Table of Contents

Researcher

Related Projects

Key Takeaways

- This partnership could mark a major turning point for tokenized equities. It opens a path for more than 25,000 companies serviced by Computershare to issue tokenized shares, significantly expanding the potential scale of the market.

- The key distinction is that these are “native” tokenized shares, not wrapper tokens. ISTs directly tokenize actual shares, allowing investors to hold tokenized equities with the same rights as traditional shareholders.

- The collaboration could become a bridge between traditional equity markets and onchain finance. Computershare provides shareholder recordkeeping and corporate action infrastructure, while Securitize provides the tokenization technology.

Securitize has opened the floodgates. A path has opened for the shares of more than 25,000 companies with a total scale of over $30T to be tokenized. “Natively”.

1. Partnership Between Securitize and Computershare

Source: Securitize

1.1 Tokenized Stocks, What Is So New About That?

The RWA market hasn't held my attention much recently, but Securitize's new partnership with Computershare changes that.

Computershare is the world's largest transfer agent, handling shareholder records for over 25,000 companies, including more than half of the S&P 500. The deal lets U.S. listed companies on Computershare's books issue their shares in tokenized form alongside their existing form.

(I'll cover what a transfer agent does in section 2.)

The obvious question: Apple and Tesla stock tokens already exist onchain. So what? The answer is that those existing tokens are wrappers, not native shares.

1.2 “Truly Native” Tokenized Stocks

There are many kinds of onchain stock tokens, such as AAPLx and TSLAx issued by Backed Finance, AAPLon and TSLAon issued by Ondo Global Markets, and Apple and Tesla tokens provided by Robinhood Stock Tokens.

However, all of these are wrapper tokens. They are not native stock tokens.

To understand this, we need to look at the methods used to tokenize stocks.

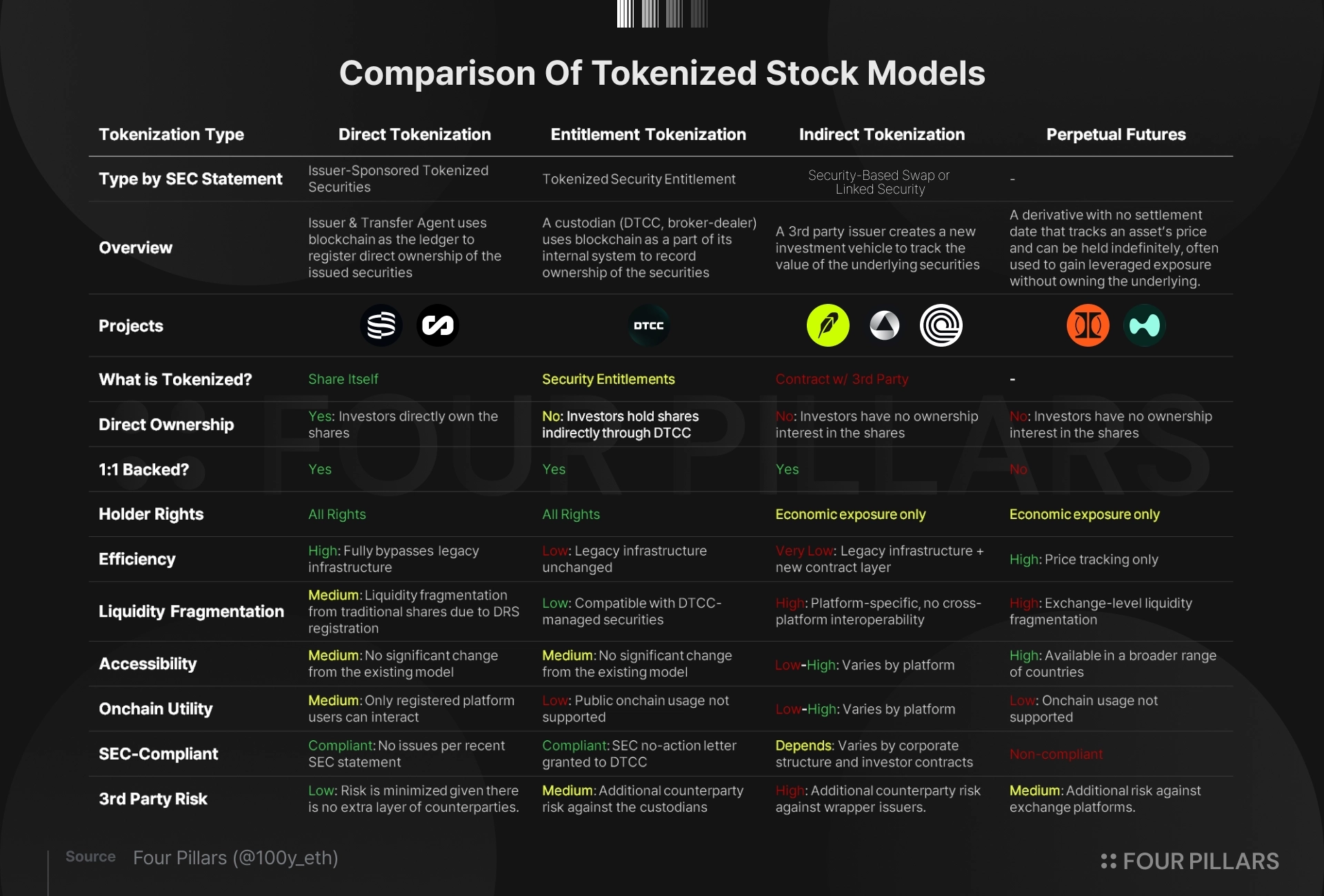

There are currently three main ways stocks are tokenized. (Strictly speaking, the final perpetual futures method does not tokenize stocks, so I will omit an explanation of it.)

- Direct Tokenization: A structure in which the issuer or transfer agency directly tokenizes the security, integrating blockchain into the shareholder register that was previously managed through an internal database.

- Entitlement Tokenization: A method that integrates blockchain into a register system managed by a third party such as the DTCC.

- Indirect Tokenization: A method in which a third party provides investors with synthetic economic exposure to a reference security.

Wrapper tokens fall under the indirect tokenization method.

Wrappers fall under indirect tokenization. The mechanism: when an investor wants to buy a tokenized stock, the platform buys the underlying share on the open market and parks it with a custodian, then issues the investor a token representing economic exposure to that custodied share. The share itself isn't tokenized. Neither are shareholder rights. Only the economic claim.

Securitize uses direct tokenization, which works because Securitize is an SEC-registered transfer agent. It can manage the company's official shareholder register and issue shares natively onchain. The token is the share. Investors get the same legal rights they would holding the stock the traditional way.

So what's a transfer agent, and how does this work?

2. Transfer agents and Computershare

2.1 Transfer Agents

A transfer agent maintains a company's official shareholder register and records changes in ownership. When you buy a stock, the transfer agent is the legal recordkeeper sitting between you and the company.

The role is defined under Section 17A of the Securities Exchange Act of 1934 and supervised by the SEC. Transfer agents must register with the SEC and meet annual reporting and compliance requirements to keep operating.

The job covers four areas:

- Ownership records: the legal record of who owns how many shares.

- Issuance and cancellation: reflecting new shares issued or shares canceled, and keeping the cap table current through stock splits and dividends.

- Transaction processing: recording ownership changes when shares trade.

- Corporate actions: dividend payments, voting, shareholder notices, and report distribution.

The main players are Equiniti Trust Company, Broadridge, Continental Stock Transfer & Trust, and Computershare. Computershare is the largest.

2.2 Computershare

Computershare started in Melbourne in 1978, not as the financial firm it is now but as a computer services company helping clients automate manual work. Its transfer agent business grew out of providing computerized shareholder register services to Australian listed companies.

The 1990s were Computershare's expansion decade. London office in 1995. Acquired KPMG and EY's transfer agent businesses in New Zealand in 1997. Entered South Africa in 1998 and Hong Kong in 1999, both through equity acquisitions.

The 2000s were when Computershare cracked the U.S. market. In 2003, it acquired Georgeson Shareholder Communications in New York, which both opened the U.S. door and pushed Computershare beyond pure recordkeeping into shareholder action and proxy voting. In 2004, it bought EquiServe, then the largest U.S. transfer agent, and scaled up sharply. Later acquisitions of BNY Mellon Shareowner Services and Morgan Stanley Global Stock Plan Services added more clients.

Today Computershare serves over 25,000 companies globally and handles roughly 58% of the S&P 500. By S&P 500 market cap alone, that's a book of business running north of $60T.

Now Computershare is taking the next step with Securitize.

3. Through IST, Computershare Is Opening The New Era With Securitize

Through this partnership, U.S. listed companies that use Computershare as their transfer agent will be able to issue tokenized shares called ISTs, Issuer-Sponsored Tokens.

Why that name? Nothing's been officially disclosed, but the SEC's recent statement on tokenized securities is the likely source. The statement classifies the existing tokenized securities in the market and identifies one category as Issuer-Sponsored Tokenized Securities. That category lines up with direct tokenization: the issuer either tokenizes shares itself or works through a transfer agent. The SEC's position is that this approach raises no issues under existing securities law.

An IST is a tokenized form of a stockholding inside a company's existing share count. Investors who want to hold their shares in a digital wallet can do so; investors who don't can keep things as they are. Because the IST is direct equity ownership in token form, it's the same instrument as the existing share, just expressed differently.

Computershare acts as the transfer agent for ISTs. It records IST ownership alongside conventional share ownership and processes corporate actions: dividends, voting, splits. Everything stays inside the existing regulatory perimeter.

Securitize handles the technology side. Building on its work tokenizing funds like BUIDL and other securities, it provides the tokenization infrastructure.

Securitize has been busy elsewhere too, including a 24/7 tokenized securities platform with NYSE. Computershare deal is the one that puts native shares of companies like Apple and Tesla onchain for the first time. That's what connects the $140T global stock market to onchain.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![Onchain Vaults Head to the Regulator's Desk [FP Weekly 31]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fewmxa9ms2zo6jb.png&w=1920&q=75)

![Journey Toward Tokenized Stocks [FP Weekly 30]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fvlq144mrur6b4t.png&w=1920&q=75)