Table of Contents

- Key Takeaways

- 1. Overview: The State of the FX Market

- 2. Global Trends: Understanding the Three Layers of FX Infrastructure

- 2.1 FX Layer 1, Trading: where prices are made

- 2.2 FX Layer 2, Settlement: where money actually moves

- 2.3 FX Layer 3, Backbone: where the dollars come from

- 2.4 Fintech Abstractors: the UX layer on top of the stack

- 3. Opportunities in the Korean Market: Retail isn't a Target, Opportunity Could be on Corporates

- 3.1 The Regulatory Wall Defines the Market

- 3.2 Where Stablecoins Can Actually Enter: Global Korean Corporates

Researcher

Key Takeaways

- FX is not just a remittance or currency exchange market; it is a massive financial infrastructure layer driven mainly by funding, hedging, and balance sheet management.

- Stablecoins can meaningfully improve FX settlement infrastructure, especially in non-CLS currency corridors such as KRW, IDR, VND, and PHP, where settlement is slow, costly, and exposed to Herstatt risk.

- Stablecoins do not replace the dollar funding backbone of the FX market; they redistribute dollar liquidity into areas where traditional infrastructure is weak, such as weekends, emerging markets, small-value transactions, and 24/7 digital markets.

- Fintech players such as Wise, Revolut, and SentBe improve user experience on top of existing infrastructure, but stablecoins can change the underlying settlement layer itself.

- In Korea, the real opportunity for stablecoin-based FX infrastructure is not retail remittance, but enterprise FX for global Korean companies that face T+2 settlement delays, correspondent banking costs, non-CLS currency risk, and limited 24/7 treasury operations.

This article is adapted from "Korean Blockchain Guidebook for Institutions 2026," jointly published by Four Pillars and Pantera Capital. The full report covers 14 more themes for companies and institutional investors.

1. Overview: The State of the FX Market

FX is the largest financial market in the world, roughly $7.5~9.6 trillion changes hands every single day. It never closes, and price formation follows the sun from Asia to Europe to North America. Unlike equities or bonds, FX doesn't price an asset, it prices sovereign monies against each other.

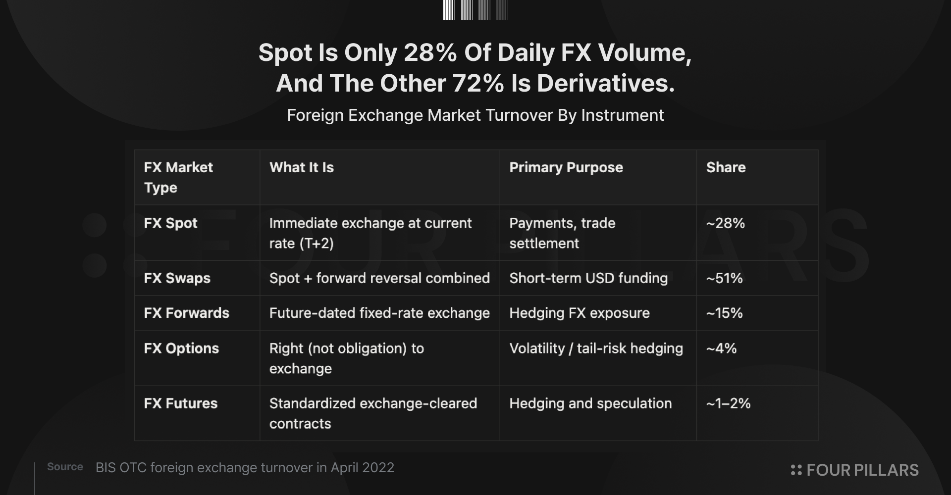

Most people imagine FX as swapping currency, an importer paying a supplier, or Samsung converting Apple revenue into won. That picture is real but small. Spot is only ~28% of daily FX volume. The other ~72% is derivatives.

The biggest single instrument is the FX swap (~51% of the market). It isn't a bet on exchange rates, it's the mechanism global banks use to borrow short-term US dollars against other currencies. The world outside the US is perpetually short dollars, and FX swaps are how those dollars get sourced every day.

The punchline: FX is driven far more by funding, hedging, and balance-sheet management than by payments.

Remittance lives inside the 28% spot slice, but its pain points like T+2 delays, correspondent hops, weekend dead zones are infrastructure problems. The same rails that slow a remittance also slow the settlement leg of a $500M swap.

Fix the rails, and you automatically relieve the ~$2.6 of derivatives sitting on top of every $1 of spot.

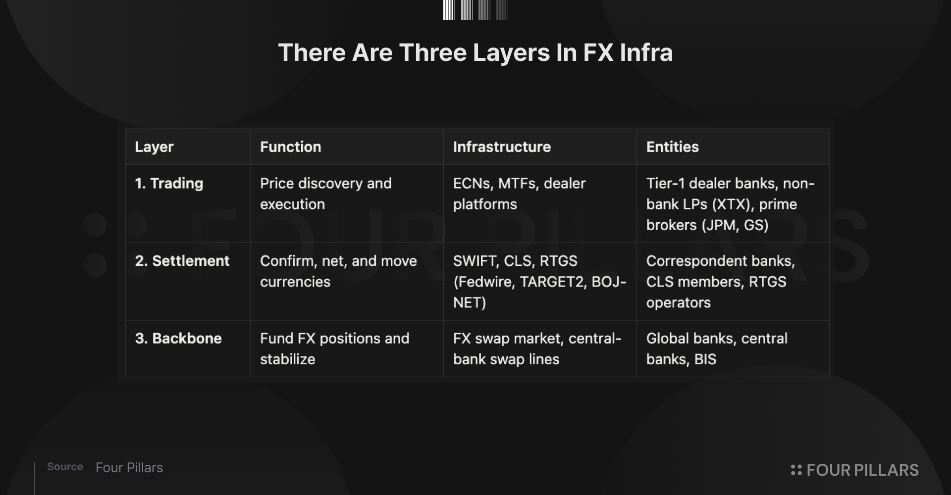

2. Global Trends: Understanding the Three Layers of FX Infrastructure

Every cross-border payment, a $5 remittance or a $500M corporate swap, passes through the same three layers:

- Trading layer, where prices are made

- Settlement layer, where value actually moves

- Backbone layer, where dollars fund the whole system

Fintechs like Wise, Revolut, and SentBe are abstractors sitting on top of this stack. They polish the UX but don't replace the rails.

Stablecoins are different. They rebuild the Settlement layer itself, collapsing SWIFT, correspondent banking, and RTGS timing windows into one 24/7, near-instant, programmable transfer.

A useful cross-cut: every FX instrument is born in FX Layer 1, dies in FX Layer 2, and is funded through FX Layer 3.

- FX Layer 1 is instrument-specific, each product has its own venue.

- FX Layer 2 is currency-specific, CLS-eligible pairs settle cleanly; everything else (KRW, IDR, VND, PHP) fights through correspondent banks.

- FX Layer 3 is USD-specific, because the entire global FX system is built on borrowed dollars: the USD is on one side of ~88% of all FX trades and makes up ~58% of disclosed global FX reserves. Non‑US banks generally do not hold Federal Reserve master accounts, so offshore banks access dollars indirectly via correspondent relationships and USD funding markets dominated by a small set of global systemically important banks (there are 29 G‑SIBs in the current FSB list).

That's why stablecoins, by operating at FX Layer 2, relieve the settlement leg of all five instruments at once, while leaving the underlying USD-funding dependency at Layer 3 untouched.

2.1 FX Layer 1, Trading: where prices are made

FX Layer 1 is where a price and a legal obligation are created, no money has moved yet. Walk through Samsung converting USD 500M into KRW:

- Request for quote. Samsung's treasury desk sends an RFQ through a multi-dealer platform (360T) to five banks simultaneously.

- Price construction. Each bank's pricing engine pulls live quotes from EBS and blends them with inventory, while non-bank LPs like XTX Markets stream prices into the bank engines.

- Winner and booking. Citi wins at 1,378.50, books the trade, and verifies Samsung's credit line.

The stack behind those three steps:

- Venues, multi-dealer platforms like 360T, Bloomberg FXGO, and FXSpotStream.

- Counterparties, Tier-1 dealer banks (JPM, UBS, Deutsche, Citi, GS) who make up ~45% of global FX volume.

- Credit, extended by prime brokers (JPM, GS, MS, Citi PB).

Stablecoins do not disrupt this layer, price formation still happens in sovereign currency on bank venues.

2.2 FX Layer 2, Settlement: where money actually moves

If FX Layer 1 is where you agree on a price, FX Layer 2 is where the two banks actually hand each other the money. This is the step that is slow, expensive, and risky today, and it is exactly the step stablecoins rebuild. The one question that decides everything here is simple: is the currency pair in CLS or not?

What is CLS, and why does it matter? CLS (Continuous Linked Settlement) is a shared settlement "utility" owned by the world's biggest FX banks.

When two banks trade, say USD for JPY, CLS makes sure both sides pay at the same moment. Neither bank can pay first and lose the money if the other fails. This is called Payment-versus-Payment (PvP), and it removes Herstatt risk (the historical nightmare of paying out in one currency and never receiving the other).

CLS by the numbers (source):

- Covers 18 major currencies

- Settles roughly ~$6.5T per day

- Handles ~50% of all global FX settlement (and ~90% within its 18 currencies)

- Compresses gross volume down to ~$50B of actual funding via netting (~99% compression)

The catch: KRW, IDR, VND, PHP, and most EM currencies are not in CLS, so they have to settle the old, clunky way. Concretely, a cross-border trade takes one of two paths:

- Path A, the clean CLS path (e.g. USD/JPY). Both banks send matched instructions to CLS early in the morning (before 06:30 CET). CLS nets everyone's trades together, then settles all legs simultaneously across central-bank accounts. Result: same-day, just a few bps of cost, zero Herstatt risk.

- Path B, the messy non-CLS path (Samsung's USD/KRW). The USD leg and the KRW leg settle separately and out of sync. Citi wires USD through Fedwire to BNY Mellon (KEB Hana's US correspondent). Instructions travel over SWIFT, which is just a messaging network, not actual money. The money hops through 2–4 banks, each taking a fee. KEB Hana then credits Samsung in won via BOK-Wire+, but BOK-Wire+ only runs during Seoul business hours, so dollars arriving after hours just sit idle. Result: T+2 (two-day delay), 15–40 bps of friction, live Herstatt risk, weekends dead.

Making matters worse: since 2021–2024, US correspondents have been cutting off EM clients ("de-risking"). Path B has been getting more expensive, not less.

This is exactly where stablecoins change the picture.

A single USDC transfer from Circle to Samsung's wallet replaces SWIFT, correspondent banks, RTGS opening hours, and CLS cut-off windows all at once, with one on-chain transfer that is 24/7, near-instant, PvP-equivalent, and programmable.

The advantage is largest precisely where today's system is worst: non-CLS corridors (KRW, IDR, VND, PHP) and weekends/holidays.

That is the entire stablecoin thesis at FX Layer 2, in one sentence.

2.3 FX Layer 3, Backbone: where the dollars come from

FX Layer 3 answers a question most people never ask: where do all those dollars moving through Layer 2 actually come from?

The Fed is the only real source of USD, but almost no bank outside the US has a Fed account. So every non-US bank has to borrow its dollars from someone who does. That borrowing chain is what FX Layer 3 is.

Think of it as a pyramid of credit:

- Local banks (like Shinhan in Korea) need USD to serve clients, but can't get it from the Fed directly.

- Global "G-SIB" banks (JPM, Citi, MUFG, HSBC) do have USD access, and lend dollars to local banks, usually through FX swaps (borrow USD now, pay it back with a fixed forward rate).

- The Fed sits at the top. In a real crisis it lends USD to other central banks through swap lines, which then feed their own banks.

A concrete example: when Shinhan needs USD 1B overnight, it borrows from MUFG via an FX swap. The extra cost versus the "fair" interest-rate differential is called the cross-currency basis, currently −15 to −30 bps for KRW, meaning Korean banks pay a premium to get dollars. MUFG itself sources those USD from its account at JPM or from the US repo market.

And every quarter-end this chain breaks. Basel III rules force the big US banks to shrink their balance sheets. JPM pulls back USD lending. The basis blows out to −80 bps. USD/KRW spot spikes.

Stablecoins do not replace this layer. A USDC is ultimately a claim on a US bank deposit or T-bill, so the dollar still has to be created inside the traditional system.

What stablecoins do is redistribute the dollars the Backbone produces, pushing them into places the legacy system can't reach: weekends, emerging-market corridors, small tickets, and 24/7 crypto markets.

2.4 Fintech Abstractors: the UX layer on top of the stack

The three layers above are bank-grade plumbing, hostile to end users, small businesses, and anyone without a treasury team. Fintech abstractors are the companies that wrap that plumbing in a product and resell access to it. They don't own any of the three layers; they rent them, route across them, and package them into something a retail user or SMB can actually use.

Three archetypes, one per layer:

- Layer-1 (pricing): multi-dealer aggregators (360T, FXall, Bloomberg FXGO) and retail brokers (OANDA, IG, Saxo). Value-add is price competition.

- Layer-2 (settlement): remittance and cross-border payment fintechs (Wise, Revolut, Nium, Airwallex, Thunes; Korea: SentBe, Hanpass, MOIN). They bypass SWIFT/correspondent banks via prefunded local accounts and internal netting, local-in/local-out, not a real cross-border wire.

- Layer-3 (USD funding): prime-of-prime brokers (LMAX, CFH), non-bank LPs (XTX, Citadel Securities).

Why this matters for stablecoins: abstractors prove the demand is real, but they've hit a ceiling, prefunded liquidity ties up working capital and margins on easy corridors are near-zero. Stablecoins relax that constraint: an abstractor settling in USDC frees working capital, gets 24/7 coverage, and reaches corridors where prefunding isn't economical.

The abstractors are the distribution layer, stablecoins just need to become their preferred settlement medium.

3. Opportunities in the Korean Market: Retail isn't a Target, Opportunity Could be on Corporates

3.1 The Regulatory Wall Defines the Market

Korean FX starts with one fact: the won is a walled currency. All cross-border FX is governed by the Foreign Exchange Transactions Act (FETA), enforced by the Ministry of Economy and Finance (MOEF) and the Bank of Korea (BOK). KRW is non-internationalized and non-deliverable offshore, meaning every KRW <> FX leg must touch a domestically licensed entity, and BOK monitors it all in real time through ORIS.

This makes Korea the strictest FX regime in the OECD:

- Retail capped at USD 50K/year

- Travel Rule kicks in at ~USD 700 (the lowest threshold in any major economy)

- FETA violations carry criminal liability

Only three legal routes exist, and each occupies a distinct, well-defended niche:

- Tier 1 banks (KEB Hana, Shinhan, KB, Woori, NH, IBK, plus Citi Korea and StanChart Korea) own USD correspondent relationships, BOK-Wire+ access, and the onshore USD/KRW interbank market. They command corporate FX end-to-end, but still settle every USD/KRW trade via T+2 correspondent banking and carry Herstatt risk.

- SAOR fintechs (SentBe, Hanpass, MOIN, Wise via local partner) bypass SWIFT entirely, netting bilaterally through prefunded pools. This is how they compress fees to ~1/10 of bank rates, but the same license that enables them also caps them at USD 5K/tx and USD 50K/user/year, legally barring them from corporate FX or SWIFT/CLS access.

- EFB-licensed travel-FX fintechs (Travel Wallet) operate as prepaid electronic payment means issuers and rely on a partner bank for the actual FX leg. They have compressed point-of-sale FX spreads aggressively, but tickets are small.

The result is a bifurcated market with no middle. Retail is saturated and capped: ~25 SAOR licensees compete over the same USD 50K/year/user budget at flat ₩2,500 fees. B2B is almost entirely bank-owned: SAOR is legally excluded above USD 5K/tx, and banks still run T+2 settlement with no 24/7 capability. Neither side has pricing power left, and neither has room to grow.

3.2 Where Stablecoins Can Actually Enter: Global Korean Corporates

This is the context for reading stablecoins into Korea. A licensed KRW stablecoin does not yet exist, the Digital Asset Basic Act (DABA) Phase 2 has not landed, and no Korean bank has publicly adopted a stablecoin settlement rail in production. What follows is a forward-looking opportunity map tied to specific policy unlocks, not a live market.

Given the structure above, retail FX is a small competitive market. The TAM is hard-capped by FETA, KRW is non-deliverable offshore, on/off ramps face the tightest Travel-Rule friction in the OECD, and margins have already been compressed to near-zero by banks, Wise, SentBe, and MOIN. Any stablecoin product targeting retail remittance would enter a market where the regulatory ceiling, not the product, is the binding constraint.

The one concrete wedge is global Korean corporates with large, recurring USD revenue like Samsung, Hyundai, SK, HD Hyundai, shipbuilders, semiconductor suppliers, and shipping and commodity trading houses. Their pain is measurable and structurally unaddressed by today's rails:

- T+2 settlement ties up working capital on every USD leg, with weekends extending exposure to three or four days.

- Correspondent banking fees stack on every hop, with no netting across affiliates.

- Non-CLS Asian pairs (KRW/JPY, KRW/SGD, KRW/IDR) lack PvP settlement entirely, forcing intra-day credit lines and manual reconciliation.

- 24/7 treasury operations are impossible under correspondent rails which is a problem that compounds as Korean globals run production and sales across Asia, the Middle East, and the Americas.

This is the segment where the pain is large enough to justify switching costs, and it is the only segment where stablecoin rails offer something banks structurally cannot: instant, PvP, 24/7 settlement with programmable netting across subsidiaries.

Winning this segment will not come from a standalone fintech. These corporates have deep Tier 1 bank relationships, in-house treasury teams running FETA-compliant processes, and existing hedging programs that resist piecemeal disruption. The realistic path is a bank-partnered consortium rail, where the licensed bank handles FETA reporting and the KRW leg, while a stablecoin layer carries the USD (or non-CLS Asian) side on-chain.

So stablecoin headroom in Korean FX is bounded, but not by market demand. It is bounded by three specific regulatory unlocks: (1) a licensed KRW stablecoin under upcoming legislation, (2) explicit BOK guidance permitting banks to settle FX legs on stablecoin rails, and (3) an amendment to FETA reporting that recognizes on-chain settlement as equivalent to correspondent messaging. Without these, even the corporate wedge stays hypothetical.

With them, the corporate FX layer, not retail remittance, is where stablecoins could enter the Korean FX market.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![50% for Ethereum, 50% for Congress [FP Weekly 33]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F1cg9d7msn1d3j2.png&w=1920&q=75)

![Coldcard Got Burned, Coinbase Froze [FP Weekly 32]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fhv83s5msebytml.png&w=1920&q=75)