Table of Contents

- Key Takeaways

- 1. Overview: A Rapidly Growing Tokenized Private Credit Market

- 2. Global Trends: Major Tokenized Private Credit Platforms

- Case Study 1: Figure Markets

- Case Study 2: Maple Finance

- Case Study 3: Apollo

- 3. Opportunities in the Korean Market: A Structurally Challenging Market for Application

- 3.1 Structural Differences Between the Global Market and the Korean Market

- 3.2 Sell side: Direct transplantation of global models is difficult

- 3.3 Buy side: Bottlenecks in the investment execution stage must be resolved

- 3.4 Constraints and growth potential

Researcher

Key Takeaways

- Tokenized private credit is emerging as one of the largest RWA categories after tokenized treasuries, driven by the appeal of private credit and the operational inefficiencies of traditional fund structures.

- The main value of tokenizing private credit is not higher yield, but improved operational efficiency through faster capital deployment, automated interest distribution, programmable compliance, and broader investor access.

- Global models differ by origin and structure: Figure tokenizes originated HELOC assets, Maple operates a crypto-native credit marketplace, and Apollo uses tokenization as a distribution layer for existing institutional private credit products.

- Korea is structurally different from the global private credit market because domestic private funds are concentrated in private equity, while private debt funds remain small and credit supply is still dominated by banks and securities firms’ balance sheets.

- In Korea, the most realistic opportunity lies in tokenizing existing loan assets through trust beneficiary certificates, while broader buy-side participation will depend on clearer rules around custody, accounting, taxation, and overseas tokenized securities holdings.

This article is adapted from "Korean Blockchain Guidebook for Institutions 2026," jointly published by Four Pillars and Pantera Capital. The full report covers 14 more themes for companies and institutional investors.

1. Overview: A Rapidly Growing Tokenized Private Credit Market

Private credit is one of the fastest-growing segments of global alternative finance. By mid-2025, the market for private credit globally exceeded $2.1 trillion in AUM, having more than doubled in size over the prior decade, as institutional allocators sought yield above investment-grade bonds without the liquidity constraints of public markets. The asset class is structurally attractive with its higher, floating-rate exposure and lower volatility than public bonds, but often has many structural and operational inefficiencies, including high minimum investment thresholds, opaque subscription windows, and administrative overhead.

Tokenization addresses these friction points directly. Rather than a single SPV with ten LP relationships, a tokenized private credit structure can maintain an on-chain loan register, automate interest distributions via smart contract, and allow whitelisted secondary transfers with programmable compliance checks embedded in the token. The core value proposition is not yield enhancement — the underlying credit risk does not change — but rather operational efficiency: faster deployment, automated servicing, and the ability to extend institutional-grade credit exposure to a wider universe of capital.

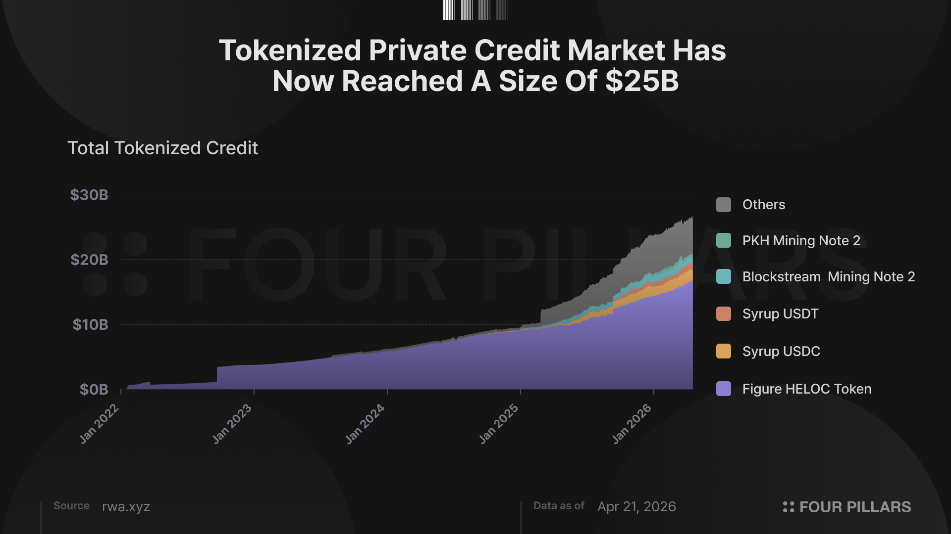

Onchain private credit has emerged as the second largest tokenized asset class behind US Treasuries, reaching over $6 billion as of April 2026. This asset class is particularly well-suited for tokenization for several reasons. First, today's private credit funds are gated by GP relationships and minimum check sizes that effectively exclude all but the largest allocators. Tokenization enables fractional participation with full KYC/AML enforcement, extending the LP base to mid-size family offices and corporate treasuries without degrading underwriting standards. Second, transparency: loan-level data — originations, repayment schedules, defaults — can be published on-chain in near-real-time, replacing the quarterly PDF that characterizes most traditional fund reporting. Third, composability: once a private credit token lives on-chain, it can serve as collateral in DeFi lending protocols or as a yield-bearing reserve in treasury management systems, generating utility beyond passive hold.

2. Global Trends: Major Tokenized Private Credit Platforms

The tokenized private credit market is not a single protocol but an ecosystem of origination, issuance, and curator platforms, each serving different credit niches with different underlying exposure and degrees of decentralization. We provide three representative examples – Figure, Maple, Apollo.

Case Study 1: Figure Markets

Figure markets (NASDAQ: FIGR), a Pantera portfolio company, is the single largest tokenized credit player by volume, with $16.7 billion USD of tokenized value (as of April 16, 2026). It originates home equity line of credit instruments (HELOCs) in the US, which are secondary liens on a home property. Figure natively tokenizes these HELOCs and issues them on its proprietary Provenance blockchain to distribute out as a lending product, such that any US KYC’ed person is able to have access to HELOC-backed yield products, which offer around 7-9% yield. Started by SoFi cofounder Mike Cagney, Figure provides an example of how a veteran fintech operator leverages tokenization as a genuine innovation (origination of a novel asset), along with appropriate regulatory compliance (operating the first SEC-licensed yield-bearing stablecoin), and reaching institutional-scale adoption.

Case Study 2: Maple Finance

Maple Finance is the leading crypto-native credit marketplace, having originated over $7 billion USD in loans since inception and currently manages $2.21 billion USD in assets. Rather than being an asset originator, Maple operates as a curator where institutional borrowers, especially crypto trading firms and market makers use digital assets as collateral and borrow stablecoins for their strategies. On the other end, Maple creates pools that offer permissionless yield to its syrupUSDC and syrupUSDT products. Credit decisions are managed by experienced pool delegates who perform off-chain underwriting, giving Maple a hybrid architecture that combines DeFi transparency with institutional risk discipline. This model has proven durable: the protocol maintained a 99% loan repayment rate as of late 2025, and scaled TVL from under $100 million in 2024 to over $4 billion by late 2025. Maple represents the archetype of a crypto-native credit infrastructure that has earned institutional trust not through regulatory licensing but through underwriting rigor and on-chain transparency.

Case Study 3: Apollo

Apollo Global Management ($733B AUM) partnered with Securitize to launch ACRED (Apollo Diversified Credit Securitize Fund) in January 2025 — a tokenized feeder fund that allocates assets into Apollo's flagship Diversified Credit Fund (ADCF), one of the fastest-growing private credit instruments managed by one of the largest alternative asset managers in the world. The underlying ADCF invests across corporate direct lending, asset-backed finance, and structured credit, and delivered an 11.7% net return in 2024. ACRED is deployed across Ethereum, Solana, Polygon, Avalanche, and Aptos via Securitize's tokenization infrastructure, making it accessible across the major smart contract ecosystems. Apollo represents a TradFi-native alternative compared to Figure and Maple’s models: rather than building credit infrastructure natively on-chain, it is a TradFi incumbent using tokenization as a distribution layer to bring existing, battle-tested private credit products to on-chain capital – a playbook that, if widely replicated by other large asset managers, could also become a mainstream mode of institutional credit tokenization.

3. Opportunities in the Korean Market: A Structurally Challenging Market for Application

3.1 Structural Differences Between the Global Market and the Korean Market

The amendments to the Electronic Securities Act and the Capital Markets Act, passed at the plenary session on January 15, 2026, recognized distributed ledgers as legally valid electronic registration account books and so established a foundation for issuing tokenized securities. They also allowed securities firms to intermediate investment contract securities and enabled multilateral OTC trading through OTC brokerage firms.

Tokenized securities are a "form" of securities, so they apply to every type of security. But the institutional design pushes actual use toward investment contract securities and trust beneficiary securities with non-standardized rights structures. Private credit tokenization has to operate inside this framework, which narrows approaches that tokenize fund interests as monetary trust beneficiary securities or as limited-partnership-type PEF equity interests.

Market structure also makes direct benchmarking against global models difficult. Korea's institutional private funds market is roughly KRW 153 trillion, but over 96 percent sits in private equity; private debt funds amount to only around KRW 6 trillion. Large LPs have historically allocated capital to buyout and growth funds. The mid-sized corporate segment is thin. Banks, public markets, corporate bonds, and policy finance already cover most financing needs, so US-style mid-market direct lending assets struggle to form.

There is a deeper structural gap. Globally, asset managers raise LP capital and operate off balance sheet. In Korea, the dominant structure is securities firms supplying credit on balance sheet within the limits of their own capital. That changes how the domestic private credit market can scale.

3.2 Sell side: Direct transplantation of global models is difficult

Looking at institutional constraints in detail shows which parts of the three global models can be applied in Korea and where they hit friction.

- Maple Finance (credit marketplace): Not applicable. Both prerequisites, a KRW stablecoin regime and a domestic pool of qualified crypto borrowers, are absent.

- Apollo Management (ACRED): The credit fund tokenization structure cannot be directly replicated in Korea. Domestic PEF interests are equity interests with transfer restrictions, so there is no way to design a structure where fund interests are freely tradable. An indirect structure using a feeder SPV is legally possible, but practical variables, including GP cooperation, interpretation of the qualified investor scope, and regulatory consistency for fund-of-funds structures, have kept any actual implementation from surfacing.

- Figure (origination, tokenization): Of the three, this model has the most realistic point of contact with Korea's regulatory system. Figure directly tokenizes HELOC loan receivables it originates on blockchain. In Korea, lending and loan origination are restricted to licensed financial institutions, which closes off the vertically integrated path for new platforms to originate and tokenize loans. Still, the structure of using individual loan receivables as securitization units and rebuilding them into beneficiary securities fits Korea's non-monetary trust beneficiary securities framework, and because the product qualifies as non-standard securities, it lines up with the STO direction.

The Figure model becomes more applicable if the supplier of loan receivables shifts from new platforms to existing financial institutions that already hold lending assets. One approach is to transfer loan receivables held by securities firms or asset managers into a trust and convert them into beneficiary securities. An early example is Bondiz by Apanda Partners, a joint venture of Shinhan Investment Corp, IGIS Asset Management, and EQBR, which tokenizes and distributes commercial real estate and SOC loan receivables using a trust beneficiary securities structure. Once the law comes into force in 2027 and this structure moves from the regulatory sandbox into a fully licensed regime, follow-up attempts that expand the range of underlying assets should follow.

3.3 Buy side: Bottlenecks in the investment execution stage must be resolved

The value proposition of tokenized private credit lies in automated interest distribution via smart contracts, embedded compliance, and secondary transferability. These features allow asset managers, pension funds, and insurers to access private credit exposure issued by global managers such as Apollo (ACRED) and Hamilton Lane (SCOPE) with higher operational efficiency, making it infrastructure worth evaluating from the buy side.

However, even after the STO legislation takes effect in 2027, the law addresses issuance and distribution of domestic token securities. It does not cover the question of Korean institutions holding offshore token securities. The buy-side gap will not resolve automatically once the law is in place.

At the level of primary legislation, the path is not closed. Tokenized private credit fund interests such as ACRED are likely to qualify as securities under the Capital Markets Act, which classifies instruments based on the substance of rights rather than the form of issuance. The Foreign Exchange Transactions Act also permits overseas securities acquisition in principle. However, the Act presumes settlement through a foreign exchange bank, and whether onchain settlement structures are compatible with this requirement has not been confirmed. Between legal permissibility and actual execution, a layer of ambiguity remains:

- Accounting and prudential standards: Accounting classification and fair value measurement of offshore private credit fund interests can be handled under the existing K-IFRS (Korean International Financial Reporting Standards) framework.

- However, there is no regulatory guidance on practical issues arising from the tokenized form, such as whether onchain custody structures qualify under institutional asset safekeeping requirements, or whether tokenized securities fall within the investable asset scope defined by the Insurance Business Act or pension fund regulations. Even in the U.S., the SEC only issued guidance in Dec 2025 recognizing broker-dealer custody of tokenized securities under the existing Customer Protection Rule (Rule 15c3-3). Korea has no equivalent precedent.

- Tax and reporting obligations: There is no domestic tax guidance on onchain transfers or income distribution from tokenized private credit feeder interests. The OECD has published classification criteria for tokenized financial assets, and structures where the issuing entity controls transfers, as with Securitize, are likely to be reported under the existing CRS (Common Reporting Standard) framework.

- However, how the Korean National Tax Service will incorporate these criteria into the domestic overseas financial account reporting system has not been determined, and there is no interpretive guidance to reference.

As a result, the Korean LP buy side for tokenized private credit is unlikely to open in the near term. The efficiency gains from tokenization, such as automated distribution and secondary transferability, are clear, but a time lag before actual incorporation into the institutional framework is unavoidable.

3.4 Constraints and growth potential

Today, the Korean STO market concentrates on fractional investment based on investment contract securities such as artworks, music, and physical real estate. Private credit tokenization has to rely on placing loan receivables into trusts and issuing non-monetary trust beneficiary securities. Because of market structure, the pool of tokenizable underlying assets is smaller than in global markets, and this segment is unlikely to scale quickly even after STO implementation.

That said, both sides of the market have room to grow. On the sell side, comprehensive financial investment firms already hold acquisition finance and real estate PF loan receivables on their balance sheets and have built STO issuance infrastructure inside the same entity over the past three years. Supply pipelines can activate the moment the law takes effect. On the buy side, institutional holding of foreign tokenized securities is not explicitly prohibited, so access pathways to global private credit exposure may open gradually as accounting standards and custody infrastructure mature.

Retail investors stand to benefit too. Bondiz shows the direction: assets such as commercial real estate and infrastructure loan receivables, previously limited to institutional investors, can be restructured into trust beneficiary securities and split into small units for retail access. Backed by senior secured loans and offering interest income above bank deposit rates, the product occupies the space between deposits and public bonds. How fast this turns into an actual market depends on two things: how quickly subordinate regulations define the scope of eligible underlying assets, and how quickly practical standards are put in place after the 2027 enforcement.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![MSTR and COIN [FP Weekly 26]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F6ivhjsmqq8e3w1.png&w=1920&q=75)

![Signals from Wall Street and Japan's Securities Industry to the Crypto Market [FP Weekly 25]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fuh58gemqes9azi.png&w=1920&q=75)

![The Fall of Two Worlds: MSTR and ZEC [FP Weekly 24]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F9w86bhmq4oqczw.png&w=1920&q=75)