Table of Contents

Researcher

Key Takeaways

- On July 1, 2026, Robinhood held an event in London called “Robinhood Presents: The World is Flat” and announced a series of major updates. The news that attracted the most attention was the mainnet launch of Robinhood Chain, but taking a closer look at the news around tokenized stocks reveals some interesting insights.

- Robinhood renamed its existing service offered through its European entity, Stock Tokens, to Classic Stock Tokens, and launched a new Stock Tokens service. The two are similar in that they tokenize stocks with 1:1 backing, but they differ across every dimension, including tokenization structure, jurisdictional authorities, and regulatory frameworks. As a result, they show very different characteristics in functional terms, such as investor accessibility and onchain composability.

- This article provides an in-depth analysis of how Classic Stock Tokens and Stock Tokens differ, and uses that analysis to examine the direction Robinhood aims to take.

1. The World is Flat

Yesterday, July 1, 2026, Robinhood held an event in London called “Robinhood Presents: The World is Flat” and announced a series of major updates:

- Official mainnet launch of Robinhood Chain: Robinhood launched the mainnet of Robinhood Chain, an RWA-focused chain built using Arbitrum’s technology stack. From Day 1, it onboarded major dApps such as Uniswap, LayerZero, Morpho, 1inch, and dYdX.

- Support for the new Stock Tokens in Robinhood Wallet: New Stock Tokens were launched and made available in more than 120 countries, and can be used in Robinhood Wallet and on Robinhood Chain.

- Launch of Robinhood Earn: A lending product offering approximately 7% APY will be launched for U.S. investors. It operates based on Morpho on Robinhood Chain. The product is protected by insurance through Lloyd’s of London and RELM.

- Integration with Lighter: Users in eligible jurisdictions can access Lighter’s perpetual futures functionality inside Robinhood Wallet.

- Expansion of perpetual futures trading in the EU: In the EU region, Robinhood is expanding beyond crypto futures to offer perpetual futures trading based on traditional financial assets such as gold, silver, stocks, and crude oil.

- Maker/taker fee structure for professional traders: For professional traders in the U.S., Robinhood is introducing a maker/taker fee structure that becomes more favorable depending on trading volume.

- Launch of crypto trading services in Canada: Robinhood acquired Canada’s WonderFi and officially launched crypto trading services based on that acquisition.

- Acquisition of Singapore MAS Capital Markets Services license: Robinhood Singapore announced that it had received a capital markets services license from MAS, laying the groundwork to provide brokerage services to Singapore customers in the future.

- Planned launch of crypto trading services in the UK: Robinhood already operates a stock investing platform in the UK and plans to expand into crypto trading services soon.

- Expansion of agentic trading technology into crypto: Robinhood announced agentic trading for stocks and options in the U.S. last month, and plans to expand this feature into crypto.

As the event name suggests, these announcements demonstrate Robinhood’s vision of lowering barriers to entry created by countries, asset classes, time zones, and more, so that anyone can access global financial markets.

2. Everyone Is Only Talking About the Robinhood Chain Launch

There were many major announcements, but the news that undoubtedly received the most attention from the crypto community was the mainnet launch of Robinhood Chain. Just as Coinbase launched the Base network to expand its crypto ecosystem onchain, Robinhood has likewise launched Robinhood Chain.

Base network generated approximately $78M in sequencer revenue last year and has already achieved considerable commercial success by building successful ecosystems across trading, AI agents, DeFi, and more. For that reason, it was only natural that people’s attention during Robinhood’s The World is Flat keynote would focus on Robinhood Chain.

Robinhood Chain is an Ethereum Layer 2 network developed using the Arbitrum technology stack. It aims to serve as onchain financial infrastructure for running tokenized stocks, ETFs, private credit, RWAs, DeFi, and AI agent-based financial applications within the Robinhood ecosystem.

Source: Robinhood

In fact, if we look at the Robinhood Chain docs, there is a separate Stock Tokens section, and the page showing key token contracts also lists the contract addresses of Stock Tokens. This makes it clear that the main purpose of Robinhood Chain is to build an on-chain ecosystem centered around Robinhood’s own Stock Tokens service.

But wait for a moment. Wasn’t Robinhood already offering a Stock Tokens service before this? Robinhood had already been offering Stock Tokens on the Arbitrum network before the Robinhood Chain mainnet launch. According to rwa.xyz, there are currently 1,888 types of Stock Tokens on the Arbitrum network, with a total value of $19.4M.

So what exactly are the new Stock Tokens introduced in this announcement? Are they simply a migration of the Stock Tokens that previously existed on Arbitrum? Or are they a new product altogether?

3. Robinhood’s “New” Tokenized Stock Playbook

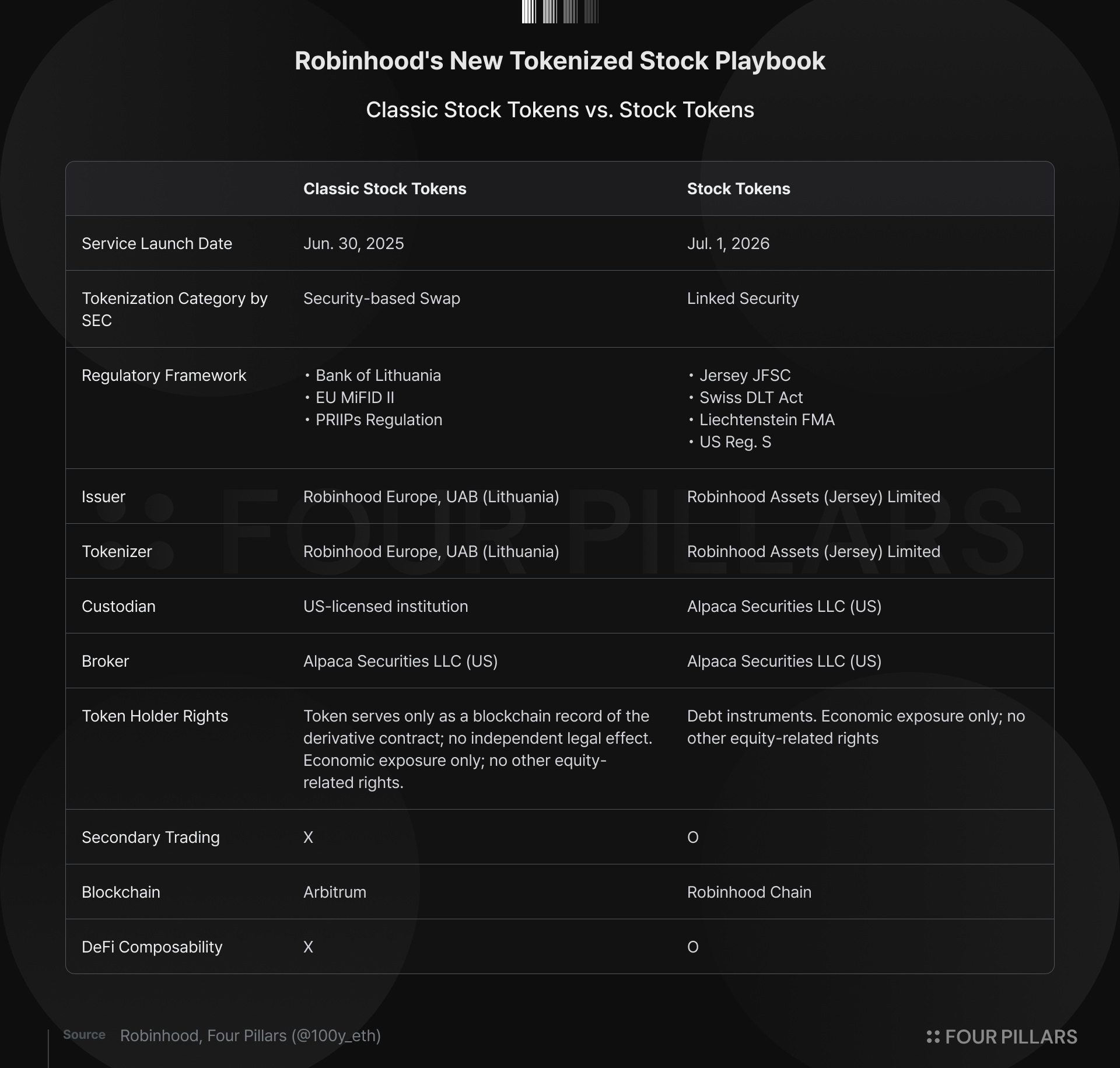

To start with the conclusion, the existing Stock Tokens and the Stock Tokens announced yesterday may share the same vision, but they are completely different services. In fact, the existing Stock Tokens service offered in the EU has been renamed to Classic Stock Tokens in the terms and conditions, while the newly announced service has taken the name Stock Tokens.

Understanding the background and differences between these two is the key.

3.1 Classic Stock Tokens

Classic Stock Tokens is a service launched on June 30, 2025 and offered by Robinhood Europe to EU users.

The tokenization process works as follows:

- An investor purchases a Stock Token through the Robinhood EU app.

- This means the investor enters into a financial derivative contract with Robinhood EU under the EU MiFID II classification, and the token serves as a representation of rights and a book-entry record for that contract.

- At the same time as Robinhood EU enters into the derivative contract with the investor, it purchases the underlying asset through a U.S. broker in order to hedge the risk of price fluctuations.

In other words, simply put, the existing Classic Stock Tokens are not tokenized stocks themselves. Rather, they are closer to a representation of rights and book-entry record on the Arbitrum network for a derivative contract that gives investors exposure to returns based on stock prices. Put differently, tokenization is merely an auxiliary mechanism, while the core is the derivative contract between the investor and Robinhood EU.

Therefore, even if an investor holds Classic Stock Tokens, they do not own the shares and do not have rights such as voting rights or claims. The source of legal enforceability is not the token, but the derivative contract between the customer and Robinhood EU. The investor’s rights are limited solely to the difference between the purchase price of the derivative contract and the underlying asset price at liquidation, as well as any dividends that arise.

Looking briefly at the operational structure, the entity that is party to the derivative contract and issues the tokens is Robinhood Europe, UAB, a Lithuanian entity. It is a financial brokerage firm, crypto-asset service provider, and payment institution authorized and supervised by the Bank of Lithuania. At the same time as Robinhood EU enters into the derivative contract with the investor, it sources the shares through Alpaca Securities LLC, a U.S.-based broker, and holds them with a U.S. custody institution.

Because of this structure, the existing Classic Stock Tokens service is a half-tokenization model. The core is ultimately the derivative contract between EU investors and Robinhood, while the token merely serves as a book-entry record without legal enforceability. For this reason, Classic Stock Tokens cannot be freely circulated on-chain, can only be offered to European customers, and can only be traded within the Robinhood app.

3.2 Stock Tokens

The Stock Tokens launched on July 1, 2026 are completely different from Classic Stock Tokens in terms of tokenization structure and usage.

They are accessible to customers in more than 120 countries, can be traded 24/7 outside the Robinhood app within the Robinhood Chain ecosystem, and can even be used in DeFi protocols such as Uniswap and Morpho. Compared with the existing Classic Stock Tokens, which were a half-tokenization model and could only be traded within the Robinhood EU app, this is an entirely different service. How is this possible?

At a primary level, the stock tokenization process works as follows:

- Bitstamp Global Ltd, participating as an AP, can take part in the primary issuance and redemption of tokenized stocks. If the AP wants to issue Stock Tokens, it transfers funds to Robinhood Assets (JE) Limited, a Jersey-based entity.

- Robinhood Assets (JE) Limited obtains the shares from Alpaca Securities, a U.S. broker and custodian, and holds them in custody.

- At the same time, Robinhood Assets (JE) Limited issues tokens representing the shares and delivers them to the AP, after which they are traded in the secondary market.

In other words, the new Stock Tokens are the same as Classic Stock Tokens in the sense that they secure the underlying shares and are backed 1:1. However, differences arise because the contractual form and tokenization structure are different. What Classic Stock Tokens represent is a derivative contract between investors and Robinhood, while what Stock Tokens represent is a debt instrument between investors and Robinhood.

There are broadly four regulatory frameworks under which Stock Tokens tokenize stocks.

- First, Robinhood Assets (JE) Limited, the issuer of the debt securities and the entity carrying out the tokenization, follows Jersey regulations. As of now, it is not under full regulation, but Robinhood explains that it has received certain consent from the Jersey financial authorities in relation to the issuance of Stock Tokens.

- Second, Stock Tokens are not actual shares, but debt instruments. They provide only economic exposure to the underlying stocks or ETFs and do not provide any other rights. The Base Prospectus has been approved by the Liechtenstein FMA, thereby establishing the regulatory conditions to sell these securities in the EU/EEA region.

- Third, Stock Tokens follow Reg. S in order to create an offshore securities offering structure that avoids registration under U.S. securities laws. Stock Tokens cannot be offered or sold within the United States or to U.S. persons, and are offered offshore.

- Finally, Stock Tokens follow the Swiss DLT Act. As a result, holders of the tokens can have rights under the debt securities.

For these reasons, the Stock Tokens announced by Robinhood this time target a broader investor base than the existing Classic Stock Tokens, can be used on-chain, and have clearer legal effect.

4. There Are Still Limitations

However, there are still limitations.

- Stock Tokens still cannot be offered to U.S. investors.

- Holders of Stock Tokens only have economic exposure and do not have rights such as voting rights or claims.

- Liquidity may become fragmented. Representative platforms that tokenize stocks in a similar way to Stock Tokens include Backed Finance’s xStocks and Ondo Global Markets. Even if the underlying stock is the same, if the tokenization platform is different, the tokens are not compatible, which ultimately causes liquidity fragmentation.

Among other methods of tokenizing stocks, issuer-sponsored tokenization solves this problem. This is a method in which the issuing company or transfer agent directly tokenizes the shares. It can comply with existing securities laws, serve U.S. persons, tokenize all rights associated with the shares, and avoid liquidity fragmentation because it tokenizes shares that have the same CUSIP as the existing shares. A representative example is Securitize. However, because this method must comply with regulations, there are constraints on permissionless on-chain trading or use within DeFi protocols.

5. The North Star Is Set

The North Star of all financial platforms is already set. It is to build a platform where anyone can trade every type of asset, anytime and anywhere, whether crypto, stocks, commodities, bonds, or anything else. Whether it is Coinbase, which started as a crypto exchange, or Robinhood, which started with stock trading, all platforms are moving toward this North Star.

From this perspective, Robinhood’s newly announced Stock Tokens can be seen as a step-up from its existing Classic Stock Tokens service. Stocks that could previously only be traded inside the app now have the foundation to be freely used within the DeFi ecosystem on Robinhood Chain.

However, this is also a transitional model. It is not the stock itself that has been tokenized. Rather, it is an indirect method in which a third party tokenizes stocks in the form of debt securities. Still, given that the SEC is recently preparing exemptions related to stock tokenization and Coinbase has previewed a tokenized stock service, this appears to be a model that can continue operating within a range where appropriate innovation is possible.

All platforms are moving toward the North Star in their own ways within the limits currently permitted by regulation. The leaders here are Robinhood and Coinbase, and we should watch what kinds of playbooks various financial platforms in different countries will unfold next.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![License Is All You Need [FP Weekly 27]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Ft4v9kemqys40d1.png&w=1920&q=75)

![MSTR and COIN [FP Weekly 26]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F6ivhjsmqq8e3w1.png&w=1920&q=75)

![Signals from Wall Street and Japan's Securities Industry to the Crypto Market [FP Weekly 25]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fuh58gemqes9azi.png&w=1920&q=75)