Table of Contents

- Key Takeaways

- 1. Overview: From Branch-First to Mobile-First to Internet-First

- 2. Global Trends: The Crypto Neobank, Four Actions with Composability

- 2.1 Store: The Wallet as a Live Portfolio

- 2.2 Spend: One Balance, Multiple Rails

- 2.3 Grow: Institutional-Grade Yield, Opened to Everyone

- 2.4 Borrow: Instant, Overcollateralized (for now)

- 3. Opportunities in the Korean Market: Where an Internet-First, Tokenization-Native Neobank Will Emerge

- 3.1 How internet banking actually grew in Korea

- 3.2 Crypto neobank: A 4 plus year build, a real opportunity

Researcher

Key Takeaways

- Banking has shifted from branch-centered distribution to mobile-centered UX, and the next shift is toward internet-centered banking where the internet functions as a settlement layer for value.

- Crypto neobanks do not simply bypass the traditional financial system; they combine licensed financial institutions with on-chain primitives such as stablecoins, tokenized assets, staking, lending, and programmable wallets.

- The core advantage of internet-centered crypto neobanks is composability: the same on-chain balance can be used for custody, spending, yield generation, collateral, and borrowing within one integrated stack.

- Globally, crypto neobanks are rebuilding the four core banking functions of custody, spending, yield generation, and borrowing on top of stablecoins, tokenized assets, DeFi protocols, and traditional payment networks.

- In Korea, the most realistic crypto neobank opportunity will likely emerge from internet banks, exchanges, or securities firms that can combine regulatory licenses, large user distribution, tokenized assets, stablecoin settlement, and on-chain product infrastructure.

This article is adapted from "Korean Blockchain Guidebook for Institutions 2026," jointly published by Four Pillars and Pantera Capital. The full report covers 14 more themes for companies and institutional investors.

1. Overview: From Branch-First to Mobile-First to Internet-First

Banking has been structurally reshaped twice in a century, and each shift was defined by the medium through which users interact with the bank. First it was the branch, then the smartphone. The next medium is the internet itself, not as a channel, but as the settlement layer. That shift is what turns a "mobile-first neobank" into an "internet-first crypto neobank."

The three eras can be summarized as follows:

- Branch-first banks: physical distribution, business-hours settlement. KB, Shinhan, JPMorgan.

- Mobile-first neobanks: smartphone-native UX built on legacy rails (ACH, SWIFT, Visa). Still the fastest-growing category in most markets. Revolut, Chime, Nubank, Toss, Kakaobank.

- Internet-first crypto neobanks: an emerging category that moves value the way the internet already moves information: globally, 24/7, and programmably. Anchorage, Circle, Figure, EtherFi Cash, Kast, Phantom.

The crucial difference is where the innovation happens. Mobile-first neobanks modernized the frontend, but the backend remained a partner bank and card rails. Internet-first crypto neobanks try to change the backend as well. They feel internet-first for two reasons.

First is accessibility. A stablecoin and tokenized asset balance can move globally, settle 24/7, and work across apps without requiring a bank account in each jurisdiction.

Second is composability. The same onchain balance can be stored, spent, lent, staked, or posted as collateral in one session, because the products share a settlement layer. Stablecoins, lending pools, staking vaults, and perps all interoperate, so store, spend, grow, and borrow can live on a single programmable balance rather than four disconnected silos. However, the category is still young, and questions around risk, consumer protection, and reliability remain open.

The other thing worth understanding is that crypto neobanks are not routing around the legacy system. They are integrating with it.

- U.S. charters and licenses: Anchorage (OCC national trust); Paxos, Fidelity Digital Assets (trust charters); Circle (national trust bank charter application, 2025); Ripple and Kraken on charter pathways; Figure and SoFi already chartered and running onchain products.

- Hybrid plumbing: Visa/Mastercard USDC settlement, Stripe/Bridge and Rain as issuer-processors, BaaS partners (Lead Bank, Cross River), USDC reserves held at BNY Mellon, tokenized MMFs (BUIDL, BENJI).

The realistic architecture is a dual stack. Chartered entities sit on one side, onchain primitives sit on the other, and the user experience stitches them together.

Where the potential unlock sits is simple. The smartphone unlocked mobile-first neobanks. The internet itself, as a settlement layer, is the unlock being tested for internet-first crypto neobanks. Whether it delivers depends less on "crypto vs. banks" than on how quickly onchain primitives and chartered institutions converge into a single stack.

2. Global Trends: The Crypto Neobank, Four Actions with Composability

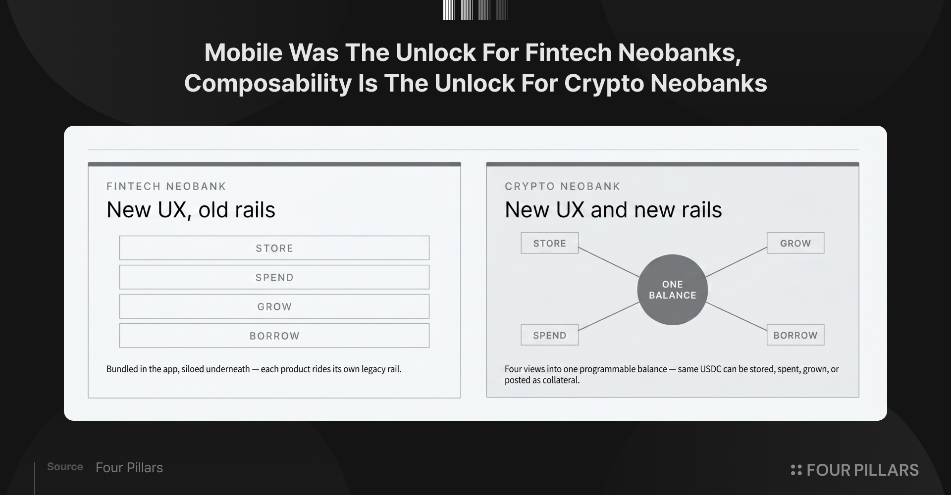

Every bank, in every era, lets a user do four things with an asset: store it, spend it, grow it, and borrow against it. Internet-first crypto neobanks keep those same four actions but reimplement each one on onchain rails that interoperate with the legacy system rather than replace it.

Two properties distinguish this new stack from mobile-first neobanks:

- Same balance across all four actions. Stablecoins, LSTs, vault shares, and tokenized T-bills are fungible tokens that can be used interchangeably as savings, collateral, yield, or payment. The stack compounds instead of fragmenting into siloed products.

- Dual-stack integration with legacy finance. Onchain primitives are increasingly fed and backstopped by regulated entities: USDC reserves sit at BNY Mellon, tokenized T-bills (BUIDL, BENJI) are issued under existing securities law, and card-rail processors (Visa, Mastercard, Stripe/Bridge) now settle in stablecoins directly. The onchain side is not an island; it is a new layer bolted onto the existing banking system.

Source: Building Permissionless Neobanks | Pantera

2.1 Store: The Wallet as a Live Portfolio

In a mobile-first neobank, a user balance is a database row at a partner bank. In an internet-first crypto neobank, a wallet is a live connection to every asset, protocol, and application onchain, with self-custody as the default. The same USDC in that wallet can be spent, lent, staked, or posted as collateral without moving between institutions or waiting for T+1/T+2 settlement.

The deeper shift is that a crypto neobank is not just about holding money, it is about holding every asset class in a single, tradable balance.

It has one balance, for every asset class. Stocks, bonds, cash, funds, commodities, and crypto can sit side-by-side in a single wallet, each represented as a token that can be swapped, posted as collateral, or redeemed 24/7. Tokenized equities (Ondo Global Markets, Dinari), tokenized T-bills and MMFs (BUIDL, BENJI, USDY), stablecoins, and LSTs all live on the same rails.

Rebalancing a portfolio moving from cash to treasuries to equities, or pledging any of them as collateral becomes a single onchain transaction instead of a multi-account, multi-broker workflow. This is a structural break from previous era.

2.2 Spend: One Balance, Multiple Rails

Mobile-first neobanks ride traditional rails: they pay interchange fees, absorb FX spreads, and live with multi-day cross-border settlement. Internet-first crypto neobanks split the spend problem into two horizons: a short-term bridge on top of traditional rails, and a longer-term to stablecoin-native payments.

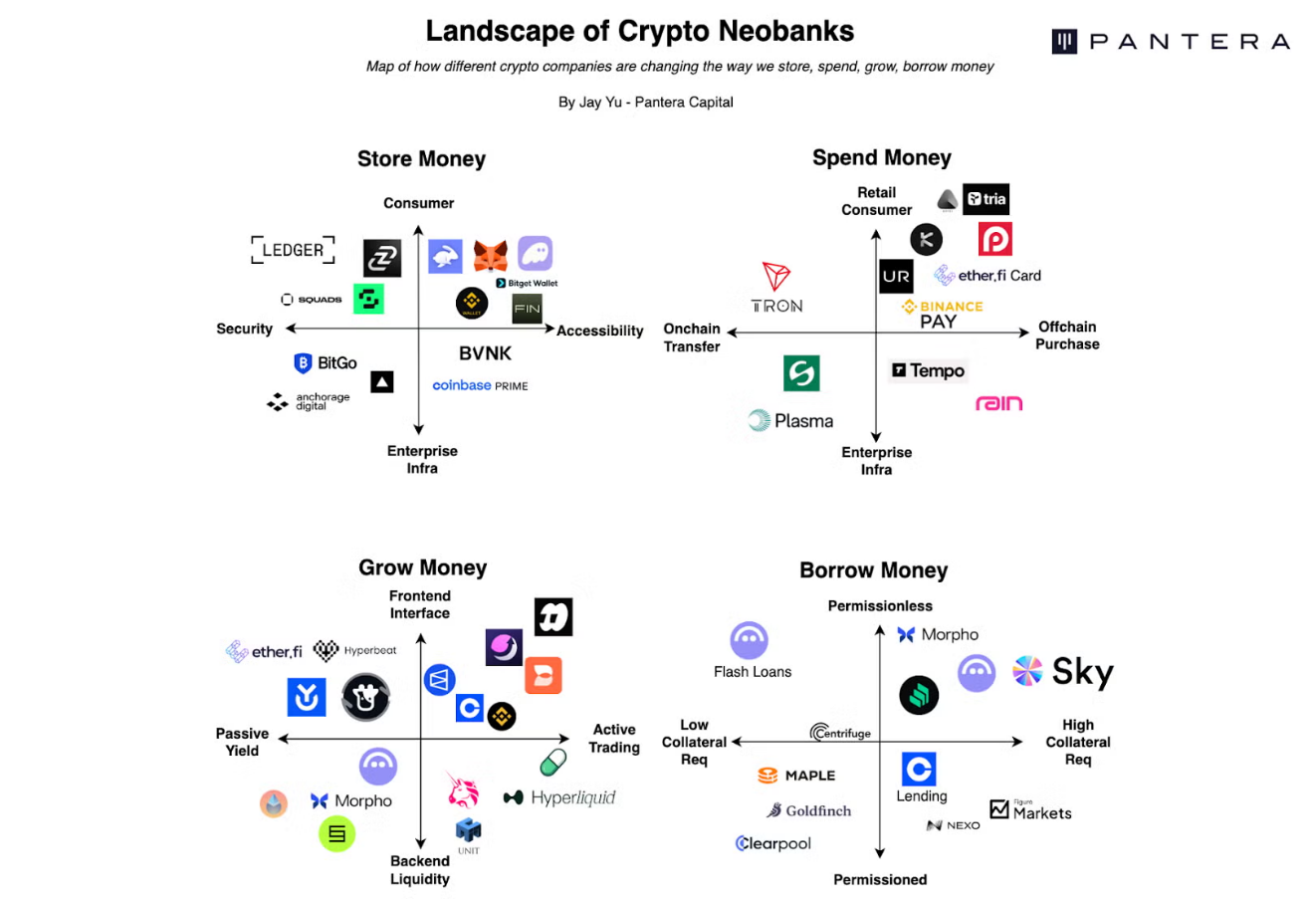

In the short term, the dominant pattern is card-rail bridges. Crypto spend apps like Kast, Tria, Redotpay, EtherFi Cash, and Gnosis Pay plug yield-bearing balances into existing card networks, so users can spend balances anywhere Visa is accepted. Stripe's acquisition of Bridge and the rise of Rain as an issuer-processor show how deeply stablecoins are now integrated into legacy card plumbing the "crypto" side is quietly becoming the settlement layer behind familiar plastic.

In the medium term, payments move toward stablecoin-native rails that bypass Visa entirely. QR-based stablecoin payments, such as Bitget Wallet's merchant pilots across Indonesia, Brazil, and Vietnam, and stablecoin-optimized chains like Tempo, Plasma, and Stable point toward a world where merchants accept stablecoins directly. The benchmark is already here: Tron settles 25–30% of global stablecoin volume and 99% of revenue is from this settlement, mostly in emerging markets where dollar access matters more than brand familiarity.

The composability point ties all of this back to the broader thesis: the "spend" balance, the "grow" balance, and the "collateral" balance are the same balance.

2.3 Grow: Institutional-Grade Yield, Opened to Everyone

The real unlock on the yield side is access, not APY. Internet-first crypto neobanks expose strategies that used to sit behind hedge funds, prime brokers, and private banks: now available to any wallet with $10. Minimums collapse from $100K–$1M to $1; geographic gating collapses from "U.S. accredited only" to "anyone with a wallet." For the first time in banking history, the yield side of the balance sheet is structurally more open than the deposit side.

The strategies that were previously accreditation-gated now look like this:

- Ethena (sUSDe / USDe): a delta-neutral basis trade (long spot ETH/BTC, short perps) that used to live inside hedge funds and prop desks, packaged as a yield-bearing stablecoin that captures the funding-rate spread.

- Tokenized T-bills & MMFs (BlackRock BUIDL, Ondo USDY, Superstate USTB, Franklin BENJI): U.S. treasury yield that used to require a brokerage account, minimums, and the right geography, now a globally accessible onchain token.

2.4 Borrow: Instant, Overcollateralized (for now)

Traditional lending is gated by credit bureaus, KYC, and geography. **Morpho, Aave, and Spark** replace that gating with code: deposit collateral, borrow against it which is 24/7, globally, permissionlessly. The tradeoff is overcollateralization, because a chain doesn't know your FICO score. But even within that constraint, the model starts to differentiate from legacy: collateral can be productive. Yield-bearing tokens (weETH, sUSDe, USDY, LRTs) keep earning yield while posted, which automatically offsets some or all of the interest owed on the loan: an idea traditional banks cannot express in their product stack.

The unsolved frontier is undercollateralized consumer credit. Three paths are being built toward it:

- Smart collateral management against yield-bearing assets with real-time LTV.

- Identity + credit primitives: Worldcoin, zk credit attestations (e.g., 3Jane), and onchain reputation layers (Coinbase Verifications).

- Hybrid underwriting: chartered partners running traditional underwriting on top of onchain settlement. Figure’s HELOC on Provenance is the live example: the loan is originated and serviced under normal legal/consumer-credit rails, while the loan record and ownership trail are represented onchain to streamline funding, transfer, and securitization.

On the institutional side, Maple, Clearpool, Goldfinch, and Centrifuge are building undercollateralized pools for institutional borrowers backed by offchain legal claims: a direct bridge between DeFi and private credit.

3. Opportunities in the Korean Market: Where an Internet-First, Tokenization-Native Neobank Will Emerge

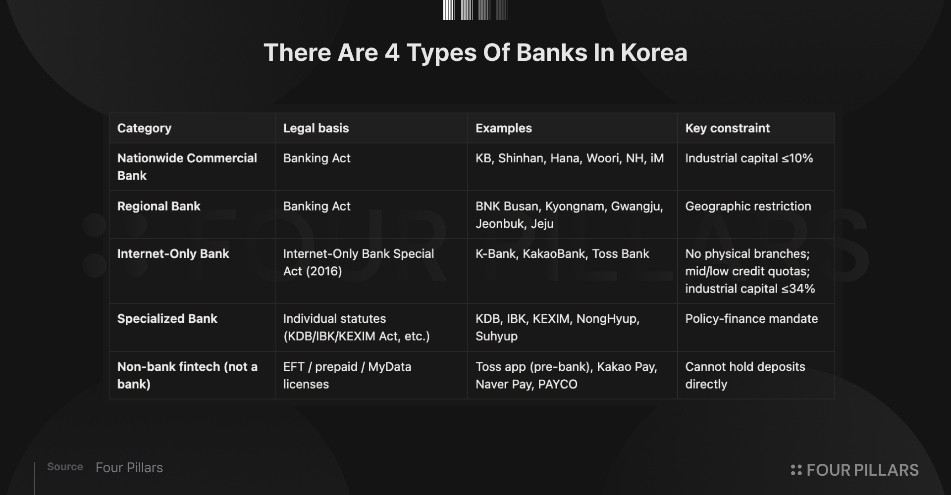

Korea does not have a "neobank" legal category the way the EU, UK, or Australia do. Instead, it has a bank license structure with a carve-out for internet-only banks. Korean banking licenses fall into four tiers, plus a non-bank fintech layer that cannot hold deposits directly.

The key nuance is that internet-only banks receive the same banking license as commercial banks. They are not a lighter-touch category. They are a sub-category of commercial banks operating under a special act.

3.1 How internet banking actually grew in Korea

The FSC and FSS deliberately did not create a lighter neobank tier. Instead, they opened the existing commercial banking license to digital-first players via a targeted special act in 2016. That single legal choice set the trajectory for everything that followed. K-Bank, KakaoBank, and Toss Bank then grew on four reinforcing levers:

- Industrial-capital exemption. Allowed big-tech and telco anchors (Kakao, KT, Viva Republica) to take control and distribute through their existing super-apps.

- Distribution via captive user bases. KakaoTalk, the Toss app, and KT provided zero-CAC onboarding at national scale. K-Bank in particular grew by being the banking partner for Upbit, which gave it an exchange-sized user funnel no other bank could match.

- Mandatory mid-to-low credit lending. A regulatory requirement that doubled as the core margin product.

- Branchless cost structure. A lower cost-to-serve enabled aggressive deposit and loan pricing relative to incumbents.

The result was decisive: internet-only banks went from zero to tens of millions of users and captured a meaningful share of new account openings in under a decade.

3.2 Crypto neobank: A 4 plus year build, a real opportunity

Three forces are converging that make a Korean crypto neobank a credible next opportunity, but due to regulatory uncertainty, I think will take at least 4 years.

First, the regulatory ground is shifting toward tokenization. The new STO and RWA legislation passed in January 2026 legitimizes onchain issuance and custody of securities and real-world assets. Banks and securities firms are now incentivized to build tokenization rails, but most efforts still lack a consumer-grade, composable front end. In parallel, KRW stablecoin policy is moving forward.

Second, Korea’s internet-bank playbook composes naturally with crypto primitives. The levers that made internet-only banks win still apply: captive distribution, branchless cost structure, and a regulated wedge. Crypto adds capabilities they cannot express on legacy rails: 24/7 settlement, onchain yield, tokenized assets as native products, and programmable collateral. The same four banking actions, store, spend, grow, and borrow, can be rebuilt on KRW stablecoins, tokenized RWAs, and DeFi primitives.

The likely builders are visible, but each starts with a different advantage and a different gap.

- Internet-only banks (K-Bank, KakaoBank, Toss Bank) are closest to the end state. They already have licenses, compliance, and mass distribution. The missing layer is an onchain product stack that is both compelling and containable: tokenization rails, stablecoin settlement, and regulated access to onchain yield and collateral.

- Exchanges (Upbit, Bithumb) start with crypto-native users, liquidity, custody, and shipping speed. The gating item is regulatory and structural. They need a bank partnership, or a pathway to bank-like permissioning, to become the primary KRW account for mainstream users.

- Securities firms pursuing STO can become the tokenization factory. They can issue and distribute tokenized equities, funds, and credit under the new regime. In fact, firms like Mirae Asset and Hanwha are moving to enable trading of tokenized securities through a single interface via their overseas subsidiaries. Their gap is a neobank wrapper that combines deposits, payments, and a default wallet.

The winner will look less like a standalone wallet and more like the next iteration of the internet-bank playbook. It will start from distribution and a regulated wedge, then expand into wealth and credit. The difference is that the balance sheet is programmable, 24/7, and global by default.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![Blockchain, the Rail for Everything [FP Weekly 28]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F43cg86mr8ytpg1.png&w=1920&q=75)

![License Is All You Need [FP Weekly 27]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Ft4v9kemqys40d1.png&w=1920&q=75)