Table of Contents

- Key Takeaways

- 1. Overview: Structural Characteristics of Deposit Tokens

- 1.1 Deposit Tokens Undervalued Relative to Stablecoins

- 1.2 Asia's Digital Currency Policy Trend

- 2. Global Trends: Three Models by Major Players

- Model 1: Commercial-Bank-Led Single Issuer, JPMorgan Kinexys

- Model 2: Private Consortium, Japan's DCJPY

- Model 3: Central-Bank-Led Public Infrastructure, Hong Kong's Project Ensemble

- 3. Opportunities in the Korean Market: Project Hangang Phase 2

- 3.1 From Phase 1 Pilot to Phase 2

- 3.2 Opportunity 1: Treasury Fund Disbursement (Policy Resource Linkage Scenario)

- 3.3 Opportunity 2: Repo / Treasury DvP Settlement (Tokenized Treasury Linkage Scenario)

- 3.4 Opportunity 3: Cross-Border Treasury Management (Project Agora Linkage Scenario)

- 3.5 Limits and Possibilities of Korean Deposit Tokens: Public Infrastructure Dependency, and the Possibility of Parallel Private Tracks

Researcher

Key Takeaways

- Tokenized deposits are structurally different from stablecoins: stablecoins are primarily a competitive strategy for acquiring new markets, while tokenized deposits are an efficiency strategy for improving existing banking and settlement infrastructure.

- Unlike stablecoins, tokenized deposits can preserve the institutional advantages of bank deposits, including credit creation, deposit insurance, lender-of-last-resort access, and compatibility with existing accounting and compliance systems.

- In Asia, digital currency policy is moving more toward CBDCs and tokenized deposits than private stablecoins, reflecting a market structure where regulation often precedes market formation.

- Global tokenized deposit models can be grouped into three categories: single-bank platforms such as JPMorgan Kinexys, private consortium networks such as Japan’s DCJPY, and central bank-led public infrastructure such as Hong Kong’s Project Ensemble.

- In Korea, the main opportunities for tokenized deposits are likely to emerge from wholesale use cases such as public treasury disbursement, repo and government bond DvP settlement, and cross-border treasury management linked to Project Agora.

This article is adapted from "Korean Blockchain Guidebook for Institutions 2026," jointly published by Four Pillars and Pantera Capital. The full report covers 14 more themes for companies and institutional investors.

1. Overview: Structural Characteristics of Deposit Tokens

1.1 Deposit Tokens Undervalued Relative to Stablecoins

Bank deposit tokens are an efficiency strategy, while stablecoins are a competitive strategy; the two follow separate decision paths. Deposit tokens address internal operational efficiency issues in existing businesses, such as reducing reconciliation costs and shortening settlement times. Stablecoins are focused on capturing newly opening markets through new customer acquisition and churn prevention.

Yet compared to stablecoins, deposit tokens are significantly undervalued. Strip crypto trading out of the $35 trillion stablecoin throughput frequently cited as market entry rationale, and actual payment and treasury activity amounts to only $390 billion, just 1% of the total. Even within that, dollar-denominated stablecoins account for roughly 99%, and non-dollar stablecoins have virtually no presence.

Deposit tokens, on the other hand, carry over the legal status and regulatory infrastructure of the existing banking system. This makes them easier to deploy immediately into already-functioning markets such as treasury disbursement, interbank repo, and large-corporate cross-border settlements. Compared with the competitive capture of new markets, the efficiency optimization of already-operating markets offers more immediate, tangible revenue opportunities, and deposit tokens are considerably overlooked on this count.

Technically, there is almost no functional implementation gap between deposit tokens and stablecoins. The benefits of tokenization, such as atomic DvP, programmable features, 24/7 real-time settlement, and composability, are not properties inherent to stablecoins but general properties of the underlying distributed ledger and smart contracts. Deposit tokens can deliver the same functionality. Where openness creates competitive advantage, such as cross-border settlement and on-chain liquidity, stablecoins hold the edge, which is why the two instruments are shaping up as coexisting by domain rather than substitutes.

The main differences between the two currencies arise from the issuer and the institutional foundation, not from function. Deposit tokens retain banking-specific institutional safeguards intact, including fractional-reserve-based credit creation, deposit insurance coverage, lender-of-last-resort access, and foreign exchange bank legal status.

For the bank, issuing stablecoins is constrained by 100% reserve asset requirements that limit net interest margin and credit creation, whereas deposit tokens preserve the revenue structure based on financial intermediation. For the corporate side as well, deposit tokens are an extension of existing banking relationships, so accounting, tax, and internal controls carry over as-is. Stablecoins require designing everything anew, from asset classification to audit standards, generating separate compliance costs. The operational fit differs sharply.

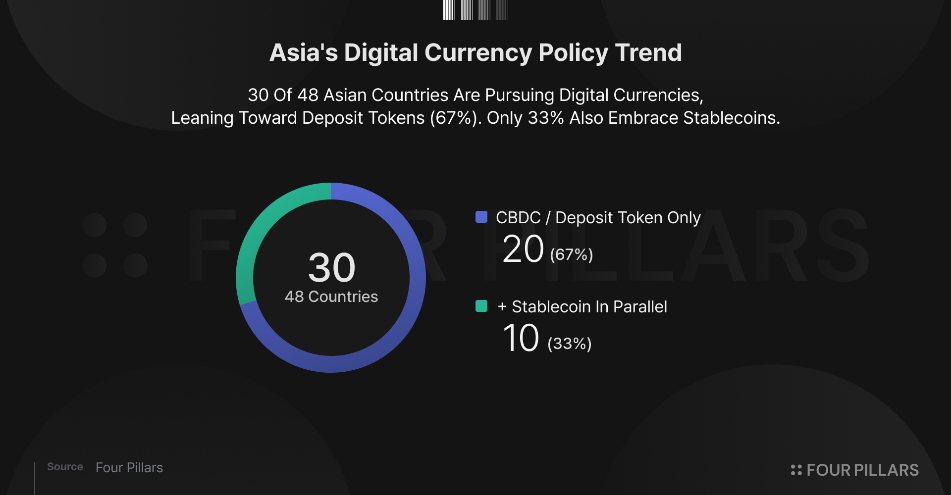

1.2 Asia's Digital Currency Policy Trend

Asian countries are in practice trending toward deposit tokens. Of the 48 Asian countries (UN basis), roughly 30 are pursuing digital currencies, and almost all of these 30 lean toward CBDC and deposit tokens. Japan's DCJPY and Hong Kong's Project Ensemble are building deposit-token-based infrastructure. China has effectively converted e-CNY, originally a central-bank-issued retail CBDC, into a deposit token by incorporating it as a liability of commercial banks. India's central bank (RBI) also launched a deposit token pilot in October 2025 using wholesale CBDC as the settlement layer.

Only 10 countries (33%) are running stablecoins in parallel. Among these, just four (Japan, Singapore, Hong Kong, and the UAE) have established independent legal frameworks. The remaining six (the Philippines, Thailand, Indonesia, Kazakhstan, Uzbekistan, and Kyrgyzstan) remain at the sandbox or pilot level.

This configuration differs from the United States and Europe. The United States banned CBDC development via executive order in January 2025, and the House passed an Anti-CBDC bill the same year (currently under Senate review). Europe is also preparing a digital euro, but the issuance decision has been postponed to after 2029, and it first activated a private stablecoin framework through MiCA. While the United States and Europe have chosen to prioritize private stablecoins, Asia is moving along a path of directly designing digital currencies led by central banks and commercial banks.

Behind this trajectory sit several overlapping layers, including geopolitical configuration, incentives around U.S. Treasury demand, and dedollarization currents. The most important point, however, is the difference in the order of market formation. Unlike the United States, which retrofitted a de facto private stablecoin market with the GENIUS Act after the fact, Asia's digital currency market is forming from the outset as an institution-centric regulated industry. The sequence of institutional permission and market formation is itself different. Where institutions precede markets, instruments that fit existing banking institutions and regulatory infrastructure are inevitably the first to enter the regulated perimeter. The market that will open first to private players may well be deposit tokens, and moving with this in view is warranted.

The same holds from a revenue structure perspective. The stablecoin market is an oligopoly, with Tether and Circle accounting for about 90% of circulation between two issuers. Whether the asymmetric performance of a tiny number of firms is creating a misleading picture of the stablecoin market as a whole deserves a check. Widening the field from stablecoins to the trends and opportunities in deposit tokens is a valid approach for decision-making.

2. Global Trends: Three Models by Major Players

Global cases of deposit tokens compress into three models: (1) commercial-bank-led single-issuer model, (2) private consortium model, and (3) central-bank-led public infrastructure model.

Model 1: Commercial-Bank-Led Single Issuer, JPMorgan Kinexys

JPMorgan started with JPM Coin in 2019, rebranded to Kinexys in November 2024, and in November 2025 launched JPMD on the public blockchain Base and the Canton Network. The Kinexys platform currently processes $5 billion daily and $3 trillion cumulatively, showing demand and market viability for deposit tokens in the institutional wholesale settlement space.

- Corporate Treasury Management: German infrastructure company Siemens (revenues of approximately €78 billion) reported that adopting Kinexys allowed it to reduce its U.S. bank accounts by 50% and save $20 million annually. The result came from eliminating idle funds and buffer deposits across global subsidiaries through 24/7 cash pooling. Ant International, BlackRock, and Mastercard are participating in the same structure.

- Tokenized Repo Settlement: Repo transactions used for short-term financing are processed with tokenized Treasury collateral and deposit tokens. Cumulative processing of $430 billion, shortening existing T+1 settlement to same-day settlement, with Goldman Sachs and BNY Mellon as principal client firms.

- Cross-Border B2B Settlement: JPMD is used in dollar settlement with Coinbase and B2C2. It removes the business-hours constraints and correspondent-bank fees of SWIFT-based foreign remittance.

JPMorgan is not the only bank operating this model. Citi launched in 2024 and provides 24/7 cross-border settlement and liquidity management across five hubs (United States, United Kingdom, Singapore, Hong Kong, and Dublin in Ireland) in five currencies (USD, GBP, HKD, SGD, and EUR). HSBC started tokenized deposit services in Hong Kong and Singapore in 2025, expanded to the United Kingdom and Luxembourg, and extended to the United States and the UAE in April 2026, now supporting five currencies: USD, GBP, EUR, HKD, and SGD. Deposit tokens are becoming standard infrastructure for institutional wholesale settlement among large global banks.

This model operates by a bank placing a proprietary platform on top of its own customer network. JPMorgan built on the institutional client network of its payments business processing $10 trillion daily; Citi, on its global clearing network; and HSBC, on its subsidiary network across 60 countries. The common target is wholesale areas such as cross-border treasury management for multinational corporations and interbank settlement, a market that is easily accessible in practice only to large global banks.

Revenue attaches directly on top of existing banking businesses. Corporate treasury management fees, cross-border settlement fees, and repo and collateral management fees are added, and more fundamentally, corporate deposits remain on the bank's ledger and function as a base for low-cost funding and credit creation. The Siemens case, reducing its U.S. accounts by 50% and concentrating funds at JPMorgan, shows that deposit tokens are becoming a new axis in deposit acquisition competition, not just a payment instrument.

Model 2: Private Consortium, Japan's DCJPY

While the Bank of Japan's CBDC decision has been delayed, private commercial banks moved first. The DCJPY network operated by DeCurret DCP was commercialized in August 2024, with major commercial banks, including MUFG, SMBC, SBI Holdings, Mizuho, and Japan Post, forming a private consortium to participate in DCJPY design.

One live use case is renewable energy certificates (REC). Telecom operator IIJ procures renewable energy certificates for data center customers from JEPX (Japan Electric Power Exchange) and settles them with DCJPY issued by GMO Aozora Bank. The remainder are at the contract or PoC stage:

- Automatic Real Estate Rent Payment: A structure that automates monthly rent payments via smart contracts and uses DCJPY as the settlement instrument. Japan Post Bank and Shinoken Group signed an MOU in November 2025 and are conducting a PoC targeting implementation in 2026.

- Tokenized Securities Settlement: A structure settling asset delivery and payment in tokenized securities transactions with DCJPY. DeCurret signed an MOU in January 2025 with Securitize, which operates BlackRock's BUIDL, and is at the solution development stage.

- Cross-Border Settlement: A structure implementing atomic settlement between DCJPY and foreign bank deposit tokens. SBI Shinsei Bank signed an MOU with Singapore's Partior in September 2025 and is preparing DCJPY issuance during 2026.

- Retail Deposit Tokenization: A structure converting existing bank deposits into DCJPY so they can be used directly in tokenized asset transactions. Japan Post Bank is pursuing its own DCJPY issuance during 2026 along with tokenizing its $1.3 trillion in held deposits.

This model operates in an environment where a single bank does not monopolize the market. It starts as a multi-bank common infrastructure. Japan has three megabanks, MUFG, SMBC, and Mizuho, but no bank has cornered the institutional settlement market alone the way JPMorgan has. DeCurret DCP coordinates, through a common ledger, a settlement market with multi-bank participation that is difficult to form under single-bank leadership. When multiple banks' deposit tokens sit on a common ledger, inter-bank fund movements are processed as atomic swaps, removing from the outset the interoperability constraints that arise when each bank issues only its own deposit token on its own ledger. Participating banks retain their own deposit bases while sharing common network liquidity, and DeCurret DCP secures revenue through infrastructure usage fees and transaction fees.

Model 3: Central-Bank-Led Public Infrastructure, Hong Kong's Project Ensemble

The Hong Kong Monetary Authority (HKMA) launched Project Ensemble in March 2024 and entered the EnsembleTX live pilot in November 2025. HKMA issues a wholesale CBDC, and seven commercial banks, including HSBC, Standard Chartered, and Bank of China Hong Kong, each issue their own deposit tokens in a two-tier structure. Added to this are asset managers and infrastructure operators such as BlackRock, Franklin Templeton, and HKEX, unfolding across four tracks.

- Fixed-Income and Fund Settlement: Issuance and settlement of digital green bonds worth HKD 10 billion processed through commercial bank deposit tokens.

- Liquidity Management: Supports real-time fund movement for corporate treasury. As the first commercial case, an HKD 3.8 million live transaction took place between HSBC and Ant International.

- Green Finance: A structure settling carbon credits and green bond transactions with deposit tokens.

- Trade Finance: Letters of credit and trade-related payments processed through deposit-token-based atomic settlement.

This model has the central bank directly participating as the anchor of interbank settlement. The two-tier structure lays wholesale CBDC as the settlement layer and places commercial bank deposit tokens on top. Commercial banks each issue their own deposit tokens, but whenever they are exchanged, final settlement occurs in central bank money. Interbank interoperability, singleness of currency, and elimination of final settlement risk are all built into the structure.

Unlike a multi-bank consortium coordinated by a private operator, the settlement anchor here is a central bank liability. The limits are that the central bank's policy will is a prerequisite for infrastructure operation, and that private innovation incentives are restricted. Issuing banks, participating asset managers, and use cases all go through regulatory approval in a permissioned ledger structure, so the path JPMorgan took to expand JPMD onto a public chain and secure openness is difficult to realize inside this structure.

3. Opportunities in the Korean Market: Project Hangang Phase 2

Korea's "Project Hangang" corresponds to Model 3. The Bank of Korea issues a wholesale CBDC, and commercial banks issue deposit tokens in a two-tier structure identical to Hong Kong's Ensemble.

3.1 From Phase 1 Pilot to Phase 2

Project Hangang Phase 1 (April to June 2025) was a functional verification pilot centered on retail small-value payments. Functional verification was completed (81,000 digital wallets opened, approximately KRW 1.64 billion in conversion volume), but the dominant assessment was that the differentiated benefits of deposit tokens are not large with retail small-value payments alone. Disagreements arose over infrastructure investment cost burden and the absence of a revenue model for the banking sector, and the second test has been tentatively suspended.

The upcoming Phase 2 addresses these limits by shifting focus to wholesale domains. Participating banks have expanded to nine, and with the addition of a public fiscal disbursement use case, the Bank of Korea has indicated a direction to disburse 25% of the government budget via deposit tokens by 2030. Based on the projected total expenditure of KRW 700 trillion in 2030, this corresponds to approximately KRW 175 trillion annually. Phase 2 therefore reflects a shift in recognition: profitable use cases sit in wholesale domains such as public finance, institutional wholesale, and large-corporate treasury management, rather than retail small-value payments.

The market opportunities that will open once the Phase 2 pilot wraps up and CBDC and deposit tokens take hold as commercial infrastructure compress into three points. Starting with banks, which are the most direct, securities firms, asset managers, large-corporate treasuries, and fintech operators can each expect a market with opportunities in different domains.

3.2 Opportunity 1: Treasury Fund Disbursement (Policy Resource Linkage Scenario)

Processing treasury fund disbursement on the deposit token ledger is set as the goal of Project Hangang Phase 2. When fiscal disbursement flows move onto the deposit token ledger, the market that opens to commercial banks extends beyond the digital expansion of treasury agent business into a structural shift in competition for low-cost deposits.

The contest for local government treasury mandates currently unfolds on a four-year cycle at the bank headquarters level. In the 2022 Seoul City Primary Treasury bid, Shinhan Bank offered a contribution of approximately KRW 300 billion, and despite bleeding more than KRW 500 billion including the Secondary Treasury, Shinhan, Woori, KB, and Hana have formed task forces and thrown themselves into the 2026 reselection competition.

The tangible gains banks obtain come from the low-cost deposit base provided when the annual budget of KRW 51 trillion secured through the Seoul City Treasury agreement is parked as demand-type public deposits (Seoul City Treasury public deposits at 2.52%, roughly 0.5 to 1 percentage point below market time deposits). On top of this, chain sales of financial products targeting city and provincial affiliates and public-sector employees, strengthening of public-interest and ESG portfolios, and cross-selling of credit cards and loans form the backdrop for contribution competition on the order of KRW 500 billion.

Deposit-token-based treasury fund disbursement is highly likely to unfold in a configuration where banks that have laid the infrastructure first can participate in the competition. Under the Bank of Korea's direction to disburse 25% of the government budget through deposit tokens by 2030, a fiscal disbursement flow of approximately KRW 175 trillion annually will move onto the deposit token ledger. Given the nature of treasury funds, where receipts and expenditures circulate throughout the year, the average daily balance sits at one to two months' worth of annual disbursements, roughly KRW 15 to 30 trillion. This low-interest public deposit becomes a new deposit base that only banks with deposit token infrastructure can secure.

For reference, Tokyo has announced a program providing subsidies of up to several hundred million won per project to companies using yen stablecoins as payment and remittance instruments. The policy intent of building a digital currency ecosystem is identical, but in Korea, policy resources are likely to concentrate on CBDC and deposit tokens rather than stablecoins under Bank of Korea leadership. During the transition period, public funds will bear part of the cost of digital currency adoption, and entities that invest preemptively in infrastructure aligned with this support structure can capture a first-mover position in the B2G business domain.

3.3 Opportunity 2: Repo / Treasury DvP Settlement (Tokenized Treasury Linkage Scenario)

The second opportunity sits in the use case most likely to activate first as the STO(Security Token Offering) market opens. In January 2026, the amendments to the Electronic Securities Act and the Capital Markets Act passed the plenary session of the National Assembly, recognizing distributed ledgers as a legally effective form of securities record-keeping and allowing investment contract securities to be distributed through securities firms. Enforcement is tentatively scheduled for January 2027, and detailed enforcement ordinance preparation and OTC exchange authorization procedures are underway under the Financial Services Commission's leadership.

The issue is that Korea's STO discussion has been focused on non-financial fractional investment such as real estate, art, and music royalties, due to the influence of the initial policy trend. The limits of this asset scope restriction are now being officially acknowledged in the industry. The NXT and KDX consortia are expanding into bond and equity fund tokenization, and the Financial Services Commission has also left open the possibility of expanding the scope of tradeable assets in the token securities secondary market through the enforcement ordinance. Mirae Asset Securities has in fact issued digital bonds worth KRW 100 billion. On top of this current, the interbank repo DvP settlement where tokenized Treasuries meet deposit tokens is likely to emerge as the substantive first large market.

Based on Korea Securities Depository data, the average daily balance of interbank repo transactions in the fourth quarter of 2025 was KRW 265.7 trillion (up 17% year-on-year), and total transaction amount for the quarter was KRW 12,538 trillion, a record high. Of the securities traded, Treasuries account for 53.9% (KRW 152.8 trillion), of trading currencies, the won accounts for 87.2%, and of tenors, one-day paper accounts for 94%, making it an ultra-short-term market. Shifted to tokenized Treasuries and won-denominated deposit tokens, it is the market structure with the highest fit, and being an ultra-short-term market centered on one-day paper is precisely the condition where the utility of atomic DvP, with assets transferring simultaneously with settlement, is most visible.

When this transition is applied to the Korean market, utility by principal actor diverges as follows:

- Securities Firms: Securities firms have operated leverage rotation as a main proprietary trading method, financing repo funds using held Treasuries as collateral to purchase new Treasury positions, which they again finance through repo. Once atomic DvP is introduced, the intraday buffer tied up in this rotation shrinks, more positions can be run on the same equity capital, and trading spread revenue can expand.

- On top of this, deposit token settlement infrastructure becomes a settlement leg that lifts the monetization of already-built STO platforms. Large firms such as Mirae Asset, Shinhan Investment, Korea Investment, KB, and NH have been building token securities issuance infrastructure since 2023 through in-house development or consortia, and two consortia, KDX and NXT, are competing for preliminary OTC exchange authorization. Once payment settlement of these STO platforms is layered on the deposit token ledger, a structure opens where intermediation fees begin to be generated in earnest.

- Asset Managers: Asset managers, especially MMFs, which account for roughly 30% of total repo purchases, operate by placing funds in repo overnight and redeeming them. Once atomic DvP of deposit tokens and tokenized Treasuries is introduced, reallocation of overnight standby funds becomes real-time and redemption delay risk disappears.

- And once won-denominated deposit tokens take hold as an institutional settlement instrument, the foundation for designing new products that tokenize won MMFs and supply them as institutional collateral also opens up. The trend of tokenized MMFs taking hold as institutional trading collateral assets is clear, with BlackRock BUIDL and Franklin Templeton BENJI circulating for purposes such as derivative margin and repo collateral. Korean asset managers are positioned to preempt the same product structure in a won-denominated context.

- Commercial Banks: Which bank's deposit token the payments for repo and tokenized securities transactions flow into determines the standard for the institutional settlement rail, and those funds naturally accrue to that bank's deposit base. Hong Kong has already formed a configuration where seven banks, including HSBC, Standard Chartered, and Bank of China (Hong Kong), each issue their own deposit tokens on EnsembleTX and interconnect institutional settlement rails. In Korea too, once repo DvP and STO settlements begin taking place on the deposit token ledger, which commercial bank first secures that standard determines the recipient of settlement-related institutional deposits.

3.4 Opportunity 3: Cross-Border Treasury Management (Project Agora Linkage Scenario)

The third opportunity opens on the premise of a cross-border extension of the Hangang Project infrastructure. The Bank of Korea has joined Project Agora, which brings together BIS and seven central banks from the United States, United Kingdom, Japan, France, Switzerland, Mexico, and other countries, and it is envisioning a scenario connecting the Hangang platform to an international multi-bank settlement network.

Agora was officially launched by BIS in April 2024, went through the design and prototype construction stages in 2025, and is approaching the first report release in the first half of 2026, with actual commercialization timing still uncertain. Once this infrastructure opens, the substantive utility of deposit tokens from a cross-border perspective will show up at two points:

- Buffer Reduction for Overseas Subsidiaries of Large Corporations: Due to cash pooling limits under the Foreign Exchange Transactions Act, obligations to report overseas deposits and remittances, and FX settlements bound to business hours, overseas subsidiaries of multinational large corporations such as Samsung, Hyundai Motor, SK, and LG constantly maintain buffer deposits that exceed operational necessity. Once the Hangang to Agora network provides 24/7 atomic settlement, these buffers cycle back to headquarters in real time, group-wide liquidity turnover improves, and mid-sized trading firms also see structural reduction of trade receivables turnover burden as trade payments settle in deposit tokens.

- Continuity of Legal Framework: Because the reporting, limit management, and disclosure obligations required by foreign exchange law are automatically processed within the deposit token infrastructure, corporate treasury teams absorb only the benefits of deposit tokens while keeping their existing accounting, tax, and audit systems. Stablecoins can perform the same function, but issuers do not hold foreign exchange bank status, so there is no legal basis to automate foreign exchange law compliance inside the institution, and firms must build a separate compliance framework anew. Stablecoins hold the advantage in cross-border free circulation, but large-corporate treasury operating under foreign exchange law regulation is a market with different required conditions.

Overseas, HSBC launched its "Tokenized Deposit Service" in Hong Kong in May 2025, expanded to Singapore, the United Kingdom, Luxembourg, and the United States supporting HKD, USD, SGD, GBP, and EUR, and processes Ant International's global treasury transfers within its own network.

Firms consolidate bank accounts that had been distributed across multiple countries due to time zones and batch processing into a single network and cut treasury management costs through 24-hour real-time transfers. For the bank, this draws overseas subsidiary deposits of firms that had been scattered across competing banks into its own network, and technical integration with ERP locks in corporate banking relationships.

If domestic institutions secure services of the same structure first at the point when the Hangang to Agora network goes into full operation, they can pursue carrying this business rail in won-denominated form.

3.5 Limits and Possibilities of Korean Deposit Tokens: Public Infrastructure Dependency, and the Possibility of Parallel Private Tracks

The three opportunities from deposit tokens we have examined share a common limit. They all operate on top of permissioned public infrastructure run by the Bank of Korea. This approach guarantees final settlement stability on a public foundation, but the central bank's policy will becomes a prerequisite for infrastructure operation. The timing of Hangang Phase 2 commercialization, cross-border expansion (Project Agora), and approval of permitted use cases are all matters decided by regulatory authorities, leaving private actors little room to independently attempt asymmetric business speed or openness.

Behind the fact that the weight of the current Korean financial market is tilted toward won stablecoins, the narrowing of the deposit token path to a single public project is also at work. With no room for private banks and fintech operators to move autonomously in the deposit token domain, alternatives inevitably tilt toward stablecoins.

The stablecoin path itself, however, involves non-trivial costs. Issuers must design a new regulatory framework including capital, reserve assets, and disclosure requirements, and firms must also build separate accounting and tax systems aligned with asset classification. Deposit tokens, on the other hand, can reuse banking regulatory infrastructure such as fractional-reserve-based credit creation, deposit insurance, reserve requirements, and foreign exchange bank status as-is, and on the corporate treasury side, since they are an extension of existing banking relationships, separate build-out is minimized. For the industry as a whole, having the path with comparative advantage excluded from the choice set from the outset is a regrettable outcome.

Project Hangang has presented the Bank of Korea led two-tier structure of wCBDC and deposit tokens as a policy trend since 2023, and preparations are underway from the Phase 1 retail pilot through Phase 2 wholesale domain expansion. Demanding a redesign of this path itself is unrealistic.

But the next stage, once public infrastructure enters commercial operation, deserves consideration alongside parallel private-led tracks. In Japan, the Bank of Japan's CBDC research and DCJPY (operated by DeCurret DCP) coexist, and in Hong Kong, HKMA's Project Ensemble and HSBC's own ledger-based tokenized deposit service coexist. Most developed countries, including Hong Kong, the United Kingdom, Germany, Switzerland, and Australia, operate central-bank-led public tracks and private tracks in parallel. In these countries, public infrastructure construction is not a frame that excludes private deposit token issuance, and commercial banks selectively use the two paths depending on use case and customer.

The potential of the deposit token market is clear. Between the second half of 2026 and 2027, as Hangang Phase 2 enforcement and the finalization of STO legislation enforcement ordinances overlap, the initial shape of the deposit token market will take form. While Project Hangang firms up the public foundation, commercial banks, securities firms, asset managers, large corporations, and fintechs should actively review how to use deposit tokens on their respective business rails.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![50% for Ethereum, 50% for Congress [FP Weekly 33]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F1cg9d7msn1d3j2.png&w=1920&q=75)

![Coldcard Got Burned, Coinbase Froze [FP Weekly 32]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fhv83s5msebytml.png&w=1920&q=75)