![Research, Burn, and Tokenization [FP Weekly 19]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fissues%2Fresearch-burn-and-tokenization-fp-weekly-19.png%3Ft%3D1777902810780&w=1920&q=75)

Table of Contents

- 1. Major News

- [Investment] Four Pillars Has Raised Series A Funding From Pantera Capital and Further Ventures

- [Crypto] Pump.fun Has Burned All Bought Back PUMP Tokens

- [Institution] Securitize and Computershare announced an agreement to support U.S. listed clients in issuing equity securities in tokenized form

- Others

- 2. Four Pillars Weekly

- : : Blockchain Guidebook for Korean Institutions 2026 (Link)

- : : Hong Kong's Stablecoin Vision: Asia's Regulated Digital Asset Hub (Link)

- : : Where Is Korea’s Crypto Tax Policy Headed? (Link)

- : : Securitize Just Opened the Floodgates (Link)

- : : Ethereum Infrasturcture Operations: A Practical Guide For Institutions And Individuals (Link)

- Comments

- 3. Macro & Onchain Metrics

Researcher

1. Major News

[Investment] Four Pillars Has Raised Series A Funding From Pantera Capital and Further Ventures

What Happened?

Four Pillars has raised a Series A round from Pantera Capital and Further Ventures, marking a key step in the company’s expansion beyond blockchain research into institutional-focused research and infrastructure services.

Over the past three years, Four Pillars has built credibility as an Asia-based firm with global reach, partnering with more than 100 protocols and companies and publishing over 600 research pieces. The company has focused on addressing regional information gaps and fragmented networks by publishing its research in both Korean and English.

Pantera Capital, one of the investors in the round, is a blockchain and digital asset investment firm known for launching the first U.S. cryptocurrency fund in 2013. Further Ventures is an investment platform that connects global capital markets with financial infrastructure, with activities spanning digital assets, structured products, and venture investing. Notably, Abu Dhabi’s sovereign wealth fund is known to be an anchor investor in Further Ventures, underscoring the strategic interest of global institutional capital in the round.

With the new funding, Four Pillars plans to expand its business across three core areas. Its research arm, FP Research, will be reorganized into five specialized divisions: Crypto, Investment, Institution, Asia, and Tech. FP Validated will provide institutional-grade validator infrastructure and staking services, while the newly launched FP Institution will focus on bridging traditional finance and Web3 through seminars and advisory services.

Four Pillars sees Asia’s blockchain market entering a new phase as regulatory frameworks take shape and the industry shifts from speculation toward real economic infrastructure. Backed by its Series A funding, the company aims to position itself as a trusted partner connecting Asia with global markets, and traditional finance with Web3.

[Crypto] Pump.fun Has Burned All Bought Back PUMP Tokens

What Happened?

On April 28, 2026, pump.fun announced on X that it had burned all PUMP tokens it had previously bought back. According to the announcement, the burn amounted to roughly $370 million, or about 36% of the circulating supply. The project described the move as an effort to “rebuild trust” with the community. At the same time, pump.fun ended its previous model of using 100% of revenue for buybacks and said that, for the next year, it would allocate 50% of net revenue to programmatic buybacks and immediate burns. The funds will come from net revenue generated by its core products, including Bonding Curve, PumpSwap, and Terminal, while the remaining 50% will be allocated to operations, hiring, marketing, M&A, and new product development.

The market reaction was strongly positive in the short term. Following the announcement, PUMP rose by roughly 7–10%, with some reports showing the token moving from around $0.0017 to $0.0020. Still, PUMP remains more than 80% below its all-time high of around $0.012, recorded in July 2025. As such, the rebound appears less like a full trend reversal and more like an immediate repricing of the large-scale supply removal and the project’s commitment to future burns.

Community reaction was mixed. Supporters pointed to the removal of roughly 36% of circulating supply and the one-year commitment to using 50% of net revenue for buybacks and burns, arguing that the move reduces overhang and makes the use of buyback funds more predictable. Some traders, however, criticized the decision, noting that previously accumulated buyback tokens could have been used for future airdrops or community rewards. In that view, burning the entire amount effectively eliminated a potential avenue for user compensation. Ultimately, while the announcement provided a short-term price catalyst for PUMP, its longer-term impact will depend on how well pump.fun manages three key challenges: revenue sustainability, supply dynamics after team unlocks, and rebuilding community trust.

Researcher’s Comment

pump.fun’s PUMP burn should be understood less as a simple supply reduction event and more as a tokenomics reset aimed at resolving market uncertainty around how accumulated buyback tokens would be handled. pump.fun had been holding roughly $369 million worth of buyback tokens, or about 126.8 billion PUMP, equivalent to around 35.8% of circulating supply. With the team’s cliff unlock approaching, any decision to sell those tokens, redistribute them through airdrops, staking, or LP incentives, or simply continue holding them could have acted as an overhang on the market. By contrast, burning the tokens reduces total supply and increases the economic ownership of each remaining token holder, making it arguably the most rational path for both the team and investors.

[Institution] Securitize and Computershare announced an agreement to support U.S. listed clients in issuing equity securities in tokenized form

What Happened?

Securitize and Computershare announced a partnership to enable U.S.-listed companies to issue their shares in tokenized form. The core of the collaboration is to provide a pathway for U.S. issuers to offer tokenized shares called “Issuer-Sponsored Tokens,” or ISTs, alongside their existing common stock. Under this structure, Securitize will provide the real-world asset tokenization infrastructure, while Computershare will handle shareholder records and transfer agent responsibilities for issuers.

What makes this partnership notable is that these tokenized shares are not derivatives layered on top of existing stocks or wrapped tokens. Instead, they represent an issuer-supported method of holding shares. According to Securitize, ISTs allow investors to hold shares onchain without changing the underlying equity itself. This means investors can hold tokenized securities in a digital wallet while preserving existing shareholder rights and corporate action flows, including direct communication with the issuer, dividends, and voting rights.

Computershare’s involvement adds significant weight to the announcement. As the world’s largest transfer agent, Computershare serves more than 25,000 corporate clients and is known to work with major companies such as Apple and Microsoft. According to the Wall Street Journal, Computershare supports 58% of S&P 500 companies. Through this partnership, it will act as transfer agent for both traditional and tokenized shares, including the handling of dividend payments and voting processes.

Researcher’s Comment

The partnership between Securitize and Computershare could mark an important turning point for the tokenized equities market. Until now, most onchain stock tokens, such as AAPLx and TSLAx, have been closer to “wrapper” structures, where the underlying shares are held in custody and only the economic exposure is issued as a token. By contrast, the Issuer-Sponsored Tokens, or ISTs, being pursued by Securitize and Computershare directly tokenize actual shares within the issuer or transfer agent framework. Put simply, these are not merely “tokens that track stock prices,” but rather “shares expressed in token form” and connected to existing shareholder rights.

Computershare’s role is especially important. As the world’s largest transfer agent serving more than 25,000 companies, it can support U.S.-listed companies in issuing ISTs alongside their existing shares. According to the official announcement, ISTs may be included as part of an issuer’s outstanding share capital alongside traditional shares and DRS holdings, while Computershare will also manage shareholder records, dividends, voting rights, stock splits, and other corporate actions for ISTs. This shows that tokenized equities do not need to remain experimental products outside the regulatory perimeter; they can operate within existing capital market infrastructure and regulatory frameworks.

The significance of this partnership is less about the near-term expectation that Apple or Tesla shares will immediately move onchain, and more about the creation of a standardized bridge between traditional finance and onchain finance. Securitize provides the technology and tokenization infrastructure, while Computershare provides issuer-centric shareholder management and corporate action infrastructure. Considering that Securitize has also recently been working with NYSE on a tokenized securities platform, the market appears to be moving beyond the simple RWA narrative and toward a phase where traditional financial assets such as listed stocks, ETFs, and funds can be brought onchain. That said, the pace of adoption will depend on issuer demand, liquidity, regulatory interpretation, and interoperability with existing market infrastructure. Only when these issues are resolved can tokenized equities move beyond being a “theme” and become a new method of holding and settling assets in capital markets.

Others

Crypto

- Aave is now live on Solana

- Tether Launches MDK, an Open Infrastructure Layer for Bitcoin Mining

- Circle Ventures is purchasing AAVE tokens

- LayerZero Labs is pledging more than 10,000 ETH to Aave-led DeFi United efforts

- OKX Introduces Agent Payments Protocol

- $MEGA is now live

- Meta Launches Stablecoin Payouts for Creators Using Stripe

Institution

- Gemini introduced agentic trading

- Visa Accelerates Stablecoin Momentum: Adding Five Blockchains for Settlement

- trade.xyz introduces Pre-IPO perpetuals

- Nanopayments powered by Circle Gateway Is Now Live on Mainnet

- MoonPay launches stablecoin debit card for AI agents on Mastercard network

Tech

Investment

- Liquid Raises $18M Series Seed Funded by Neo and Left Lane Capital to Build the Ultimate Financial Superapp

- Blockworks Announces Series A Extension at $192M Valuation

- Altitude has raised $18M

- Crypto onramping solution Fun raises $72 million Series A co-led by Multicoin Capital and SignalFire

Asia

- SBI Holdings in talks to acquire stake in crypto exchange Bitbank, eyes subsidiary status

- South Korea's Shinhan Card to test real-world stablecoin payments on Solana

- Crypto VC Hashed gains financial services license in Abu Dhabi

2. Four Pillars Weekly

: : Blockchain Guidebook for Korean Institutions 2026 (Link)

This report is designed for Korean enterprises and financial institutions preparing for the next phase of the onchain economy.

In this guidebook, we explore onchain opportunities across four major themes:

- Stablecoin

- Tokenization

- Institutional finance

- Future opportunities

For each theme, we examine the fundamentals, global trends, and what they could mean for the Korean market.

: : Hong Kong's Stablecoin Vision: Asia's Regulated Digital Asset Hub (Link)

- This report maps the ecosystem across four parts: Part 1 covers the regulatory architecture: Cap. 656's licensing requirements, the narrow-issuance/wide-distribution model in which HKMA monopolizes stablecoin issuance while five categories of Permitted Offerors share distribution, and the broader digital asset framework spanning the VATP regime, the SFC's "see-through" approach to tokenized securities, and the Digital Bond Grant Scheme.

- Part 2 covers the key initiatives shaping Hong Kong's digital money landscape: the note-issuing banks (HSBC, the Standard Chartered-led Anchorpoint, and BOCHK), Chinese tech giants (JD.com, Ant Group) caught in Beijing's crosshairs, former HKMA chief Norman Chan's RD Technologies, OSL Group's pivot from exchange to issuer, and the parallel tokenized deposit and e-HKD tracks already running while licensed stablecoins wait for circulating tokens.

- Part 3 traces the China dimension: the offshore RMB stablecoin arc from hope to crackdown, Yinfa No. 42's extraterritorial reach, and what Beijing's interventions leave of Hong Kong's currency-agnostic framework.

- Part 4 closes with the outlook: near-term execution risk for the first licensees, the structural competition between stablecoins, tokenized deposits, and e-HKD, plus Beijing as the largest swing factor.

: : Where Is Korea’s Crypto Tax Policy Headed? (Link)

- On April 29, 2026, the National Tax Service (NTS) announced that it has begun building infrastructure in earnest, on the premise that crypto taxation will take effect on January 1, 2027. Data collection from exchanges, the construction of an integrated analysis system, and the development of an information exchange framework based on CARF are all proceeding in parallel, with the first filings expected in May 2028 as part of the comprehensive income tax filing.

- Current income tax law, however, has barely established taxation standards for areas beyond simple trading and crypto-to-crypto exchanges, namely DeFi staking and lending, airdrops, hard forks, and NFTs. The NTS itself has stated that it is in the process of gathering overseas legislative cases and expert opinions.

- Since Notice 2014-21 in 2014, the United States has classified cryptocurrency as property and has built up taxation principles for nearly every area, including simple trading and exchanges, DeFi, staking, and airdrops, on the basis of self-reporting. Form 1099-DA, which took effect in 2025, applies only to centralized exchanges, while DeFi remains the taxpayer's own responsibility.

- Given the constraints of underdeveloped infrastructure and a short preparation window, Korea is likely to adopt the broad framework of the U.S. model. The four pillars are asset classification, the self-reporting principle, the phased introduction of exchange reporting obligations, and the provisional neglect of the DeFi gray zone.

- This convergence brings side effects such as fairness issues, regulatory arbitrage between domestic exchanges and overseas/DeFi venues, and the shifting of documentation burdens onto taxpayers. The start of taxation is only a starting point, and supplementary legislation aimed at securing substantive fairness is unlikely to be enacted within this year.

: : Securitize Just Opened the Floodgates (Link)

- This partnership could mark a major turning point for tokenized equities. It opens a path for more than 25,000 companies serviced by Computershare to issue tokenized shares, significantly expanding the potential scale of the market.

- The key distinction is that these are “native” tokenized shares, not wrapper tokens. ISTs directly tokenize actual shares, allowing investors to hold tokenized equities with the same rights as traditional shareholders.

- The collaboration could become a bridge between traditional equity markets and onchain finance. Computershare provides shareholder recordkeeping and corporate action infrastructure, while Securitize provides the tokenization technology.

: : Ethereum Infrasturcture Operations: A Practical Guide For Institutions And Individuals (Link)

- Ethereum validator infrastructure is different from other blockchain operations in ways that matter. Each layer of the modular, multi-layered stack requires its own choices, and as staked assets grow, the number of validators and infrastructure requirements scale with it. Whether you are a solo staker or an institution, understanding this structural characteristic is the starting point for all infrastructure design.

- The optimal architecture changes entirely depending on operational scale. After PeerDAS, node types have been explicitly differentiated, and the increase in MaxEB has raised both efficiency and risk at the same time. A single machine is sufficient for solo stakers, but institutional operators must consider multi-client setups, DVT, multi-layered slashing protection, disaster recovery, and much more. Finding the right combination for your specific scale and context is the hard part.

- Client diversity and slashing prevention are the most important strategies for operators of every size. Running a mix of clients improves fault tolerance and reduces risk. Slashing prevention mechanisms block irrecoverable asset loss at the system level. Even at the cost of some performance, these two priorities should come first.

- Ethereum staking yield depends on the proficiency of infrastructure operations. There is no universal answer, because every operator's context differs: scale, geography, risk tolerance, technical capability, regulatory environment, cost structure, and more. Finding the right combination for your own context is itself a core competency. This requires both traditional infrastructure operations skills and a deep understanding of Ethereum's protocol-specific characteristics, along with systematic monitoring and an environment that can structurally prevent slashing.

Comments

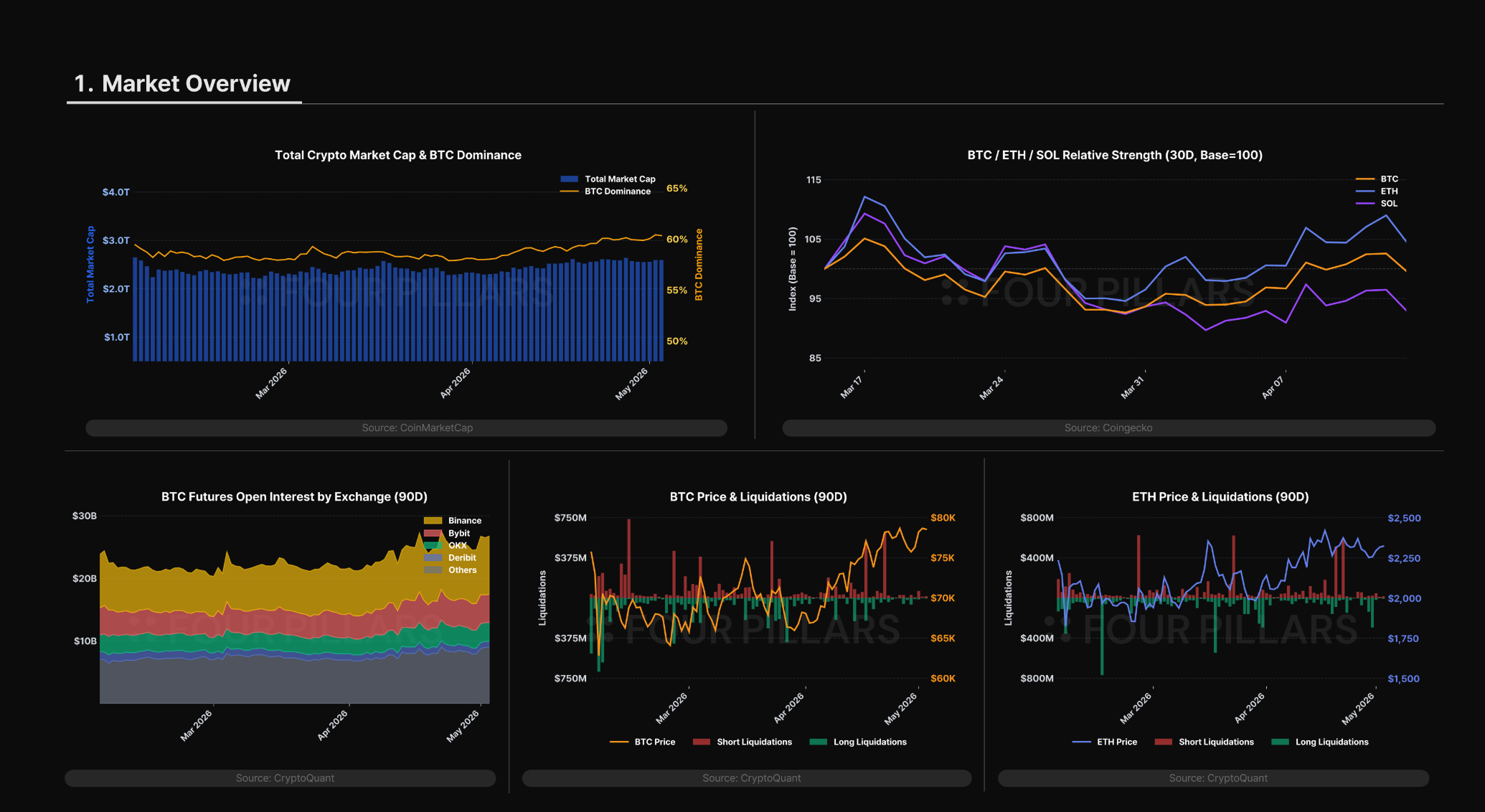

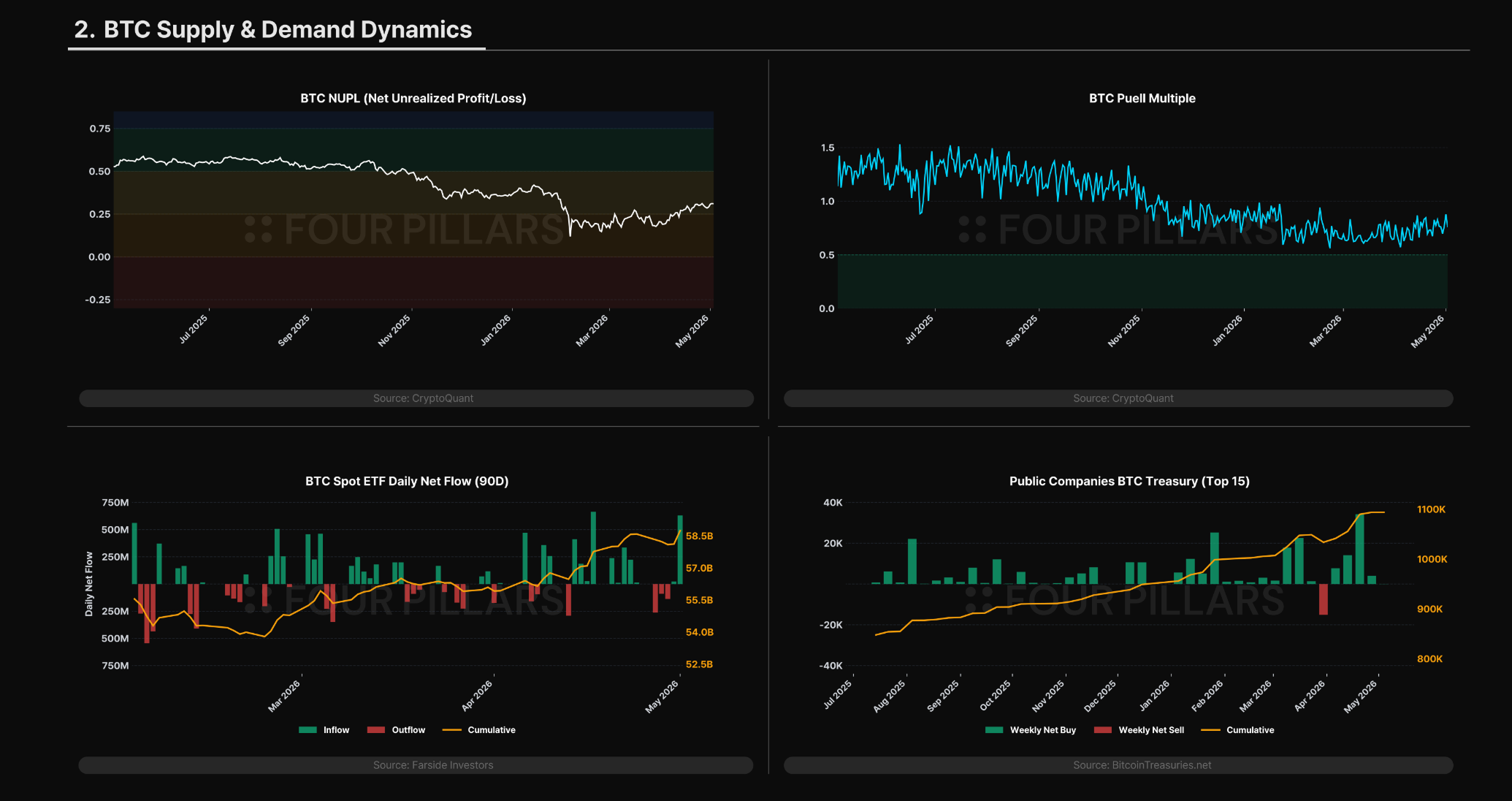

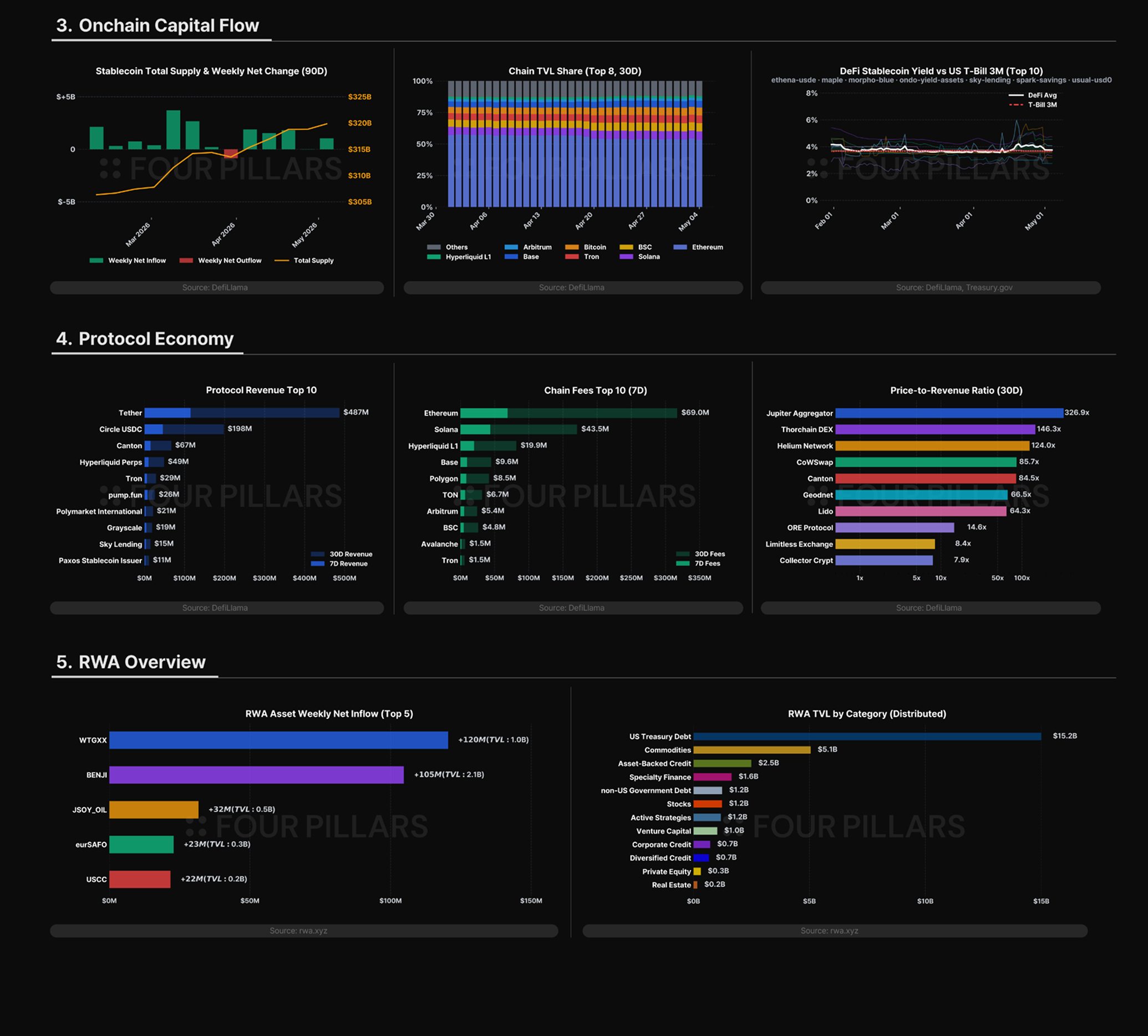

3. Macro & Onchain Metrics

Some of the charts below are powered by CryptoQuant. For those interested in exploring the underlying data in greater detail, CryptoQuant provides access to a comprehensive suite of onchain and market analytics used by institutional participants.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![Coldcard Got Burned, Coinbase Froze [FP Weekly 32]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fhv83s5msebytml.png&w=1920&q=75)