Table of Contents

- Key Takeaways

- 1. Overview: A $140T Market, Still Mostly Untouched

- 2. Global trends: Direct Tokenization and Entitlement Tokenization as Key Approaches

- Case 1: Direct tokenization

- Case 2: Entitlement tokenization

- Case 3: Indirect tokenization

- From issuance to utilization

- 3. Opportunities in the Korean Market: Fundamental Challenges

Researcher

Key Takeaways

- Tokenized equities are still in an early stage, but they may become one of the most important RWA sectors given the massive size of global equity markets and growing interest from both crypto-native and traditional financial institutions.

- Unlike tokenized treasuries, tokenized equities are structurally complex because equities involve not only economic rights, but also voting rights, residual claims, preemptive rights, and other shareholder rights.

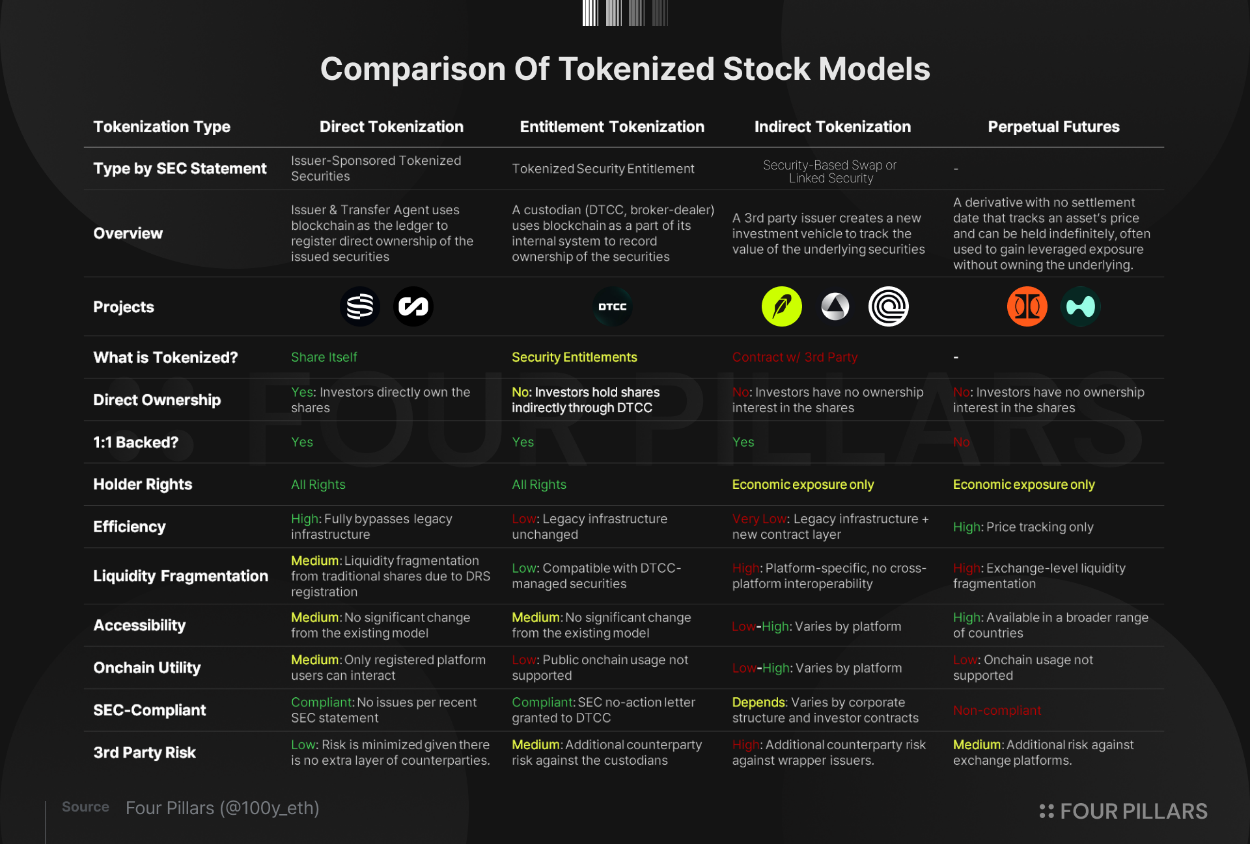

- The tokenized equity market can be divided into three main models: direct tokenization, entitlement tokenization, and indirect tokenization, each with different implications for ownership, liquidity, regulation, and on-chain utility.

- Direct tokenization and entitlement tokenization are more aligned with existing securities law and shareholder rights, while indirect tokenization mainly provides synthetic economic exposure and is likely to remain a transitional model.

- In Korea, near-term opportunities for tokenized equities are limited because listed shares must be electronically registered with KSD, and the current STO framework is focused more on non-standard securities than traditional stocks.

This article is adapted from "Korean Blockchain Guidebook for Institutions 2026," jointly published by Four Pillars and Pantera Capital. The full report covers 14 more themes for companies and institutional investors.

1. Overview: A $140T Market, Still Mostly Untouched

The tokenized stock market is still small, but the upside is larger than in any other sector. The global stock market is worth about $140T. In the US, firms like Securitize and Robinhood are building for it, and incumbents like DTCC, Nasdaq, and NYSE are preparing their own infrastructure. The next three years will decide how this market takes shape.

Like any legacy system, stock markets carry inefficiencies. Trading hours are limited (the exact window varies by country), and settlement usually takes T+1 to T+3. Blockchain runs 24/7 and settles instantly, which addresses both problems.

One difference from tokenized government bonds: tokenization methods for stocks vary widely. Two reasons. First, the market is early, and issuers have built different structures to either comply with or sidestep securities laws in different jurisdictions. Second, stocks carry more than cash-flow rights. They come with voting rights, residual claims, preemptive rights, and other layers that every tokenization model has to handle. Financial institutions preparing for tokenized stocks need to start by understanding the methods already in use.

2. Global trends: Direct Tokenization and Entitlement Tokenization as Key Approaches

Tokenized equities are being actively discussed and developed primarily in the U.S. market. From Securitize and Backed Finance (recently acquired by Kraken) to Robinhood and Coinbase to DTCC, Nasdaq, and NYSE, everyone from crypto-native startups to legacy infrastructure providers is building their version.

The key point: not all tokenized equities produce the same effects. The tokenization model determines ownership structure, associated rights, liquidity fragmentation, trading accessibility, on-chain utility, regulatory compliance, and risk. These differences matter.

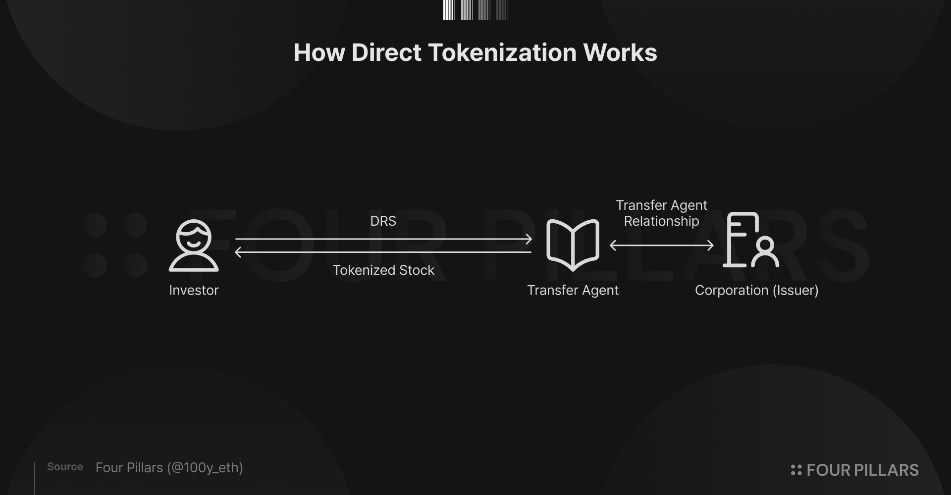

Case 1: Direct tokenization

Direct tokenization is what the SEC calls Issuer-Sponsored Tokenization. The issuer or transfer agent tokenizes the security directly, replacing the internal-database shareholder registry with a blockchain-based one. Securitize and Superstate are the main players here.

This model ties into the U.S. Direct Registration System (DRS). Normally, when an investor buys shares through a broker, those shares are registered under Cede & Co. (a DTCC nominee), and the investor holds indirect rights. DRS lets investors register shares directly in their own name, bypassing DTCC. Securitize manages shareholder registries via DRS and issues on-chain tokenized shares to DRS-registered investors.

The approach is fully SEC-compliant, bypasses DTCC, and is operationally efficient. Because the shares themselves are tokenized, token holders inherit all associated rights. The downsides: liquidity is fragmented from traditional equity markets, and regulatory compliance requirements limit on-chain utility.

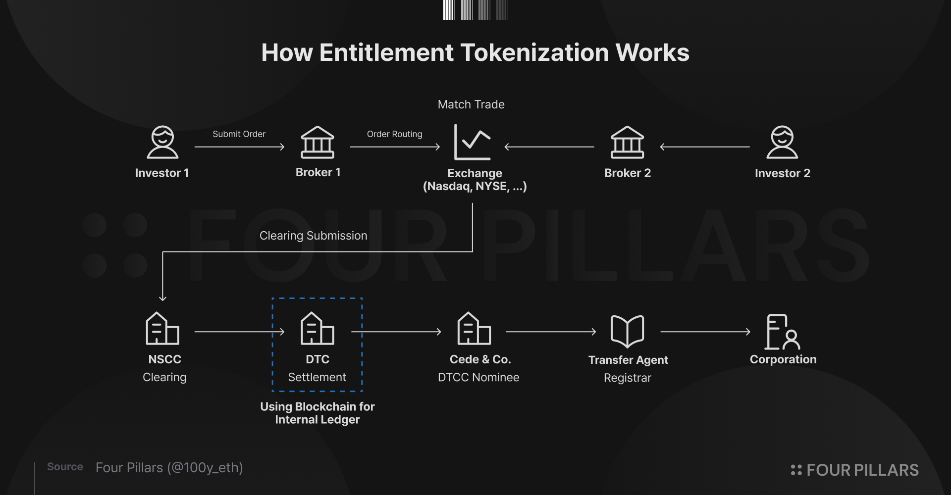

Case 2: Entitlement tokenization

Entitlement tokenization falls under Tokenized Security Entitlement within Third-Party-Sponsored Tokenization in the SEC framework. Here, a third party like DTCC integrates blockchain into its own registry system. DTCC is the main player.

DTCC recently received a No-Action Letter from the SEC, clearing it to begin under controlled conditions. The goal: keep the existing equity clearing, settlement, and custody pipeline intact while using blockchain to record entitlement data and improve settlement efficiency.

This approach is highly compatible with existing securities infrastructure, investors keep all their rights, and liquidity stays concentrated. But because it preserves most of the existing structure, the efficiency gains from cutting out intermediaries are modest. Investors still hold equities indirectly, and global accessibility remains limited.

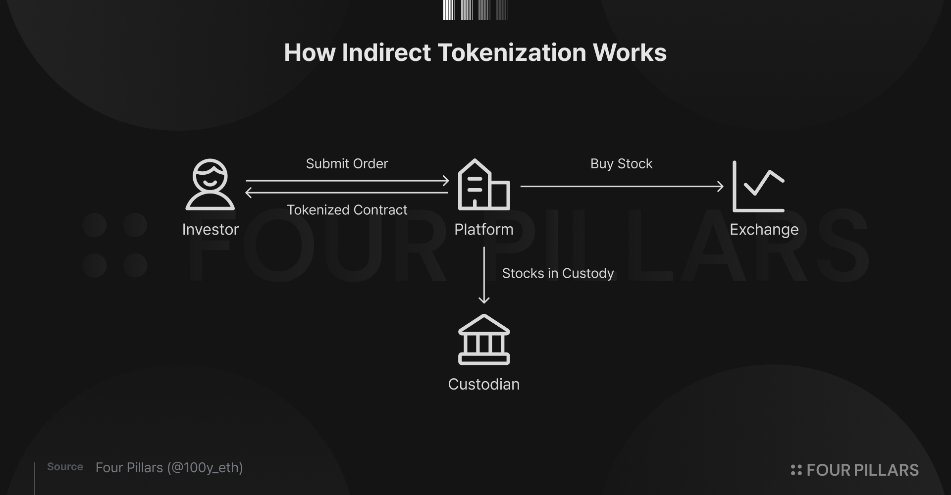

Case 3: Indirect tokenization

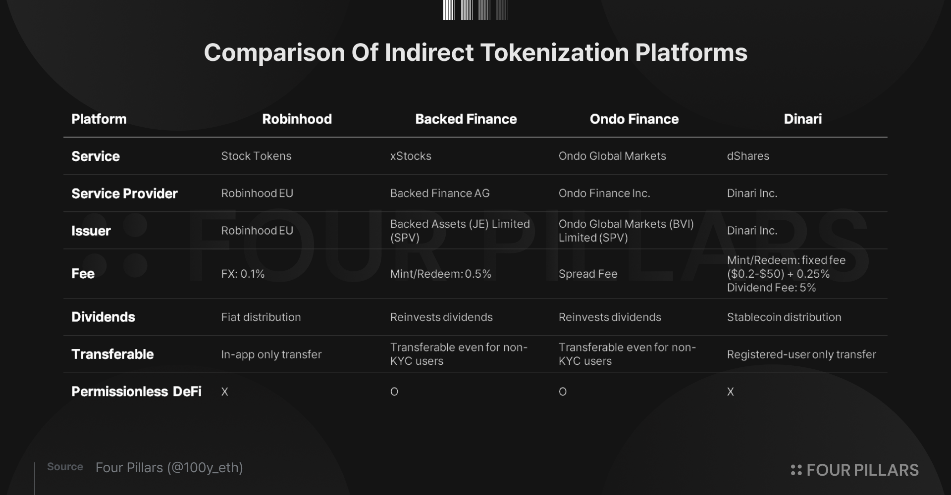

Indirect tokenization corresponds to Linked Security or Security-based Swap in the SEC framework. A third party gives investors synthetic economic exposure to a reference security. Robinhood, Backed Finance, and Ondo Global Markets all use this model.

The mechanics: when an investor requests tokenized equities, the platform buys the underlying shares on the stock market and holds them with a custodian, then issues tokens representing economic exposure to those shares. Strictly speaking, this model does not tokenize the shares or their associated rights directly.

Platforms using indirect tokenization vary in accessible jurisdictions and on-chain usability depending on their legal structures, as shown above. Robinhood and Dinari, for instance, operate regulated entities in the U.S./EU that hold U.S. equities, limiting distribution to KYC-verified users. Backed Finance and Ondo Finance use offshore SPV structures, which allow freer trading and on-chain usage.

Indirect tokenization is a transitional model compared to direct and entitlement tokenization. Token holders can only claim economic returns, not the full rights that come with direct or entitlement models. Liquidity is fragmented across platforms, and the extra token issuance layer on top of existing systems adds inefficiency. The SEC has flagged concerns about these models in its tokenized securities statement. Given Kraken's collaboration with Nasdaq after acquiring Backed Finance, and Ondo Finance's recent SEC filing, it looks likely that platforms using indirect tokenization will eventually move to direct or entitlement models.

From issuance to utilization

Beyond issuance, there are interesting directions in how tokenized equities can actually be used.

- Dividends, interest payments, stock splits, and other corporate actions that were previously handled manually can be automated through smart contracts. Securitize has built infrastructure for this via its DS Protocol.

- Compliance rules like KYC/AML can also be embedded into tokenized equities, so that transactions are automatically verified and only compliant trades go through. DTCC's Compliance Aware Token Framework and Securitize's DS Protocol both do this.

- Tokenized equities can be put to work on-chain: used as liquidity in protocols or as loan collateral. Backed Finance's xStocks (now under Kraken) already integrates with DeFi protocols like Kamino, Orca, Raydium, and Byreal for exactly this.

3. Opportunities in the Korean Market: Fundamental Challenges

Korea's recently passed STO law focuses on non-standard securities like investment contract securities, not traditional securities like equities and bonds. That leaves limited room for tokenization in the Korean equity market.

Can direct tokenization work here? In Korea, listed shares must be electronically registered with the Korea Securities Depository (KSD). Unlike Securitize or Superstate, which bypass DTCC entirely, there is no way to directly register and hold listed shares outside of KSD.

Unlisted shares are a different story. Electronic registration with KSD isn't mandatory for unlisted shares, so there's some room for direct tokenization. But Korea doesn't allow traditional and tokenized forms of shares to coexist: you pick either electronic registration or distributed ledger registration. Tokenizing shares that are already circulating is effectively impossible.

KSD could consider entitlement tokenization, similar to what DTCC is doing. Blockchain integration could simplify reconciliation, cut settlement times, and enable around-the-clock settlement. But Korean investors already directly own their shares (rather than holding them indirectly like in the U.S.), and listed shares are fully digitized. The incentive to adopt blockchain is weaker than it is for DTCC.

The bottom line: short-term opportunities for tokenized equities in Korea are hard to find. The better play is to take a long-term view, watch how the U.S. securities market migrates to blockchain-based systems, and prepare accordingly.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![50% for Ethereum, 50% for Congress [FP Weekly 33]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F1cg9d7msn1d3j2.png&w=1920&q=75)

![Coldcard Got Burned, Coinbase Froze [FP Weekly 32]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fhv83s5msebytml.png&w=1920&q=75)