Table of Contents

Researcher

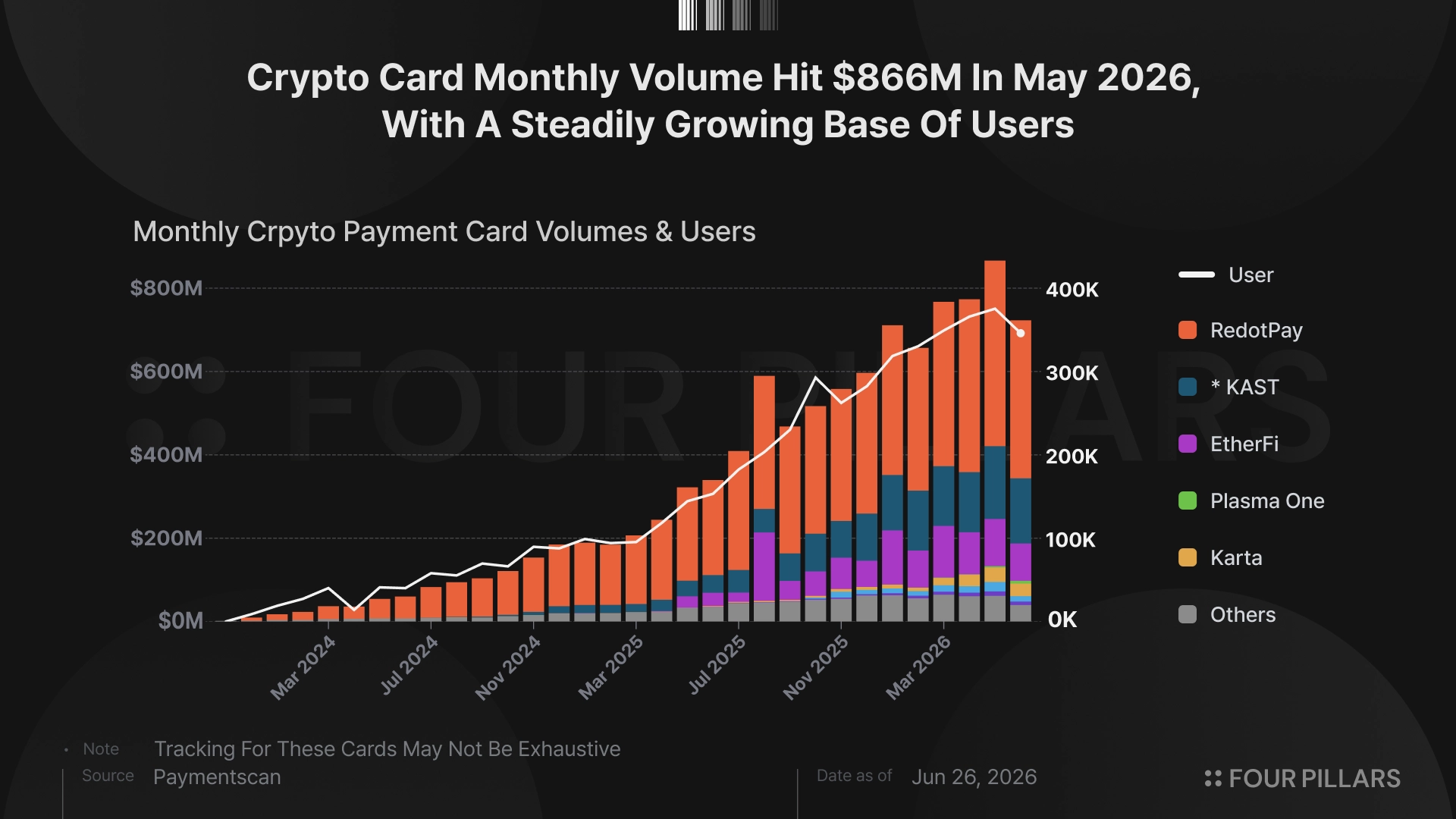

Crypto cards are gaining traction

According to Paymentscan (@Paymentscan), monthly crypto card payment volume rose from about $271 million in May 2025 to about $656 million in May 2026, more than doubling in one year. Cumulative volume has exceeded $7.8 billion. The category has continued to grow despite the bear market.

What drove this growth? The commonly cited factors are clearer stablecoin regulation, Visa’s integration of stablecoin settlement, and reward programs. With the GENIUS Act in July 2025, stablecoins were recognized as an institutional payment rail, and their market capitalization grew by about 49% ($205 billion to $306 billion). Visa also adopted stablecoins directly as a settlement rail, rather than treating them only as an on-ramp tool. This made it easier for crypto projects to issue cards and led to clear improvements in UX. Aggressive reward programs also gave users a sufficient incentive.

These factors matter. But a closer look at the chart shows that one project is processing most of the card volume. That project is RedotPay (@RedotPay). When we examine how RedotPay captured most of the market share, its strategy becomes clear.

The simple answer: RedotPay targeted emerging markets

RedotPay processed more than $2.95 billion in card volume in 2025. That was more than four times the combined volume of the other 13 competitors. How did it produce this level of growth? The answer is simple. It targeted emerging markets.

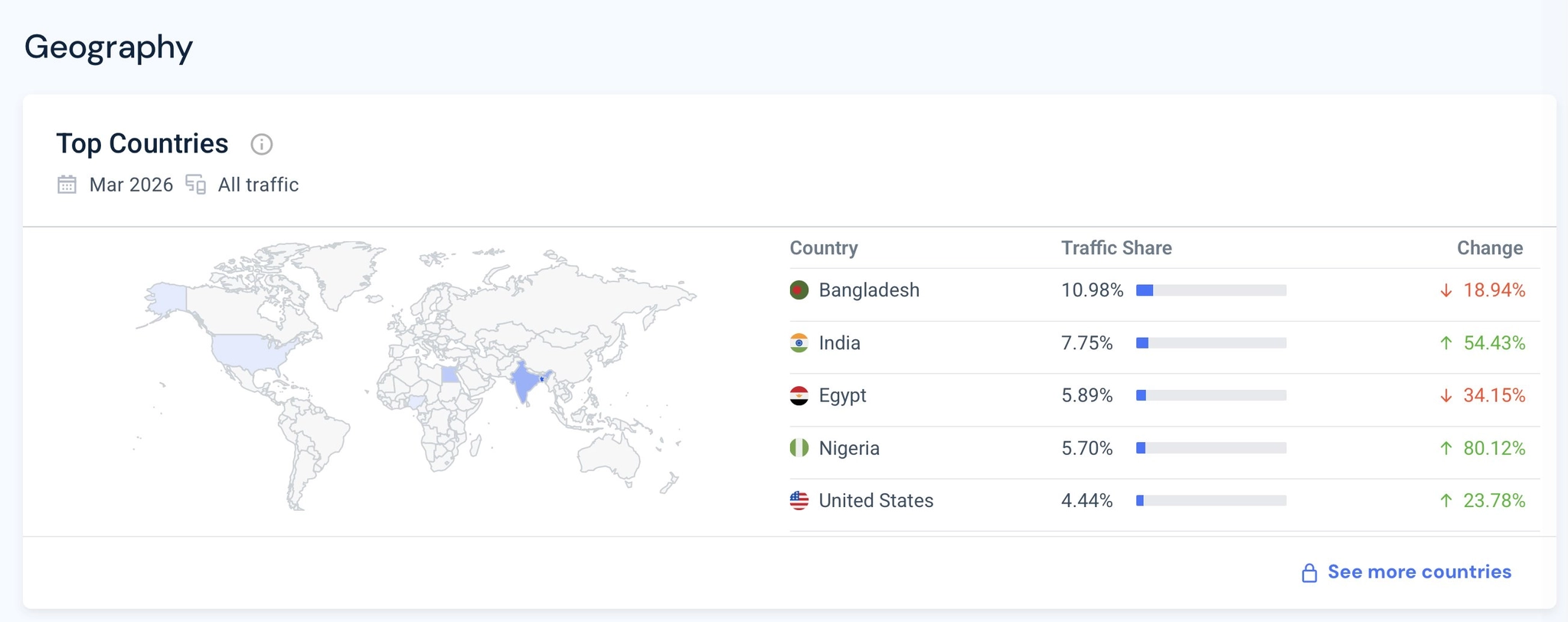

More specifically, RedotPay brought crypto cards to markets where they solve real problems. Rather than focusing on countries with well-developed payment infrastructure, it focused on emerging markets where local currencies are unstable. Traffic data supports this view:

Source: X (@stacy_muur)

- Bangladesh: 10.98%

- India: 7.75%

- Egypt: 5.89%

- Nigeria: 5.70% of site traffic

- The United States: only 4.44%

Source: X(@stacy_muur)

This is because crypto cards have clearer PMF in emerging markets. In these countries, there is structural demand for dollar-pegged assets that can protect against local currency depreciation. Stablecoins also offer lower remittance costs, which naturally increased interest. In this context, demand for crypto cards grew because users could spend stablecoins directly without going through a cumbersome off-ramp process.

RedotPay’s strategy was aligned with this demand. According to public analysis, RedotPay used local crypto traders, KOLs, and OTC networks as agents to build offline viral channels. It also used a commission structure tied to card activation, which helped it reach users with actual demand. This was not online performance marketing. It was a distribution strategy suited to markets where trust travels through local networks.

At the same time, RedotPay actively used existing card rails on the UX side. In February 2025, RedotPay worked with StraitsX and Visa to launch a digital asset-based card program in Singapore. StraitsX participated as a Visa BIN sponsor, allowing users to spend digital assets across Visa’s merchant network.

We should treat RedotPay’s strategy as a useful lesson.

How should crypto approach agentic commerce?

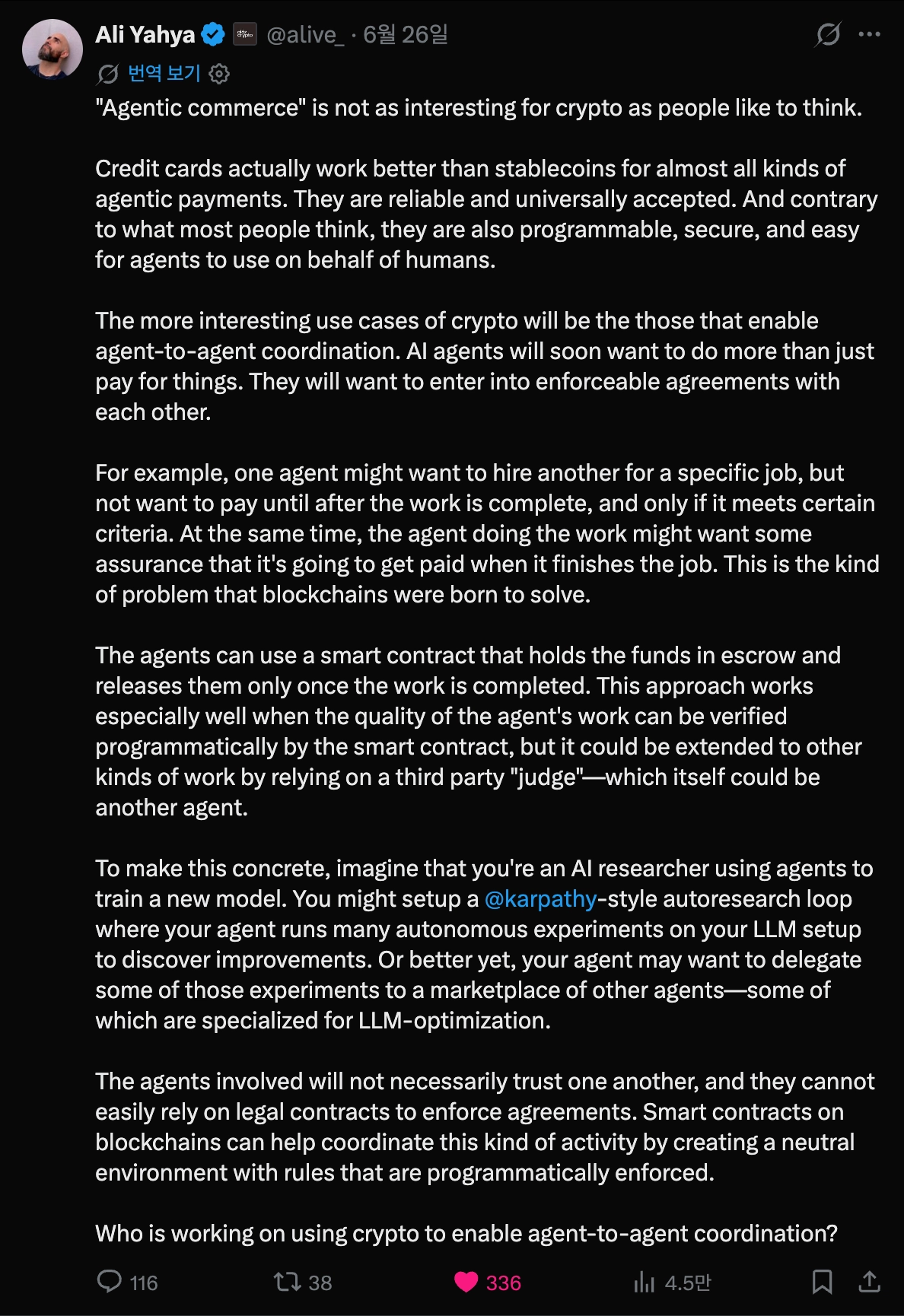

Source: X(@alive_)

Ali Yahya (@alive_) of a16z recently argued that “agentic commerce may not be as interesting for crypto as people think.” In particular, he argued that credit cards may work better than stablecoins for ordinary agent payments. He also argued that crypto is stronger in coordination between agents that do not trust each other, meaning escrow-based contract structures with enforceable terms.

There is much to agree with in this view. Card networks are not simple payment tools. They are trust infrastructure that combines merchant acceptance, consumer protection, fraud prevention, settlement, and regulatory compliance. In existing consumer payments, it is not easy for crypto to surpass this level of trust and stability head-on.

Traditional card companies also already have strong fee-based revenue pipelines. They are unlikely to voluntarily give up a working revenue structure to crypto.

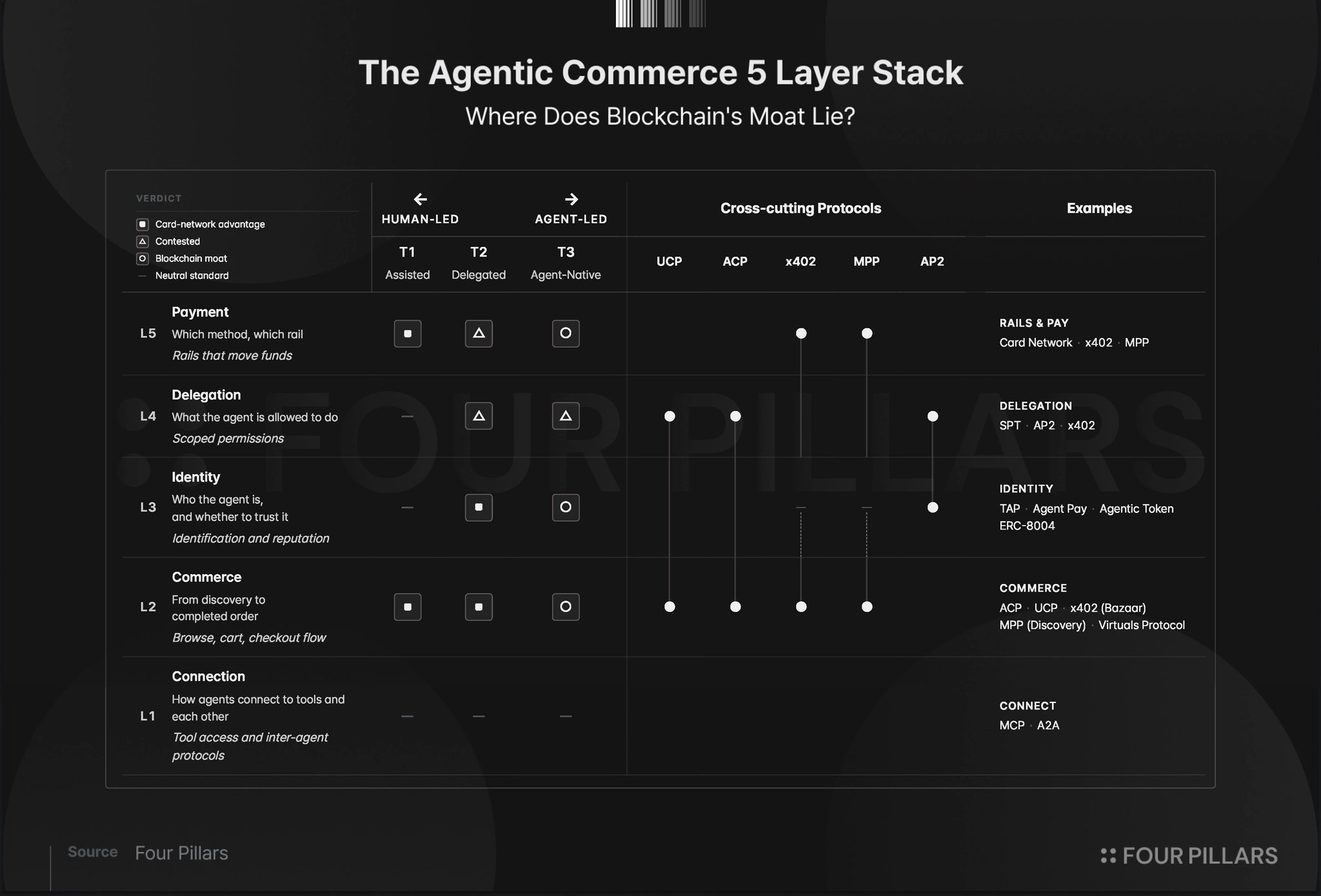

For that reason, the area crypto should enter in agentic commerce is not the existing card payment market. It is a new market that does not yet have a clear owner. The candidate is the headless merchant.

Finding the next emerging market: the headless merchant

“The store of the future will not be a website. It will be an endpoint.”

The headless merchant is a third form of store, following physical stores and e-commerce. It removes the human-facing frontend. Instead, an agent directly calls digital resources such as APIs, data, model inference, and on-chain information, pays for them, and receives the result.

Here, crypto’s programmable nature means more than simple payment. Payment conditions, usage limits, permissions, and settlement rules can be embedded in code. An agent can call resources within defined conditions and finalize payment at the moment of the call, without a human approval loop.

This is the important point. In traditional payments, finality is often treated as a weakness of crypto. In the headless merchant market, it becomes a core function.

In existing consumer payments, the fact that a payment does not end immediately is a benefit. Products may be delivered incorrectly, service quality may be poor, card fraud may occur, and refund disputes may arise. For this reason, card networks built post-transaction protections such as chargebacks, refunds, and dispute resolution into the payment structure. This delay and reversibility are not inefficiencies. They are trust costs designed to protect human consumers.

Headless merchant transactions have a different nature. When an agent calls an API, buys model inference, or receives data, the more important questions are whether the call succeeded, whether the result was returned, whether usage was measured, and whether the budget limit was respected. The center of trust shifts from “Can the transaction be reversed afterward?” to “Can the conditions be restricted before the transaction and finalized at the moment of execution?”

What this market needs is not post-transaction protection. It needs prior permission management, conditional execution, instant settlement, and an atomic link between payment and result delivery. When an agent calls a specific API, payment should be finalized per request rather than billed later. The provider has no reason to bear receivables, settlement delays, or the cost of small invoices. The buyer is also safer when limits and conditions are set in code, rather than giving the agent unlimited authority.

This is where crypto’s strength becomes clear. Crypto does not eliminate trust costs. It reallocates post-transaction dispute costs into prior conditions and settlement finality. Traditional payment networks leave room for reversibility to protect human consumers. In the headless merchant market, that same reversibility becomes delay, cost, and settlement risk. The smaller and more frequent the transactions are, the larger this difference becomes.

In the end, the important point in the headless merchant market is not whether users can pay with crypto. It is whether permission checks, payment, settlement, and result delivery can be tied into a single workflow when an agent calls a resource.

Here, payment finality becomes more than a technical feature. It becomes trust infrastructure that allows the M2M economy to be used repeatedly.

Where, then, does crypto stand in the headless merchant market today?

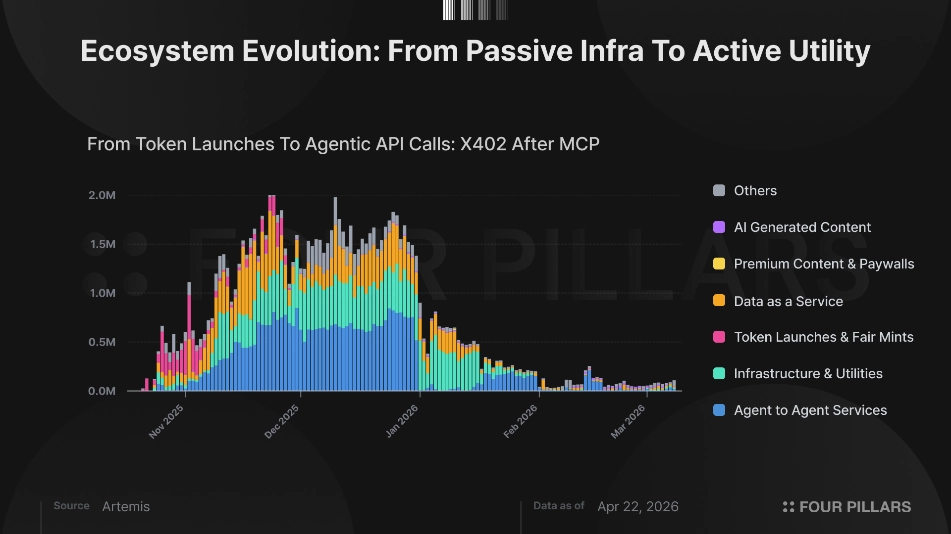

Based on x402 stats for the second quarter of 2026, the market is still in the development stage. Transaction count and buyer count are more important indicators than payment volume alone. These indicators have continued to rise, regardless of the broader market mood.

In particular, the growth of DaaS (Data-as-a-Service) and A2A share matters. These categories are more closely related to the headless merchant market than test calls, early experiments, or token launches. Their growth, along with the rise in broader x402 metrics, points to progress toward the headless merchant model.

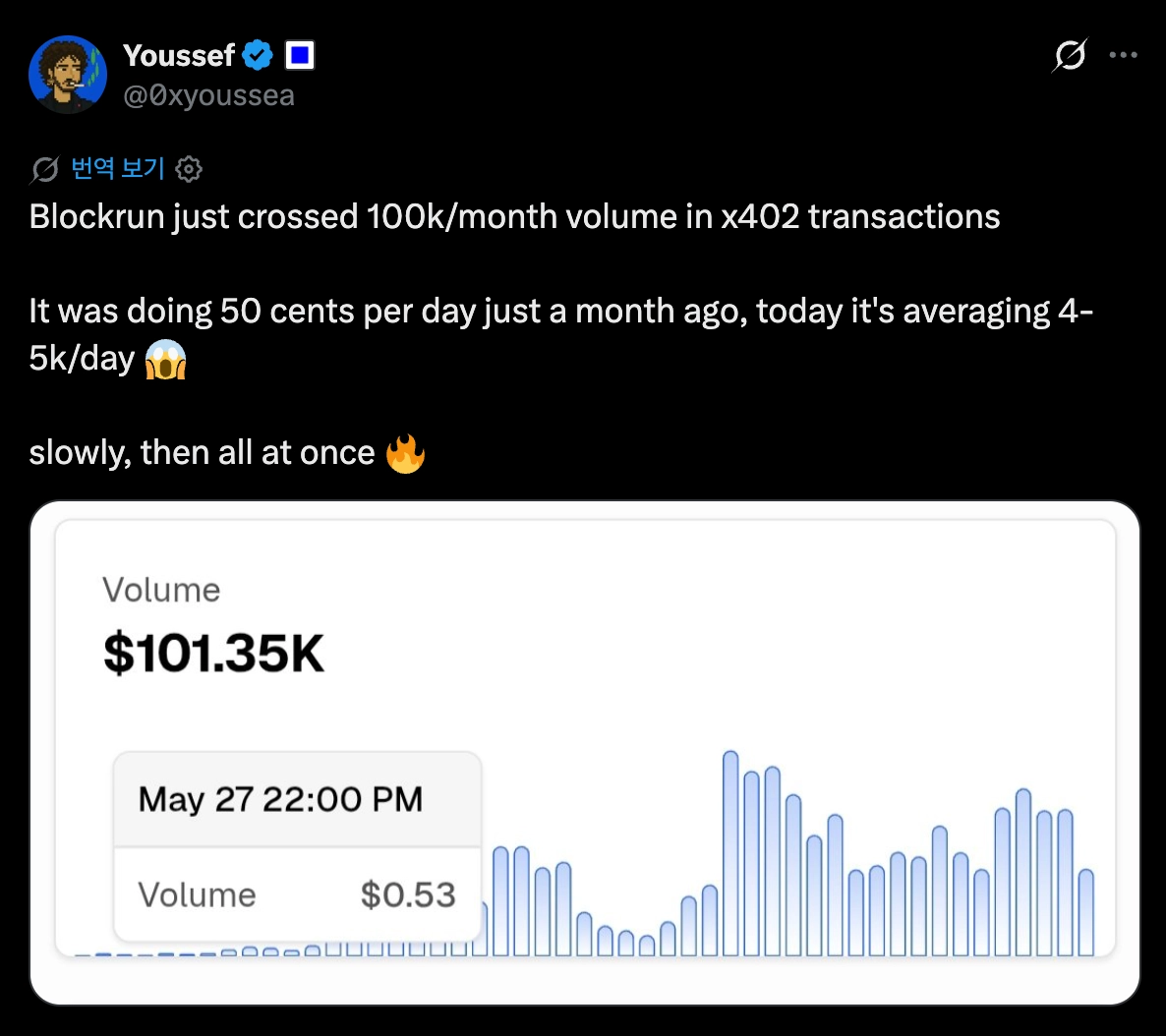

Source: X(@0xyoussea)

From this perspective, the metrics of providers such as BlockRunAI (@BlockRunAI) show potential. BlockRunAI is a pay-per-call AI gateway that allows AI agents to use about 60 AI models through real-time per-call payments from a USDC wallet, without API keys or subscriptions. According to x402scan, its transaction count over the past 30 days approached 9.5 million.

As services with this level of performance, or stronger killer services, appear, the market will move faster.

For agentic commerce centered on headless merchants to gain traction, and for crypto to sit at its center, many problems still need to be solved. The market needs a system that can convince both agents and people, from accessibility to trust and coordination layers.

Even so, the direction is clear. RedotPay identified and targeted payment bottlenecks in emerging markets before others did. In the same way, the next emerging market crypto should target is not consumer payments controlled by existing card companies. It is the headless merchant market, which still has no clear owner. The side that recognizes and enters this market first will eventually take that position.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.