Table of Contents

- Introduction

- Part 1: Regulatory Architecture

- 1.1 The Regulatory Landscape

- 1.2 The Stablecoins Ordinance

- 1.3 Broader Digital Asset Framework

- Part 2: Key Initiatives

- 2.1 Note-Issuing Banks: The Structural Advantage

- 2.2 Chinese Tech Giants: JD.com & Ant Group

- 2.3 RD Technologies: The Startup Pioneer

- 2.4 OSL Group: From Exchange to Issuer

- 2.5 Tokenized Deposits & e-HKD: The Parallel Tracks

- Part 3: The China Dimension

- Part 4: Outlook

Researcher

Stablecoins, Tokenization, and the Race for Digital Finance Leadership

Introduction

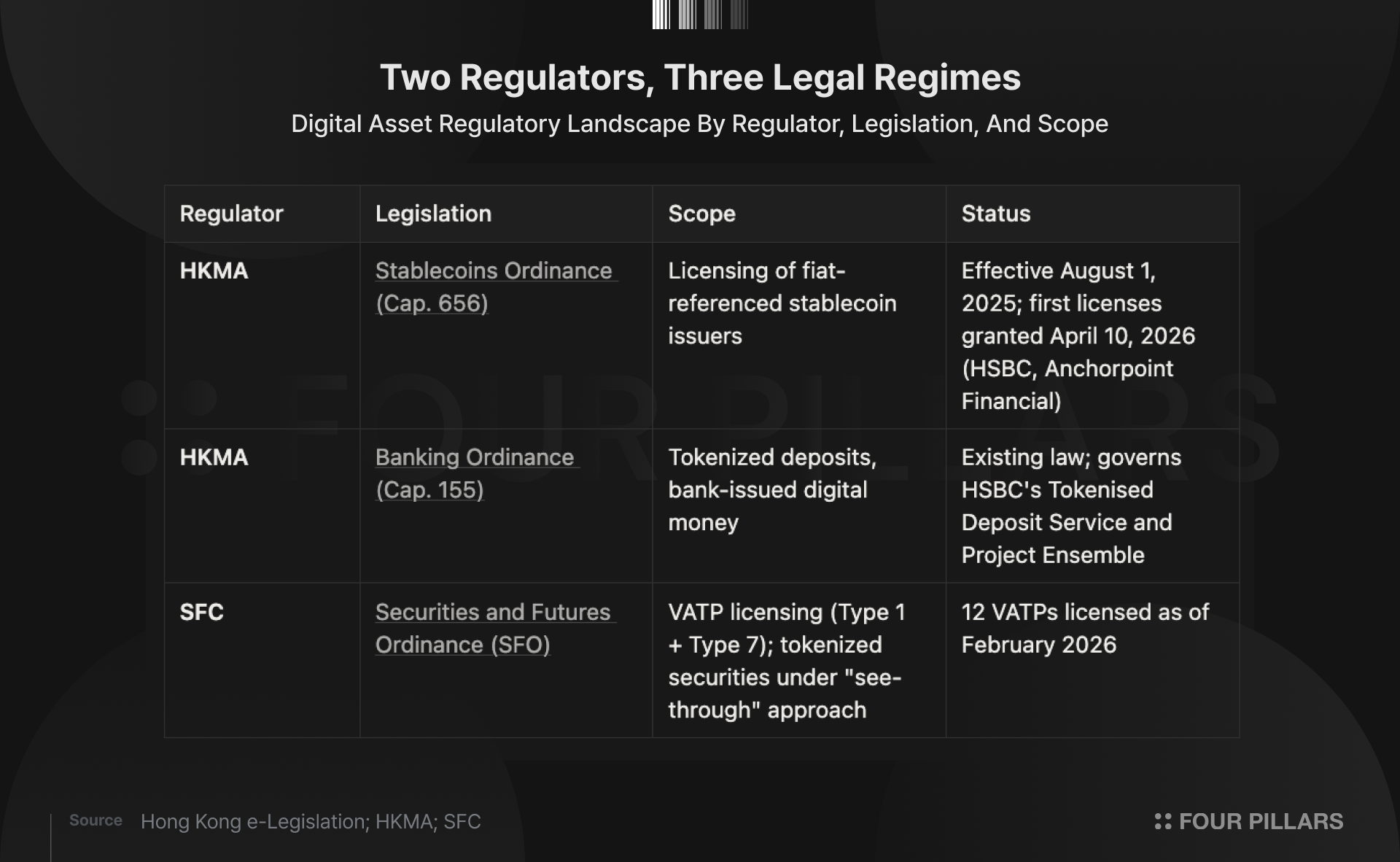

On April 10, 2026, shortly after the market's end-of-March expectation, the HKMA granted Hong Kong's first two stablecoin licenses to HSBC and to the Standard Chartered–led Anchorpoint Financial, ending an eight-month wait under one of the world's most detailed stablecoin laws.

Hong Kong's digital money architecture is the most comprehensive in Asia, and the stablecoin licenses are only its most recent piece. The Stablecoins Ordinance (Cap. 656) took effect in August 2025; by November, the HKMA had launched EnsembleTX, a live tokenized deposit settlement platform running with seven banks, and Hong Kong had issued the world's largest digital bond, HK$10 billion in tokenized green bonds settling in both e-HKD and e-CNY, the first integration of two sovereign digital currencies in capital market infrastructure. Throughout the same period, Beijing intervened twice, first ordering JD.com and Ant Group to pause their Hong Kong pilots in September 2025, then formally banning unapproved RMB-pegged stablecoins in a February 2026 directive co-signed by eight regulatory bodies, narrowing Hong Kong's legally currency-agnostic framework to HKD and USD in practice.

This report maps the ecosystem across four parts:

- Part 1 covers the regulatory architecture: Cap. 656's licensing requirements, the narrow-issuance/wide-distribution model in which HKMA monopolizes stablecoin issuance while five categories of Permitted Offerors share distribution, and the broader digital asset framework spanning the VATP regime, the SFC's "see-through" approach to tokenized securities, and the Digital Bond Grant Scheme.

- Part 2 covers the key initiatives shaping Hong Kong's digital money landscape: the note-issuing banks (HSBC, the Standard Chartered-led Anchorpoint, and BOCHK), Chinese tech giants (JD.com, Ant Group) caught in Beijing's crosshairs, former HKMA chief Norman Chan's RD Technologies, OSL Group's pivot from exchange to issuer, and the parallel tokenized deposit and e-HKD tracks already running while licensed stablecoins wait for circulating tokens.

- Part 3 traces the China dimension: the offshore RMB stablecoin arc from hope to crackdown, Yinfa No. 42's extraterritorial reach, and what Beijing's interventions leave of Hong Kong's currency-agnostic framework.

- Part 4 closes with the outlook: near-term execution risk for the first licensees, the structural competition between stablecoins, tokenized deposits, and e-HKD, plus Beijing as the largest swing factor.

The thesis emerging from these initiatives: Hong Kong is building a digital money regime that is currency-agnostic in law and institutionally anchored in practice, not just for stablecoins, but for the full spectrum of tokenized money. The question is whether this multi-track approach converges into a coherent ecosystem, or fragments into parallel experiments where licensed stablecoins arrive too late to matter.

Part 1: Regulatory Architecture

1.1 The Regulatory Landscape

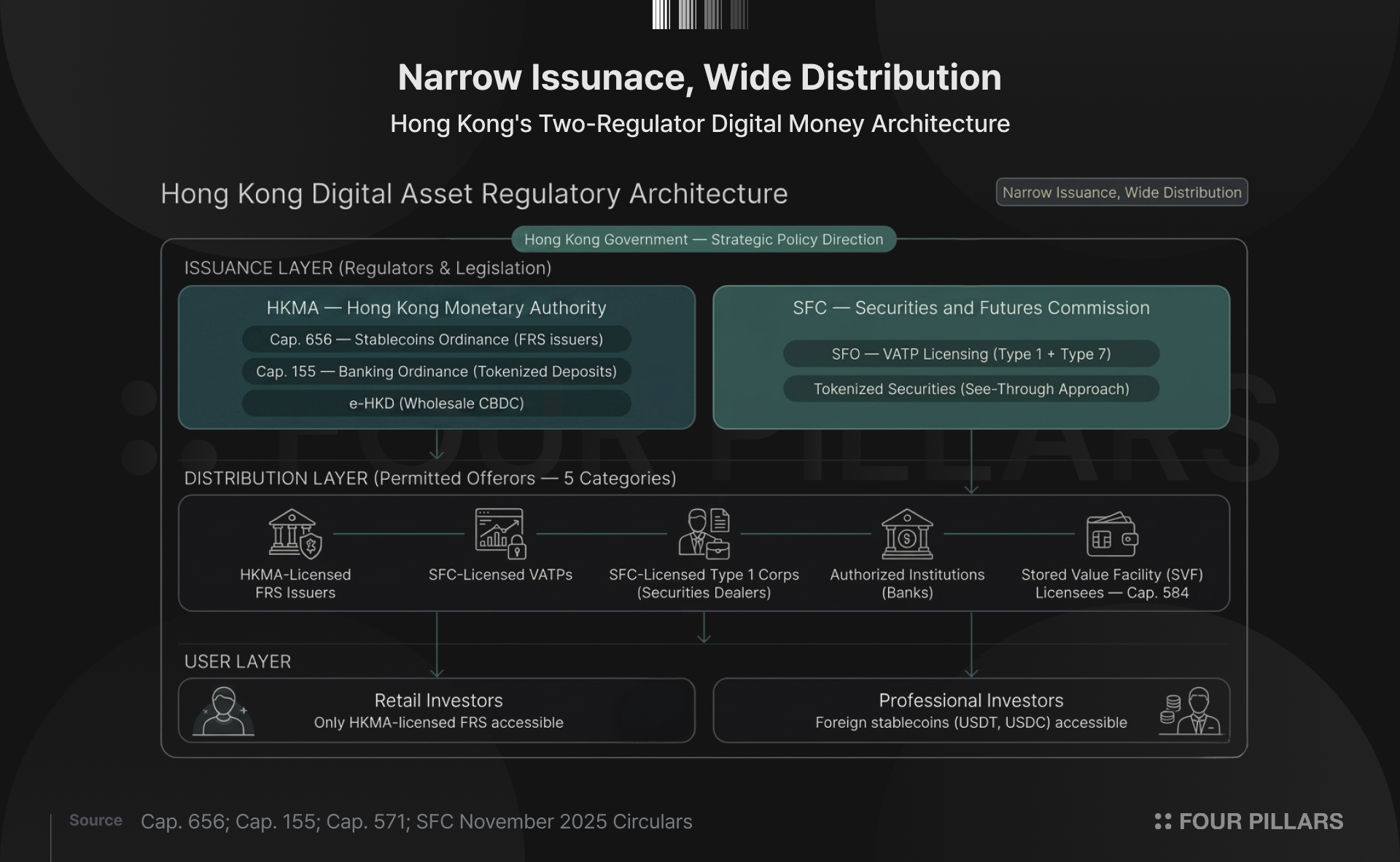

Hong Kong's digital asset regulation is not governed by a single law or a single regulator. It is a multi-layered system where two statutory regulators oversee different activities under multiple pieces of legislation:

- The Hong Kong Monetary Authority (HKMA) is the city's de facto central bank and banking regulator, responsible for stablecoin issuer licensing, banking supervision under the Banking Ordinance, and monetary policy.

- The Securities and Futures Commission (SFC) is the statutory regulator for securities and futures markets, responsible for licensing virtual asset trading platforms (VATPs), tokenized securities, and investment products.

Strategic policy direction sits above both regulators and is set by the Hong Kong government through policy statements and roadmaps. Before examining each component in detail, it is useful to map the full landscape:

The key structural feature is narrow issuance, wide distribution. Only HKMA-licensed FRS issuers can create stablecoins, but distribution is opened up across multiple categories of "Permitted Offerors" spanning banks, exchanges, securities dealers, and stored-value wallet operators (detailed in Section 1.2). The two main regulators coordinate through joint circulars, for instance, the SFC's November 2025 circulars explicitly enabled VATPs to distribute HKMA-licensed stablecoins, opening the exchange channel without requiring issuers to build their own retail front end.

Tokenized deposits sit under an entirely different regime. The Banking Ordinance already governs deposit-taking, so HSBC's tokenized deposits and the banks participating in Project Ensemble do not need stablecoin licenses; their tokens are regulated as conventional bank deposits, with fractional reserve banking, deposit insurance, and interest-bearing characteristics that stablecoins cannot offer under the Stablecoins Ordinance.

Rather than forcing all digital money into a single regulatory box, Hong Kong has created separate pathways for stablecoins, tokenized deposits, and CBDC, letting each develop under the regime best suited to its characteristics while coordinating through joint HKMA-SFC circulars and government policy statements.

1.2 The Stablecoins Ordinance

Hong Kong's Stablecoins Ordinance (Cap. 656) is among the most detailed pieces of standalone stablecoin legislation anywhere in the world. It was shaped over three and a half years, beginning with the HKMA's January 2022 discussion paper, progressing through a December 2023 joint HKMA-government consultation and July 2024 framework conclusions, before the Legislative Council passed the bill on May 21, 2025 and the Ordinance took effect on August 1, 2025.

Scope: Fiat-Referenced Stablecoins (FRS)

The Ordinance applies to stablecoins that maintain a stable value with sole reference to one or more official fiat currencies, termed "Fiat-Referenced Stablecoins" or FRS. Critically, there is no currency restriction. Unlike Singapore's Monetary Authority of Singapore (MAS) framework, which limits the "MAS-regulated stablecoin" label to stablecoins pegged to SGD and G10 currencies, Hong Kong's framework permits FRS pegged to HKD, USD, EUR, CNH, or any other official fiat currency. Algorithmic stablecoins and crypto-backed stablecoins (e.g., DAI/USDS) fall entirely outside the FRS framework.

Who Must Be Licensed

The Ordinance captures three categories:

- Issuers of FRS in Hong Kong: Any entity issuing fiat-referenced stablecoins from Hong Kong must hold an HKMA license

- Issuers of HKD-linked FRS outside Hong Kong: The Ordinance has extraterritorial reach for HKD-pegged tokens, regardless of where the issuer is incorporated

- Entities actively marketing FRS to the Hong Kong public: The HKMA interprets "actively markets" broadly, considering language used, geographic targeting, and domain names

This creates a sharp split between retail and professional access. Only FRS from HKMA-licensed issuers can be offered to retail investors in Hong Kong. Unlicensed foreign stablecoins, including major global stablecoins like USDT and USDC, are restricted to professional investors only. Under the SFC's Professional Investor Rules, "professional investor" covers two broad groups:

- Institutional investors (banks, insurers, licensed SFC intermediaries, the HKMA, the government, and multilateral agencies)

- High-net-worth investors, defined as individuals with a portfolio of at least HK$8 million (approximately US$1 million), trust corporations with HK$40 million in trust assets, or other corporations with a portfolio of HK$8 million or total assets of HK$40 million.

Even with the April 10, 2026 licenses now granted to HSBC and Anchorpoint, no licensed stablecoin has yet entered circulation, which means Hong Kong retail investors still cannot access any HKD-denominated stablecoin through the city's regulated exchanges.

Licensing Requirements

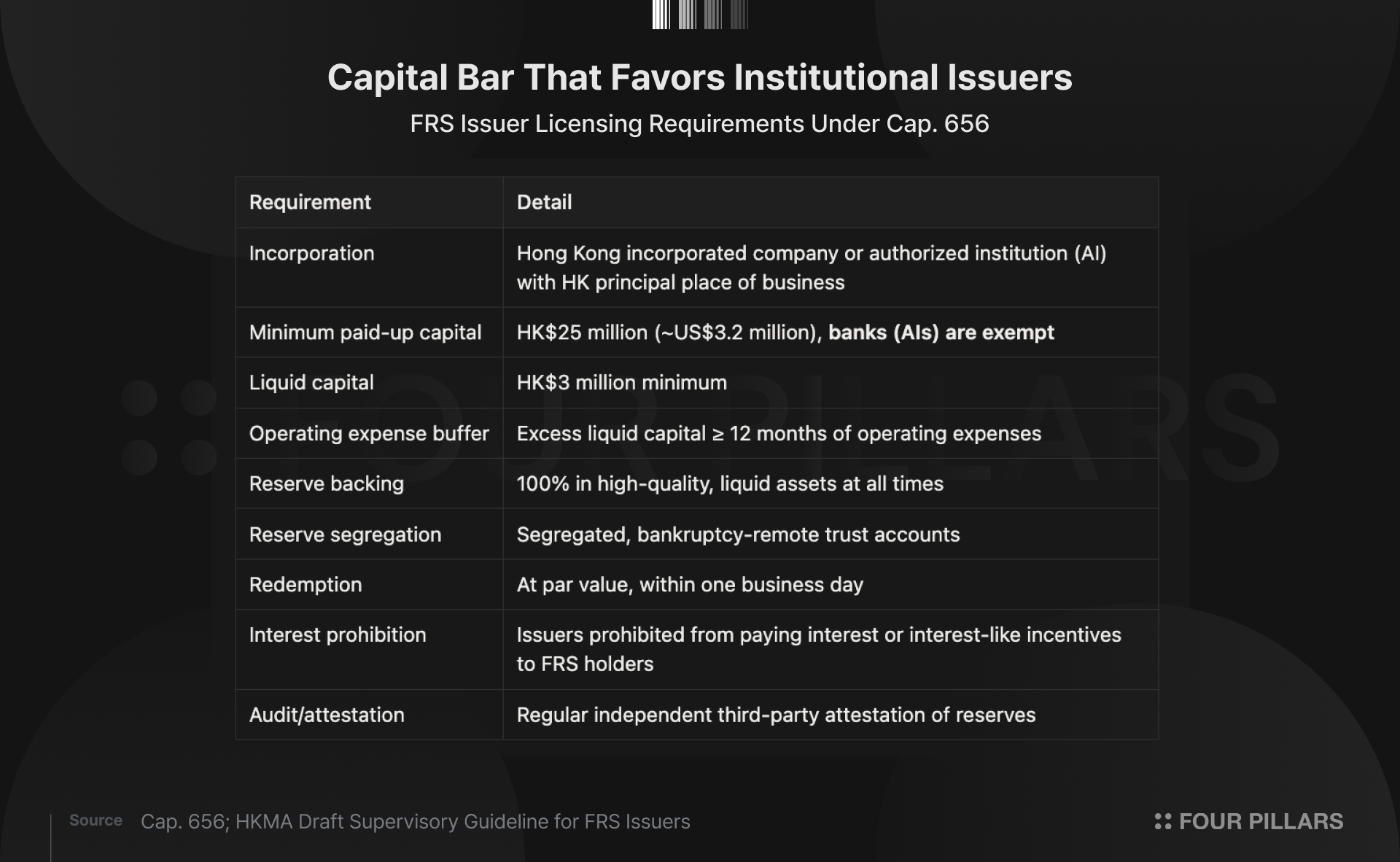

The financial requirements are deliberately steep, reflecting the HKMA's preference for well-capitalized institutional issuers:

The bank exemption from the HK$25 million capital requirement is worth noting. Authorized institutions under the Banking Ordinance, including HSBC, Standard Chartered, and Bank of China (Hong Kong), already meet far higher capital requirements under Basel III. This exemption effectively creates a two-tier system: banks face lower incremental regulatory cost to become stablecoin issuers, while non-bank applicants face a substantial capital threshold that filters out smaller fintech players.

For context, Hong Kong's HK$25 million minimum is substantially higher than Singapore's S$1 million (~US$750,000) and the EU MiCA's baseline of EUR 350,000. Japan sidesteps the question by restricting stablecoin issuance to already-regulated financial institutions (banks, trust companies, fund transfer providers), each with their own existing capital requirements.

Reserve rules broadly mirror Singapore, MiCA, and the US GENIUS Act: 100% backing in high-quality liquid assets, held in segregated bankruptcy-remote accounts with regular third-party attestation. The one distinctive twist is that the HKMA's draft supervisory guideline requires reserves to be held in the same reference currency as the stablecoin, quietly making HKD and USD far easier to support than CNH or other less liquid currencies.

Distribution: The Permitted Offeror Framework

Not everyone can sell stablecoins to the public. The Ordinance restricts offers, sales, and promotion of FRS to five categories of "Permitted Offerors":

- HKMA-licensed FRS issuers

- SFC-licensed VATPs (virtual asset trading platforms)

- SFC-licensed Type 1 corporations (dealing in securities)

- Authorized institutions under the Banking Ordinance

- Stored value facility (SVF) licensees under Cap. 584, added during legislative passage

The inclusion of SVF licensees was a late amendment, expanding potential distribution channels to include e-wallet operators, a recognition that stablecoins may ultimately compete or integrate with existing stored-value products like Octopus cards and mobile wallets.

1.3 Broader Digital Asset Framework

The Stablecoins Ordinance does not operate in isolation. It sits within a broader regulatory architecture covering virtual asset exchanges, tokenized securities, and digital bonds. Three pieces of this architecture matter directly for the stablecoin story: the VATP regime that controls how licensed stablecoins reach users, the SFC's approach to tokenization, and the grant program underwriting Hong Kong's digital bond pipeline.

The VATP Regime and Stablecoin Distribution

Hong Kong's exchange licensing regime is overseen by the SFC, separate from the HKMA's stablecoin issuer licensing. Platforms require Type 1 (Dealing in Securities) and Type 7 (Providing Automated Trading Services) licenses. As of February 2026, 12 VATPs are licensed, the most recent being Victory Fintech (VDX) on February 13, 2026, which ended an eight-month pause in new approvals. The caution has been bilateral: OKX, Gate.io, KuCoin, Binance, HTX, and Bybit all withdrew applications, largely because the SFC requires VATPs to prevent mainland Chinese residents from accessing services, a rule that conflicted with their user bases.

On November 3, 2025, the SFC published a circular that redefined what VATPs can do with stablecoins. VATPs may now distribute stablecoins from HKMA-licensed issuers, and these stablecoins are exempt from the 12-month track record requirement that normally applies to newly listed virtual assets, for both retail and professional investors. This means that the moment the HKMA grants a stablecoin license, the 12 licensed VATPs can immediately offer that stablecoin to retail customers with no waiting period. The same circular also expanded VATP custody to non-traded assets via affiliated entities, while a companion circular introduced a "Shared Order Book" model letting VATPs tap overseas affiliate liquidity, a general reform that licensed stablecoins would benefit from once listed.

Tokenization: The "See-Through" Approach

The SFC treats tokenization as a "wrapper" over traditional securities. Existing legal and regulatory requirements continue to govern the underlying asset, a tokenized bond is still a bond, subject to the same rules. The November 2025 circulars waived the 12-month track record requirement for tokenized securities entirely, recognizing that the underlying assets typically have established track records regardless of their digital form. This pragmatic approach has enabled Hong Kong to move quickly on tokenized government bonds and tokenized funds without requiring new primary legislation for each asset class.

Digital Bond Grant Scheme (DBGS)

To accelerate adoption, the HKMA launched the DBGS on November 28, 2024, a three-year program subsidizing 50% of eligible expenses for digital bond issuances (up to HK$2.5 million per issuance, capped at two issuances per issuer) to seed the market without providing open-ended support.

Part 2: Key Initiatives

Hong Kong's digital money initiatives split across two tracks. The stablecoin applicant field reveals the city's institutional character: of the 36 formal applications under HKMA review, only about 6–8 have been publicly identified, but they represent the full spectrum of Hong Kong's financial ecosystem, global banks, Chinese tech giants, a former central banker's startup, and licensed exchanges pivoting to issuance. On April 10, 2026, the first two licenses went to HSBC and to Anchorpoint Financial, the Standard Chartered–led joint venture, confirming the HKMA's note-issuing-bank-first approach and leaving the remaining applicants in contention for subsequent rounds.

Running alongside, and arguably ahead of, the stablecoin track are two adjacent forms of digital money already moving real value: tokenized bank deposits under Project Ensemble and HSBC's Tokenised Deposit Service, and the e-HKD wholesale CBDC. Sections 2.1 through 2.4 profile the stablecoin applicants and first licensees in turn; Section 2.5 covers the parallel tokenized deposit and e-HKD tracks and what addressable market they leave for FRS stablecoins.

2.1 Note-Issuing Banks: The Structural Advantage

HSBC, Standard Chartered, and Bank of China (Hong Kong) are Hong Kong's three note-issuing banks, the institutions authorized to issue physical HKD currency, a privilege dating back to the colonial era and continued under the Basic Law. Two of the three, HSBC and Standard Chartered (via Anchorpoint), took the first-batch licenses, with BOCHK notably absent from the initial round.

HSBC

HSBC's path to stablecoin issuance is unusual: it arrived from the tokenized deposit side rather than through the stablecoin sandbox. The bank did not participate in the HKMA's stablecoin issuer sandbox, concentrating its blockchain work instead on tokenized deposits (its Tokenised Deposit Service, discussed in Section 2.5) and capital markets infrastructure. Its first-batch license is therefore a strategic expansion rather than a sandbox graduation, giving the bank licensed footprints in both tokenized deposits and stablecoins simultaneously, the full optionality across the digital money spectrum.

HSBC has signaled a second-half 2026 launch for its HKD-denominated stablecoin, with distribution anchored in two of its existing retail channels: the HSBC HK mobile banking app and PayMe, HSBC's retail e-wallet with approximately 3.3 million Hong Kong users. Integrating directly into PayMe gives HSBC an immediate consumer front end without building a new one, and the initial use cases center on everyday retail activity: P2P transfers, peer-to-merchant payments, and in-app subscription to tokenized investments.

The technical foundation is substantial. HSBC's Orion platform has facilitated over US$3.5 billion in digitally native bonds globally, including Hong Kong's third digital green bond (HK$10 billion record) and the UK HM Treasury's DIGIT pilot. This gives HSBC deep experience in digital asset issuance and settlement, even though its application to stablecoins specifically is new. Product details remain the key near-term questions for HSBC's stablecoin business.

Standard Chartered → Anchorpoint Financial

Standard Chartered took the opposite approach: it entered the stablecoin sandbox early and built a dedicated joint venture. Anchorpoint Financial Limited was formed in February 2025 as a partnership between Standard Chartered Bank (Hong Kong), Animoca Brands, and HKT (Hong Kong Telecommunications). The exact ownership percentages have not been disclosed, but SCMP describes it as "Standard Chartered-led." The first-batch license is the culmination of the sandbox-first strategy Anchorpoint had pursued since July 2024.

Anchorpoint was the first entity to formally initiate the licensing process on August 1, 2025, the day the Stablecoins Ordinance took effect. It had been in the HKMA sandbox since July 2024, testing use cases including tokenized payroll processing and cross-border settlements, reportedly cutting transfer costs from $15,000 to $500 for $10 million transactions.

The target product is an HKD-backed stablecoin aimed at both Web3-native and traditional payment use cases: in-app purchases on Animoca's gaming platforms, retail payments through HKT's Tap & Go mobile wallet, and cross-border settlement via Standard Chartered's banking network. This is the broadest distribution strategy among the applicants, spanning Web3, mobile payments, and institutional banking in a single vehicle.

Bank of China (Hong Kong)

BOCHK is the most conservative of the three note-issuing banks. It has formally applied for a stablecoin license, established a dedicated working group, and is among the 36 applications under HKMA review. But it has made no public announcements about specific stablecoin products, formed no joint ventures, and issued no detailed strategy statements. At a recent earnings announcement, the bank stated only that it is actively researching application scenarios and risk management mechanisms for digital assets.

Where BOCHK has been active is in the CBDC and tokenized deposit space. In the e-HKD+ Phase 2 pilot, BOCHK issued unified digital wallets to approximately 500 test participants, running approximately 1,500 e-HKD transactions on its proprietary alliance blockchain integrated with multiple mobile banking applications. It is also one of seven banks participating in Project Ensemble, though it has not been named in the specific real-value transactions that HSBC and Standard Chartered completed.

BOCHK's caution likely reflects its dual identity. As a mainland Chinese state-owned bank operating in Hong Kong, it must navigate both HKMA expectations and Beijing's preferences, a balancing act that became more complex after the February 2026 People's Bank of China (PBOC) directive on RMB stablecoins (discussed in Part 3).

2.2 Chinese Tech Giants: JD.com & Ant Group

The presence of mainland China's largest technology companies is the single most distinctive feature of Hong Kong's stablecoin market. No other jurisdiction has this combination of institutional banking capital and Chinese tech capital competing for stablecoin licenses, though as Part 3 details, Beijing's 2025–2026 interventions have cast a long shadow over both applicants.

JD.com (Jingdong Coinlink)

Jingdong Coinlink Technology Hong Kong Limited is a wholly-owned subsidiary of JD Technology Group (formerly JD Digits, originally JD Finance). It entered the HKMA sandbox in July 2024 with ambitions to issue an HKD-pegged stablecoin (JD-HKD) targeting cross-border payments and supply chain finance, with plans for a USD-pegged stablecoin and potentially an offshore RMB stablecoin pending Beijing's approval.

The business case is built on JD's existing infrastructure. JD Chain (智臻链, Zhizhen Chain) is JD's independently developed permissioned enterprise blockchain, launched in 2018, serving supply chain finance, cross-border payments, product traceability, and e-CNY integration. The stablecoin pitch was that it can reduce cross-border payment costs by 90% and settlement time to under 10 seconds by routing JD's existing cross-border trade flows through stablecoin rails rather than correspondent banking.

JD completed two phases of sandbox trials, with use cases including cross-border settlements and experimental retail payments. Beijing's intervention then hit JD directly. The company officially denied exiting and confirmed Coinlink remains an active applicant, but reporting from KR-Asia paints a bleaker picture, citing sources familiar with JD's decision-making who suggest the subsidiary has effectively abandoned its stablecoin efforts, in part due to what they describe as excessive regulatory oversight from Hong Kong authorities.

Ant Group (Ant International & Ant Digital Technologies)

Ant Group's stablecoin strategy is complicated by its 2024 corporate restructuring, which split the group into three independently operated subsidiaries. Two of them are pursuing stablecoins in Hong Kong: Ant International (headquartered in Singapore, focused on cross-border payments through Alipay+, treasury management, and global financial services) and Ant Digital Technologies (international HQ established in Hong Kong in April 2025, focused on AI, blockchain, and privacy computing, and developer of Jovay, a Layer 2 public blockchain for RWA tokenization). Ant Digital completed sandbox testing and filed a trademark for "Antcoin" in Hong Kong, while Ant International is pursuing licenses simultaneously in Hong Kong, Singapore, and Luxembourg, announced June 2025.

In a parallel move, Ant Group acquired a 50.55% controlling stake in Hong Kong-listed brokerage Yau Choy Securities in March 2026 for HK$2.814 billion, giving it effective control of a fully licensed Hong Kong entity through which to pursue stablecoin and virtual asset approvals rather than building from scratch.

Ant International's scale is formidable. Its blockchain-based Whale platform processed over US$1 trillion in global transactions in 2024, with approximately one-third settled on-chain. Ant International joined Project Ensemble's sandbox in August 2024 as an industry partner (not a bank issuer), focusing on liquidity management use cases and collaborating with HSBC and Standard Chartered on global liquidity solutions.

Like JD.com, both Ant entities were caught by Beijing's interventions and neither was included in the first-batch allocation. But Ant's multi-jurisdiction strategy (HK + Singapore + Luxembourg) and its existing transaction infrastructure suggest it is positioning for the long term rather than the opening round.

2.3 RD Technologies: The Startup Pioneer

RD Technologies occupies a unique position in the applicant field: it is the closest thing to an independent fintech startup in a market dominated by banks and tech conglomerates, but its founder is Hong Kong's former top financial regulator.

Norman Chan Tak-lam served as Chief Executive of the HKMA from 2009 to 2019, giving RD Technologies an unusual depth of regulatory experience among the applicant field. Before that, he was Vice Chairman of Asia at Standard Chartered Bank (2005–2007) and a member of the Financial Stability Board. He founded RD Technologies in 2020, making it one of Hong Kong's earliest stablecoin-focused ventures.

Unlike most stablecoin applicants, RD Technologies already operates a live, licensed business. Its flagship payments arm, RD Wallet Technologies Limited (RDWT), holds a Stored Value Facility license (SVF0016) from the HKMA and runs Hong Kong's first enterprise-focused digital wallet, offering corporate customers multi-currency accounts (HKD, CNY, USD, JPY, SGD, EUR, GBP, AUD), cross-border payments, and FX services with 100% mobile onboarding. In September 2025, RDWT rebranded its cross-border payment service as OristaPay; the legal entity and SVF license are unchanged, only the brand. OristaPay launched its Global Collection service in January 2026.

Alongside this live payments business, RD Technologies' sandbox subsidiary RD InnoTech is developing HKDR, a planned Hong Kong dollar-pegged stablecoin designed to be backed 1:1 by fiat reserves and issued on Ethereum. HKDR would plug directly into RD Wallet and OristaPay's existing cross-border corridors, giving the stablecoin an immediate institutional user base the day it launches. As of April 2026, however, HKDR remains sandbox-stage; RD Technologies was not included in the first-batch licenses and HKDR has not yet entered circulation.

2.4 OSL Group: From Exchange to Issuer

OSL Group is attempting something none of the other licensed exchanges are: pivoting from distribution to issuance. OSL was the first exchange to receive SFC Type 1 and Type 7 licenses in December 2020, making it the pioneer of Hong Kong's licensed VATP ecosystem. It is now also pursuing an HKMA stablecoin issuer license.

While OSL's application is still under review, OSL is not just waiting for the HKMA license to enter the stablecoin market. On February 10, 2026, OSL Group unveiled USDGO, a USD-denominated enterprise stablecoin issued by Anchorage Digital Bank, with OSL as the branding partner and distributor. USDGO is 1:1 backed by US Treasuries and other high-quality liquid assets, initially deployed on Solana, and targets institutional cross-border settlement. In Hong Kong, USDGO is distributed exclusively through OSL Digital Securities Limited under its existing SFC license.

Because USDGO is not issued by an HKMA-licensed issuer under Cap. 656, it falls under the same retail restriction as USDT and USDC: OSL can only offer it to professional investors, not retail. Even so, this makes OSL the only Hong Kong-based entity already plugged into a live stablecoin product, albeit USD-denominated, US-regulated, and professional-only in its home market.

If OSL secures an HKMA issuer license while maintaining its SFC VATP license, it would be the only entity in Hong Kong holding both, an issuer that can list its own stablecoin on its own exchange. HSBC and Anchorpoint can sell their own stablecoins through banking and consumer channels as Permitted Offerors, but neither operates a secondary trading venue. Combined with USDGO's existing USD stablecoin infrastructure, OSL would offer both HKD and USD stablecoins across regulated and DeFi channels.

2.5 Tokenized Deposits & e-HKD: The Parallel Tracks

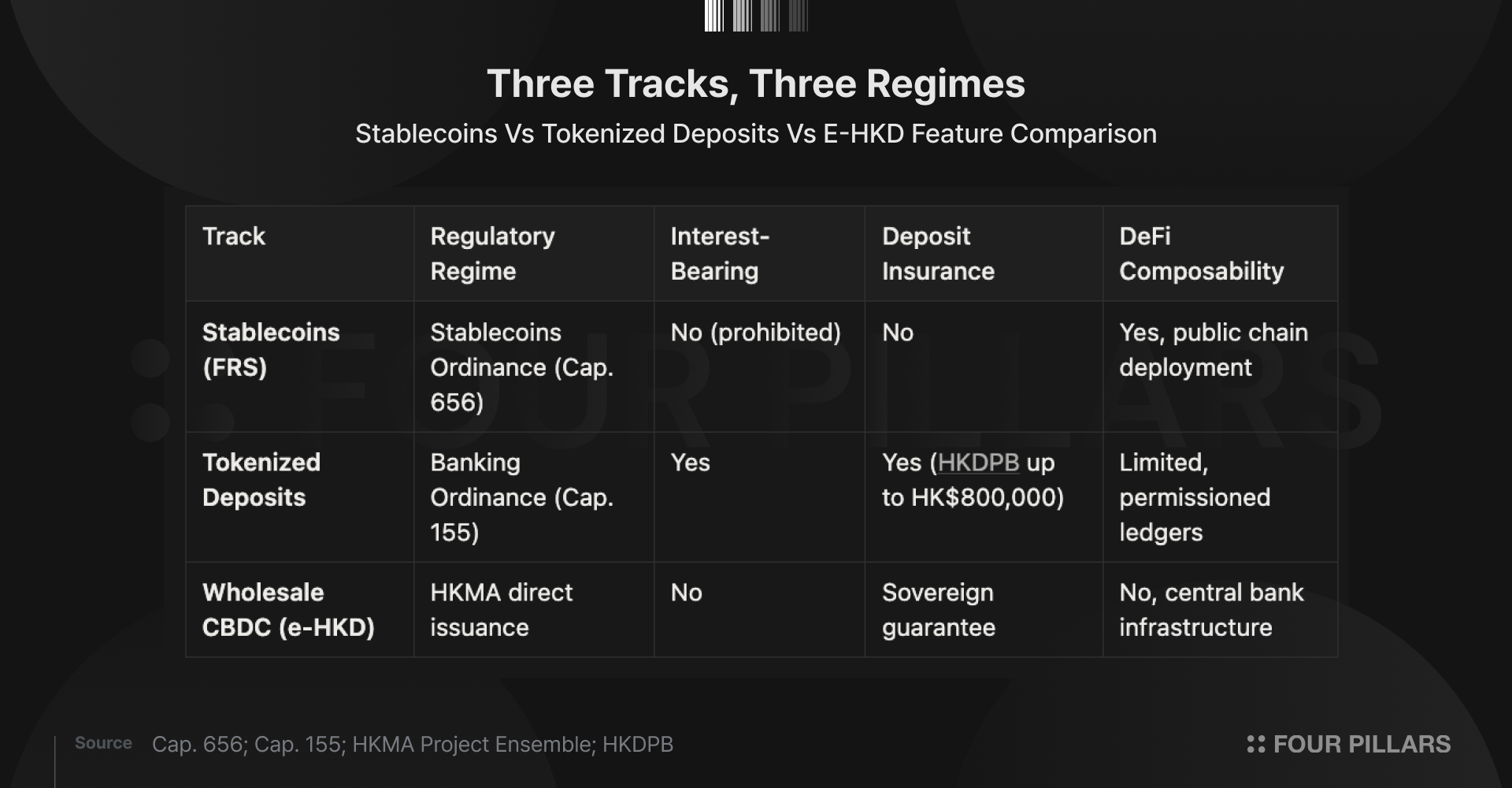

Two adjacent forms of digital money are already operating in Hong Kong under entirely different regulatory regimes from FRS stablecoins:

- Tokenized deposits are governed by the Banking Ordinance (Cap. 155), allowing any authorized institution to issue them without an HKMA stablecoin license, with deposit insurance and interest-bearing characteristics that FRS stablecoins are statutorily prohibited from offering.

- e-HKD is the HKMA's wholesale CBDC, a direct central bank liability designed to settle the interbank leg between participating banks.

Both are already moving real value while licensed stablecoins wait for their first circulating token, and together they shape what addressable market remains.

Project Ensemble

Launched in March 2024, Project Ensemble is the HKMA's flagship initiative for tokenized deposit infrastructure, designed to enable seamless interbank settlement of tokenized commercial bank money, ultimately upgraded to 24/7 settlement in tokenized central bank money (CeBM). Each participating bank operates its own DLT infrastructure with interoperability achieved at the settlement layer, initially through the existing HKD RTGS system and progressively upgrading to CeBM for around-the-clock finality. The sandbox phase ran from August 2024, and on November 13, 2025 the project transitioned to EnsembleTX, a live pilot processing real-value transactions across seven participating banks throughout 2026. The first day saw HSBC complete a HK$3.8 million tokenized deposit transfer for Ant International. Standard Chartered completed two transactions, including a tokenized deposit transfer that helped Futu Securities subscribe to ChinaAMC's tokenized money market fund, the first use of tokenized deposits to purchase a tokenized financial product.

HSBC's Tokenised Deposit Service

While Project Ensemble provides the interbank rail, HSBC has built the most advanced individual bank implementation: the Tokenised Deposit Service (TDS), launched for corporate clients in Hong Kong and Singapore in May 2025, extended to UK and Luxembourg in September 2025 (adding EUR and GBP), and planned to expand to US and UAE in H1 2026. By early 2026, TDS operates across four countries in five currencies. TDS tokens are direct balance-sheet liabilities of HSBC, accumulate interest, are covered by deposit insurance where applicable, and are regulated under the Banking Ordinance — all of which makes them fundamentally different from FRS stablecoins.

e-HKD

The e-HKD is Hong Kong's central bank digital currency, a direct HKMA liability sitting above tokenized deposits in the monetary hierarchy. In Project Ensemble's architecture, tokenized deposits are what banks issue to clients while e-HKD (in CeBM form) settles the interbank leg, mirroring traditional banking but with both layers tokenized and capable of 24/7 operation beyond RTGS hours. The program ran two pilot phases between 2022 and 2025, with Phase 2 renamed e-HKD+, and the October 2025 report confirmed the HKMA's strategic direction: wholesale first, retail later. CeBM settlement for Project Ensemble and cross-border sovereign corridors is the priority; retail CBDC foundations will be ready by H1 2026 but implementation remains undetermined.

If institutional use cases consolidate around the deposit and CBDC stack, the addressable market for FRS stablecoins narrows to retail payments and bearer-instrument niches that bank-issued tokens cannot serve.

Part 3: The China Dimension

No other jurisdiction's stablecoin story has anything quite like this. Hong Kong operates under "one country, two systems", with regulatory autonomy over financial markets but political alignment with Beijing. This creates both the jurisdiction's greatest advantage and its greatest source of uncertainty: Beijing can constrain the scope of permissible innovation at any time, as it did twice in 2025–2026.

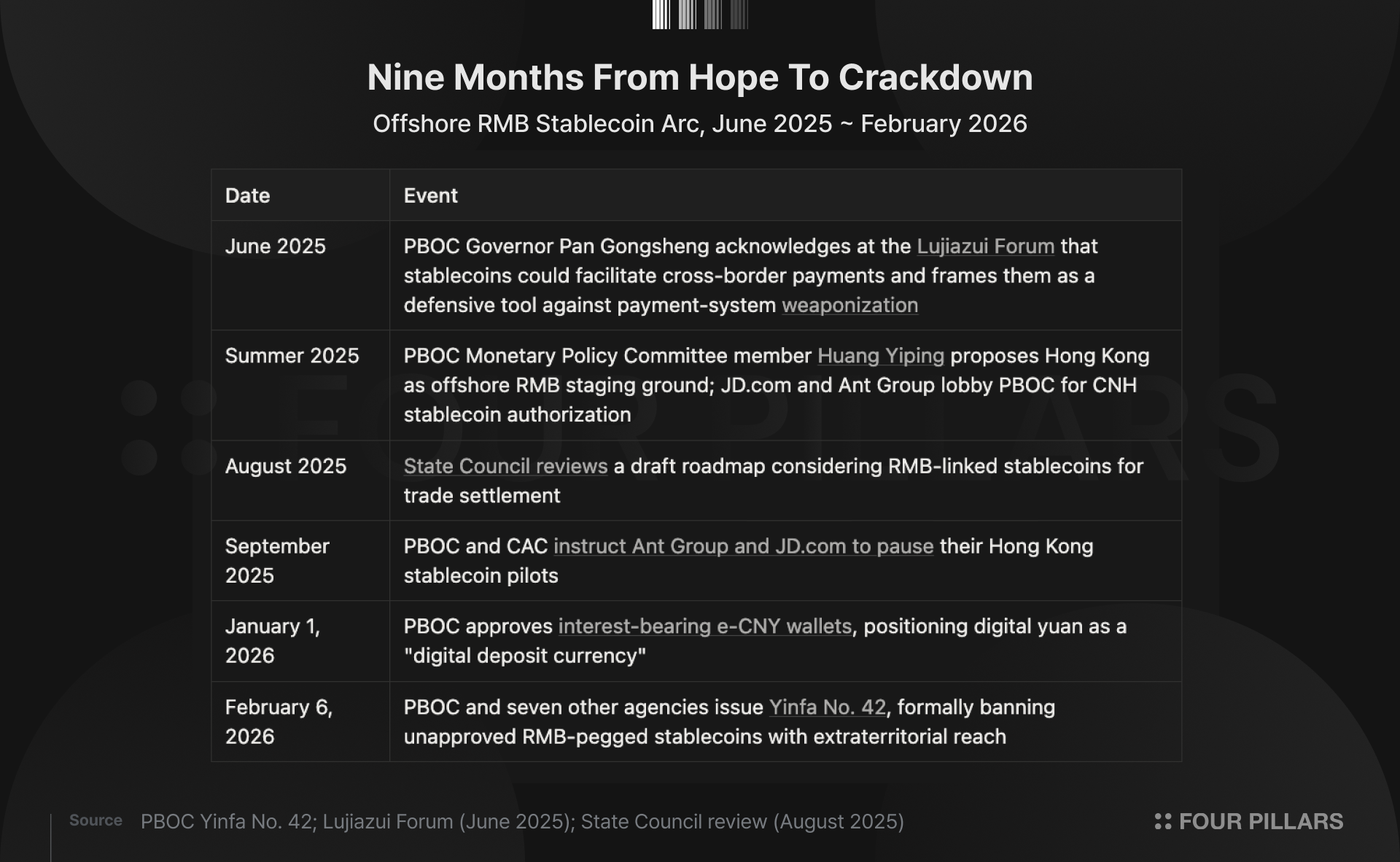

The most dramatic arc in Hong Kong's stablecoin story is what happened to the offshore RMB stablecoin, an idea that went from tentative PBOC endorsement to formal ban in less than nine months.

Hong Kong's currency-agnostic framework was designed with CNH in mind. For a few months in mid-2025, it looked like Beijing might let it work: the PBOC governor publicly framed stablecoins as a defensive tool against payment-system weaponization, mainland tech giants lobbied for offshore yuan authorization, and the State Council reviewed a draft roadmap for RMB-linked trade settlement. The motivation was not enthusiasm but defense: with 99% of stablecoins USD-pegged and the US GENIUS Act having just locked that dominance into law, Beijing had a strategic interest in offshore yuan rails it could control.

The opening closed in two steps. A September 2025 instruction told JD.com and Ant Group to pause their pilots, and Yinfa No. 42 in February 2026 made the reversal formal: eight regulators classified all virtual-currency activity as illegal financial activity, banned unapproved RMB-pegged stablecoin issuance, and restricted RWA tokenization. The decisive clause for Hong Kong was the extraterritorial language reaching "domestic entities and the overseas entities they control", because an offshore CNH stablecoin only matters if mainland-connected entities can use it, and the directive ensured they cannot.

The other half of the strategy is e-CNY. By approving interest-bearing wallets in January 2026, the PBOC pushed the digital yuan from "digital cash" toward a "digital deposit currency" capable of competing with both stablecoins and commercial bank deposits. Hong Kong's November 2025 HK$10 billion digital green bond, which settled an RMB tranche in e-CNY alongside an HKD tranche in e-HKD, had already demonstrated that e-CNY can clear cross-border capital market settlement without private stablecoins as intermediaries. Beijing's preference is now explicit: digital RMB will exist, but as a state instrument.

For Hong Kong, this leaves the Stablecoins Ordinance currency-agnostic only on paper. CNH was the framework's most distinctive use case, and Yinfa No. 42 has put it out of reach. AxCNH (AnchorX) launched in Kazakhstan rather than Hong Kong specifically to stay outside Beijing's reach. JD.com and Ant Group remain in the HKMA process for HKD and USD licenses, and Ant's March 2026 acquisition of Yau Choy Securities signals a long-horizon Hong Kong strategy rather than a retreat, but the RMB stablecoin both originally wanted is off the table.

The "China gateway" thesis is not dead, but it is now constrained to HKD and USD and the timeline has been pushed back significantly. A narrower pathway still exists: HKD stablecoins could become the critical link between e-CNY and global digital assets without ever touching an RMB stablecoin, with the HKD's peg to the USD making HKD stablecoins quasi-USD instruments that bridge the dollar-denominated stablecoin world and Beijing's digital yuan infrastructure.

Part 4: Outlook

The immediate test is whether HSBC and Anchorpoint can turn their April 10 licenses into circulating tokens before USDT and USDC entrench further in Hong Kong itself. A second batch will show whether the HKMA moves beyond note-issuing banks, and whether the narrowed HKD/USD-only gateway still appeals to mainland tech giants who wanted CNH. Running alongside is the structural question of whether licensed stablecoins can carve out a role before tokenized deposits absorb the institutional use cases: HSBC's TDS is already live across four countries and Project Ensemble across seven banks. If institutional treasury and interbank settlement consolidate around the deposit and CBDC stack, FRS stablecoins are pushed toward retail and bearer-instrument niches. By late 2026 the market should know whether Hong Kong's stablecoins have found real demand or remain compliance products without product-market fit.

The largest swing factor is Beijing. Yinfa No. 42 froze RMB stablecoins, but the State Council's August 2025 deliberation showed the idea is under consideration, not closed, and pressure from the GENIUS Act, e-CNY's cross-border limits, and trade settlement demand could all reopen the calculus. Hong Kong's currency-agnostic framework is ready for CNH the moment Beijing permits it, which would shift the city from "Asia's HKD/USD hub" to the offshore venue for a currency covering roughly a fifth of global trade. The opposite path, where Beijing tightens further and constrains JD.com and Ant Group's Hong Kong operations, erodes the China gateway thesis to rhetoric. Either outcome is plausible within twelve to eighteen months, and which one lands determines whether Hong Kong's regulatory architecture anchors a differentiated digital money hub or becomes the most sophisticated framework in Asia for a market that moved on without it.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.