Table of Contents

- Key Takeaways

- 0. Introduction: Why Lido, Again

- 1. Lido from Its Beginning to Today

- 1.1 The Founding Context and the Birth of Liquid Staking

- 1.2 Rapid Growth Before the Merge and the Multichain Expansion Attempt

- 1.3 After Shapella: Lido V2

- 1.4 Establishing Lido's Identity: Focusing on Ethereum

- 1.5 The Era of V3, Earn, and Institutional Products

- 2. How Lido Works: Protocol and Infrastructure

- 2.1 The ETH Staker Flow in Lido

- 2.2 Node Operators and Withdrawal

- 2.3 The Lido Oracle System

- 2.4 The Staking Router

- 2.5 The Curated Module

- 2.6 The Simple DVT Module

- 2.7 The Community Staking Module

- 2.8 Changes to the Lido Core After Pectra

- 3. What Lido Offers: New Product Lines

- 3.1 Lido V3 and stVaults: Customized Staking on Shared Liquidity

- 3.2 Lido Earn: Product Expansion Beyond Staking

- 4. Who Owns and Operates Lido: Discourse, Governance, and Token

- 4.1 Is Lido Moving Toward Credibly Neutral Infrastructure

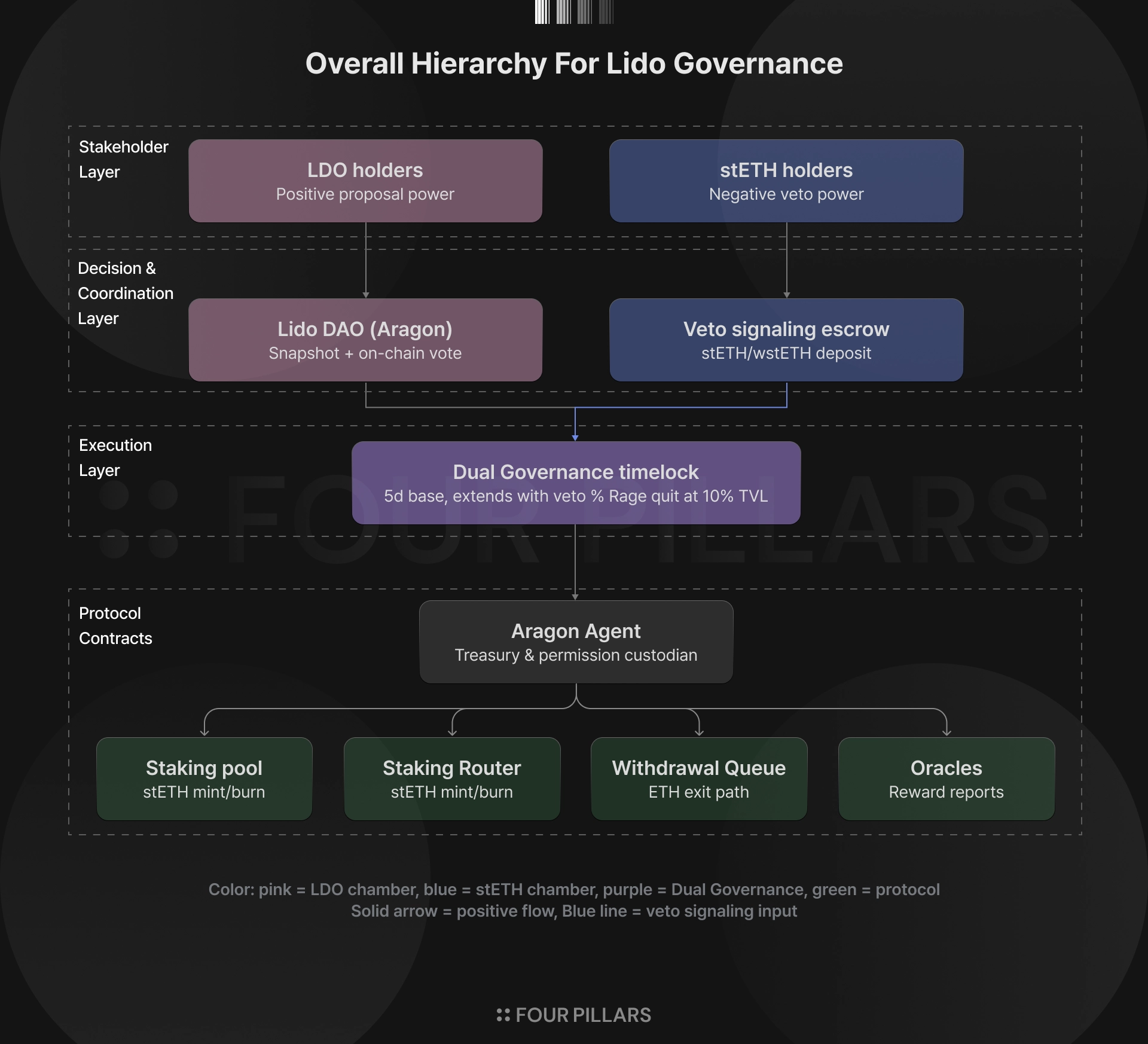

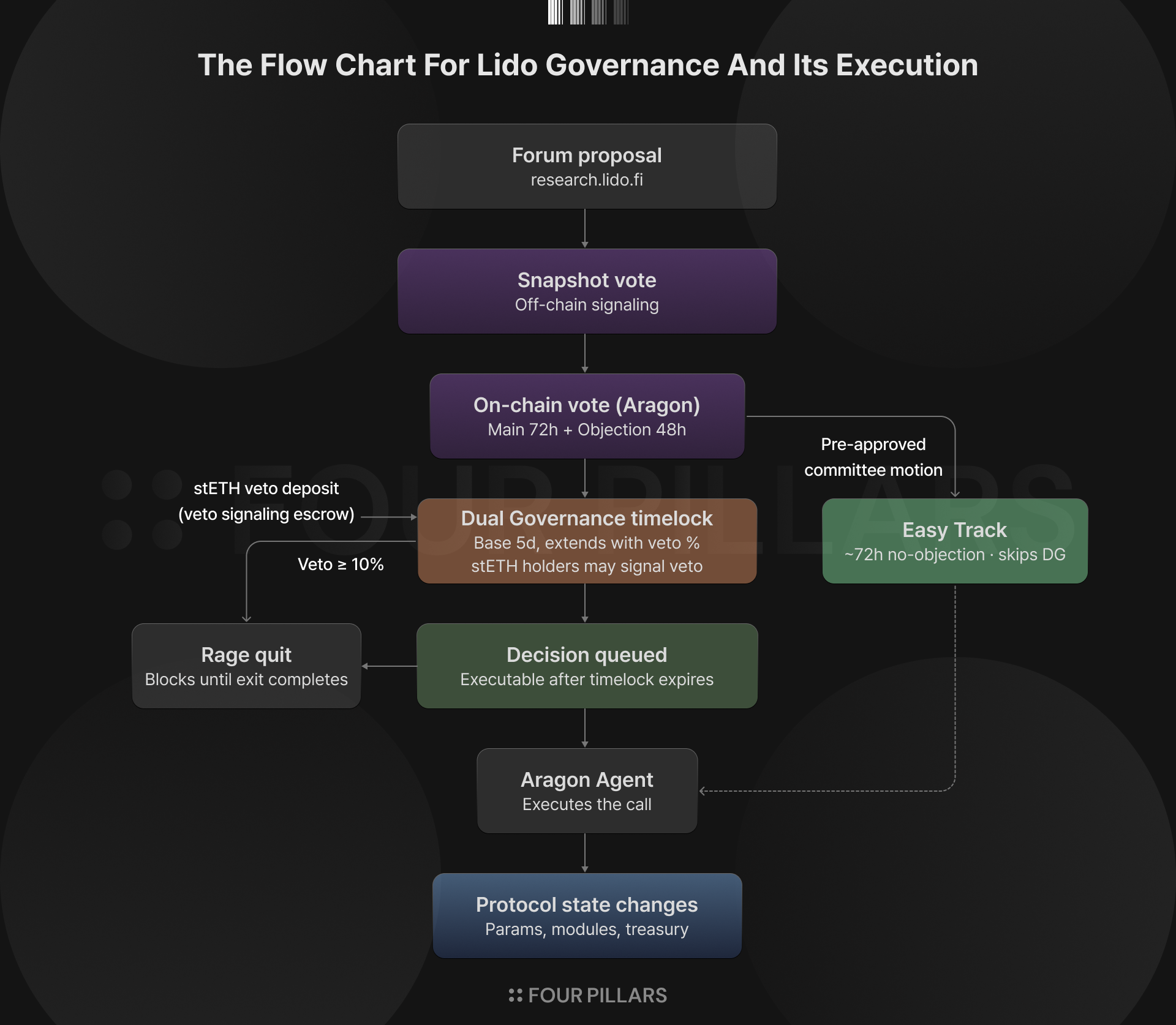

- 4.2 The Lido Governance Framework

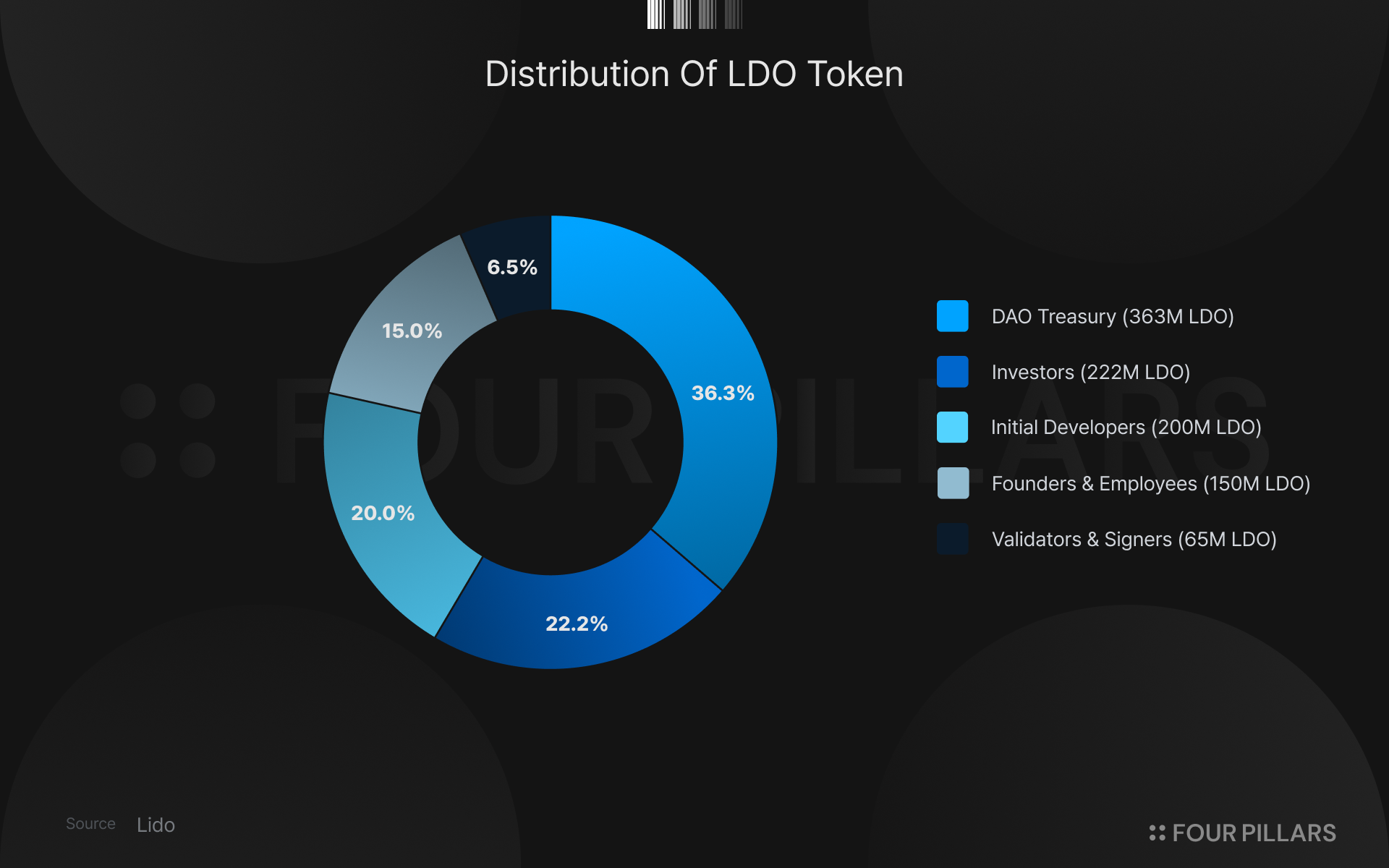

- 4.3 The Economic Structure of the LDO Token

- 4.4 The Five-Year Journey and Its Lessons

- 5. Lido's Next Stage

- 5.1 The Competitive Landscape of the Ethereum Staking Market

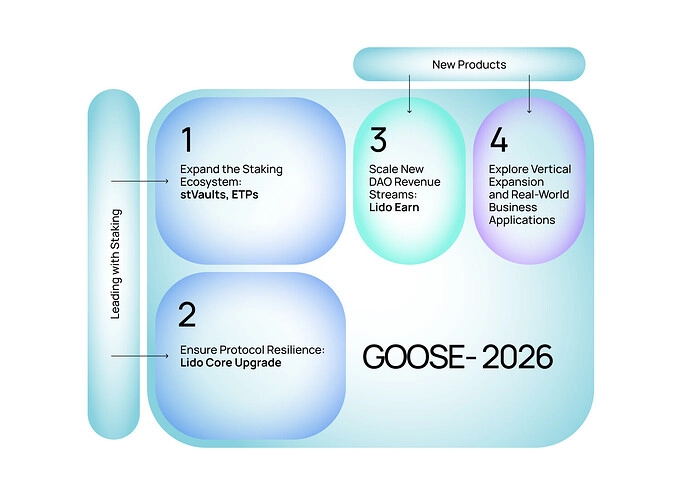

- 5.2 GOOSE-3

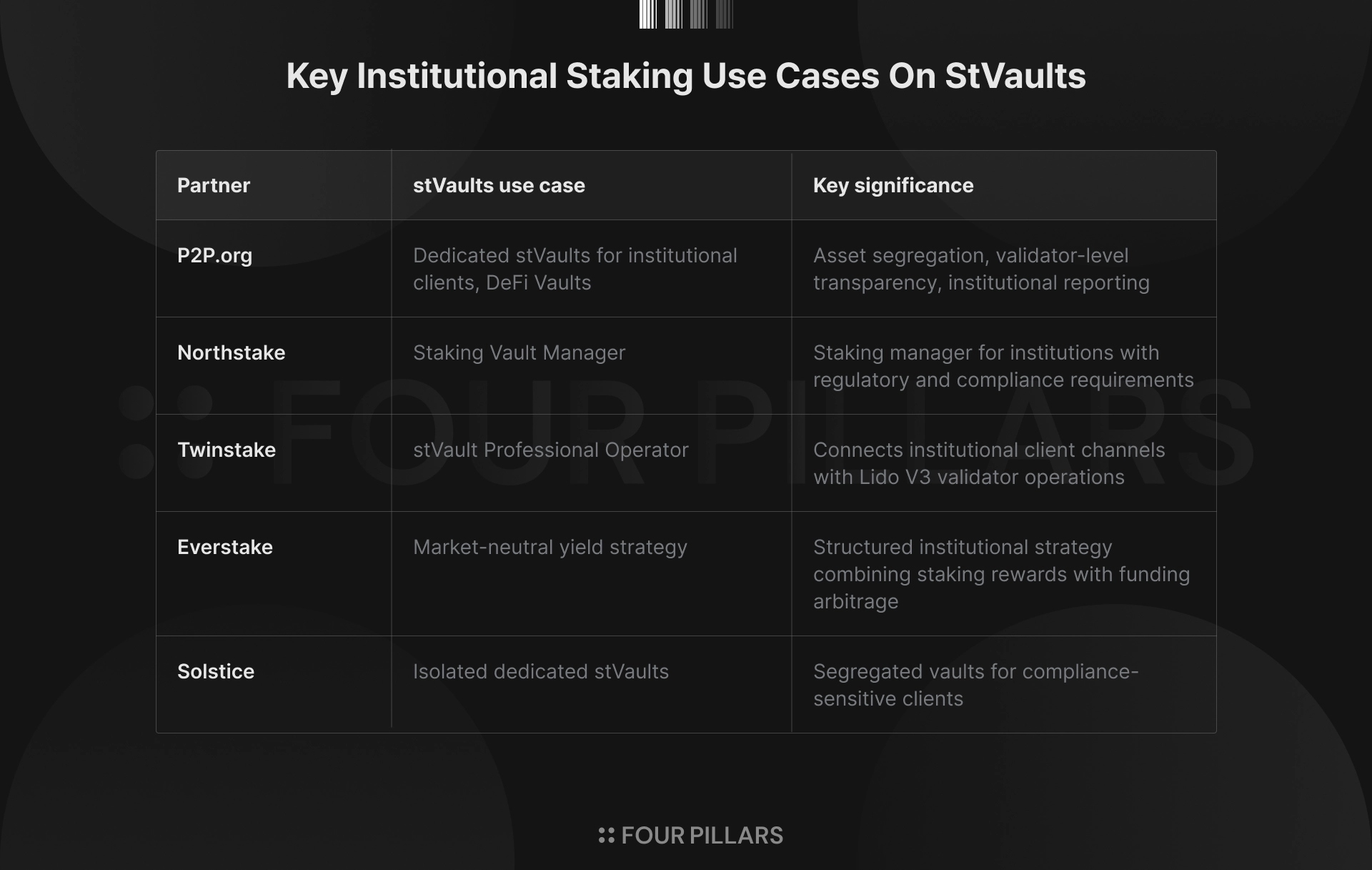

- 5.3 Institutional Staking and Regulated Products

- 5.4 Ethereum's Changes and Lido

- 6. Closing

Key Takeaways

- Understanding Lido lets you understand the changes in the Ethereum staking market and DeFi infrastructure. This article covers how Lido popularized liquid staking by solving the high barrier to entry and the liquidity problem of early Ethereum staking, and how a protocol once criticized as a symbol of centralization risk is evolving into core staking infrastructure aligned with Ethereum's direction of decentralization.

- Lido's history runs alongside the process by which the Ethereum staking market matured through experiment and crisis. Having grown by solving the early user experience problems, Lido went through several risks and learned from them, evolving into more sophisticated staking infrastructure.

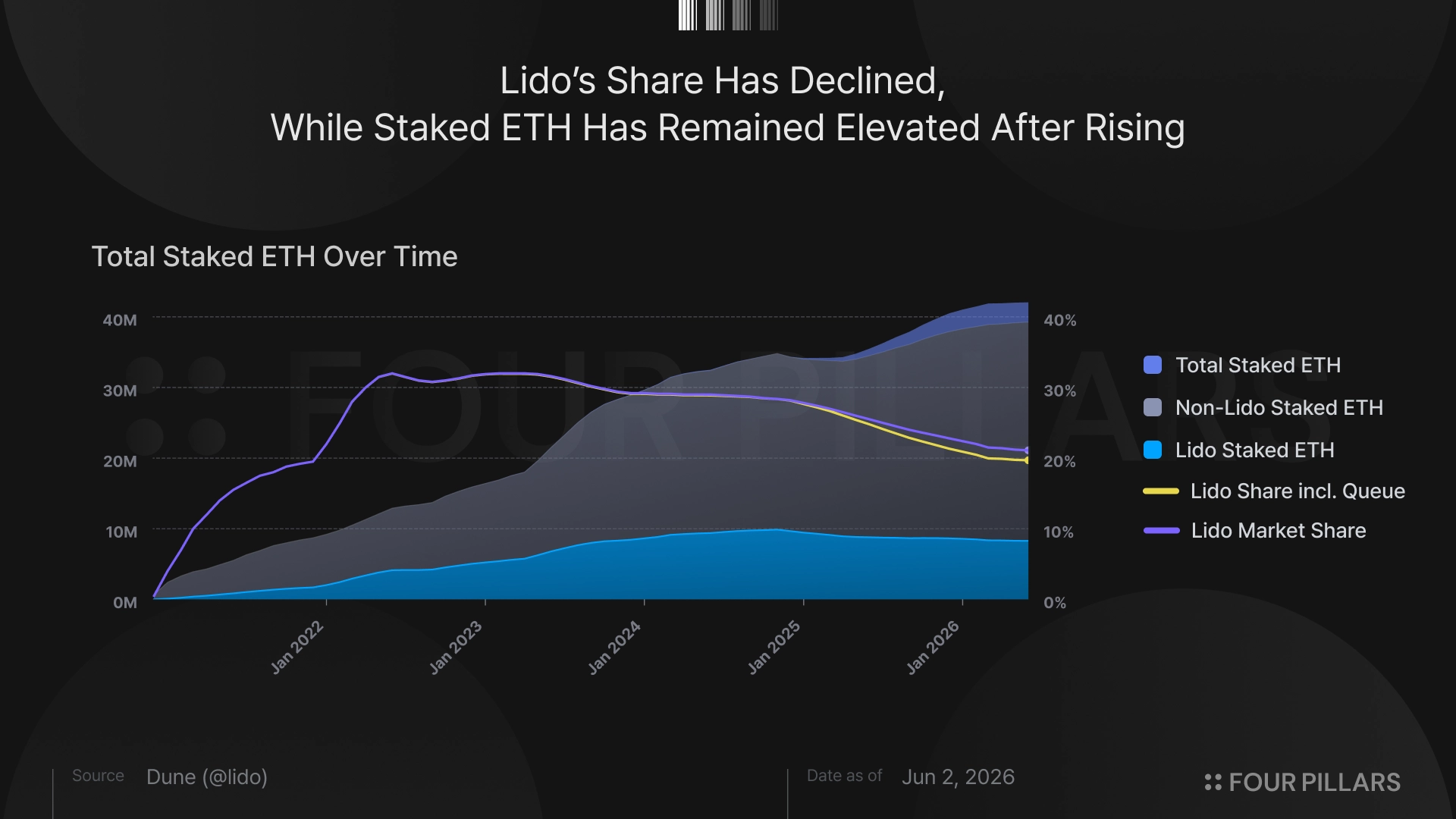

- Although Lido protocol's market share has declined significantly since its 2023 peak, its staked ETH has remained relatively resilient, staying near historical highs. This means not so much a weakening of Lido's competitiveness as the rapid maturing of the Ethereum staking market. The differentiation of the staking service itself is leveling off, and today's staking market is no longer a simple competition over share among protocols. It should be seen as a market differentiated by target user segment. Lido too is now expanding from a single liquid staking product into a platform on which various staking demands can sit.

- Lido protocol's decentralization is not a finished state but a process of continually coordinating different trust models and interests. Lido has gradually differentiated its modules, governance, and operating entities, distributing power and accountability more widely.

- Lido's next task is to be redefined as institutional onchain/DeFi infrastructure suited to a changing Ethereum era. As market demand and Ethereum itself change rapidly, Lido's future depends on how safely it can absorb and productize the market's changes. This is why Lido is worth looking at again now. Tracing Lido's history and changes lets you understand, in compressed form, how Ethereum financial infrastructure has been productized, and gauge what form the next standard, demanded by the new institution-centric crypto demand, will take.

0. Introduction: Why Lido, Again

Understanding Lido tells you a great deal about the Ethereum staking market. Lido is the most important protocol on Ethereum. It was the single biggest force in bringing Ethereum staking to a mainstream audience, and it is the foundation of Ethereum's DeFi money lego.

Around 2022, when Lido's market share crossed 30%, the framing that came up most often inside and outside the Ethereum community was that "Lido is the enemy of Ethereum decentralization." In that period, whenever Ethereum's PoS (Proof of Stake) mechanism came under attack on decentralization grounds, Lido was named alongside it and treated as if it were the enemy of decentralization.

As of 2026, though, Lido has become a key driver of the decentralization of the Ethereum staking and validator network. It institutionalized DVT (Distributed Validator Technology) at the protocol level, built an ecosystem with hundreds of participating node operators, and through the CSM (Community Staking Module) opened a path for anyone to participate permissionlessly as an Ethereum operator with a small amount of capital.

Lido is evolving along two axes. The first is functional evolution: the process by which a protocol once criticized as a centralizing factor in Ethereum was able to position itself as a leader in decentralization through specific design choices and institutional mechanisms. This is not a claim that Lido has fully solved its centralization risk. What deserves attention is how Lido has worked through that centralized risk and changed its character.

The second axis is the evolution of its target users. Lido started by reinventing the staking UX for retail users. It solved the staker UX problems of early Ethereum: that you could only participate in staking in units of 32 ETH, that staked Ethereum could not be used, and that the absence of protocol-level delegation forced stakers to run nodes themselves. Today Lido is expanding from a service for retail users into a staking platform for institutions.

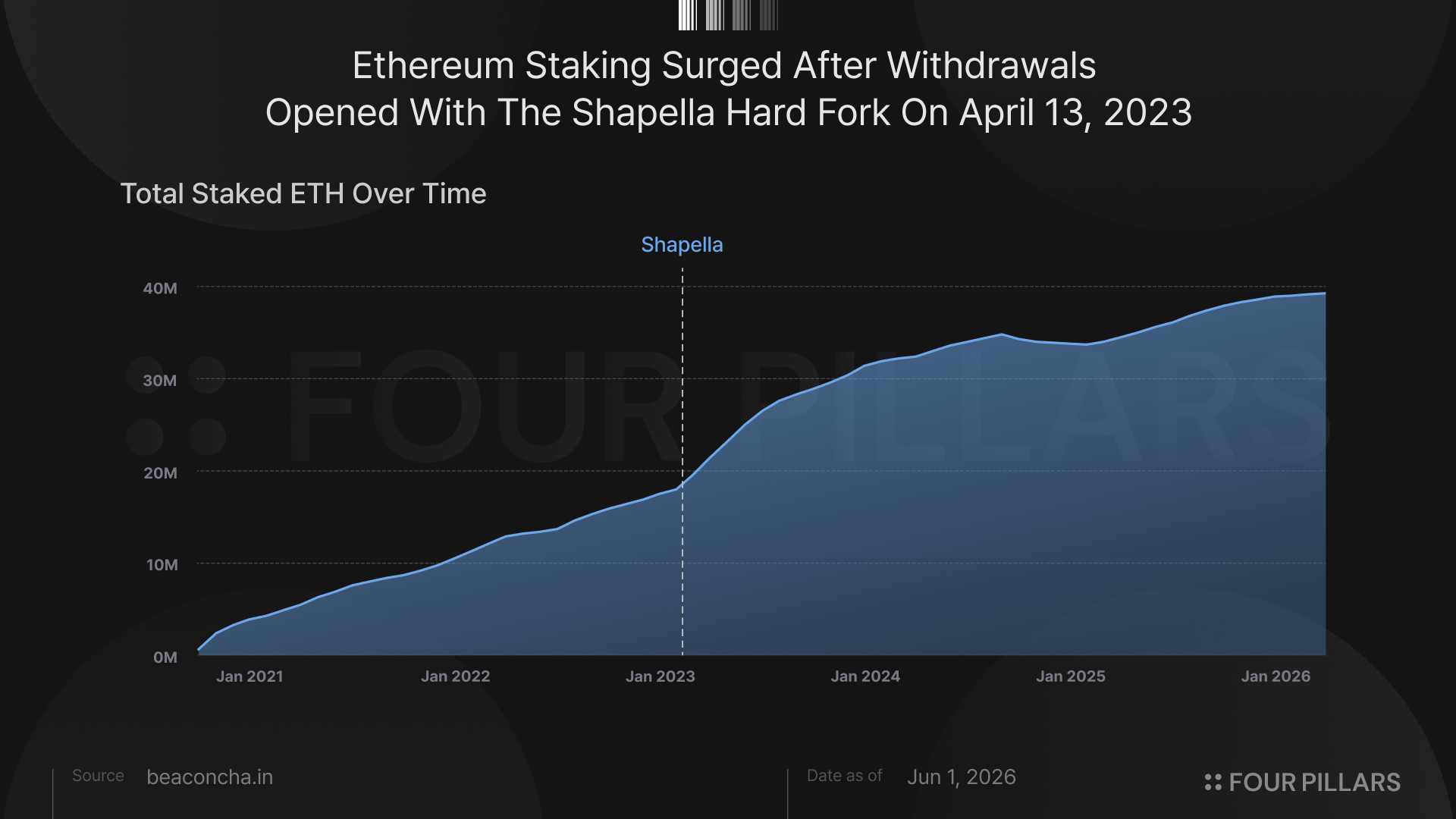

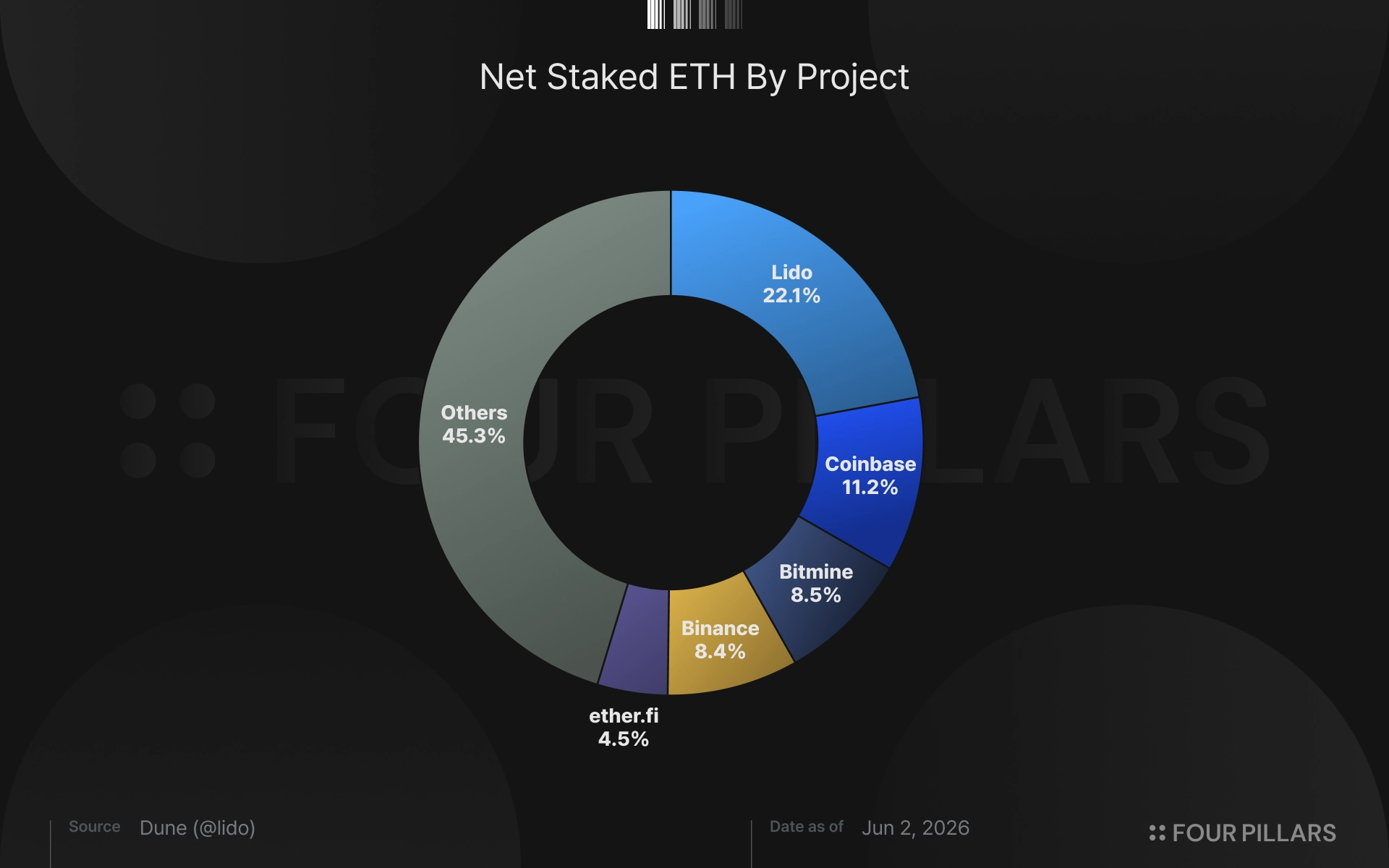

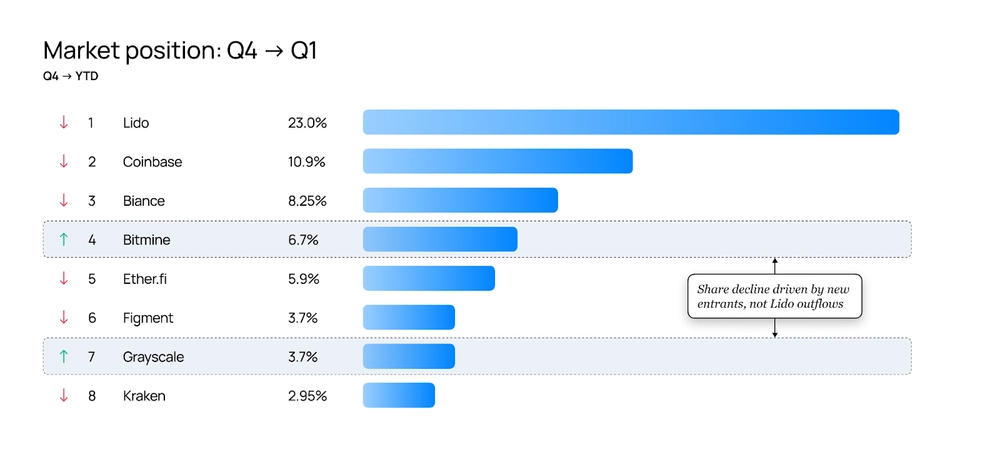

Lido's share, which once operated 33% of all staking on the Ethereum network, has come down to the low 20% range as of 2026. On the surface, this decline looks like a crisis for Lido. But the shift is closer to a signal that the Ethereum staking market is maturing.

Lido's recent sharp drop in share is tied to the direct staking entry of large institutional players such as BitMine and staking ETFs. Large institutions began running validators directly rather than going through an LST like Lido, while exchange-based staking products and LRT (Liquid Restaking Token) protocols are absorbing different user segments. In other words, Lido's declining share shows that the Ethereum staking market and its users have entered a stage where demand is no longer met through a single channel. Lido's relative share has fallen, but the range of problems it addresses has actually widened.

Source: beaconcha.in

Today's crypto market is changing faster than ever. In this market, where regulation is opening up and institutions are entering, the dominant infrastructure is still Ethereum. Against this backdrop, examining the changes at Lido, which anchors a major part of Ethereum infrastructure and DeFi, carries more weight than simply checking the success or failure of one project. Lido's changes are bound up with the changes in DeFi and the Ethereum staking market as a whole. Understanding Lido lets you understand the foundation of the DeFi market and the structure of the Ethereum staking market.

This article examines Lido along five axes: its history, its protocol and infrastructure, its products, its governance, and its future.

1. Lido from Its Beginning to Today

1.1 The Founding Context and the Birth of Liquid Staking

1.1.1 Ethereum Around the Merge

To understand the context in which Lido appeared, you have to go back to before the end of 2020. At the time, Ethereum was not yet a PoS network. Ethereum mainnet ran on PoW (Proof of Work), and it had begun a gradual transition to PoS through a separate chain called the Beacon Chain. The Beacon Chain launched on December 1, 2020, and ran in parallel with Ethereum's PoW mainnet for about a year and ten months. Then, on September 15, 2022, the Merge update combined the Beacon Chain with the existing Ethereum mainnet, and Ethereum transitioned fully to a PoS-based blockchain network.

The arrival of the Beacon Chain was an important turning point in Ethereum's history. After its launch, users could deposit ETH to join the PoS validator set, and after the Merge this structure became Ethereum mainnet's consensus mechanism. But the staking structure was not friendly to ordinary users. To stake on Ethereum and earn rewards, you had to deposit at least 32 ETH and run a validator node yourself. A validator node stores network data, processes transactions, and participates in producing new blocks. This imposed a high capital and technical barrier to entry for ordinary users.

In addition, withdrawals of staked assets were not implemented in the early days of the Beacon Chain. Staked ETH could not be freely withdrawn, and users who deposited ETH had to lock up their assets until a future upgrade. A user had to stake a large unit of capital, 32 ETH, take on validator operation risk directly, and give up liquidity at the same time. These three conditions were the structural reason Ethereum staking was hard to bring mainstream.

Ethereum also does not provide protocol-level native delegation, unlike chains that follow a DPoS (Delegated Proof of Stake) model. A structure where a user delegates stake to a specific validator within the protocol is not part of the base design. Ethereum wanted a decentralized validator set, but its early staking UX was a structure only a fairly limited set of users could access.

These problems are the context in which liquid staking appeared. Liquid staking lets users participate in staking rewards without running a validator themselves, and it goes a step further by tokenizing the staking position to provide liquidity for the staked asset. Liquid staking emerged to solve the limitations of early Ethereum staking within a single product.

1.1.2 Lido's First Product: A Liquid Staking Platform

Lido's first product, a liquid staking platform, is simple. A user deposits native ETH and receives stETH tokens in receipt. stETH is a token that represents 1:1 ownership of the user's staked ETH. When a user deposits ETH, a corresponding amount of stETH is minted, and stETH automatically reflects staking rewards or penalties in the holder's wallet (rebasing). At the same time, stETH is a liquid token usable across DeFi and the Ethereum ecosystem.

Lido's liquid staking service mattered because it turned staking into a token interface, and the benefit this product offered was a powerful force in the staking market. Users no longer had to run a validator themselves, operate a client, manage keys, watch uptime, and bear slashing risk individually. Users could also participate in staking through Lido with less than 32 ETH, and they could keep the liquidity of their staking position by using stETH. The actual staked ETH is locked, but the user can put that position to work elsewhere through stETH. In this sense, stETH was not a simple proof token but an interface connecting Ethereum staking and DeFi. stETH was later integrated into a range of DeFi protocols such as Curve, Aave, MakerDAO, and Pendle, becoming a core asset of the DeFi money lego. For the user, Lido is a simple experience of putting in ETH and receiving stETH, but behind it, professional node operators selected by the DAO handle the actual validator operations.

Lido mainnet went live on December 18, 2020, almost the same time the Beacon Chain went live. The moment Ethereum took its first step toward PoS, a protocol set out at the same time to fill the user-experience gap that transition would create. The timing of Lido's launch carried real significance for the evolution of the Ethereum ecosystem.

1.1.3 The Early DAO and Contributor Structure

Lido started as a DAO rather than a single company from the beginning. Among the people central to Lido's start are Konstantin Lomashuk, Vasiliy Shapovalov, and Jordan Fish. Lomashuk and Shapovalov came from a node operator background, having run a non-custodial staking service called P2P (P2P Validator) since 2018. As of 2020, P2P was already a professional infrastructure operator running validators on several PoS chains. Jordan Fish, known in the crypto community as "Cobie," left the Lido team around 2021, and Lido's operations evolved into a structure driven jointly by a contributor group centered on P2P alumni and a gradually expanding DAO community.

Lido's early fundraising was deeply tied to key figures in the DeFi ecosystem of the time. Lido’s early financing is better understood as a series of treasury allocations to strategic backers rather than traditional equity rounds. In December 2020, the DAO allocated roughly $2 million worth of LDO to early contributors, followed by a $73 million treasury sale led by Paradigm in May 2021 and a $70 million treasury sale to a16z in March 2022. The early investment brought together a range of crypto-focused funds and DeFi builders. This shows that Lido intended from the start not simply to launch a single staking protocol but to position itself as infrastructure that would integrate with the entire DeFi ecosystem.

In a January 2021 post introducing LDO, Lido explained that it built its Ethereum staking protocol as a DAO "to maintain decentralized infrastructure while preserving upgradability and stability." The Lido DAO decides the core parameters of the liquid staking protocol, leads network upgrades, and manages the growth of the Lido community.

Of course, it is hard to say the early Lido DAO was fully decentralized. One billion LDO tokens were issued when the DAO launched, and the founding members held a substantial share of them at the time. The product Lido shipped aimed at being a DAO, but in practice its actual operations and decision-making had to rely heavily on the early contributors and early investors. This became the seed of the centralization debate that would surround Lido.

Beyond that, while Lido offered users a decentralized staking service, trust assumptions existed across several dimensions: node operator selection, governance token distribution, and withdrawal key management. Lido's early withdrawal key generation was in fact carried out through a separate ceremony held from December 13 to 16, 2020. This shows the structure of the time was closer to an early-stage protocol that still had to pursue decentralization gradually than to a fully trustless system.

Lido is an innovative protocol that opened Ethereum staking to a broader public. But it also started out, despite being a DAO, carrying a number of trust assumptions and a centralized governance structure. The Lido that follows develops as a process of narrowing the gap between these two tensions. It began by giving retail users a simple staking UX, but over time Lido has evolved into staking infrastructure with more and increasingly permissionless node operators, more distributed validator operations, and a more sophisticated governance layer.

1.2 Rapid Growth Before the Merge and the Multichain Expansion Attempt

1.2.1 stETH's DeFi Integration

Lido's rapid growth was not simply because it made staking easy. The core of that growth was that stETH, the liquid staking token, became an asset usable within the Ethereum DeFi ecosystem. Right after launch, Lido's focus was to make stETH an asset that actually got used. Held idle, stETH simply sits in the wallet as a claim on staked ETH. Once deployed across DeFi, it becomes a productive asset that functions as a working form of staked ETH. stETH reflects staking rewards and at the same time was quickly integrated so it could serve as collateral, liquidity, and a building block for yield strategies across various DeFi protocols.

ETH deposited into the Beacon Chain was locked until withdrawals were implemented via the Shapella hard fork in April 2023. For Lido, securing enough liquidity for stETH to trade as close to ETH as possible was therefore a make-or-break factor for the product. The Curve stETH/ETH pool played the most important role in this. From January 2021, Lido provided a guide for supplying stETH liquidity through Curve and ran the pool as a venue where users could swap stETH and ETH with low slippage. stETH later expanded to other DeFi protocols such as 1inch and Uniswap.

Integrations that let stETH be used as collateral on Aave and MakerDAO also moved forward. In 2022, stETH was formally listed as a collateral asset on Aave V2, and Aave V3, launched the same year, integrated wstETH (wrapped stETH) in earnest. As discussed later, the rebasing token stETH was hard to make compatible with some DeFi protocols due to its contract structure, so Lido created a wrapping token, wstETH, whose balance does not change and whose value instead changes in proportion to staking rewards. wstETH became one of the largest collateral assets on Aave V3, and users began using a loop staking strategy: borrowing ETH against wstETH collateral and re-staking that ETH on Lido to receive stETH.

The ability to pursue two returns at once with the same capital, staking yield and additional DeFi yield, was a strong incentive for ETH holders, and Lido became the foundation of Ethereum's DeFi money lego.

1.2.2 Merge Anticipation and Lido's Rapid Growth

2021 and 2022 were a period when anticipation for Ethereum's PoS transition peaked. The Beacon Chain and Ethereum staking were already operating, and right up to the Merge hard fork that fully transitioned Ethereum mainnet to PoS, the market saw Lido as "the most direct way to invest in Ethereum's PoS transition." As the Merge approached, ETH holders' staking demand grew, and Lido was the largest absorber of that demand. Having simplified Ethereum's complex staking structure, Lido was the simplest option for users.

In January 2021, Lido's total deposited ETH was around 76,000 ETH, but a month later, in February 2021, it crossed 180,000 ETH, growing 136% in a single month. From this point, Lido began to establish itself as effectively the single dominant protocol in the Ethereum liquid staking market. By 2022, Lido's staking share entered the 30% range, and concerns began to be raised in earnest that a single entity could cross the 33% stake threshold at which it could temporarily affect Ethereum's finality.

Lido's growth meant more than TVL growth. Once Ethereum transitioned to PoS, the amount of ETH staked by a single protocol or node operator could have an influence over network consensus. So the more staking share Lido absorbed, the more it became both the base protocol of the DeFi money lego and infrastructure that affects Ethereum's consensus layer.

1.2.3 Multichain Expansion: Terra, Solana, Polygon, and Kusama

Lido did not stay only on Ethereum. From 2021 to early 2022, Lido treated liquid staking as a general category and tried to expand to several PoS chains. In this period, Lido aimed to be a multichain liquid staking protocol rather than an Ethereum liquid staking protocol. Over roughly a year after launch, Lido shipped liquid staking on several PoS chains including Terra, Solana, Polygon, and Kusama, and each attempt was led by an external contributor team within the Lido DAO's LEGO (Lido Ecosystem Grants Organisation) framework.

Lido on Terra was the first to launch. bLUNA launched on the Terra network in early 2021, structured so that when a user staked LUNA they received bLUNA, which could be used as collateral on Anchor, a core protocol of the Terra DeFi ecosystem. Products in the same vein followed: stLUNA, and bETH, which bridged Ethereum's stETH to the Terra chain. Because Anchor offered UST depositors a fixed yield of around 20%, bETH quickly drew capital as an asset that could pursue Anchor's additional yield on top of stETH's staking yield.

Lido on Solana launched in September 2021 in collaboration with the Chorus One team. It aimed to issue stSOL and integrate with Solana DeFi ecosystem protocols such as Saber, Serum, Raydium, and Mercurial. Solana was growing fast at the time, and with a variety of DeFi services emerging, it was the most suitable chain for an LST after Ethereum.

Lido on Polygon went live in April 2022 with Shard Labs as the developer. It issued stMATIC to tokenize MATIC staking on the Polygon PoS chain and integrated with several DeFi protocols such as Balancer, Aave, and Curve. Lido on Kusama was also run in a form led by a separate contributor team (MixBytes).

In this period Lido clearly aimed to be a multichain LST platform. In each chain's launch announcement, Lido emphasized multichain expansion as a core strategy, going so far as to use the phrase "Future is multichain, so is Lido." This multichain expansion was a natural strategy at the time. PoS chains were steadily increasing, and the liquidity problem for staking assets was common to each chain. Lido sought to be a protocol that could solve this problem repeatedly across many chains.

But multichain expansion also greatly increased the complexity and risk Lido had to bear. Each chain carried a different structure and its own risks, and the stETH model that worked on Ethereum could not simply be copied to other chains. Multichain expansion could extend Lido's brand and category, but it also brought each chain's risks and operating costs into the Lido ecosystem.

1.2.4 The LUNA/UST Collapse and the stETH Depeg

The Terra collapse of 2022 was the first major risk to reach Lido. Over about a week starting May 7, 2022, Terra's UST stablecoin depegged from one dollar and fell apart. UST, which held around $1 on May 9, crashed below $0.30 by May 12, and along with it LUNA's market cap, once around $40 billion, converged on essentially zero. The collapse took down Lido on Terra, one of Lido's multichain expansion lines. More importantly, the Terra collapse was the trigger for a follow-on event: the uncouplingof stETH's secondary market liquidity.

The risk-transmission path was as follows. When Terra fell apart, users who held bETH on Anchor bridged bETH back to Ethereum and converted it to stETH to recover their assets. According to Nansen's analysis, about 615,980 bETH returned to Ethereum during this period. Because withdrawals were still not possible on the Ethereum protocol, this stETH acted as selling pressure in the market, and the selling route was almost entirely the Curve stETH/ETH pool. At the same time, with a broad risk-off mood and a decline in the ETH price itself, the Curve pool's liquidity began to drop sharply. On May 12, 2022 alone, 3AC and Celsius withdrew a combined roughly $780 million of liquidity from the Curve stETH/ETH pool. 3AC pulled out 128k stETH and 73k ETH (about $400 million total) in a single transaction, and Celsius withdrew about $380 million across three transactions the same day. The pool's TVL, around $4.08 billion on May 9, fell more than half to $1.91 billion by May 12. As the pool's liquidity drained, the stETH price began trading at a discount to ETH. stETH fell to about 97% of ETH during May, and dropped further to about 93% by mid-June.

The important point is that this secondary market decoupling was not a technical problem with the Lido protocol. 1 stETH still carried a claim on 1 staked ETH. But staked Ethereum could not yet be withdrawn at the time due to Ethereum protocol technical limitations, and combined with the market mood, this amplified fear among users. Once the uncouplingbegan, large players holding leveraged ETH borrowing positions collateralized by stETH started to deleverage, and that deleveraging itself formed a feedback loop that added further stETH selling pressure. Celsius held about half of its user assets in stETH and had to sell stETH to meet user withdrawal requests. But the deeper the stETH discount, the less ETH the same amount of stETH could be exchanged for. Celsius, already under broader liquidity strain, froze user withdrawals on June 12 and soon entered bankruptcy proceedings. 3AC also sold its stETH position at a loss around the same time, though its collapse was driven mainly by other exposures such as LUNA. For both firms, the stETH discount was one pressure among many rather than the cause of failure.

Throughout the period before withdrawals were possible, stETH did not trade exactly one-to-one against ETH on the secondary market, and some discount was the normal state. What this episode did was widen that discount, which then narrowed only gradually up to the Merge. To be precise, stETH's backing was not broken; the market price gapped open under liquidity pressure in a situation where withdrawals were impossible. After the Merge, the stETH price converged back to its backing value, and once withdrawals were enabled in April 2023, the structural reason for such a discount disappeared entirely. Lido did not take a direct loss in this event. But it left a lesson: the more deeply stETH integrates into DeFi, the more an external protocol's systemic risk can transmit to Lido's users. This is also the background for Lido later making risk isolation a core principle when designing new products such as Lido Earn.

1.3 After Shapella: Lido V2

1.3.1 What Shapella Changed

On April 12, 2023, the Shapella (Shanghai-Capella) upgrade went live on Ethereum mainnet. The core of Shapella was enabling withdrawals of ETH deposited into the Beacon Chain. For about two years and four months after the Beacon Chain went live in December 2020, staked ETH could not be withdrawn. After Shapella, stakers could finally withdraw the ETH they had deposited. Many in the crypto community expected the staking ratio on Ethereum to fall once withdrawals opened after Shapella, but with the stability that withdrawability provided, Ethereum staking instead grew explosively.

For Lido, a secondary-market liquidity pool that let users swap stETH for ETH already existed. But the fact that the staked asset itself could not actually be withdrawn was a major source of uncertainty for users. stETH could trade at a discount to ETH depending on market conditions, and the stETH depeg after the Terra collapse, discussed earlier, was a case that illustrated this structural limit.

After the Shapella upgrade, stETH was no longer just a token exchanged for ETH on the secondary market; it became an asset that could actually be withdrawn into ETH. If the stETH price discounted heavily against ETH, a market participant could arbitrage by buying stETH and then withdrawing it into ETH on Lido. This change lowered stETH's risk premium and played an important role in raising the stability of Lido's product.

1.3.2 Lido V2 and the Staking Router

Lido could not let users withdraw stETH into ETH immediately after Shapella went live on Ethereum. Lido V2, which added the withdrawal feature, was activated on mainnet on May 15, 2023, about a month after Shapella. This lag was to secure stability through seven external security audits. Because Lido is an on-chain protocol handling billions of dollars of ETH, it tends to reflect Ethereum protocol changes conservatively, going through audits, governance, and phased rollout rather than reacting immediately.

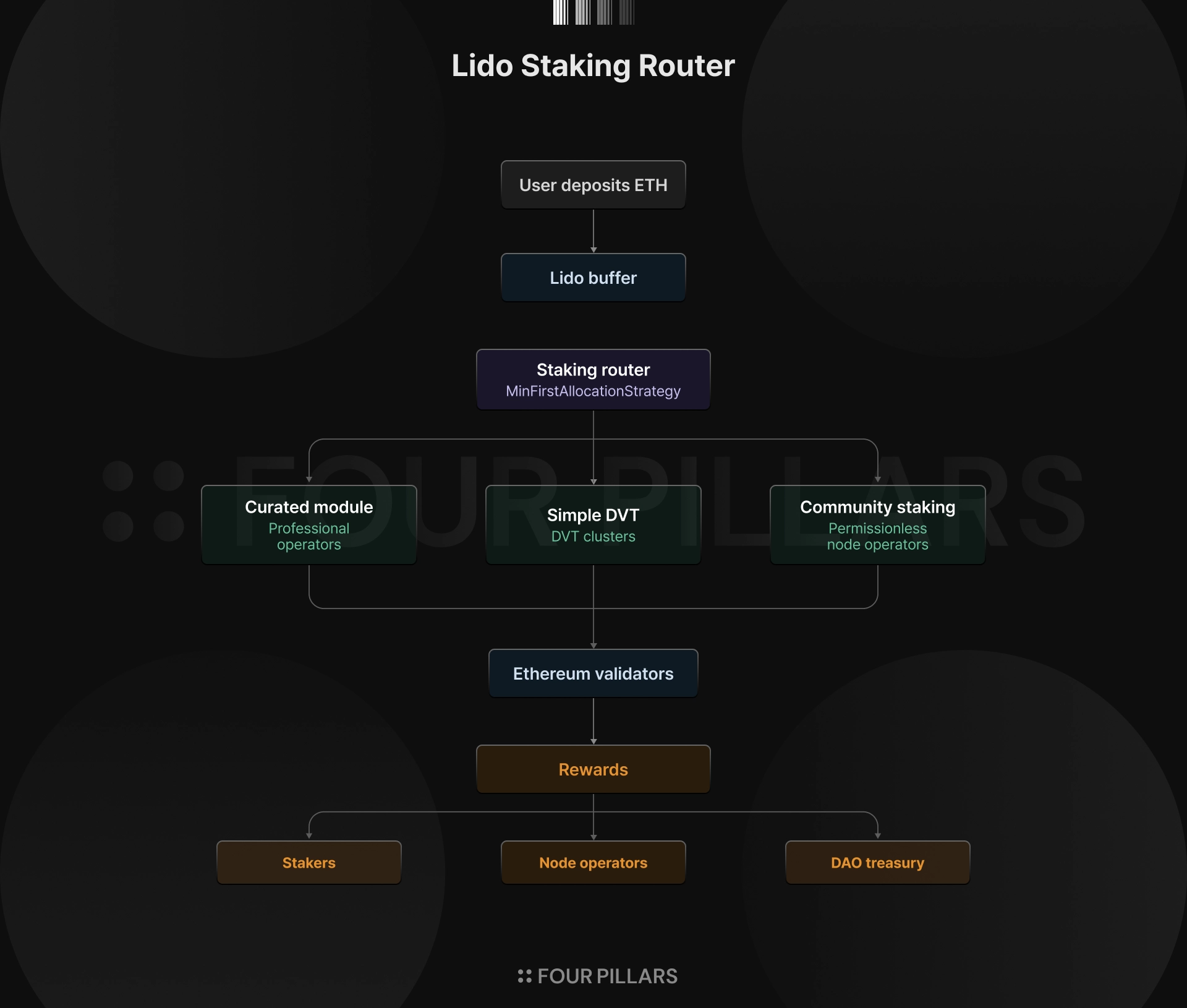

Lido V2 included two very important upgrades. One is the withdrawal support discussed so far, and the other is the Staking Router. If withdrawal support was Lido supporting a change in Ethereum, the Staking Router was a more fundamental change that altered Lido's direction.

Up to Lido V1, Lido's node operator pool was a single pool of about 30 Curated operators selected directly by the Lido DAO. This structure was favorable for securing operational stability, but it was hard to expand node operator diversity, and it was also a cause of the centralization criticism Lido faced.

The Staking Router is a modular structure that lets Lido separate the forms of node operators running its staked ETH into various staking modules. It keeps the Curated module as is while building an extensible structure where node operator groups of a different nature can be added as separate modules. Each module can have its own operator selection criteria, bond requirements, fee structure, and reward distribution method. The Staking Router laid the groundwork for creating new node operator on-ramps such as solo stakers and DVT clusters, and for bringing a more diverse validator ecosystem into Lido. Lido V2 and the Staking Router are covered in detail in Section 2.4.

The Simple DVT module and CSMthat appear later are all modules that utilize this Staking Router to connect to the protocol, in addition to the existing Curated Module. So Lido V2 was not a simple withdrawal-feature upgrade but the starting point for Lido's evolution from a staking service into modular staking infrastructure.

1.4 Establishing Lido's Identity: Focusing on Ethereum

1.4.1 Winding Down the Multichain Product Line

From 2021 to 2022, Lido pursued a multichain LST protocol strategy, expanding to several chains including Terra, Solana, Polygon, Kusama, and Polkadot. But after 2023, Lido gradually withdrew from chains other than Ethereum and established its identity as staking infrastructure focused on Ethereum.

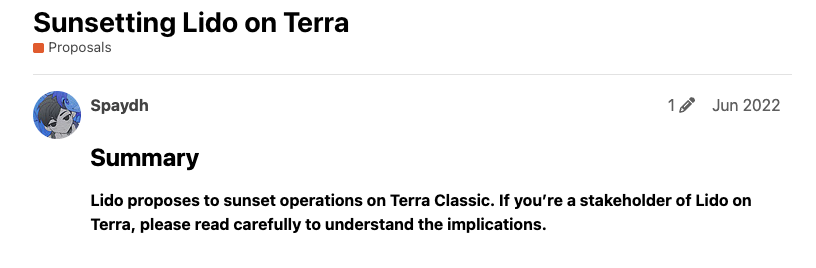

Terra was wound down first. After the Terra collapse in May 2022, Lido on Terra became a service that was no longer viable to maintain, and a proposal to sunset it was posted to the Lido research forum in June 2022. Terra was a case that showed Lido both the upside and the risk of multichain expansion at once. Entering a fast-growing chain let Lido share in that growth, but if the chain fell apart, Lido had to take on that chain's systemic risk as well.

Source: Lido Research Forum

Sunset proposals for Polkadot and Kusama followed in March 2023, and in October 2023 the DAO voted to sunset Solana. The direct reason for this decision, which passed with 92.7% in favor, was financial unsustainability. According to the P2P team that handled the development and operation of Lido on Solana after taking over the responsibilities from Chorus One, revenue generated on Solana up to that point came to about $220,000, while cumulative losses reached about $480,000. P2P asked the Lido DAO for additional funding, but Lido chose to sunset rather than provide more funds. New staking stopped on October 16, 2023, and the front end was fully shut down on February 4, 2024.

Polygon was the last to be wound down. Lido on Polygon's wind down was decided about a year after the Solana sunset, on December 16, 2024. The reason for the Polygon sunset was similar to Solana's, but in its Polygon withdrawal announcement post, Lido added the phrase "strategic refocus on Ethereum." This clearly shows that Lido's strategy converged on an identity that abandoned multichain and focused on Ethereum.

Lido's full withdrawal from chains other than Ethereum should not be read only as "the failure of the multichain strategy." Lido's strongest point is not issuing a liquid staking token itself, but having that token carry enough liquidity and DeFi integration to operate as a foundation of the money lego. The chain where this condition was most strongly met was Ethereum, and rather than spend resources maintaining services across several chains, Lido began to solve harder problems on Ethereum. It sought to evolve beyond a single LST product into a protocol's true "staking infrastructure," with diverse node operator structures and a governance layer.

1.4.2 The Key Turning Points of 2023–2025

From 2023 to 2025, Lido was systematizing its Ethereum-focused identity in practice. The first turning point was Lido V2, discussed earlier in 1.3.2. V2 strengthened stETH's trust structure through withdrawal support, and built the foundation to accommodate several staking modules through the Staking Router.

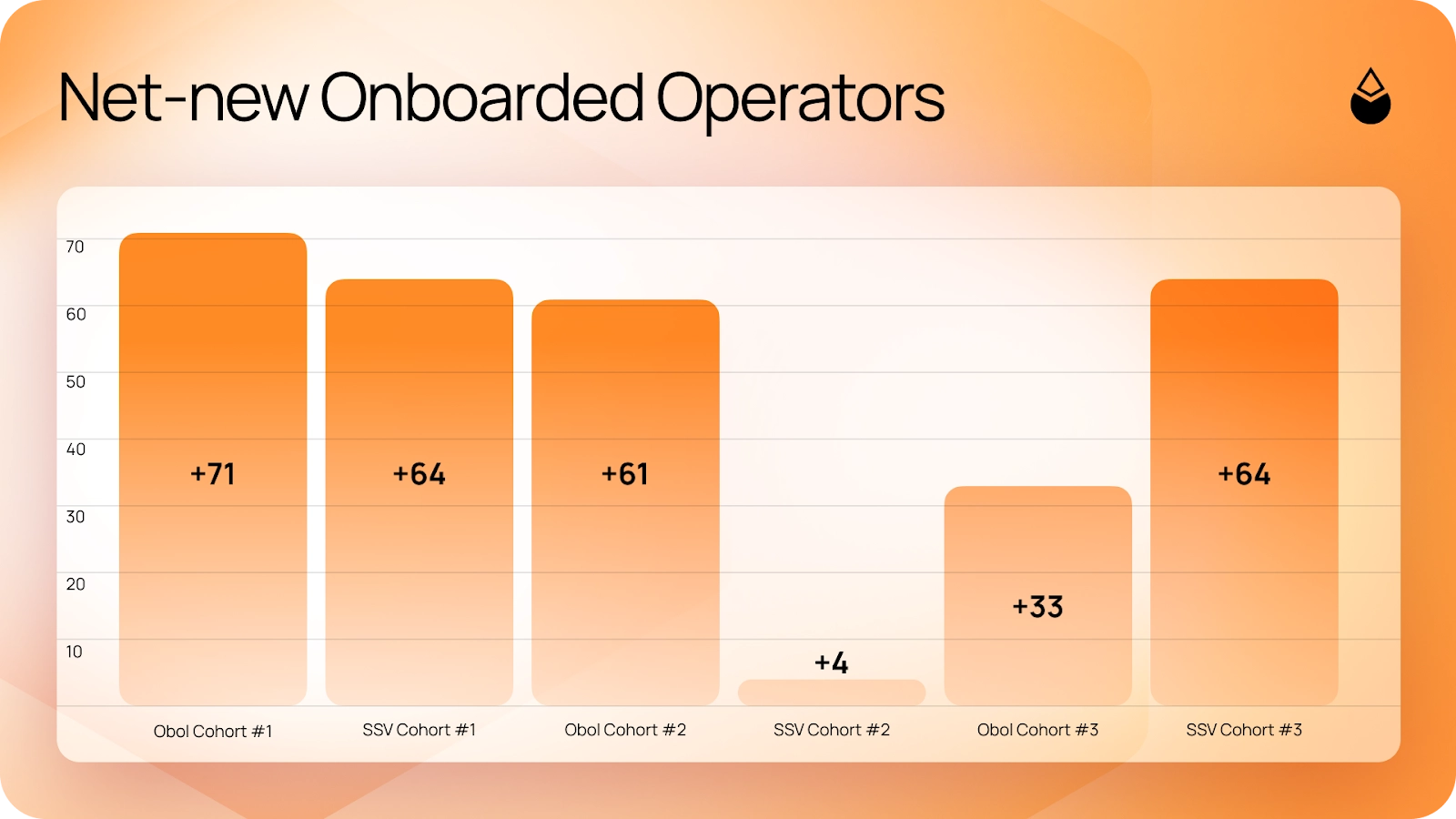

After the Curated module, the second Lido staking module added through the Staking Router was the Simple DVT module. The Simple DVT module was deployed to mainnet in April 2024, and using Obol- and SSV-based DVT, it opened the first path for solo stakers and community stakers to participate in running Lido validators.

DVT in particular opened an important path for Lido. Rather than a single node operator running one validator, DVT made it possible for several operators to run one validator together as a cluster. Technically this raises the resilience and security of validator operations, and structurally it opens an opportunity for more operators to participate as Lido operators. Simple DVT is not Lido's final form but an early stage toward a more scalable, permissionless DVT-based module.

The next module added was the CSM (Community Staking Module). CSM can be called the most important module in Lido's decentralization strategy, given that it was the first module to allow permissionless entry by node operators via the use of an ETH bonding system. Through CSM, a variety of solo stakers and community operators could be brought into the Lido ecosystem securely. In January 2025, CSM passed its initial testing stage and transitioned to fully permissionless. Simple DVT and CSM are covered in detail in 2.6 and 2.7.

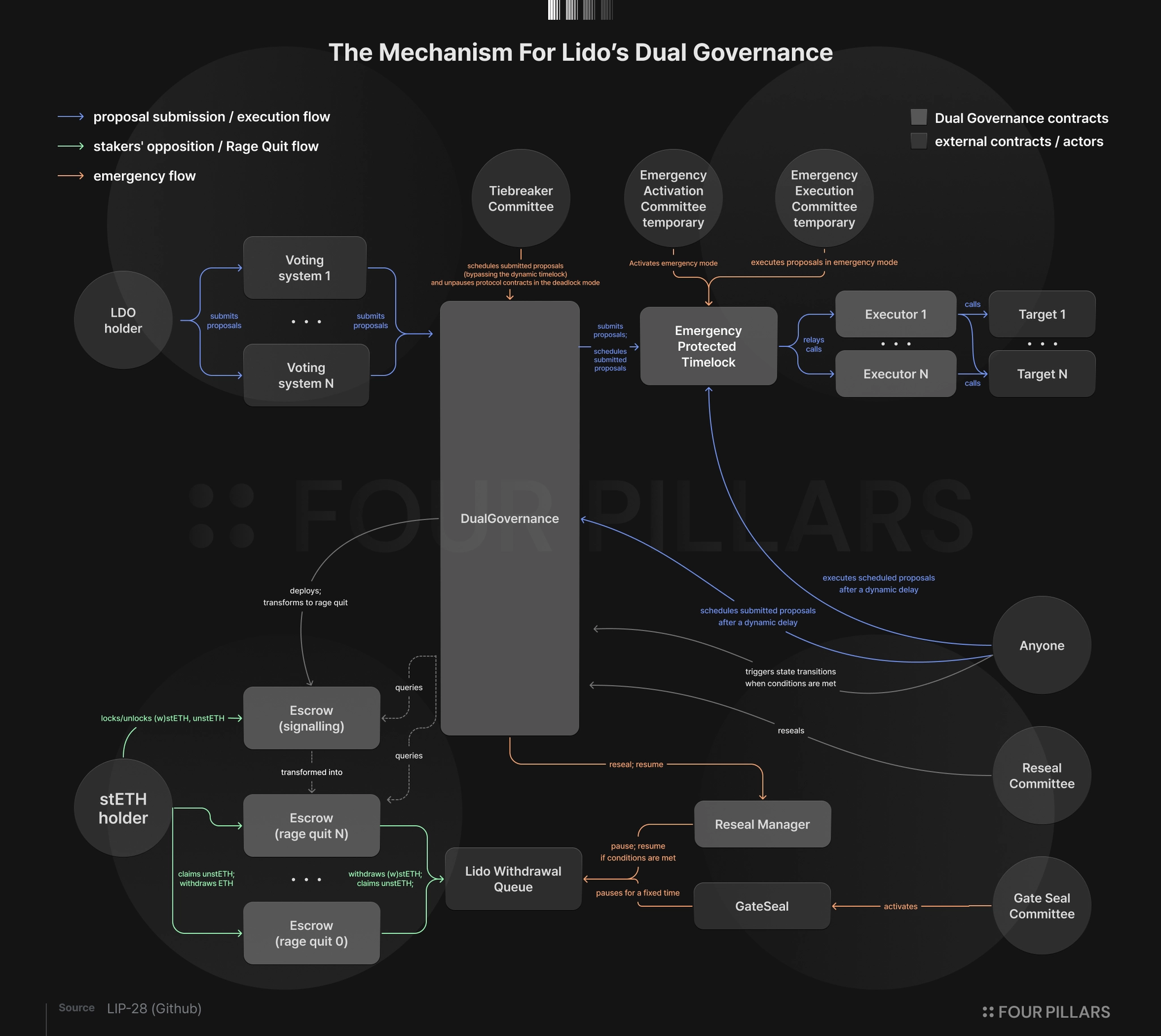

Beyond the staking modules, another important turning point was Dual Governance (LIP-28), activated on July 4th, 2025. Where LDO token holders had previously been the final decision-makers of the protocol, Dual Governance elevates stETH holders to important stakeholders in Lido DAO governance. Dual Governance is a mechanism for resolving, at the protocol level, the structural tension between LDO holders' governance power and stETH holders' interests. This is covered in detail in 4.2.2.

In short, Lido in 2023–2025 wound down multichain expansion and focused on qualitatively advancing Ethereum infrastructure. If the Lido of its 2020 launch was a protocol born to solve Ethereum's staking UX problem and promote decentralized staking, the Lido of 2025 had moved closer to a protocol offering solutions to the various problems of Ethereum staking infrastructure.

1.5 The Era of V3, Earn, and Institutional Products

1.5.1 Why Lido V3 Was Needed

Through V2, Lido introduced withdrawals and the Staking Router, and through Simple DVT and CSM it built a structure where a wider variety of node operators could participate. But as demand for Ethereum staking expanded, new demand emerged that liquid staking alone could not satisfy: institutional demand.

A Lido user can participate in staking through a simple front-end experience of depositing ETH and receiving stETH. The complex parts, node operator selection, validator operation, reward distribution, and withdrawal processing, are handled on the back end by the Lido protocol, the DAO, and node operators. This structure is close to ideal for retail users, and for institutions too, stETH is an attractive option as an alternative way to gain Ethereum staking exposure. Regulated products built on core stETH already exist, such as the WisdomTree ETP and the VanEck S-1 filing.

The one-size-fits-most core pool does, however, have the limit of insufficient flexibility. Certain kinds of stakers, such as advanced DeFi users and some institutions, want conditions the shared pool cannot provide on its own. The current Lido core pool gives no choice over which node operators to use, what risk policy to apply, how to segregate and manage assets, and what fee structure and operating conditions to set.

Institutional users do not look only at "staking yield." They look at accounting segregation, auditability, jurisdiction, custody, withdrawability, and risk control structure. Lido's existing staking approach has the advantage of simplicity but does not reflect these requirements in fine detail. Conversely, bespoke staking, which offers per-client customized staking, provides operational control but has constraints on liquidity. Lido V3 emerged precisely to resolve the trade-off between these two models, not to replace the core pool but to add flexibility for the users who need it.

1.5.2 The Arrival of Lido V3 and stVaults

Source: Lido

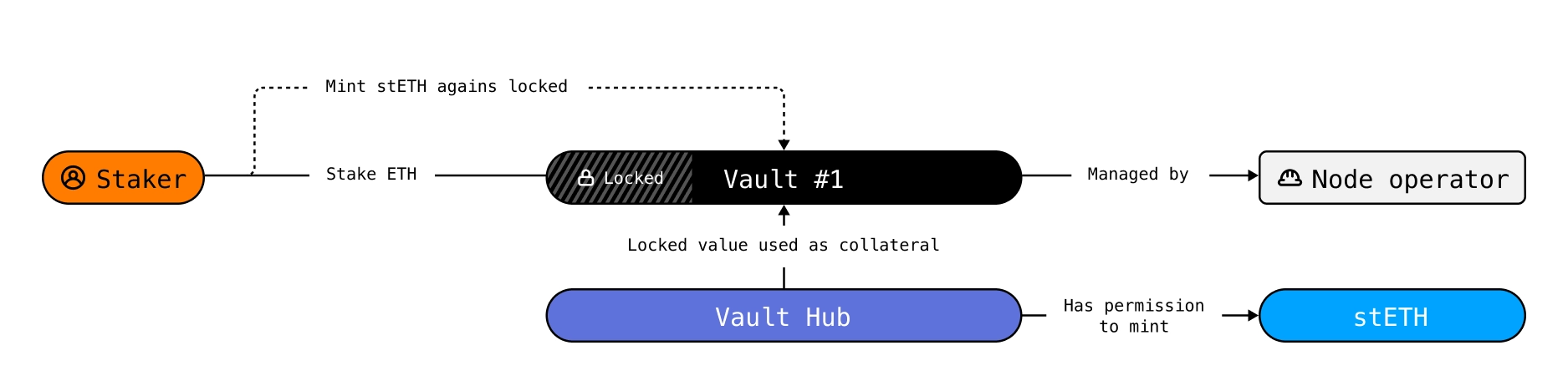

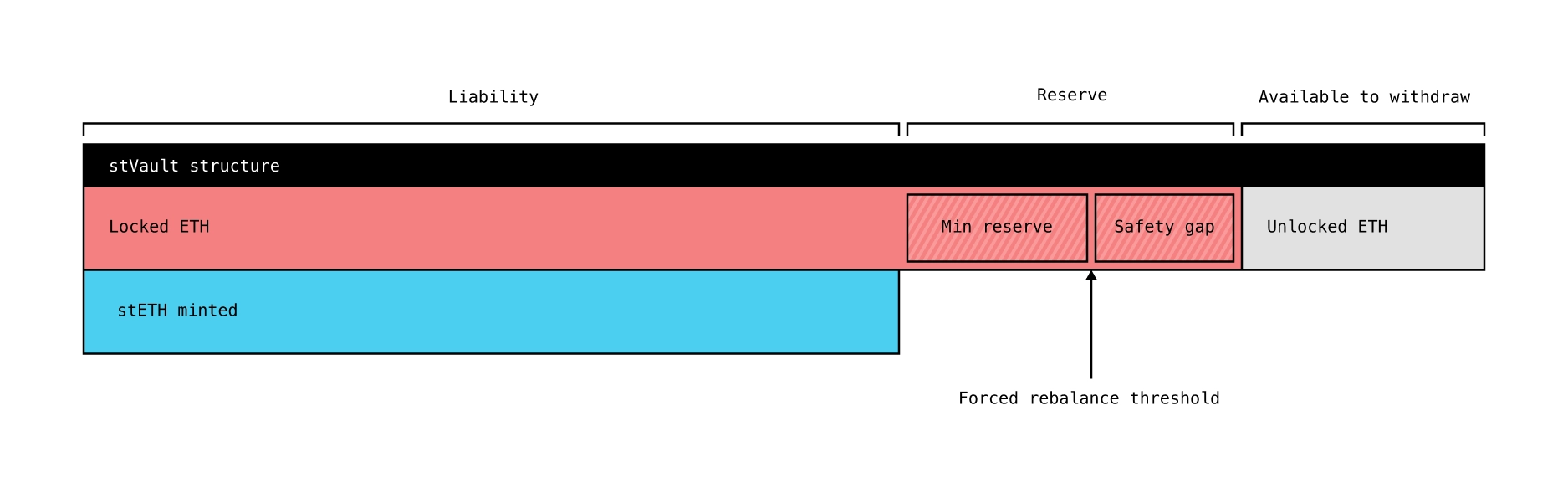

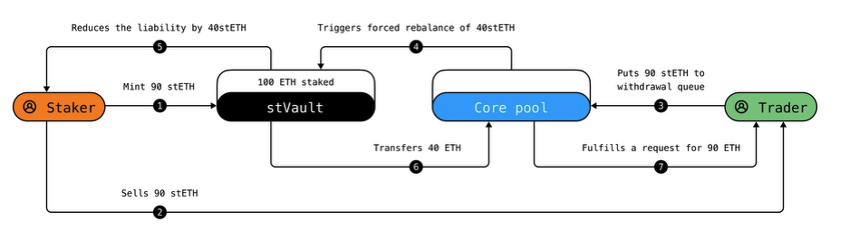

On January 30, 2026, Lido V3 launched on Ethereum mainnet. The core of Lido V3 is stVaults. stVaults is a modular staking structure that lets institutions and builders design their own validator operation structure while keeping the shared liquidity of stETH.

Rather than seeing stVaults simply as Lido's institutional product, it should be seen as a mechanism that diversifies the structure of staking operations while keeping a single shared liquidity in stETH. A vault owner can set the node operators, operating conditions, fee structure, and risk parameters they want. The ability to customize the vault while still using stETH's liquidity and DeFi integration is the differentiator from ordinary bespoke staking.

Through stVaults, Lido begins to expand its target users from a retail-centric staking service toward one that encompasses institutions and builders. In the past, Lido was a staking liquidity service for retail users. But after V3, Lido moves closer to an infrastructure protocol that lets institutions, L2s, node operators, and DeFi builders create their own staking products. An institution can secure asset segregation and operational control through a separate vault; an L2 can turn ETH bridged to its chain into a yield-bearing asset; and node operators can move beyond delegated staking that depends on inflows through the existing Lido protocol to build differentiated staking products of their own. The detailed mechanics of V3 and stVaults are covered in earnest in 3.1.

1.5.3 The Arrival of Lido Earn

Source: Lido

If V3 is a change aimed at platformizing Lido's staking structure, Lido Earn is a product-level change aimed at expanding the product portfolio itself. Lido is well known as a liquid staking protocol for ETH. But as the staking market matured and competition intensified, staking services alone began to hit limits for the protocol's growth and revenue expansion.

Lido Earn is a new attempt to overcome this limit. As of May 2026, Lido Earn consists of two services: EarnETH and EarnUSD. EarnETH takes in ETH, WETH, and stETH and allocates capital across several DeFi protocols. EarnUSD takes in USDC and USDT and allocates them to on-chain stablecoin yield strategies. Through Lido Earn, Lido is expanding its product range beyond providing ETH staking rewards to structured DeFi-based yield products. The detailed structure of Lido Earn is covered in more depth in 3.2.

1.5.4 Lido's New Identity in 2026

Now, in 2026, you can see Lido's identity shifting once again through the launch of V3 and Lido Earn. In 2020, Lido emerged to solve Ethereum's staking UX problem. It then tried multichain expansion in 2021–2022, but after 2023 it established an Ethereum-focused identity. As a result, Lido was able to evolve, through the Staking Router and Dual Governance, into a protocol that responds to the various problems of Ethereum staking infrastructure. And in 2026, through V3, stVaults, and Lido Earn, Lido is moving toward a comprehensive staking infrastructure platform that targets a wider set of users.

2. How Lido Works: Protocol and Infrastructure

Having looked at the path Lido has walked, this chapter examines how Lido actually works. The aim is to follow the full process from the moment a user deposits ETH into Lido, through stETH being minted, who runs the nodes and how, how rewards are distributed, and how withdrawals are processed.

As of May 2026, Lido V3 has two structures side by side: the base Lido core pool and stVaults. This chapter explains how the Lido core pool works, where users deposit ETH into a shared staking pool and stETH is minted.

2.1 The ETH Staker Flow in Lido

2.1.1 Deposit ETH, Receive stETH

ETH staking in Lido starts with a user sending ETH to a Lido contract. Through the Lido staking website or a direct contract call, the user deposits ETH via the submit() function and receives an equal amount of stETH. The stETH the user receives is a token representing a claim on the ETH staked through the Lido protocol. A stETH holder has the right to withdraw back into ETH on Lido at any time. This right is not instant settlement, however. A withdrawal goes through Lido's withdrawal queue, and the time to receive ETH varies with the queue length, the ETH in the buffer, and node operators' response speed, ranging from a few hours to a few days in normal times and longer when withdrawal demand surges. The detailed withdrawal procedure is covered in 2.2.2.

The important point here is that depositing ETH does not mean this ETH is immediately staked to a validator on Ethereum mainnet's Beacon Chain. The stETH is minted first, and the deposited ETH moves to the protocol's next stage. So the user stakes through a simple experience of receiving stETH immediately on deposit, but on the actual back end an asynchronous process of buffering, routing, and validator deposit follows. This is not directed by any party. It works programmatically, according to the smart contracts of the Staking Router. The detailed allocation logic is covered in 2.4.

2.1.2 The Role of the Buffer

Until the Pectra hard fork, the minimum and maximum stake for a single Ethereum validator was 32 ETH. Within the Lido protocol,the ETH a user deposits is not immediately staked right away; it first enters the buffer. The buffer acts as a cushion that balances Lido's inflows and outflows. When a user deposits ETH, it is first stored in the buffer and then used for two purposes. One is processing withdrawal requests, and the other is staking through the Staking Router. Because Lido prioritizes withdrawals over deposits, if there are processable withdrawal requests remaining, it uses the ETH in the buffer for withdrawals first.

After the MaxEB (EIP-7251, Maximum Effective Balance) increase applied in the Pectra hard fork, the meaning of "using it for staking" needs to be understood a bit more broadly (covered in more detail in 2.8). After Pectra, the MaxEB of an Ethereum validator expanded from 32 ETH to 2,048 ETH, which made it possible not only to keep creating new validators but also to top up and consolidate existing ones. According to Lido's CMv2 migration documentation, depositable ETH is first used for seed deposits, and once there are no more validator keys to seed, it can be used for top-ups. The buffer of the future is therefore more accurately understood not as funds waiting for 32 ETH to accumulate, but as an account that allocates ETH left over after withdrawal processing on a balance basis, across new deposits, top-ups of existing validators, and consolidation.

2.1.3 stETH, a Rebasing Token

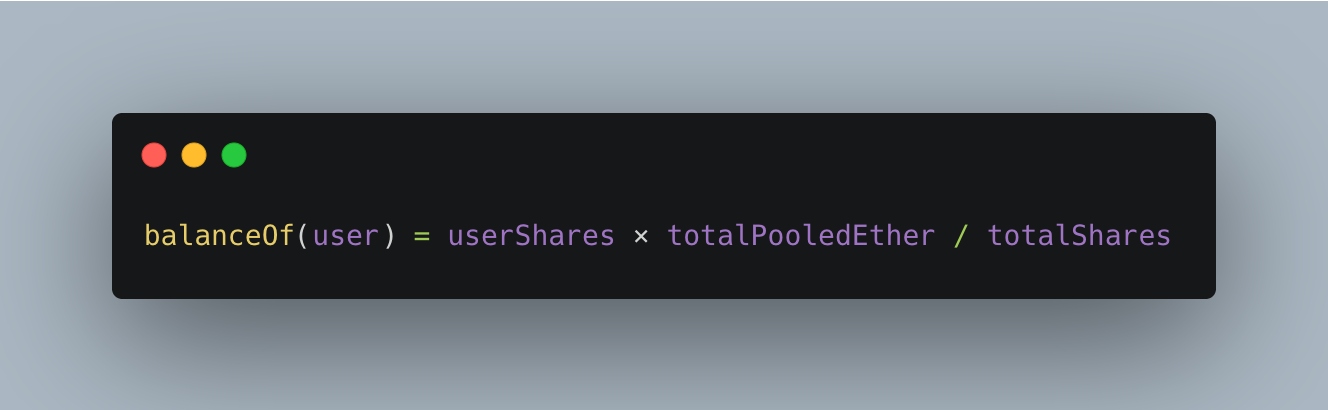

The most important feature of stETH is that it is a rebasing token. The stETH balance increases automatically once a day. This mechanism is known as a rebase.

The Lido protocol contract does not store the stETH balance directly; it stores the shares a user holds. The user's actual stETH balance is then computed from each user's shares as follows.

Here, totalPooledEther is the total ETH held by the entire Lido pool, including buffer ETH, Beacon Chain validator balances, execution layer rewards, and ETH pending withdrawal. totalShares is the total of issued stETH shares. The userShares representing a user's shares stays the same after an ETH deposit; the stETH balance changes because totalPooledEther changes. As validator rewards accumulate, totalPooledEther rises, and every stETH holder's balance rises in proportion.

The rebase is triggered once a day at about 12:30 UTC. At that point Lido's oracle contract, AccountingOracle, aggregates Beacon Chain validator balances and EL-side rewards and updates totalPooledEther. AccountingOracle consists of nine independent oracles selected by the Lido DAO and operates on a 5-of-9 quorum, where five of the nine must report the same data for consensus. Once the oracles' agreed data is submitted to the Lido contract, totalPooledEther is updated, and from that moment every stETH balance is recomputed at the new ratio. The user does not need to separately claim stETH or receive it via a transaction; they simply see the updated figure computed at the time they check their stETH balance.

This is why stETH is a special asset, different from an ordinary ERC-20. Usually the balance rises as staking rewards accrue, but a negative rebase is also possible (though has never occured), where supply decreases if slashing or large penalties occur. stETH is more accurately seen not as a token that accrues interest, but as a token where a user's share of the entire Lido pool is repriced daily.

2.1.4 The Arrival of wstETH

stETH's rebase structure is intuitive for users, but it does not always fit DeFi protocols or bridge structures. Many DeFi protocols were designed without assuming an ERC-20 token's balance could change for reasons other than transfer, mint, or burn.

To solve this, Lido introduced wstETH (wrapped stETH), a wrapped form of stETH. wstETH is an ERC-20 token, but unlike stETH its held quantity does not change automatically. Instead, the value of one wstETH changes over time.

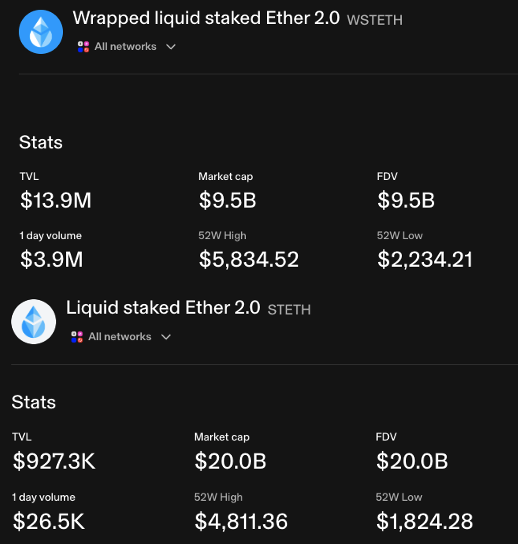

For example, on Uniswap v3, even if a user puts a rebasing token like stETH into an LP, the quantity gained from rebases is not properly reflected in the LP position's accounting. As a result, the LP does not properly capture the yield from rebases. For this reason, Lido recommends using the non-rebasing token wstETH instead of stETH on Uniswap. In practice, the TVL of Uniswap's wstETH pool reaches $13.9M, while the stETH pool is $920K, a clear difference in size.

Source: Uniswap

Since introducing wstETH, Lido recommends it as the standard asset for DeFi integration. On major lending protocols such as Aave, MakerDAO, and Morpho, wstETH has become one of the largest collateral assets. The loop staking strategy through lending protocols, which borrows ETH against wstETH collateral and re-deposits it on Lido, also cannot work without wstETH. When bridging stETH to another chain, the standard is also to bridge via wstETH first and then convert back to stETH on the other chain, to avoid the problem of bridge contracts not handling balance changes.

In short, stETH and wstETH are two representations of the same asset. stETH is the token through which a user can intuitively feel rewards, and wstETH is the token compatible with DeFi infrastructure. Users can freely wrap and unwrap between the two through the Lido interface.

2.2 Node Operators and Withdrawal

If the previous section looked at how a user's ETH becomes the liquid token stETH from a user-experience angle, this section explains who actually runs the validators on the back end, and how the process of a user getting ETH back from stETH works.

2.2.1 The Node Operator's Role and Lifecycle

The ones who actually run validator nodes in Lido are the node operators. Lido is an on-chain protocol that lives on contracts, but the actual operation of validators delegated to Ethereum through those contracts is carried out off-chain by node operators.

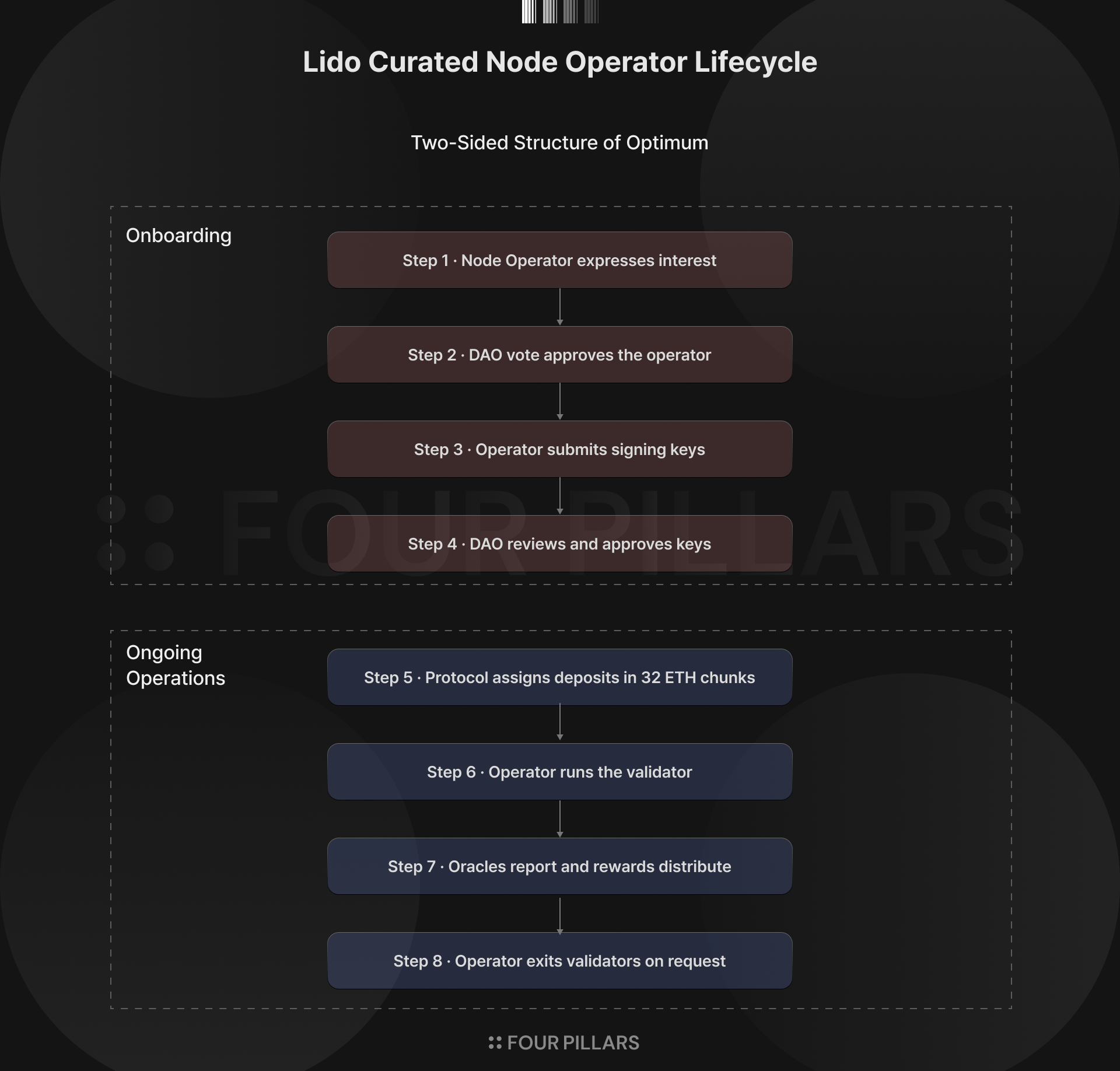

A Lido node operator's lifecycle splits broadly into two stages. The first is onboarding, a one-time procedure for node operators to join Lido. Taking the Curated Module as the basis, this stage goes through four steps. A node operator candidate expresses intent to join the Lido protocol's Node Operator setand is approved as an active operator through a DAO vote. This process generally happens via onboarding rounds announced on the Lido Research forum. The approved node operator then submits its signing keys and signatures to the Curated Module, via an optimistic form of governance called Easy Track. At this point the validator keys the node operator submitted finally become eligible targets for Lido to delegate to.

The second stage is ongoing operations. Under SRv2 (Staking Router v2), the Lido protocol allocates the ETH gathered in the buffer to node operators in units of 32 ETH (Curated Module v1). Because delegation to a specific node operator proceeds in the order of the keys a node operator submitted, node operators must make sure that their first unused keys among their submitted keys are ready to run. For the validators they have been delegated, node operators are responsible for running the validator in line with a set of operating policies such as uptime, accuracy of network participation, and slashing prevention.

After a validator is activated, when the Lido oracle (AccountingOracle) reports Beacon Chain balances and rewards earned on the execution layer, fees are distributed to node operators according to the fee rate. Later, when a user requests a withdrawal and a validator exit becomes necessary, the Lido protocol issues an exit signal through a contract. Node operators monitor this signal, and if a validator they run becomes a withdrawal target, they submit a voluntary exit message for that validator to the Beacon Chain.

This explanation is limited to the Curated Module; Lido's other node operator modules, Simple DVT and CSM, follow different procedures and operating methods. The Curated Module, currently consisting of 34 active node operators, has the Lido DAO directly vet and approve node operator candidates, whereas CSM is a permissionless module anyone can join by depositing a bonding amount. In Simple DVT, instead of a single operator, SSV- and Obol-based DVT clusters are registered as operators, a structure where several node operators run a validator together. The detailed procedures and differences for each module are covered by module in 2.5, 2.6, and 2.7.

A node operator thus runs the validators staked through Lido, manages validator keys, maintains uptime and performance, and even exits validators when the protocol requires it. Node operators in particular have an obligation to fulfill the protocol's withdrawal requests on time. The Lido DAO continuously monitors their performance, and sanctions follow if this is not upheld.

The important point is that Lido's node operators running validators does not mean they hold control over the funds. In Lido's structure, operation and ownership are separated. Node operators run validator nodes, but the withdrawal credentials that hold final ownership of the ETH assets must match the value the protocol sets. The feeRecipient into which execution layer rewards such as priority fees and MEV from block proposals flow must also be set to the address the protocol designates. A node operator therefore only runs the validator node and cannot arbitrarily take the withdrawal address or execution layer rewards. The Lido protocol programmatically distributes ETH across node operators for delegated assets while maintaining control of assets and reward attribution via smart contracts at the protocol level. A Lido node operator is a validator operator, not a custodian of users' ETH.

2.2.2 Lido's Withdrawal Procedure

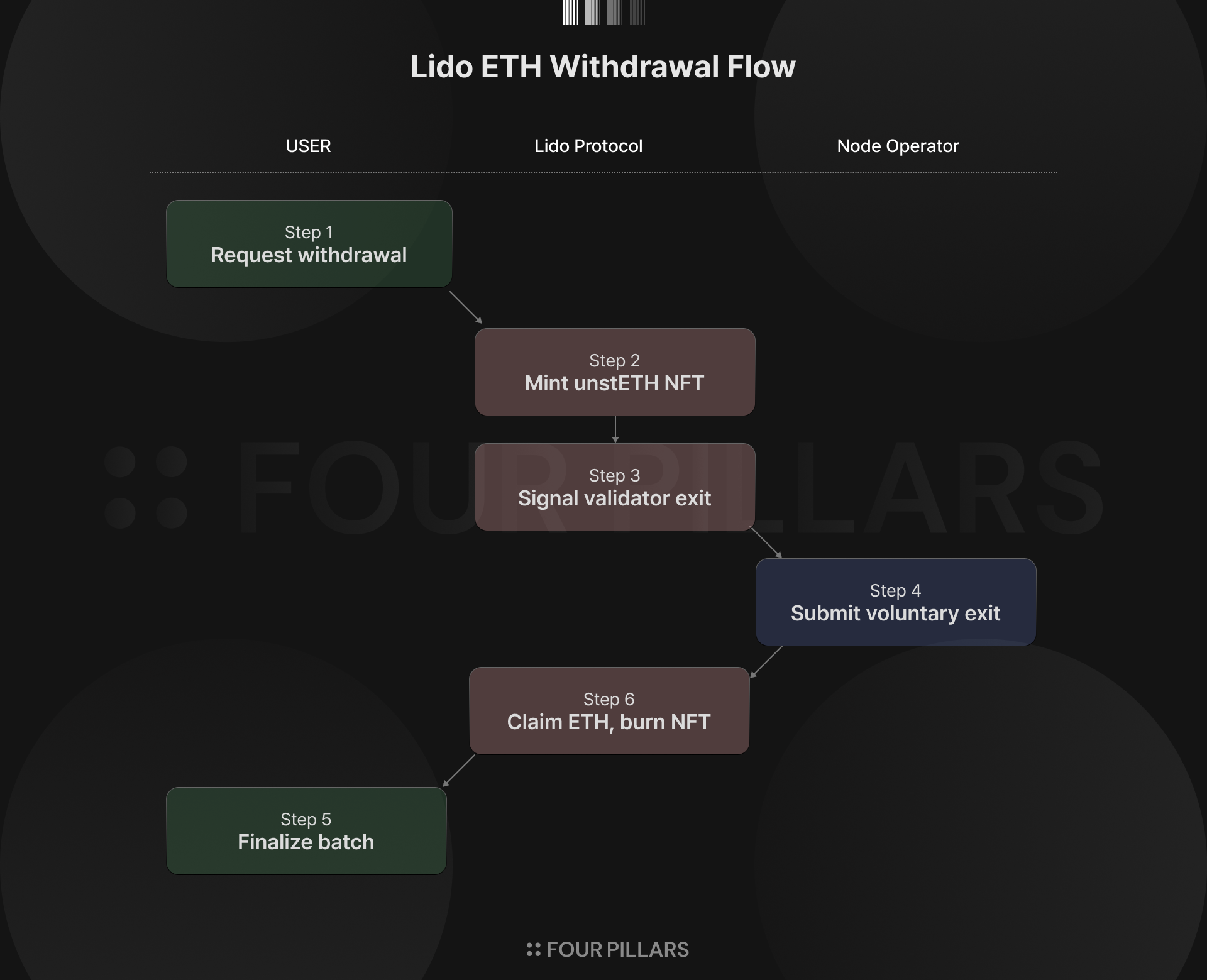

The procedure a user goes through to return stETH and withdraw ETH works through cooperation among three parties: the user, the Lido protocol, and node operators. The steps where the user sends transactions directly are only the two ends, the withdrawal request and the ETH claim, a simple experience. But on the back end, the Lido protocol and node operators handle withdrawal queue management, validator exit requests, withdrawal execution, ETH recovery, and finalization.

The full flow, from the user's perspective, is as follows.

First, the request stage. The user sends stETH or wstETH to Lido's withdrawal contract, WithdrawalQueueERC721, to request a withdrawal. The minimum unit of a request is 100 wei and the maximum is 1,000 stETH. Amounts above 1,000 stETH must be split into several requests. When the user sends a request, a corresponding NFT (ERC-721) called unstETH is minted to the user's wallet. Because this NFT is transferable, the right to withdraw can be moved to another address even while waiting in the queue, and it can be traded on a market such as OpenSea.

Second, the queue-wait and ETH-recovery stage. Lido's withdrawal queue is first-in-first-out, processing the earliest requests in turn. For a request to be finalized, enough ETH to fulfill it must gather in the Lido pool. ETH for withdrawals gathers through two paths: new users' deposit ETH being added to the buffer, and node operators exiting validators to recover ETH from the Beacon Chain.

The node operator's exit process is very important here. When the buffer from new deposits alone cannot fulfill withdrawal requests, the Lido protocol issues a validator exit signal on-chain through ValidatorsExitBusOracle. Node operators monitor this signal, and when they detect an exit request for a validator they run, they submit a voluntary exit message signed with that validator's key to the Beacon Chain. Once the validator exit completes, the ETH that was staked to that validator is recovered into Lido's WithdrawalVault and re-enters the buffer.

Previously, a validator exit was only possible with the validator key the node operator held, so in some cases there was a risk that withdrawals could become permanently impossible. But this dependency is being resolved through EIP-7002, introduced after the Pectra hard fork. This is covered in more detail in 2.8.

Third, the claim stage. Once the user confirms that their unstETH NFT is finalized, they call the contract's claimWithdrawals function to receive ETH. At this point the NFT is burned, and ETH corresponding to the requested amount is transferred to the user's wallet.

Total withdrawal time varies with the length of the queue, the amount of ETH in the buffer, and node operators' response speed. In normal times when Lido operates stably, it ranges from a few hours to a few days, but during periods of a sudden surge in withdrawal requests it can take more than several weeks. Since Lido first enabled withdrawals with the V2 launch in May 2023, the longest queue extensions happened twice, in June 2024 and January 2025, both driven by short-term surges in withdrawal demand following ETH price moves.

Lido processes withdrawals in two modes: Turbo Mode, the normal operating mode, and Bunker Mode, the emergency operating mode. In Turbo Mode, withdrawals are processed as described above. Bunker Mode activates in emergencies such as mass slashing or large-scale validator penalties; in this mode withdrawals are not halted, but the processing speed is intentionally slowed. This is a deliberate mechanism to prevent some users from exiting quickly in an emergency and concentrating losses on the remaining users.

Lido is also steadily working to improve this withdrawal processing speed. In April 2026, a proposal to shorten the VEBO reporting frame was posted to the Lido governance forum. As explained earlier, ValidatorsExitBusOracle issues validator exit signals every fixed frame, and previously this frame was 75 epochs (about 8 hours), with three reports issued per day. The proposal is to reduce this to 45 epochs (about 4.8 hours), increasing it to five times a day. Shortening the oracle's reporting frame reduces the delay from withdrawal request submission to the start of a validator exit. It also has the effect of spreading exit batches more evenly across the day, reducing the volume of exit messages a node operator must process at once.

2.2.3 The Importance of Withdrawal Credentials

Validator operation for Ethereum staking is made up of two key systems. There is the validator key, used for the various signatures needed to participate in the network as a validator, and the withdrawal credentials, which hold the right to withdraw the validator's assets. As stated earlier, in Lido the parties that own these two are clearly separated. Validator keys are generated and held by node operators, but the withdrawal credentials are tied to a Lido protocol smart contract (WithdrawalVault).

The withdrawal credentials address is specified in the deposit message used to register a new validator, and this address must match the address the Lido DAO sets. Node operators must verify this address value through the Staking Router contract's getWithdrawalCredentials function to create the deposit message. Because a node operator cannot arbitrarily set the withdrawal credentials address, the ETH withdrawn upon a validator exit is programmatically routed to the Lido withdrawal vault. Through this structure, Lido can distribute validator operations while ensuring the assets clients deposit follow the proper flow and are available for withdrawal. This is the key mechanism that makes it possible to decentralize Ethereum staking infrastructure, which does not support protocol-level delegation, in a non-custodial form.

2.2.4 Changes After Pectra (EIP-7002, EIP-7251)

The Pectra hard fork, applied to Ethereum mainnet in May 2025, brought two very important changes to the Ethereum staking infrastructure environment: EIP-7002 (Execution Layer triggered exits) and the previously mentioned EIP-7251 (MaxEB).

The new 0x02-type withdrawal credentials introduced in EIP-7251 are the most important change in the staking structure since Ethereum transitioned to PoS. The existing 0x01 credentials have a MaxEB fixed at 32 ETH. The 0x02 type, by contrast, raises the maximum balance that can be staked to a single validator from 32 ETH to 2,048 ETH, and supports a compounding function that automatically accrues rewards as well as partial withdrawals. EIP-7251 is a very important upgrade for large validator operators such as Lido's node operators. It raises node operators' operational efficiency for validator keys they previously had to manage in units of 32 ETH, and it reduces the bandwidth burden on the network as a whole.

EIP-7002 is an upgrade to solve the problem of validator exits depending on the validator key. Before EIP-7002, the only party that could exit a validator and withdraw staked ETH from the Ethereum network was the node operator holding the validator key. So when the Lido protocol needed a specific validator to exit in order to process a user withdrawal request, Lido could not send the exit message directly because it does not know the validator key. Lido had to propagate a signal on-chain through ValidatorsExitBusOracle saying "please exit this validator," and the node operator had to receive that signal and submit a voluntary exit message signed with that validator key to the Beacon Chain. In this structure, if a node operator ignored or delayed the signal, Lido's withdrawal queue processing could be delayed, and in the worst case, if a node operator disappeared without processing the withdrawal, there was a risk that a full withdrawal of the assets could become permanently impossible.

After EIP-7002, a validator exit can be triggered directly through the withdrawal credentials. For Lido, this means the Lido contract can trigger an exit directly, without waiting for a node operator's response. Ethereum is a pure PoS network that does not support protocol-level delegation, and it aimed at a structure where every validator is run directly by the staker. But because most staking in practice proceeded in an indirect, delegated form, this upgrade appears to have been made for that reality. With Ethereum applying EIP-7002 to mainnet, Lido was able to raise the reliability of its withdrawal processing by a level.

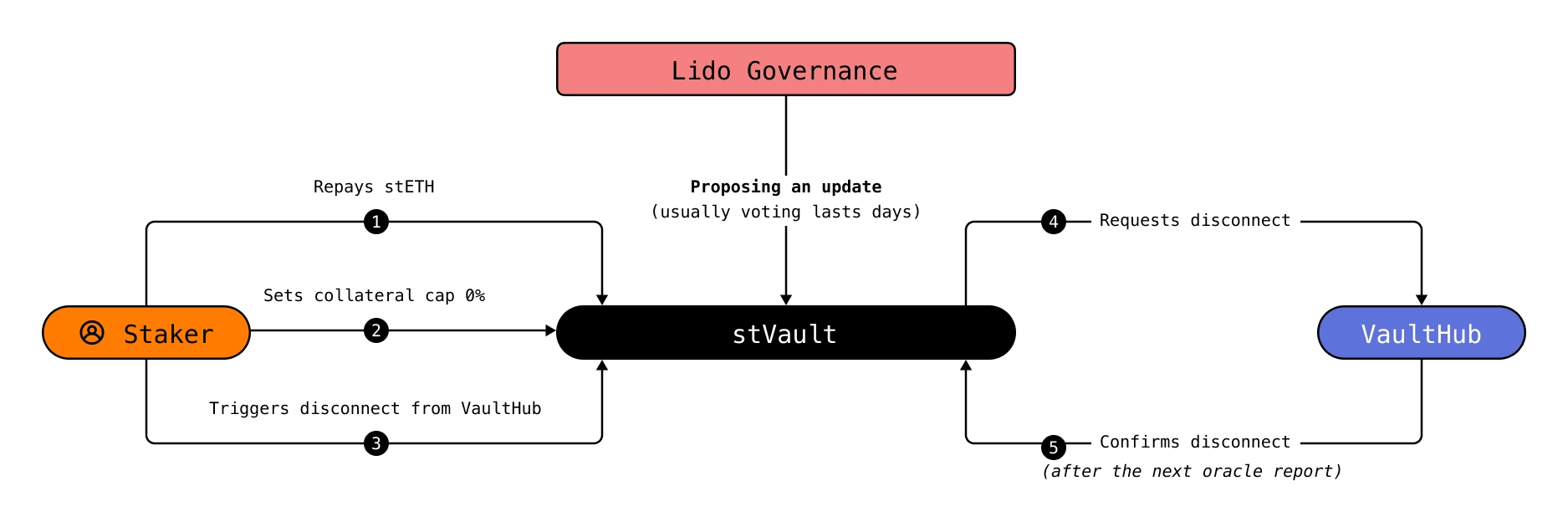

Lido did not, however, adopt these two changes into the protocol immediately after the Pectra hard fork. LIP-27 placed the focus of Lido's Pectra response first on "maintaining the protocol's continued compatibility," and stated that new features such as EIP-7002 and EIP-7251 would be handled in separate proposals. As of June 2026, EIP-7002 has been fully applied. This is why the Lido protocol can trigger validator exits through the withdrawal credentials as described above. The shift to 0x02 credentials and balance-based accounting, then, is moving over in phases. stVaults, by contrast, were designed to support 0x02 credentials from the start at launch. The Lido core pool is in a process of moving over in phases, together with CMv2, SRv3 (the upgraded version of the Staking Router), top-ups, and validator consolidation. This migration is covered in earnest in 2.8.

2.3 The Lido Oracle System

2.3.1 Why Lido Needs an Oracle

Every time the workings of the Lido protocol have been explained so far, the "oracle" has come up. Lido depends on the oracle for important parts such as reward processing and withdrawal processing. This is due to a structural feature of Ethereum, where the consensus layer and the execution layer are separated. Information such as Ethereum mainnet user transactions, smart contract execution, and asset balances lives on the execution layer, but staking information such as validator balances, slashing penalties, and withdrawal processing lives on the consensus layer. Above all, there is the problem that execution layer smart contracts cannot directly read consensus layer state. For an Ethereum contract to use consensus layer data, someone has to bring the Beacon Chain data and deliver it to the contract on the execution layer.

Lido takes a user's ETH and stakes it on the consensus layer, but the liquid token stETH is minted and operated on an execution layer contract. For Lido to reflect the correct stETH balance, it has to bring the balance changes of Lido validators on the consensus layer into the Lido contract on the execution layer. The withdrawal queue, node operator rewards, and the handling of slashing and penalties are all consensus layer information as well, so a mechanism is needed to bring them to the execution layer. The Lido oracle is a mechanism for synchronizing information between Ethereum's execution layer and consensus layer.

2.3.2 The Lido Oracle

The Lido oracle system consists of nine independent oracle members. They are selected through a Lido DAO vote, and each member runs its own Ethereum execution client, consensus client, and Lido KeyAPI. A frame begins every 225 epochs (about 24 hours), and at the start of each frame the nine oracle members each gather data and submit a report to the Lido contract. The Lido oracle operates on a 5-of-9 quorum, where consensus is reached only if five of the nine report the same data. Verification of this quorum is performed in a separate contract called HashConsensus.

The Lido oracle system consists of two core contracts: AccountingOracle and ValidatorsExitBusOracle.

First, AccountingOracle is the most important oracle, updating Lido's accounting state. Every frame, once the agreed report is submitted, the following operations execute sequentially within a single transaction.

- Update the total balance of Lido validators on the Beacon Chain and the number of validators that have completed their exit.

- For each module connected to the Staking Router, update the number of already-exited validators and the number of validators that received an exit request but have not yet exited.

- Call the Lido contract's core handle function to update

totalPooledEtherand trigger the stETH rebase. - Distribute rewards to node operators.

- Finalize the withdrawal requests that this report makes processable.

stETH rebasing, finalization of user withdrawals, and node operator reward distribution are thus all processed at once by this single oracle report. It is fair to say that nearly every state change in the Lido protocol happens through AccountingOracle.

Second, the role of ValidatorsExitBusOracle is to decide which validators must be exited to secure the ETH needed to process the withdrawal queue, and to publish that information on-chain. The nine oracle members each look at the current withdrawal queue length, the amount of ETH in the buffer, and the list of active validators, and compute candidate validators to exit. Once a 5-of-9 oracle consensus is reached, that list is published on-chain, and node operators receive the signal and process the exit of the validators on the list.

Because the oracle holds such large power, Lido also keeps a separate on-chain sanity check on it. OracleReportSanityChecker is a dedicated contract that verifies the reports submitted by AccountingOracle and ValidatorsExitBusOracle. Because the data the oracle provides has a very large effect on protocol state, the oracle's report must pass the on-chain sanity check. The Lido oracle is not simply a system that relays external data but a structure where reporting, consensus, and verification are separated in stages.

2.3.3 Accounting Oracle Second Opinion and the ZK Oracle

As discussed, Lido's oracle system already has a distributed committee, HashConsensus, and on-chain sanity checks, but an essential trust assumption still remains: if five or more of the nine oracle members report wrong (or malicious) data at the same time, the Lido protocol's state could be updated incorrectly. There was an awareness of the problem of verifying the oracle's reported data itself more independently, and the Accounting Oracle Second Opinion discussion started from there.

The idea is to prove the accuracy of the oracle report with a zero-knowledge proof, so that the fact that data reported by an oracle member matches the actual state of the Beacon Chain can be verified without a separate trust assumption. In that case the 5-of-9 quorum remains a mechanism for the efficiency of data collection, while the accuracy of the data is guaranteed by the ZK proof.

This discussion is paused as of April 2026, however. Technically, most of the early milestones were met, and the cost of mainnet proving is achievable at the targeted level of "30 minutes at ~$5 per report," a tenth of the $50 it had been. But because Lido currently prioritizes the 0x02 migration and SRv3 integration, the main integration of the ZK oracle is likely to be pushed back until after that. If the ZK oracle is later introduced, the trust model of the Lido oracle will become a level more robust, and it would be one of the most fundamental changes for reducing stETH's systemic risk.

2.4 The Staking Router

2.4.1 The Concept of the Staking Router

As seen earlier, Lido takes a user's ETH and entrusts the actual validator operation to node operators. Deciding to whom, by what method, and how much ETH to allocate is a very important question. In its early days, the Lido DAO selected sufficiently vetted professional operators as Curated node operators and staked ETH to the validator nodes those professional operators ran.

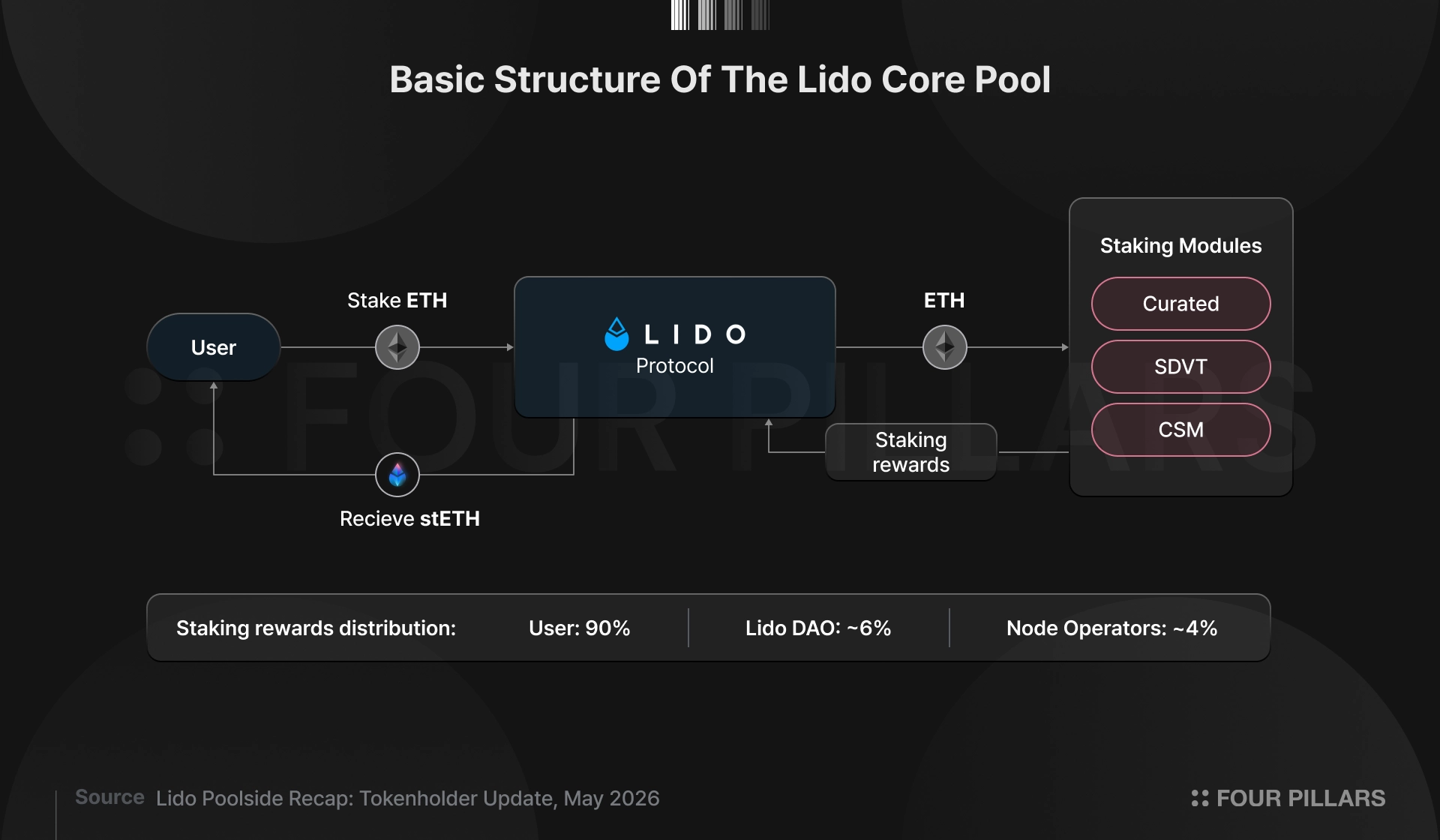

A Curated pool made up of a few professional node operators was favorable for securing stability and operational quality. But as Lido grew, it sought to bring validator operators of a different nature, such as solo stakers, community operators, and DVT clusters, into the Lido ecosystem, aiming for a more decentralized protocol on the node operator side as well. Lido sought to evolve beyond a simple staking liquidity service into Ethereum staking infrastructure, and that required a structure capable of managing several kinds of operator sets within a single protocol.

The Staking Router, introduced in Lido V2, was built to solve this. The Staking Router is a top-level controller contract that registers multiple staking modules, allocates staking shares to each module, distributes protocol fees, and tracks the related information. Each staking module has its own validator set. For example, the Curated operator set that existed from the start is treated, after V2, as one module within the Staking Router: the Curated Module. Each module has its own operator selection method, bond structure, reward distribution method, and risk management method.

When a user deposits ETH, that ETH first accumulates in the Lido buffer and is then allocated to a specific staking module through the Staking Router. This is not something the user chooses directly; it is carried out through Lido's deposit bot and the DepositSecurityModule. In this process, the Staking Router allocates the ETH in the buffer to validators belonging to a module with a specific _stakingModuleId.

The current Lido core Staking Router manages each module's allocation limit with stakeShareLimit. This is a target share, set by the DAO, that each module can take of total active staking. For example, if a module's stakeShareLimit is 10%, that module can run up to 10% of Lido's total active staking and receives no allocation beyond that. The allocation algorithm is a priority-based method called MinFirstAllocationStrategy. As the name suggests, it allocates ETH first to the module with the fewest active validators, within the bounds of each module's limit.

The core of the Staking Router is that the user still uses a single liquid token, stETH, while on the back end validator operation structures of different natures coexist. Because this structure was in place, Lido could afterward gradually draw not only existing professional node operators but also DVT clusters, community stakers, and permissionless operators into the protocol.

2.4.2 The Problem the Staking Router Solves

Early Lido (V1) had a very complex and slow process for onboarding new node operators. Adding a new node operator required the Lido DAO to approve them one at a time through an LDO vote, and the operator's identity, infrastructure capability, and reputation had to be vetted. This process was effective for stability and security, but it made it hard to expand node operator diversity in a fast-growing LST market. And even if Lido wanted to introduce a different operator model such as permissionless participation, V1's single-pool structure had no real method other than adding operators.

Because each module in the Staking Router has its own operator selection policy and bond policy, Lido could create a separate module per operator model and run them simultaneously. While keeping the stability the Curated Module had, it became possible to add as separate modules the Simple DVT module, which accommodates DVT clusters, and CSM, which anyone can join by depositing a bond. The Lido DAO controls the balance among modules by adjusting each module's stakeShareLimit.

Another important point is that the Staking Router made adding new modules possible. Once the Lido DAO decides to introduce a new staking module, that module can implement an interface compatible with the Staking Router and be connected as part of the Lido core pool within the fee structure and per-module limits the DAO sets. This means Lido's node operator ecosystem is not a structure defined once and for all, but an extensible structure where experimental or more efficient new operator models can be added easily. The Staking Router played a very large role in Lido's move from a protocol seen as a risk of Ethereum validator centralization to one leading decentralized staking infrastructure.

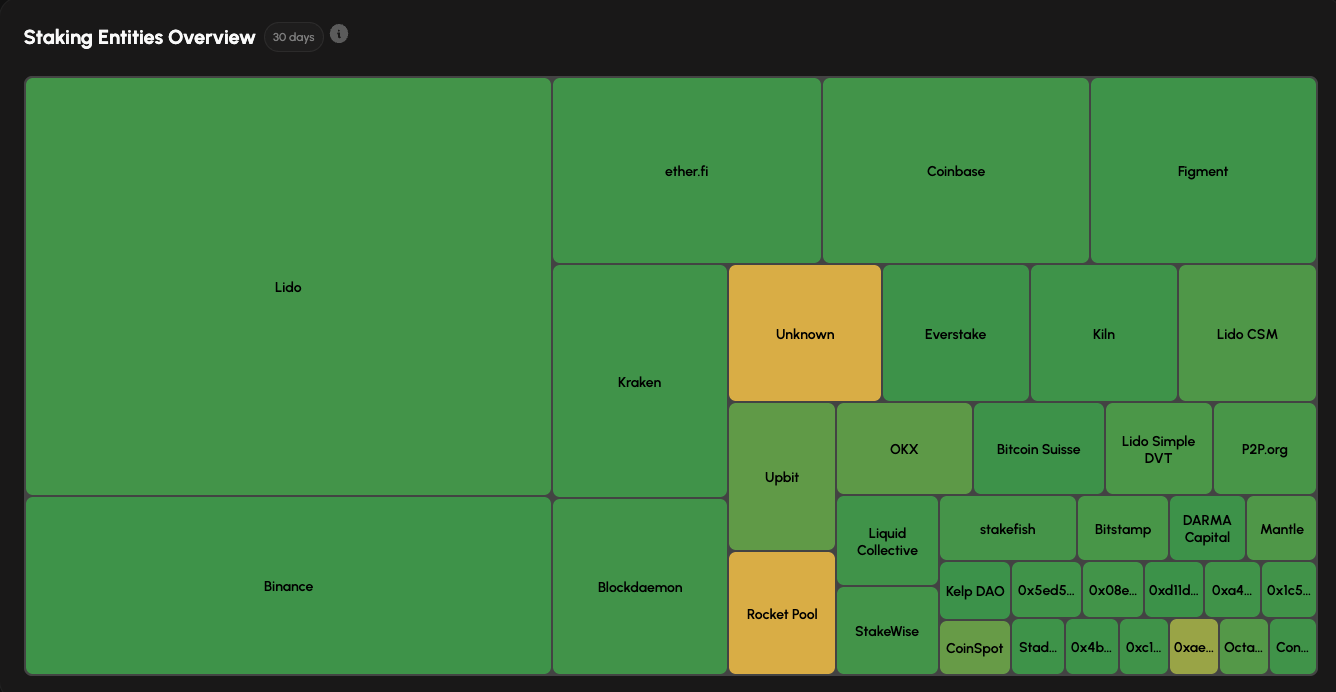

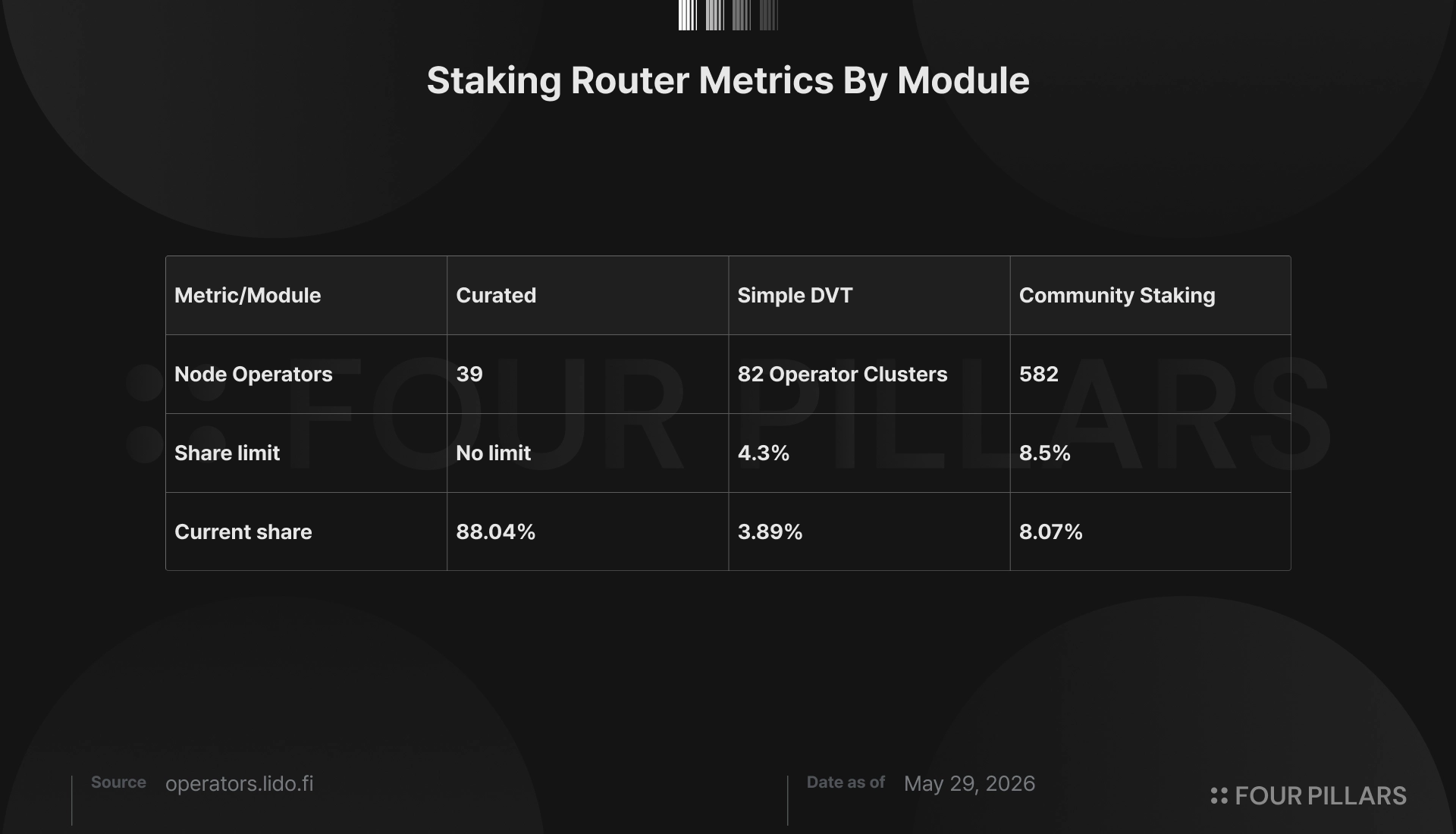

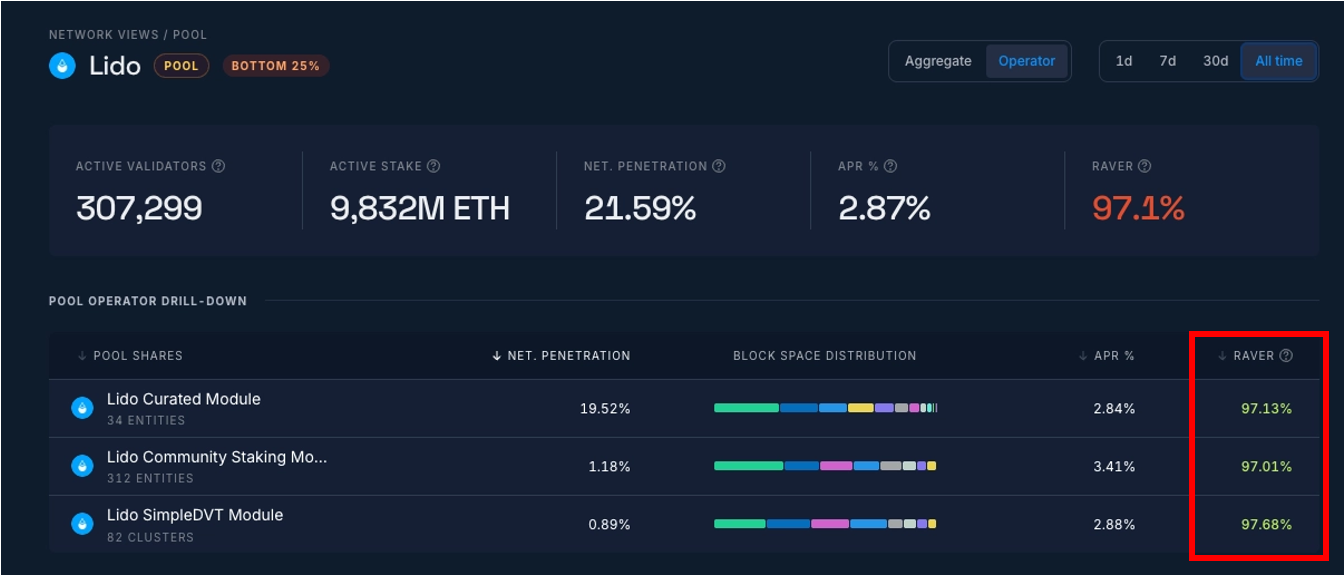

As of May 12, 2026, per the Lido operator dashboard, the Curated Module has 39 registered node operators, the Simple DVT module has 82 SSV- and Obol-based DVT clusters active as operators, and CSM has 578 operators participating permissionlessly. The Curated Module accounts for 88.3%, Simple DVT 3.94%, and CSM 7.76%, but CSM's share is on a steady upward trend. Lido is effectively the protocol running the most diverse node operator network in Ethereum PoS.

2.5 The Curated Module

2.5.1 The Historical Role of the Curated Module

The Curated Module is the oldest staking module, existing since Lido V1. Up to V1, Lido effectively operated as a single pool of Curated operators, and after V2 it was folded into the Staking Router as its first module, named the Curated Module.

The Curated Module is a staking module made up only of professional node operators vetted by the LNOSG (now replaced by the CMC) and approved through a Lido DAO vote. Only node operators whose identity, infrastructure capability, reputation, and business sustainability are sufficiently vetted can participate in this module, and each operator does not deposit a separate bond for validator operation. It is a model of reputation-based participation without a bond. The node operators of the Curated Module are professional node operators selected on the expectation that they will run validators reliably and accurately, without controlling user funds themselves.

Ethereum staking rewards differ with the node operator's skill, and in some cases can lead to a loss of staked principal. Moreover, until EIP-7002 was introduced in the Pectra hard fork, a validator exit absolutely required the validator key the node operator held. This meant that if a node operator suddenly disappeared or did not respond to a withdrawal request, Lido could not exit that validator. Ownership of the assets does not pass to the node operator, but because withdrawal execution depended on the node operator, there was a possibility of ETH that could not be recovered. So a Lido Curated operator had to be vetted not only on operational skill but also on identity, reputation, and business sustainability.

The Curated Module was, in other words, the Lido protocol's "professional operator layer." Lido was able to mint stETH and simplify the staking UX for retail users because vetted professional node operators handled validator operations on the back end. But this structure was also the starting point of the Lido centralization debate. As Lido grew, "who runs Lido's validators" became not a simple operational matter but one directly tied to Ethereum decentralization. The Curated Module provided stability, but it was hard to escape criticism given that operator selection was a permissioned structure chosen directly by the Lido DAO.

As of May 2026, about 88.3% of the Lido core pool is run through the Curated Module. The Curated Module serves as a fallback that operates when other modules' limits are full, when an emergency exit occurs in a problem situation, or when there are no validators available to deposit to. The Curated Module remains the most important module, serving as a safety net for the availability of all of Lido.

2.5.2 LNOSG (Now Transferred to CMC) and Node Operator Selection

Selecting node operators in the Curated Module is very important. As seen in the previous section, validator operation is technically complex, and a node operator's skill can lead to rewards, penalties, and in the worst case slashing. The Lido DAO selected node operators with a professional review process from the start. The separate organization for node operator selection in the Curated Module was LNOSG (Lido Node Operator Sub-Governance Group).

LNOSG's role is closer to that of a recommender through vetting than a final decision-maker. When operator candidates apply, LNOSG evaluates technical capability, infrastructure setup, operational experience, client usage, geographic distribution, and security posture, and proposes a candidate list to the DAO. Which operators are ultimately included is decided through a DAO snapshot vote in which LDO token holders participate.

The onboarding process for a new node operator to join the Curated Module follows a very strict procedure.

- When Lido publicly announces a new node operator recruitment, candidates apply through an official application form.

- LNOSG evaluates the applicants together with Node Operator Mechanism (NOM) workstream contributors. The criteria include not only operational performance but also contribution to Lido's overall decentralization, such as geographic distribution, client diversity, and infrastructure hosting method.

- Candidates LNOSG deems suitable are referred to a Lido DAO snapshot vote.

- Node operators who pass the vote are added to the Curated Module.

- The selected node operator goes through a verification stage on testnet and is then onboarded as a node operator on mainnet.

In the Wave 5 onboarding in 2023, 7 new node operators were selected out of 117 applications submitted by professional node operators.

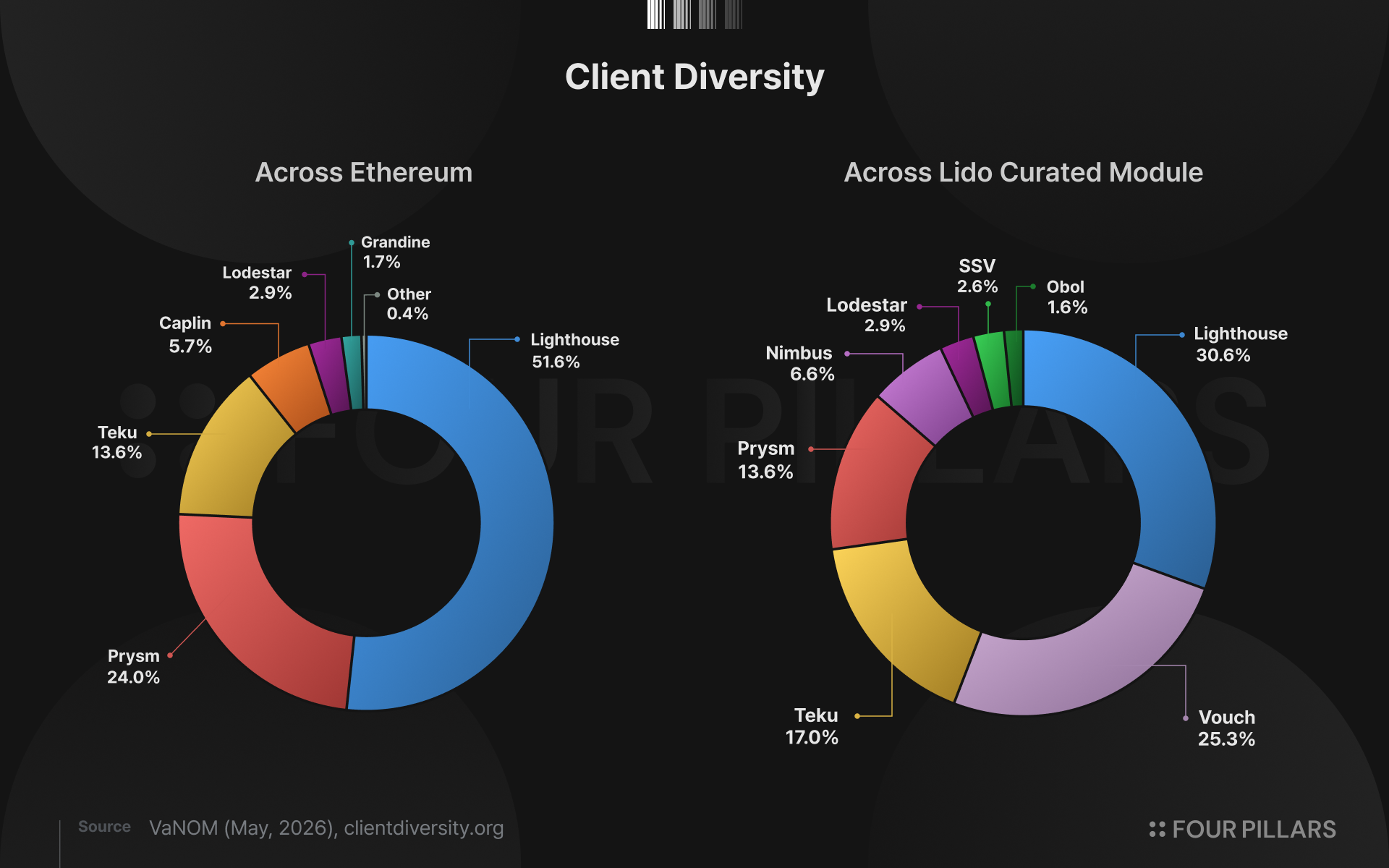

This strict selection method in the Curated Module brought positive effects to Ethereum infrastructure beyond Lido. Lido evaluated factors important for Ethereum infrastructure decentralization, such as geographic distribution, infrastructure hosting method, and client diversity, as important criteria in Curated Module selection. This was not just a standard for Lido to run its own pool stably; it amounted to Lido presenting the market with an operator standard that contributes to the decentralization of Ethereum PoS as a whole. Criteria such as geographic distribution, client diversity, and infrastructure hosting method gradually became important evaluation factors across Ethereum infrastructure in general, including other LST protocols and institutional staking services.

In practice, the Lido node operator set shows more balanced metrics than the Ethereum network as a whole on geographic distribution, infrastructure composition, and client diversity. Had Lido selected node operators on operational performance alone, all of Lido would likely have ended up dependent on a few large infrastructure providers, which would also have weakened Ethereum's own decentralization. In this sense, the Curated Module's selection criteria played a positive role not only for Lido's own stability but also for the resilience and decentralization of Ethereum PoS.

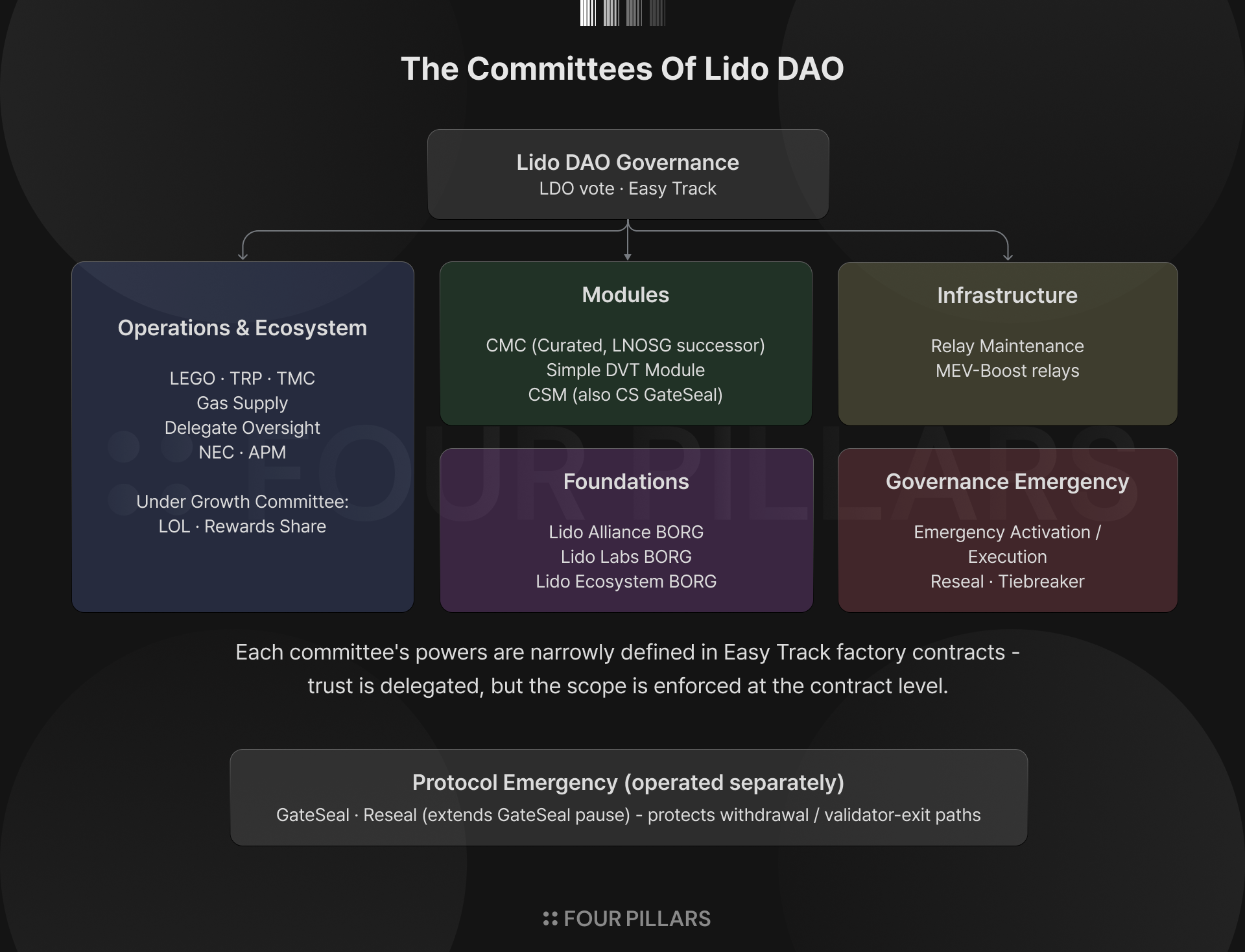

As discussed later, LNOSG was fully dissolved after a governance vote in March 2026. To build a more granular and systematic governance-based operating process, the roles and responsibilities LNOSG had handled were transferred to a new committee, CMC (Curated Module Committee), which oversees not only CMv1 but also the CMv2 and Simple DVT discussed later.

Lido transparently publishes per-module metrics through its quarterly VaNOM (Validator & Node metrics) report, which is an important guide for the entire Ethereum validator community hoping to onboard into the Lido Curated Module.

2.5.3 The Limits of the Curated Module

The Curated Module's biggest strength is stability. Through a Curated Module made up of strictly selected professional node operators, users who stake through Lido can get a stable staking experience without running a validator themselves. But the Curated Module has a few clear limits.

The first limit is that the Curated Module is an unavoidably permissioned structure. Being selected through strict LNOSG vetting was necessary for quality control, but it was also the core reason Lido faced the criticism that it "depends on a few professional operators." Users feel they are participating in decentralized staking through stETH, but the actual validator operation can be concentrated among a few professional operators Lido selected directly.