Table of Contents

- Key Takeaways

- 1. Overview: You Need to Understand Payment Structures Before You Can Fix Them

- 2. Global Trends: How Stablecoin Payment Structures Actually Differ

- Case 1: Crypto Cards

- Case 2: Stablecoin Settlement via Card Networks

- Case 3: PSPs Adding Stablecoin Checkout

- Case 4: Fully On-Chain Payments

- 3. Opportunities in the Korean Market: Limited in the Short Term, Boundless in the Long Run

- 3.1 The Gap Between Potential and Opportunity

- 3.2 Short-Term Opportunities Are Unclear

- 3.3 Long-Term: Build the Stablecoin Ecosystem First

- 3.4 Merchants Should Take Fully On-Chain Payments Seriously

Researcher

Key Takeaways

- Stablecoin payments are not a one-size-fits-all solution; their impact depends on where they are integrated into the existing payment stack.

- Many current stablecoin payment models, such as crypto cards and PSP-based checkout options, improve accessibility more than cost efficiency because they still rely on existing intermediaries.

- Fully on-chain payments have the greatest potential to reduce fees and settlement time by replacing traditional intermediaries with wallets, smart contracts, and blockchains.

- In Korea, short-term opportunities for stablecoin payments are limited because the existing payment infrastructure is already highly efficient.

- The larger long-term opportunity lies in building a broader stablecoin-based financial ecosystem that provides clear value to both users and merchants.

This article is adapted from "Korean Blockchain Guidebook for Institutions 2026," jointly published by Four Pillars and Pantera Capital. The full report covers 14 more themes for companies and institutional investors.

1. Overview: You Need to Understand Payment Structures Before You Can Fix Them

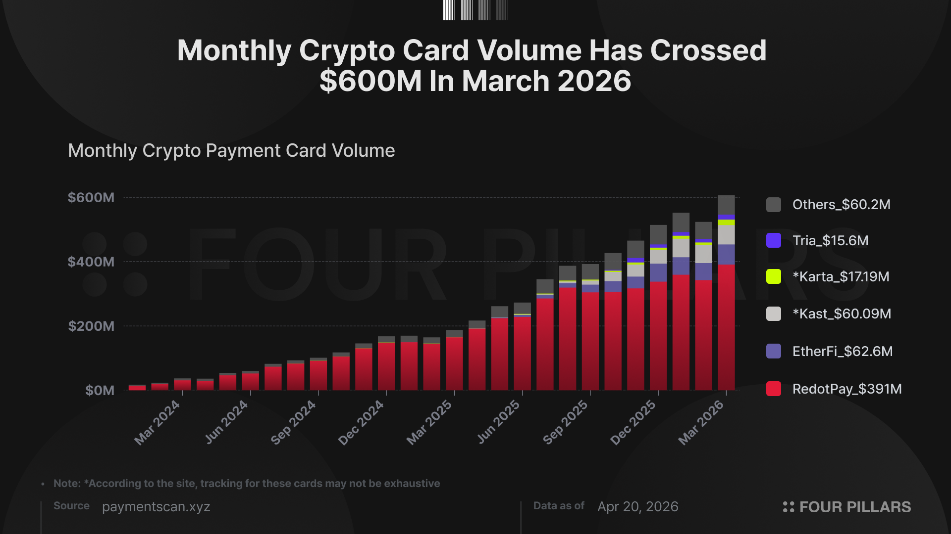

Stablecoin payments have real momentum. Visa settled $4.5B worth of stablecoins last year. Stripe, PayPal, and Revolut are all building stablecoin payment products. Startups like Redot Pay ($4B valuation) and Rain ($2B) reached those numbers fast.

Stablecoins can improve two things in payments: broader accessibility and lower fees with faster settlement. But not all stablecoin payment structures deliver these benefits. Just as there are many ways to process payments, there are many ways to integrate stablecoins, and the differences matter.

If you're considering stablecoin payments for your business, you need to know which user segments your current payment system reaches, where the inefficiencies are, and exactly where in the pipeline stablecoins would help. Without that clarity, you won't capture any real benefit.

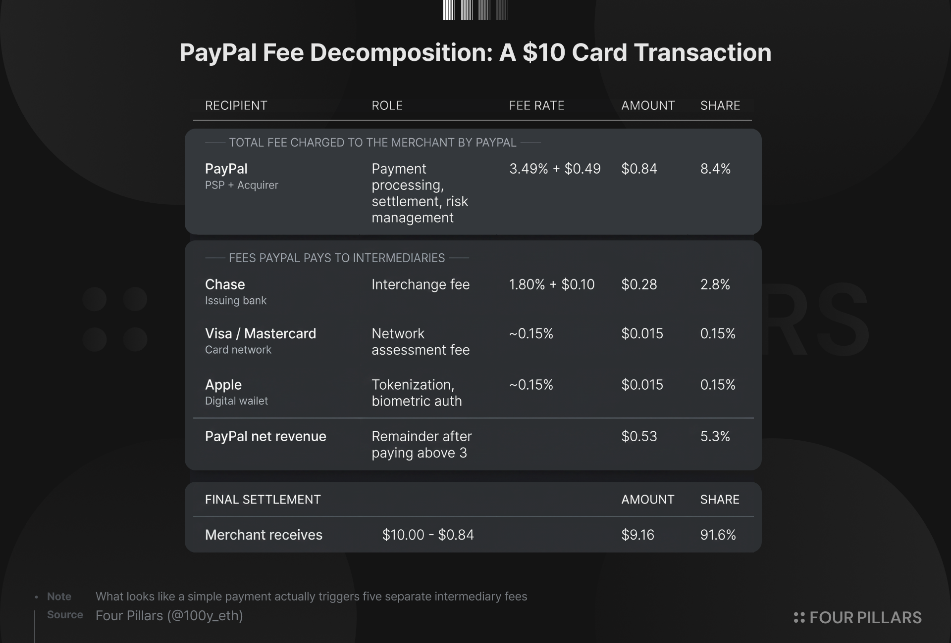

Take a concrete example. A user buys a $10 item online using PayPal via Apple Pay, with a Chase card linked. The fees break down like this:

PayPal acts as both PSP and acquiring bank, charging the merchant 3.49% + $0.49. That's $0.84 on a $10 sale, so the merchant receives $9.16. PayPal's take gets split further:

- Interchange fee: PayPal pays $0.28 (1.80% + $0.10) to Chase, the issuing bank.

- Card network fee: ~$0.015 to Visa or Mastercard.

- Apple Pay fee: ~$0.015 for tokenization and biometric auth.

- PayPal's net: $0.53 from a $10 transaction.

A simple-looking payment, but five intermediaries touched it: PSP, acquiring bank, issuing bank, digital wallet, and card network. That creates real cost and time overhead.

Stablecoins can sometimes reduce these inefficiencies. But they can also add friction through on/off-ramp steps instead of expanding access. The structure matters. Here are the global use cases that illustrate the differences.

2. Global Trends: How Stablecoin Payment Structures Actually Differ

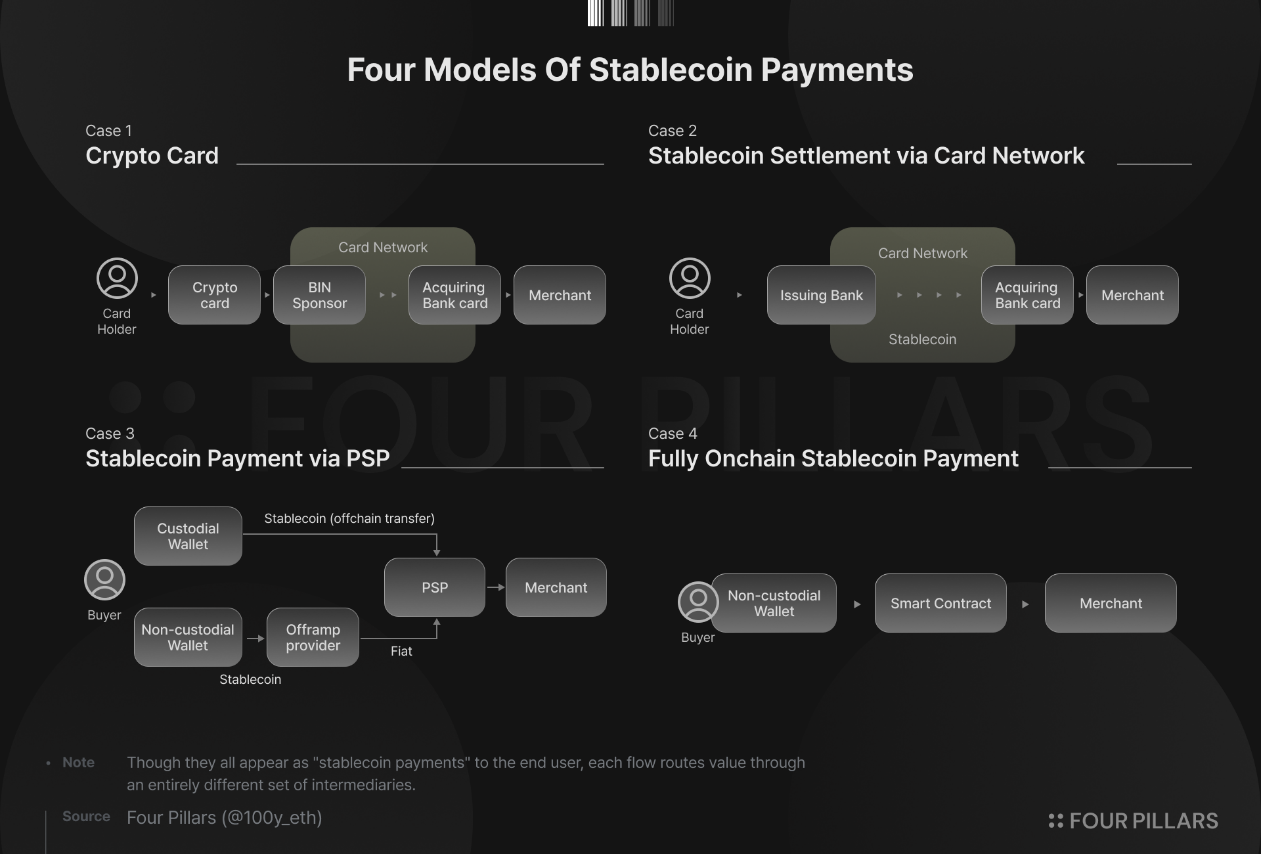

Many global companies are building stablecoin payments: Visa, Stripe, PayPal, Coinbase, Redot Pay. They look similar on the surface, but the actual payment flows differ in important ways.

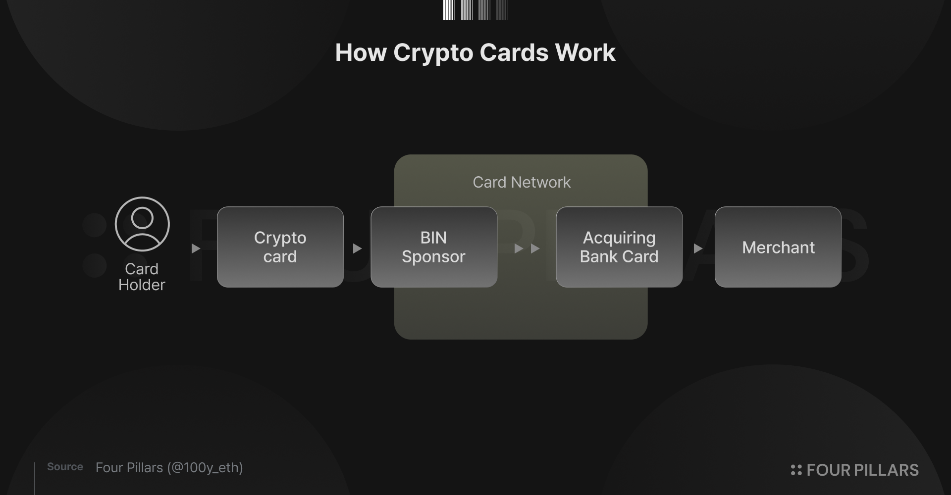

Case 1: Crypto Cards

Crypto cards are growing fast. Crypto.com and Binance launched them first; RedotPay, EtherFi, KAST, MetaMask, and Tria have since followed.

The basic idea: let users spend stablecoins or crypto at any merchant using a card. But crypto cards aren't all built the same. They differ in BIN sponsorship providers, custodial vs. non-custodial models, whether the card network supports stablecoin settlement, and who handles the crypto-to-fiat off-ramp.

Despite these variations, most crypto card payments still flow through Visa or Mastercard via BIN sponsors. So crypto cards don't meaningfully improve cost or settlement time. Their real advantage is reaching crypto-native users who already hold stablecoins.

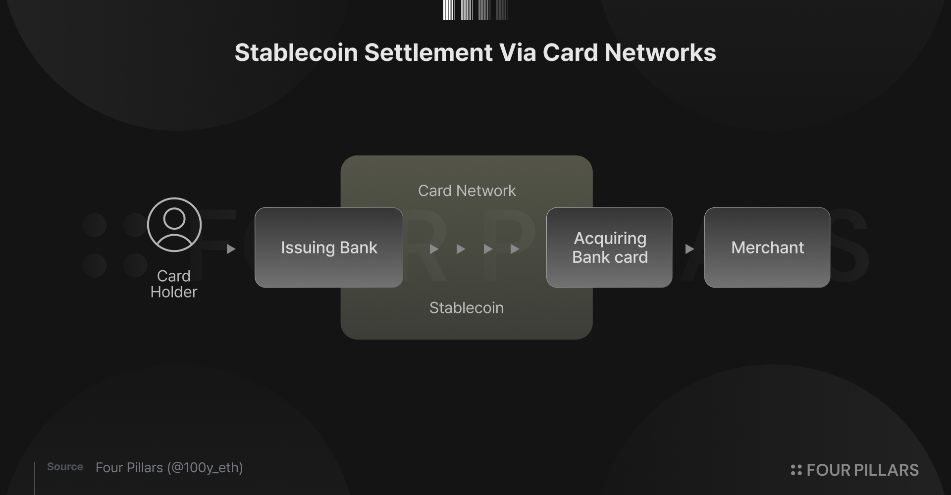

Case 2: Stablecoin Settlement via Card Networks

In traditional card systems, funds move from the issuing bank to the acquiring bank and settle to the merchant in 1–3 days.

Visa and Mastercard now let issuing and acquiring banks settle with each other using stablecoins. Cross River Bank, Lead Bank, Worldpay, and Nuvei already participate. Visa alone settled $4.5B in stablecoins in 2025.

This still runs on the traditional card pipeline, so it doesn't cut costs much. The benefit: it bypasses SWIFT/banking networks and extends settlement windows from 5 to 7 days.

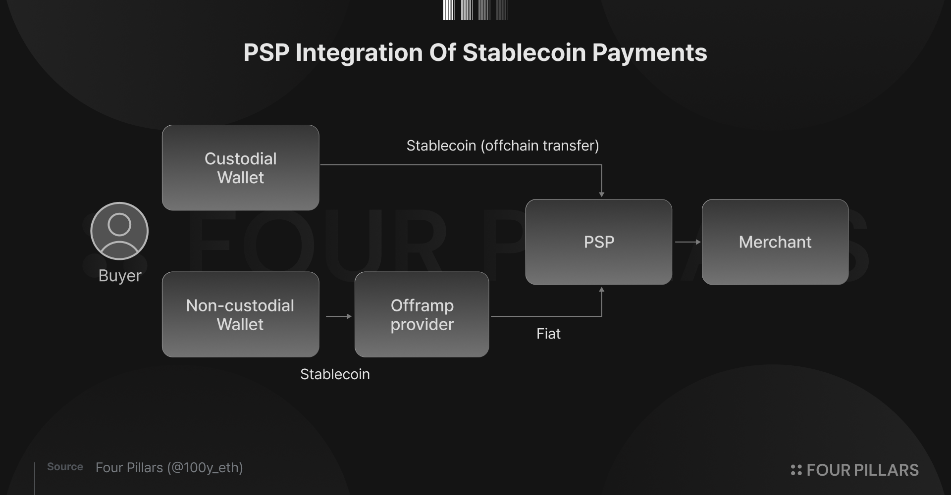

Case 3: PSPs Adding Stablecoin Checkout

PSPs like PayPal and Stripe now let users pay with stablecoins alongside their existing options (app balances, bank accounts, cards). Their approaches differ.

Stripe lets users connect non-custodial wallets for checkout. When someone pays with stablecoins from MetaMask, Stripe's subsidiary Bridge processes the payment and either settles in stablecoins or converts to fiat for the merchant.

PayPal supports both custodial and non-custodial models. PYUSD held inside the PayPal app is custodied by Paxos, and those transactions happen on PayPal's internal ledger without touching the chain. For external wallets, a third-party service (Mesh Connect, Inc.) converts crypto to fiat before completing the transaction.

Non-custodial stablecoin payments through PSPs add off-ramp steps, which can erode fee savings compared to traditional payments. The trade-off: merchants can accept payments from a much larger global user base.

Custodial stablecoin payments work like digital wallet balances (think PayPal Balance) with similar costs. But when merchants receive stablecoins directly, settlement times can drop substantially. And unlike wallet balances, stablecoins work across different platforms.

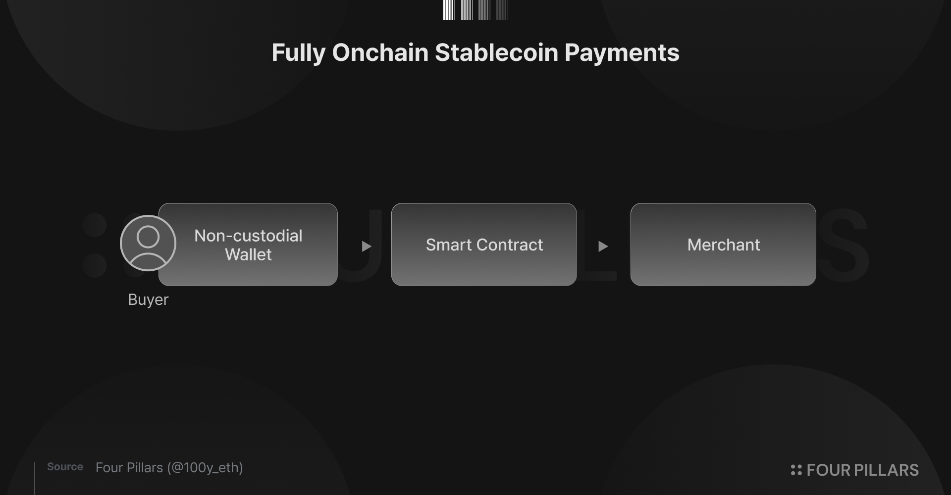

Case 4: Fully On-Chain Payments

This model processes payments entirely on-chain through smart contracts. It's the closest thing to the ideal stablecoin payment vision.

The best example is the Commerce Payments Protocol built by Coinbase and Shopify. A smart contract handles escrow and includes dispute features like refunds and cancellations.

Users connect their wallets at checkout and pay with USDC on Base. The smart contract processes the payment. Merchants can settle in fiat or receive USDC directly.

In this model, Web3 wallets replace issuing and acquiring banks. The blockchain replaces the card network. With most intermediaries gone (except possibly a PSP), costs and settlement times improve by a wide margin.

The Commerce Payments Protocol has processed only 14,573 transactions and $4M in volume about a year after launch. Small scale. But if adoption grows, this is the payment model that threatens the existing structure most directly.

3. Opportunities in the Korean Market: Limited in the Short Term, Boundless in the Long Run

3.1 The Gap Between Potential and Opportunity

Outside of crypto trading, stablecoin payments have the largest potential for mainstream adoption in Korea.

Korea is already a cashless-dominant country. According to the Bank of Korea, cash usage dropped to 15.9% in 2024, down from 41.3% in 2013. Average daily simple payment volume hit KRW 1.0464 trillion in H1 2025. If KRW-based stablecoins enter the payment system, the transaction volume could be massive.

But potential for adoption and actual business opportunity are not the same thing.

3.2 Short-Term Opportunities Are Unclear

In the card industry (Cases 1 and 2), you could either accept stablecoins users already hold or use stablecoin settlement in the merchant settlement process.

The first option needs a mature domestic stablecoin usage environment where many people already use stablecoins daily. That's a high bar. (The alternative is targeting tourists holding stablecoins, which limits the opportunity.)

The second option bypasses traditional banking networks, which could speed up settlement. But competition in the card industry centers on acquiring card users, not merchants. It's not obvious that better fees or settlement times would shift the competitive dynamics.

What about prepaid balance payments like Naver Pay, Kakao Pay, and Toss Pay? It's hard to see where stablecoins add system-level value. Prepaid balance payments are already efficient, with only one intermediary between users and merchants. If stablecoins replace prepaid balances but merchant settlement still happens in fiat, the gains in cost and speed are minimal.

The bottom line for a market like Korea, where payment infrastructure is already strong:

- Users have almost no reason to switch from existing payment methods to stablecoins.

- Since card competition focuses on user acquisition and prepaid systems are already efficient, stablecoin payments face an uphill battle against Korea's mature payment industry.

So where does the opportunity actually lie?

3.3 Long-Term: Build the Stablecoin Ecosystem First

The answer is ecosystem building. Looking at Korea's financial history, banks, card companies, and payment firms have all competed by building proprietary ecosystems. Stablecoins may be the best form of money for exactly that purpose.

Look at PayPal. The existing PayPal Balance is trapped inside PayPal's closed loop. It only works with PayPal merchants, and withdrawing it means navigating complex banking processes. PYUSD breaks that constraint. Users can transfer and pay within PayPal, but they can also withdraw on-chain and use it across DeFi services or for payments in products that have nothing to do with PayPal.

With smart contract integration, PYUSD connects to on-chain investment products, enables micropayment streaming, and makes reward distribution easier. Through PYUSD, PayPal can move beyond its closed system and build a broader global financial network. Users and merchants who see value in the rewards, utility, and cross-platform compatibility will have real reasons to adopt PYUSD.

Applied to Korea: financial companies shouldn't focus narrowly on stablecoin payments. They should take an ecosystem approach that includes payments as one piece. If stablecoin adoption turns existing financial system inefficiencies into real improvements for customers and merchants, adoption will follow naturally, and stablecoin payments will come with it.

3.4 Merchants Should Take Fully On-Chain Payments Seriously

From a merchant's perspective, Case 4 deserves close attention. It replaces all intermediaries with smart contracts and can cut both fees and settlement times by a large margin.

If large retail platforms with high transaction volumes adopted this model, merchants could reduce what they currently pay to card companies, VAN providers, and PG companies. Faster settlement would also improve liquidity.

Consider Starbucks Korea. They push hard on prepaid app balance usage through rewards, trying to reduce fees paid to card companies and PG providers. But customers find Starbucks balances unattractive because the money is stuck inside one app.

If Starbucks Korea adopted an on-chain payment model like Case 4, they could cut fees while giving customers stablecoins that work beyond Starbucks. Both sides win. This is exactly the kind of problem stablecoin payments solve well.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![50% for Ethereum, 50% for Congress [FP Weekly 33]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F1cg9d7msn1d3j2.png&w=1920&q=75)

![Coldcard Got Burned, Coinbase Froze [FP Weekly 32]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fhv83s5msebytml.png&w=1920&q=75)