Table of Contents

- Key Takeaways

- 1. Korea's Crypto Taxation Enters the Countdown

- 2. The Gaps in Korea's Crypto Tax Regime

- 2.1 What Has Been Decided: Income from Transfers and Lending

- 2.2 The Onchain Activity Domain Is Completely Empty

- 3. The U.S. Crypto Taxation System: A Structure Built on Self-Reporting

- 3.1 Asset Classification and Taxation Principles

- 3.2 Areas Treated as Ordinary Income

- 3.3 The DeFi Gray Zone: The Burden of a Conservative Approach

- 3.4 Token Sales and ICOs

- 3.5 The US Tax Infrastructure: A Dual Structure of Exchange Reporting and Self-Reporting

- 4. Why Korea Has No Choice but to Adopt a Self-Reporting Based Model

- 4.1 The Inevitability of Self-Reporting

- 4.2 CARF Adoption and the Pressure of Global Information Standards

- 4.3 Time Pressure

- 5. The Likely Shape of Korea's Cryptocurrency Tax Regime

- 6. The Feasibility of Korea's Integrated Virtual Asset Analysis System

Researcher

Key Takeaways

- On April 29, 2026, the National Tax Service (NTS) announced that it has begun building infrastructure in earnest, on the premise that crypto taxation will take effect on January 1, 2027. Data collection from exchanges, the construction of an integrated analysis system, and the development of an information exchange framework based on CARF are all proceeding in parallel, with the first filings expected in May 2028 as part of the comprehensive income tax filing.

- Current income tax law, however, has barely established taxation standards for areas beyond simple trading and crypto-to-crypto exchanges, namely DeFi staking and lending, airdrops, hard forks, and NFTs. The NTS itself has stated that it is in the process of gathering overseas legislative cases and expert opinions.

- Since Notice 2014-21 in 2014, the United States has classified cryptocurrency as property and has built up taxation principles for nearly every area, including simple trading and exchanges, DeFi, staking, and airdrops, on the basis of self-reporting. Form 1099-DA, which took effect in 2025, applies only to centralized exchanges, while DeFi remains the taxpayer's own responsibility.

- Given the constraints of underdeveloped infrastructure and a short preparation window, Korea is likely to adopt the broad framework of the U.S. model. The four pillars are asset classification, the self-reporting principle, the phased introduction of exchange reporting obligations, and the provisional neglect of the DeFi gray zone.

- This convergence brings side effects such as fairness issues, regulatory arbitrage between domestic exchanges and overseas/DeFi venues, and the shifting of documentation burdens onto taxpayers. The start of taxation is only a starting point, and supplementary legislation aimed at securing substantive fairness is unlikely to be enacted within this year.

1. Korea's Crypto Taxation Enters the Countdown

On April 29, 2026, during a briefing on the May comprehensive income tax filing, Park Jung-yeol, Director of the Individual Taxation Bureau at the NTS, was asked about preparations for cryptocurrency income tax filings. He replied, "Since the law has been enacted to tax cryptocurrency income arising from next year, we are preparing to receive filings starting with the May 2028 comprehensive income tax return." Even amid continued calls from political circles to abolish the tax, the tax authority has now begun substantive operational preparation on the premise of implementation.

Source: Bloomingbit

According to the response, preparation is proceeding along three tracks: a system for compiling data from domestic exchanges, the "Virtual Asset Integrated Analysis System" announced last month by the Public Procurement Service, and the development of CARF (Crypto-Asset Reporting Framework) based information exchange functions.

Under the current Income Tax Act, income arising from the transfer or lending of cryptocurrency from January 1, 2027 will be classified as other income, with separate taxation of 22% applied to the portion exceeding 2.5 million won annually. The taxable scope covers all domestic cryptocurrency investors.

Whether implementation will proceed without disruption, however, remains uncertain. In a November 2025 report, the Korea Capital Market Institute assessed that "the current Income Tax Act's framework for taxing virtual asset other income has too many unsettled gaps to be implemented on January 1, 2027," raising the possibility of a fourth deferral. Detailed guidelines on what to tax, how to tax it, and when remain absent.

2. The Gaps in Korea's Crypto Tax Regime

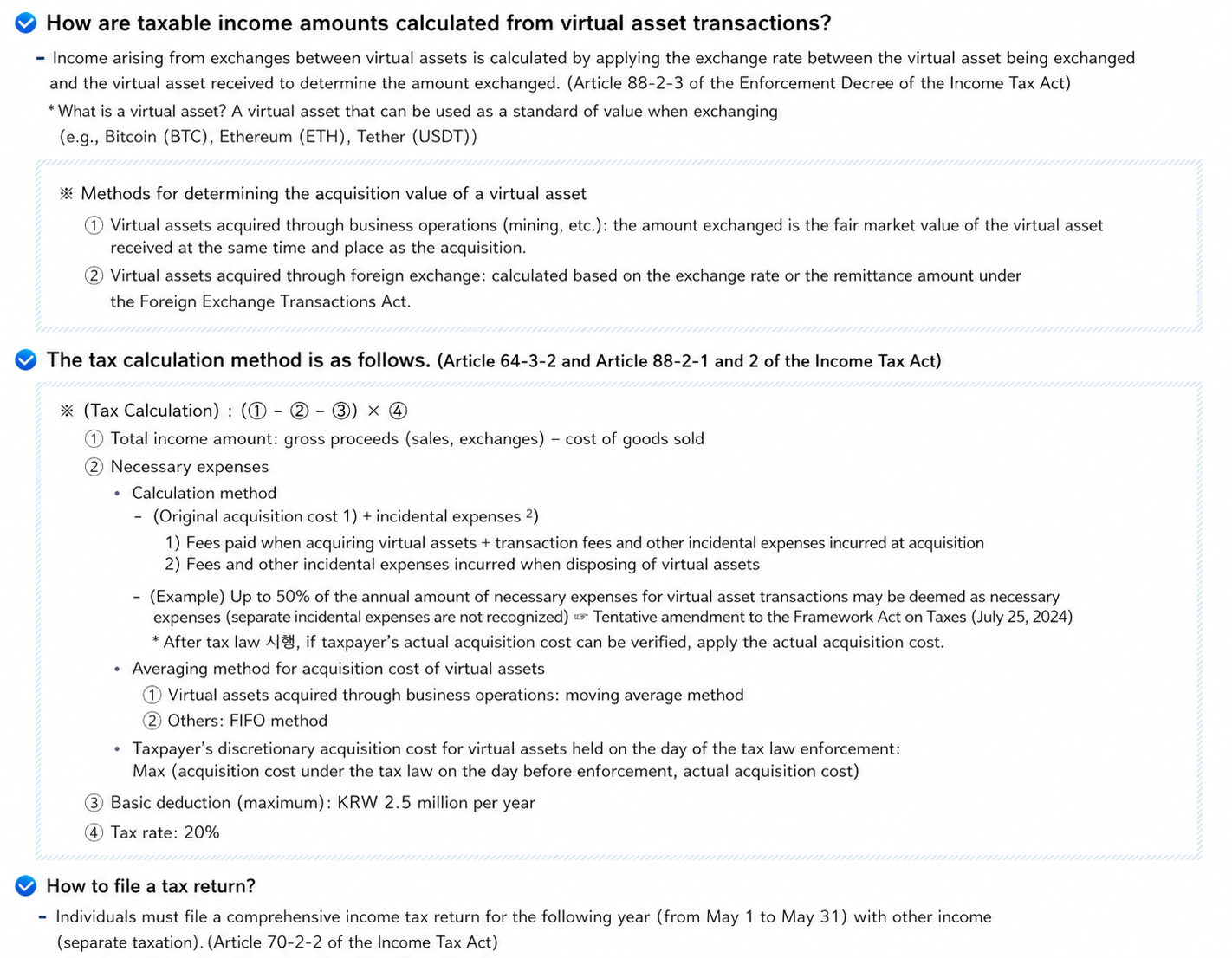

2.1 What Has Been Decided: Income from Transfers and Lending

Source: NTS (Reproduced Image)

According to the Overview of Virtual Asset Income Taxation published by the NTS, taxable income is calculated as proceeds from the transfer or lending of cryptocurrency, less necessary expenses. The general rule for necessary expenses is the actual acquisition cost plus incidental costs. Where the actual acquisition cost of cryptocurrency obtained after implementation is difficult to verify, a portion of the transfer price (up to 50%) may be deemed as necessary expense.

For acquisition cost valuation, the moving average method applies to exchange transactions, while the first-in-first-out method applies to others. The deemed acquisition cost for holdings held before the law's effective date is set at the greater of the market price as of December 31, 2026 or the actual acquisition cost. For income from crypto-to-crypto exchanges, the value is calculated by applying the exchange ratio to the value of the base virtual asset (Bitcoin in BTC markets, Ethereum in ETH markets, Tether in USDT markets, and so on).

This is the limit of what has been clearly established. Nominally, taxation is feasible only for spot trading on exchanges and crypto-to-crypto exchanges.

2.2 The Onchain Activity Domain Is Completely Empty

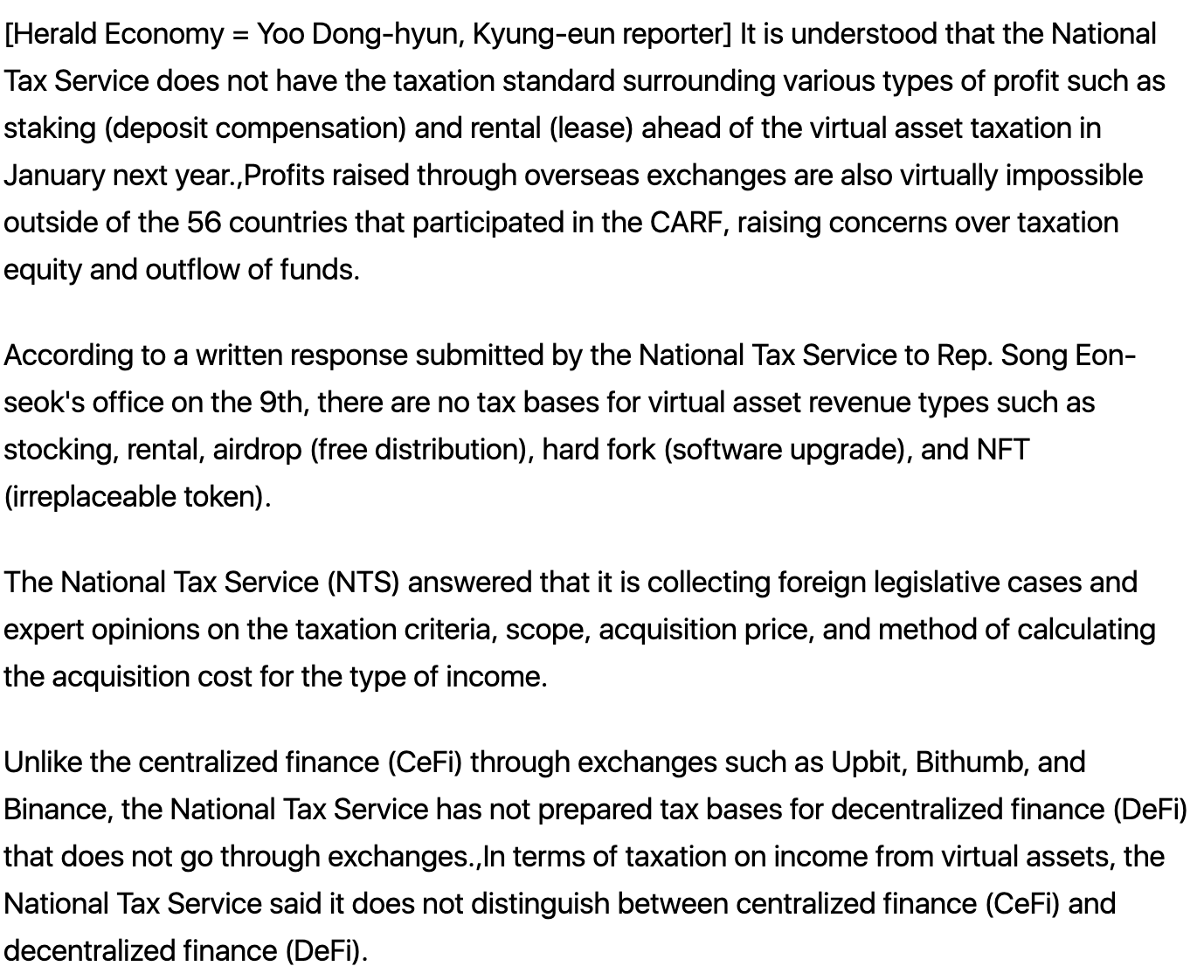

Source: Herald Economy

The problem lies in everything else. In a written response submitted to Representative Song Eon-seok's office, the NTS stated that taxation criteria are absent for cryptocurrency income types such as staking, lending, airdrops, hard forks, and NFTs. Regarding whether such income types are taxable, their scope, and how to compute acquisition cost and original cost basis, the NTS replied that it is "currently gathering overseas legislative precedents and expert opinions."

Particularly noteworthy is the NTS's response that "from the perspective of cryptocurrency income taxation, centralized finance and decentralized finance are not separately distinguished." Not making a separate distinction means applying the same principles, but it also means there is no separate guideline that reflects the characteristics of DeFi transactions. There is no explicit standard for how taxation applies when a user swaps tokens on Uniswap from a self-custody wallet, deposits assets on Aave to earn interest, or stakes ETH on Lido to receive stETH.

It is not realistic for Korea to fill these gaps independently within a short period. The cryptocurrency industry itself moves at a very fast pace globally, and DeFi continually produces new variations. Given that expanding tax infrastructure is realistically difficult to accomplish in a short time, I expect Korea's taxation model will naturally end up following the most established precedent, the US model. The next section examines the current US cryptocurrency taxation structure.

3. The U.S. Crypto Taxation System: A Structure Built on Self-Reporting

3.1 Asset Classification and Taxation Principles

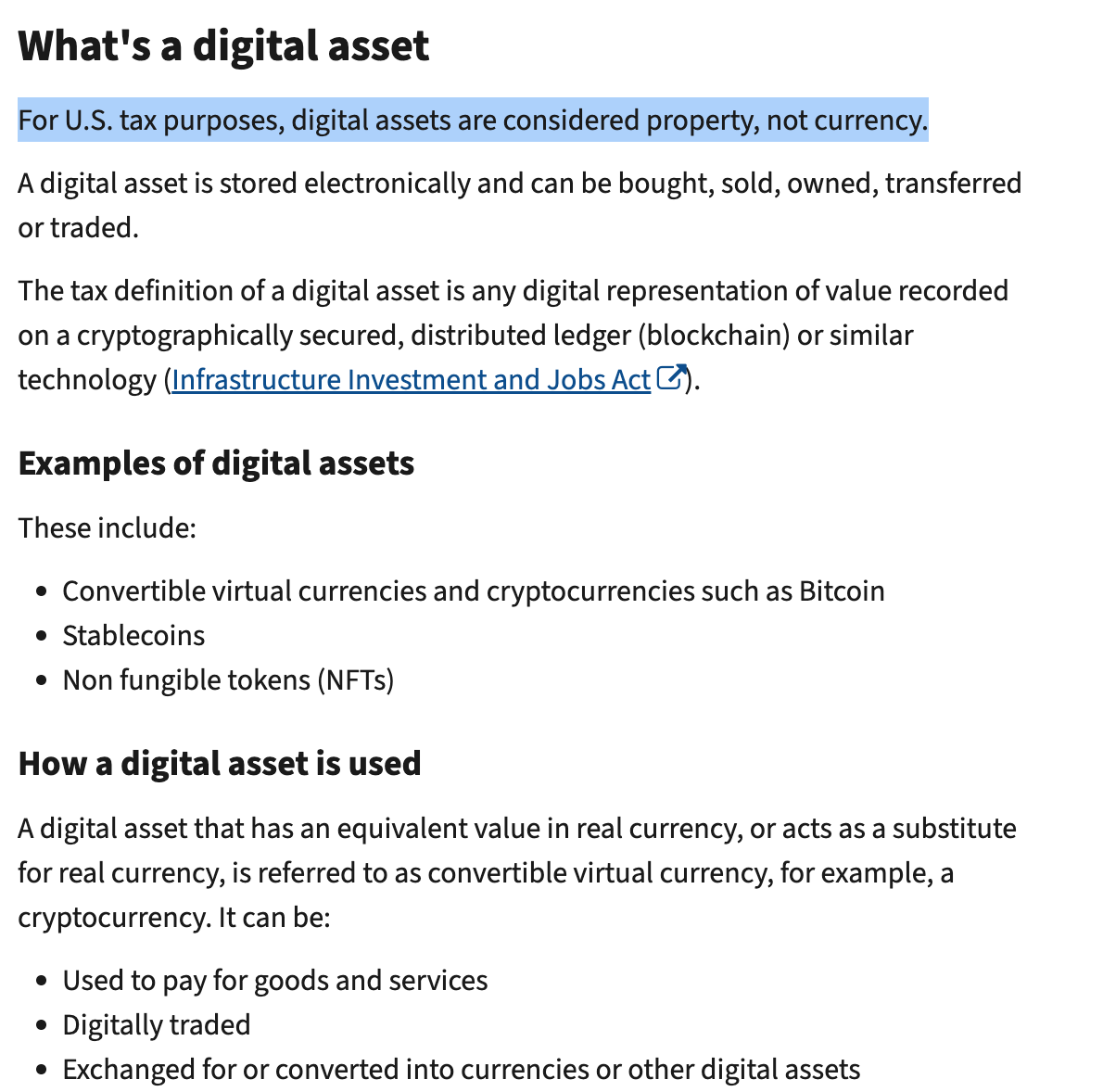

Source: IRS

Through Notice 2014-21, the Internal Revenue Service (IRS) classified cryptocurrency as property rather than currency, and all subsequent guidance has been built on this premise. Classification as property means that the same capital gains principles applied to stocks or real estate apply here. Holding alone is not a taxable event, but capital gains or losses are recognized whenever a disposal occurs.

Capital gains treatment splits into two depending on the holding period. Disposal after holding one year or less results in short-term capital gains, taxed at ordinary income rates (10–37%). Holding for more than one year qualifies as long-term capital gains, taxed at preferential rates (0%, 15%, or 20%).

What matters here is that the definition of "disposal" extends well beyond simple sales. The IRS treats all of the following as disposals:

- Selling cryptocurrency for fiat

- Exchanging cryptocurrency for another cryptocurrency

- Paying for goods or services with cryptocurrency

- Exchanging cryptocurrency for other assets

Among these, the second item, that crypto-to-crypto exchanges trigger capital gains taxation, is especially important. Swapping ETH for USDC or exchanging BTC for ETH is treated under US tax law identically to selling ETH and using the proceeds to purchase USDC.

3.2 Areas Treated as Ordinary Income

Separate from capital gains, the United States includes cryptocurrency from the following activities in ordinary income at the fair market value at the time of receipt:

- Mining: Mined cryptocurrency is recognized as ordinary income at the market price at the time of receipt. When operated as a business, related expenses can be deducted.

- Staking: Under Revenue Ruling 2023-14, staking rewards are recognized as ordinary income at the market price at the moment the taxpayer gains the ability to sell, exchange, or transfer the tokens. If rewards are locked or unclaimable, recognition is deferred until the point of dominion and control.

- Airdrops: Under Revenue Ruling 2019-24, airdrops are included in ordinary income at fair market value on the date the taxpayer obtains control. Upon subsequent sale, that value becomes the cost basis for separately calculating capital gains or losses.

- Hard Forks: The same guideline as airdrops applies. The fork itself is non-taxable, but receiving new coins as a result triggers ordinary income treatment at the time of receipt.

- Lending Interest: Whether on DeFi or centralized lending, interest is recognized as ordinary income at the time of receipt. Subsequent sales are separately computed for capital gains or losses.

For example, if a user receives 1 ETH as a staking or lending reward, ordinary income tax is first owed on the market value at the time of receipt, and then capital gains tax is owed again on any price change when that 1 ETH is sold. This creates a double-layered structure.

3.3 The DeFi Gray Zone: The Burden of a Conservative Approach

DeFi taxation remains an area where codified guidance is lacking even in the United States. The IRS has taken the position that principles inferred from general digital asset guidance also apply to DeFi, and a conservative approach has become the de facto standard in practice.

- Liquidity Pools: Conservatively, depositing tokens and receiving LP tokens is treated as a taxable transaction in which the two tokens are exchanged for an LP token, and another taxable event occurs upon withdrawal. A more aggressive interpretation views it as a non-taxable loan, but with no explicit rule on point, the conservative approach is recommended.

- Liquid Staking: An ETH-to-stETH swap can plausibly be interpreted as a taxable exchange, and the increase from stETH rebasing is generally treated as ordinary income. There is no separate IRS guidance on this.

- Lending: A crypto-collateralized loan itself is non-taxable, but in the event of liquidation, the collateral is treated as sold at its value at the time of liquidation.

- Bridging: Simple movement of the same asset is non-taxable, but when wrapping or unwrapping is involved, part of the transaction may be regarded as an exchange into a different asset and treated as taxable.

The common thread across all these areas is that, despite the lack of explicit IRS guidance, the responsibility for self-reporting falls squarely on the taxpayer.

3.4 Token Sales and ICOs

Purchasing tokens through an ICO or IEO is not itself a taxable event at the moment of purchase, but the token used for the purchase is treated as disposed of, and capital gains or losses are recognized accordingly. The cost basis of the tokens received is the value of the tokens used at the time of purchase, or the fair market value of the tokens acquired. On the issuer's side, token sale proceeds are treated as ordinary or business income, and additional regulations may apply depending on whether the token qualifies as a security.

3.5 The US Tax Infrastructure: A Dual Structure of Exchange Reporting and Self-Reporting

The most interesting aspect of the US cryptocurrency tax system is that nearly every area operates as a dual structure of self-reporting plus exchange reporting.

The final regulations issued by the Treasury and IRS in July 2024 introduced Form 1099-DA (Digital Asset Proceeds from Broker Transactions), which is being phased in:

- For 2025 transactions: only gross proceeds reported

- For 2026 transactions: full reporting including cost basis

The covered entities are centralized exchanges, hosted wallet providers, payment processors, and digital asset kiosks, namely businesses that take custody of customer assets. Major exchanges including Coinbase, Kraken, and Gemini began issuing 1099-DAs in early 2026.

What matters is what 1099-DA does not capture. IRS Notice 2024-57 temporarily excluded the following transactions from broker reporting obligations:

- Wrapping and unwrapping

- Liquidity provider transactions

- Staking transactions (including liquid staking and restaking)

Furthermore, the DeFi broker regulations announced in December 2024 were subsequently repealed via a joint resolution of Congress. This was the first cryptocurrency-related bill signed by the Trump administration and reflected a policy direction of not classifying DeFi front-ends as brokers. As a result, all transactions occurring on DEXs such as Uniswap, PancakeSwap, and 1inch, as well as on self-custody wallets, remain outside the IRS's direct reporting scope.

In the end, what is reported via 1099-DA covers only the basic transactions the IRS can automatically match. DeFi, self-custody wallets, and inter-exchange transfers fall under the taxpayer's own responsibility. Discrepancies between filings and 1099-DA figures trigger automatic balance-due notices and can lead to a tax audit.

4. Why Korea Has No Choice but to Adopt a Self-Reporting Based Model

4.1 The Inevitability of Self-Reporting

Korea faces the same infrastructural limitations as the United States. Even if the NTS gathers data from the five major domestic exchanges including Dunamu and Bithumb, the scope is fundamentally identical to what the US 1099-DA captures. That is, it is limited to transactions intermediated by centralized exchanges.

Transactions on overseas exchanges will be partially captured once CARF goes fully operational in 2027, but not all transactions will be automatically pulled in. DeFi transactions are not automatically captured by any information reporting system, and without the user's own filing, there is no way for the NTS to detect them automatically.

This structural limitation is a problem the United States has wrestled with for nearly a decade, and it is not one Korea can solve within a year. As a result, Korea, too, will inevitably begin with a dual structure of "exchange reporting plus self-reporting," with self-reporting likely playing a greater role than in the United States. A Korean version of an "Integrated Virtual Asset Analysis System" is currently being built under NTS leadership, but its feasibility is examined separately in Section 6.

4.2 CARF Adoption and the Pressure of Global Information Standards

CARF, which took effect on January 1, 2026, is an international standard jointly developed by the OECD and G20, with 48 countries participating. Korea signed the MCAA in November 2024 and will exchange data on 2026 transactions for the first time in 2027.

CARF goes beyond exchanging transaction data; it standardizes reporting items and classification criteria. Covered transactions include crypto-to-fiat exchanges, crypto-to-crypto exchanges, and crypto transfers (including retail payment transactions over USD 50,000). Reporting items include the asset name, annual transaction count, transaction unit count, and transaction value.

This classification framework is effectively compatible with the IRS's cryptocurrency classification system. Every CARF participant will end up receiving similar transaction data, and to apply this data to its domestic tax system, each country needs a compatible classification framework. Korea's NTS Integrated Analysis System is being developed in parallel with CARF-based information exchange functions, so it will naturally take a structure friendly to OECD and IRS standards.

4.3 Time Pressure

The NTS does not have the time, eight months before implementation, to precisely design independent tax guidelines for DeFi, staking, airdrops, hard forks, and NFTs respectively. This is also the central basis for the Korea Capital Market Institute's mention of a possible fourth deferral.

Under this time pressure, the most reasonable choice is to borrow the broad framework of an already-validated overseas model, particularly the US model. It is worth noting that Korean cryptocurrency exchanges have already begun aligning with this trend. Upbit formally implemented identity verification submission procedures under CARF compliance rules starting January 2026, while Coinone and Korbit partially revised their terms of use on the premise of CARF implementation. Bithumb is restructuring in a way that allows it to fulfill CARF obligations even without separate amendments to its terms.

5. The Likely Shape of Korea's Cryptocurrency Tax Regime

Assuming the US model serves as the broad reference point, Korean cryptocurrency taxation is likely to take shape category by category as outlined below. Because this must operate within the existing Income Tax Act's framework of other income (subject to separate taxation), it cannot be entirely identical to the US dual structure of ordinary income and capital gains.

- Spot Trading and Crypto-to-Crypto Exchanges: This is the codified area. The gain after subtracting the acquisition cost and incidental expenses from the transfer price is subject to 22% separate taxation. Unlike the United States, there is no short-term/long-term distinction, so the same rate applies regardless of holding period. This is more favorable than the US framework for traders who trade frequently in the short term.

- Staking and Lending Rewards: This is one of the murkiest areas. Since the current Income Tax Act defines crypto other income only as income arising from "transfer or lending," the prevailing interpretation is that the moment of receiving rewards is not in itself a taxable event. An NTS official also stated in a 2024 interview that "taxation is based not on the moment of receiving the staking service compensation, but on the moment the cryptocurrency received is transferred for KRW." This is the point of greatest divergence from the United States. Whereas the US uses a dual structure of taxing ordinary income at receipt and capital gains at sale, Korea is closer to single taxation at the point of transfer. Even within a single-taxation structure, however, calculating the acquisition cost of rewards is an additional issue. Treating receipt as a no-cost acquisition (with cost basis of zero) would render the entire sale price as taxable income, while applying the deemed necessary expense provision would recognize only 50% of the sale price as transfer income. Which approach prevails will need to be settled through enforcement decrees or further guidance. For lending, the scope of how the law's term "lending" is interpreted is a separate issue. If interest received from exchanges or DeFi lending protocols is captured under "income arising from lending," there could be room, unlike with staking, for a taxable event at the moment of receipt. Consistent application is feasible for exchange services, but DeFi protocols will largely depend on self-reporting.

- Airdrops and Hard Forks: There are no explicit standards. Unlike staking and lending, however, these involve a stronger element of gratuitous acquisition, providing reasonable grounds for differing treatment. If Korea maintains its current approach of taxing only on disposal, the most natural structure would be to treat the receipt of tokens as non-taxable, recognize the market value at receipt as the cost basis, and tax only the gain at the point of transfer. This treatment is more favorable for taxpayers compared to the United States. However, the single category of "airdrops" mixes activities with very different economic substance. Passive airdrops based on simply holding or locking up tokens are entirely different from active farming, where capital is intentionally consumed to obtain tokens. The UK's HMRC partially captures this distinction by treating airdrops with a service-like component as ordinary income while treating purely gratuitous receipts closer to non-taxable. If the two types are treated identically in Korea, the central issue will be whether to recognize incidental costs incurred by active farming users. If they are not recognized, the entire sale price of tokens acquired with capital expenditure becomes transfer income, which is at odds with substantive equity. Even if recognized, the method of substantiating those costs remains a practical challenge. Estimating the fair market value of obscure tokens received in self-custody wallets is a similarly common difficulty.

- DeFi: This is the area most likely to remain a gray zone. Given the NTS's response that it does not separately distinguish between centralized finance and DeFi, the position is effectively to apply general principles abstractly without separate DeFi-specific guidance. The conservative US approach may become the de facto standard in Korea as well, but without explicit guidance, taxpayer interpretations will inevitably vary. This also creates equity issues. Users performing the same economic activity on a domestic exchange are taxed precisely at 22%, while users doing the same activity through DeFi will either omit self-reporting, bear excessive tax under conservative interpretation, or carry the risk of potential back-tax assessment under aggressive interpretation.

- Token Sales and ICO Participation: As in the United States, the most reasonable structure is to first recognize transfer income on the disposal of cryptocurrency used to purchase tokens, and to set the cost basis of the received tokens at the market value at the time of purchase. Codified guidance to this effect, however, is currently absent.

- NFTs: The NTS previously stated that taxation criteria for NFTs are absent. It is unclear at the outset whether NFTs even fall within the definition of cryptocurrency, and even in the United States certain NFTs are classified as "collectibles" subject to 28% long-term capital gains tax, receiving separate treatment. How Korea will reflect this remains an issue to be addressed after implementation.

6. The Feasibility of Korea's Integrated Virtual Asset Analysis System

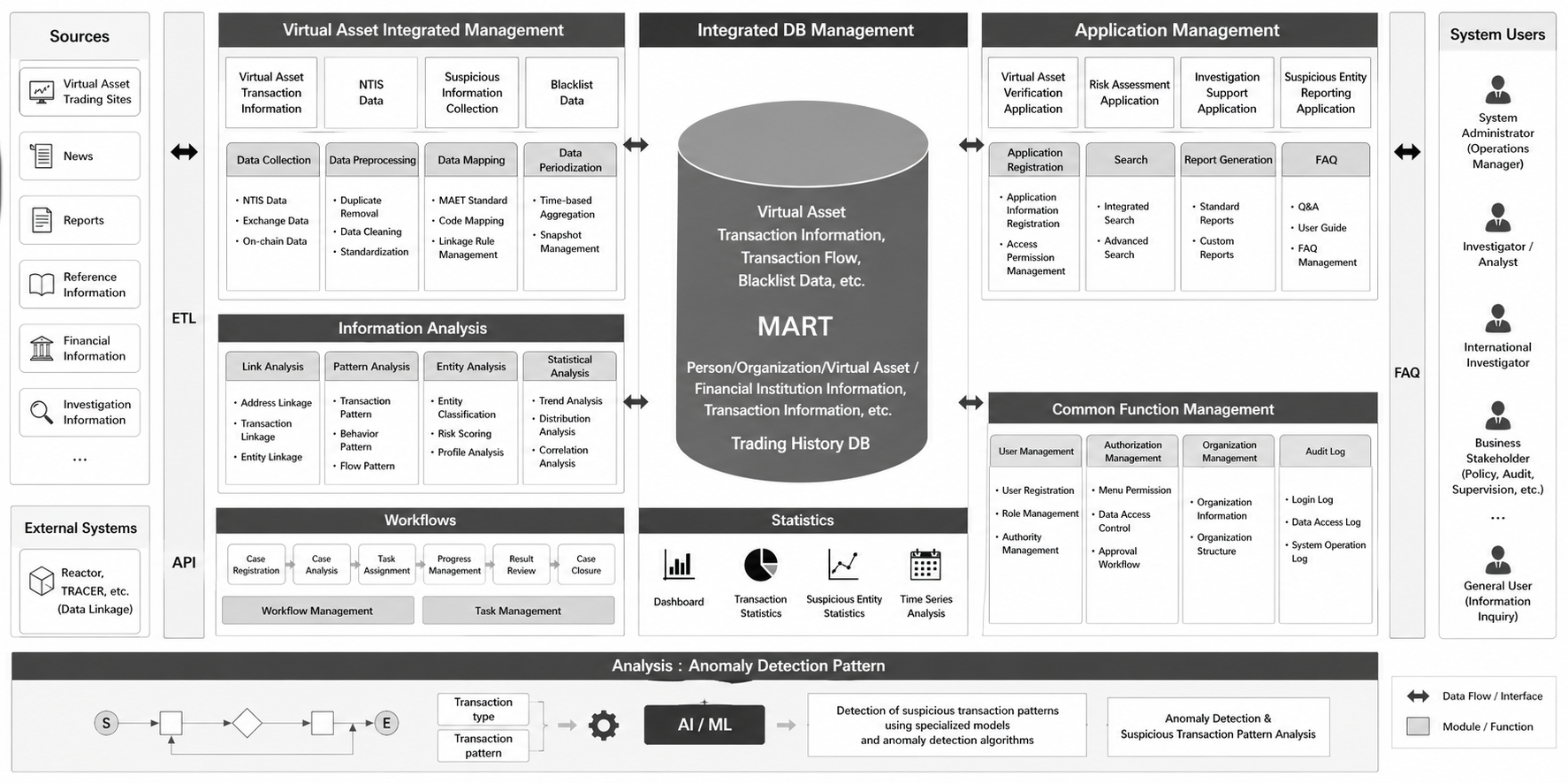

If category-by-category guideline gaps belong to the policy domain, whether the tools to actually enforce that policy are in place is a separate question. The detailed scope of the "Integrated Virtual Asset Analysis System" project currently underway offers a sense of what information the government intends to capture, and how far, in the course of taxing individuals.

Source: PPS (Reproduced Image)

According to the preliminary specifications disclosed on the PPS Nara Marketplace last March, the project budget is approximately KRW 3 billion including VAT. The schedule begins with design in April, pilot operation in November, and a formal launch by year-end. The project's scope goes well beyond simply compiling exchange data. Transaction statements and aggregate transaction tables submitted by virtual asset service providers will be combined with on-chain transaction data and managed in an integrated manner. Each taxpayer's wallet addresses will be matched so that transaction flows can be visually traced. Functions such as anomaly detection using AI machine learning and statistical methods, as well as combined analysis of wallet addresses identified as overseas financial accounts with on-chain transaction data, are also included. In its request for proposals, the NTS justified the project by stating, "Due to the anonymity and decentralized nature of virtual assets, problems are emerging in which they are misused as means for money laundering, irregular gifting, and offshore tax evasion," presenting the establishment of a foundation for proactive evasion detection as the rationale. The intent is not merely to receive data reported by exchanges after the fact, but to combine and proactively trace on-chain activity from self-custody wallets as well.

The challenge is technical and budgetary feasibility. Industry observers question whether a KRW 3 billion budget is sufficient to fully implement these features. Combining on-chain and off-chain data to comprehensively analyze overseas exchanges and personal wallets requires substantial infrastructure investment and external solution licensing costs. The schedule of about seven months from an April start to November pilot operation is also demanding. In particular, tracing DeFi transactions requires not just identifying wallet addresses but semantic analysis of on-chain transactions. For example, active farming, which consumes capital to mine tokens, must be distinguished from passive deposits, which makes it important to grasp the inherent meaning of transaction clusters.

These limits are also indirectly reflected in political moves during the same period. In February of this year, the National Assembly Budget Office posted a bid notice for a research project titled "Issues and Improvement Measures for Virtual Asset Taxation," and the request for proposals explicitly included a review of taxation criteria for non-standard acquisitions and transactions such as lending and staking. The very fact that an external research project on core taxation criteria began only eight months before implementation reveals the unsettled state of the current framework.

In all likelihood, the integrated analysis system at the time of January 2027 implementation will only have some of its intended functions in place. Standardized integration of exchange data and basic anomaly detection may be feasible, but covering semantic analysis of DeFi transactions and real-time matching of overseas exchange transactions will require additional time and budget. The fact that implementation begins with both the category-level guideline gaps examined earlier and the infrastructure gaps noted in this section unaddressed signals that the work after implementation will go beyond simple administrative refinement to take on a structural character.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.