588, less than 0.01% of total users. Since 2017, corporations have not been able to open real-name accounts for crypto purchases, so any company looking to invest in crypto or run a related business had to set up an overseas entity as a workaround. That gap has shaped the liquidity supply structure of domestic exchanges. In global markets, professional market makers post two-sided quotes to provide depth and tighten spreads, but in Korea, with corporate purchase accounts blocked, no professional market maker can legally operate inside the regulated perimeter. Order books are thin, large orders push price further than they should, and this stands as one of the structural causes behind the 73% volatility cited earlier. That said, Phase 1 of the corporate participation roadmap took effect in June 2025, allowing non-profits and sell-side corporate accounts at exchanges. Corporate accounts jumped 167% from 220 in H1 to 588 in H2. Phase 2, which expands eligibility to listed companies and professional investors, is expected to accelerate that growth further.

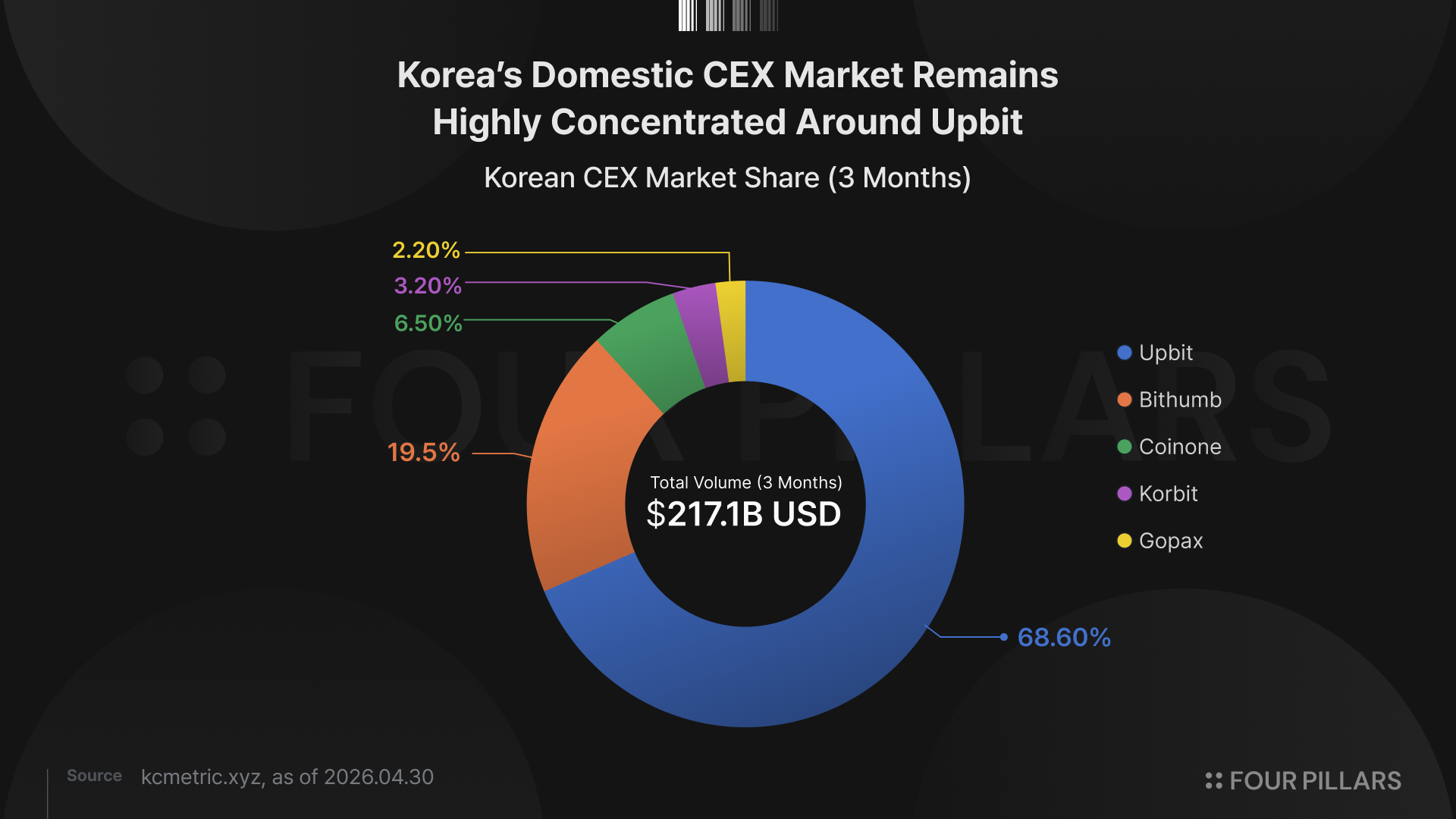

Upbit and Bithumb hold over 88% of the exchange market

This retail-driven market is concentrated on a handful of exchanges. As of April 30, 2026, of the roughly ₩320T ($217B) traded across the top 5 exchanges (Upbit, Bithumb, Coinone, Korbit, Gopax) over a 3-month window, Upbit accounted for 68.6% and Bithumb for 19.5%, putting the two together above 88%. Even this duopoly is showing cracks. Upbit's share, which sat close to 80% through 2024, declined steadily through 2025 and ended the year in the low 60s, while Bithumb, backed by aggressive marketing and the lowest fee policy in the market, briefly hit a record 45.7% in September 2025.

Combined operating profit across all exchanges in H2 2025 came in at ₩380.7B, down 38% from H1. Quarterly figures fell from ₩457.9B in Q1 to ₩81.1B in Q4. Average fee rates dropped from 0.17% to 0.15%, and capital adequacy ratios fell from 49.3% to 41.2%, signaling broader weakness in financial health. The fight for market share is eating into industry-wide profitability.

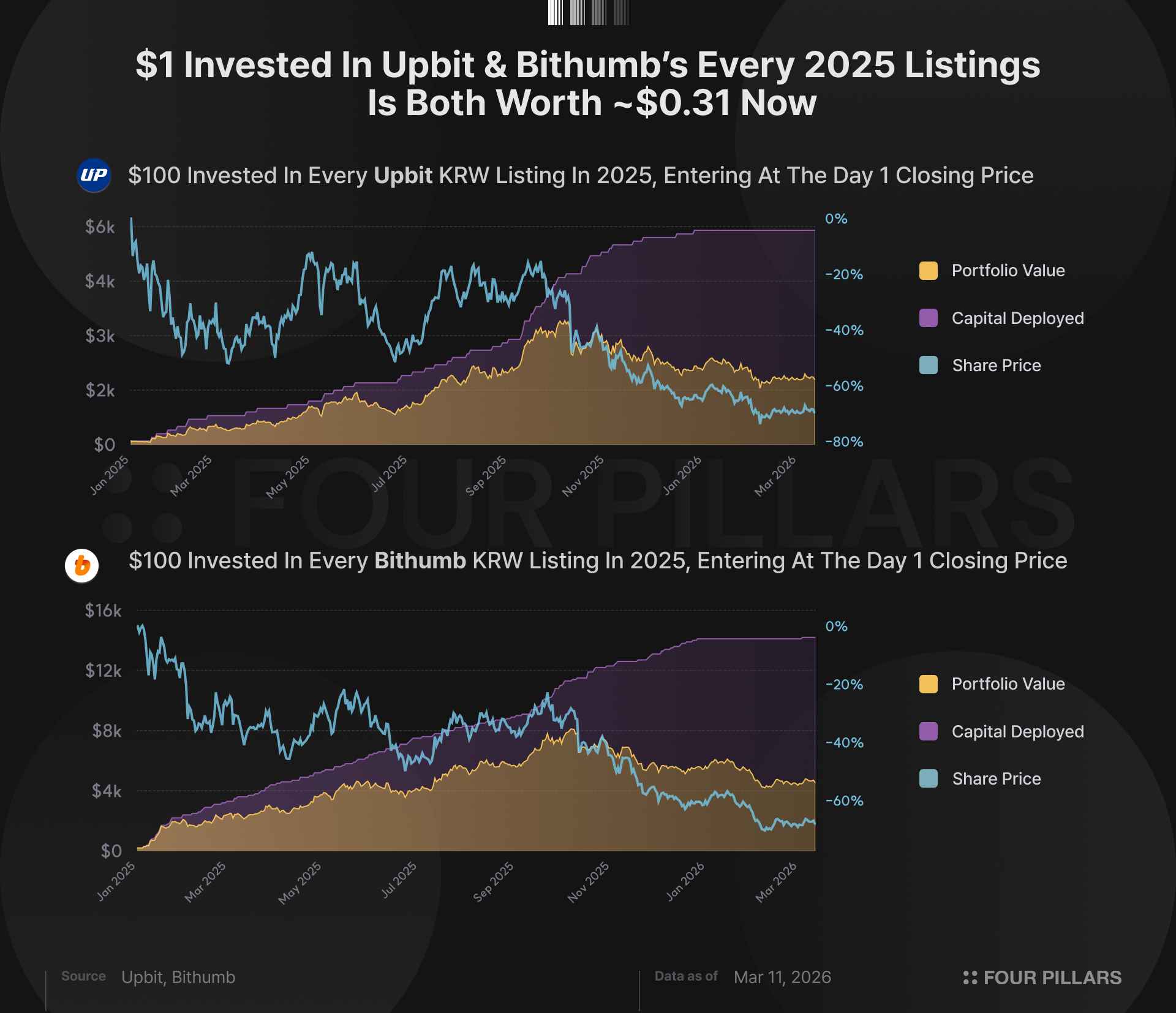

Of 59 tokens newly listed on Upbit in 2025, residual value after 1 year sits at 31%

What happens when trading concentrates on a few exchanges shows up clearly in the post-listing price performance of new tokens. According to c4lvin's 2025 Korean CEX KRW Listing Post-Mortem, if $100 had been invested at the first-day closing price of each of the 59 new KRW-pair listings on Upbit in 2025, by March 2026, the residual value would sit at about $0.31 per dollar invested. Roughly 69% has evaporated. Dual exchange listings, in other words, don't guarantee future price performance, and the losses don't come from a specific exchange or token quality. They're built into the demand concentration structure of the listing event itself. This cycle, known as the listing beam, repeats in four phases. Phase 1 sees volume spike 10 to 50 times right after the announcement. Phase 2 brings premium expansion from concentrated buy-side liquidity. Phase 3 compresses the premium as arbitrage capital flows in. Phase 4 ends with early holders selling and price returning to pre-listing levels. With ₩320T in 3-month trading volume sitting across the top 5 exchanges, access to KRW liquidity becomes a variable that directly shapes token price.

₩169T flowed overseas

The fact that KRW liquidity is locked into a narrow set of channels determines where capital ends up. Trading volume and market cap both shrank into H2 2025. Average daily trading volume came in at ₩5.4T, down 15% from H1, while market cap dropped 8% to ₩87.2T. Crypto transferred to overseas service providers and personal wallets (whitelisted) added up to ₩78.9T in H1 and ₩90T in H2, totaling roughly ₩169T for the year. The user base is widening, but capital is flowing out in parallel.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.