Table of Contents

- Key Takeaways

- 1. Overview: Staked Assets as the Base Primitive for Institutional On-Chain Entry

- 2. Global Trends: Institutional Staking Is Becoming a Structured Pipeline

- 2.1 Anatomy of the Pipeline: Five Functional Modules and Five Product Cases

- 2.2 Competitiveness, Redefined: From Yield to Structural Design

- 3. Opportunities in the Korean Market: Importance of Collaboration

- 3.1 Current State

- 3.2 Whose Assets Will Be Staked, and to What End?

- 3.3 Differences by Digital Asset

- 3.4 Role Separation Is What Makes the Pipeline Work

- 3.5 Checklist for Preparing for Institutional Staking in Korea

Researcher

Key Takeaways

- Staked assets are becoming the base primitive for institutional on-chain strategies because they combine price exposure, protocol rewards, network participation, and collateral utility.

- Institutional staking is no longer just about earning the highest APR; it has become a structured pipeline involving custody, validator operation, liquidity management, reporting, and regulatory compliance.

- Global staking products are evolving across five models: non-custodial staking, white-label validator infrastructure, liquid staking, custodial staking, and regulated wrappers such as ETFs and ETPs.

- In Korea, institutional staking is still blocked by unresolved regulation around corporate crypto ownership, tax and accounting treatment, custodian permissions, and the distinction between treasury staking and client-asset staking.

- The most realistic path for Korea is a collaborative model where regulated financial institutions handle custody and compliance, while crypto-native infrastructure firms handle validator operation, protocol risk, and on-chain execution.

This article is adapted from "Korean Blockchain Guidebook for Institutions 2026," jointly published by Four Pillars and Pantera Capital. The full report covers 14 more themes for companies and institutional investors.

1. Overview: Staked Assets as the Base Primitive for Institutional On-Chain Entry

Institutional investors allocate capital over decades, and every new asset class arrives as both a risk and an opportunity. The crypto market, which took off with Ethereum's 2015 launch, now exceeds $2 trillion in market capitalization as of 2026, a scale that global asset allocators can no longer ignore. With BlackRock, Fidelity Investments, and Franklin Templeton rolling out products alongside growing client demand for crypto exposure, many institutions have reached an inflection point: the risk of staying out now outweighs the risk of entering.

So where, among all crypto assets, are institutions actually focusing? The answer is "infrastructure assets." In traditional finance, institutions invest in assets with essential-good characteristics, high entry barriers, and predictable revenue: power grids, telecom networks, data centers, airports. By the same logic, blockchains such as Ethereum and Solana, with their network effects, proven security, and deep liquidity, can be read as "digital infrastructure." A grid operator earns revenue in proportion to usage; a blockchain validator earns rewards tied to network usage. This is not an entirely new asset but a digital extension of an existing investment model. And because these infrastructure assets run on Proof of Stake (PoS), staking sits at the center of any institutional crypto strategy.

From an institutional perspective, the first thing staked assets offer is native yield. In traditional finance, making an asset produce yield requires trading, lending, rollovers, or leasing, which means asset managers, brokers, and operational infrastructure on top. A staked asset earns by being held; rewards are generated automatically by the protocol. That simplifies operations and makes the yield transparent at the same time. Reward rates are verifiable on-chain, reward history is permanently recorded on the blockchain, and both meet institutional accounting, audit, and reporting needs. The second thing staked assets offer is composability and scalability. Staking locks up the underlying asset, but Liquid Staking Tokens (LSTs) such as Lido's stETH and Coinbase's cbETH remove that constraint. While the underlying asset accrues rewards in the protocol, the LST works as a liquid asset: posted as DeFi lending collateral, supplied to DEXs, or used as the underlying for interest rate swaps, yield tokenization (Pendle, for example), and options.

Institutional on-chain entry is therefore being redefined. It is no longer "holding tokens"; it is “value creation through network participation”. Holding ETH and holding staked ETH are not the same position. The former is passive exposure to price; the latter bundles network security contribution, protocol rewards, and on-chain collateral optionality into one position. Viewed this way, staked assets are the base-layer asset of on-chain finance, the layer on which LSTs and derivative products are stacked. In an institutional on-chain strategy, they are not an optional add-on but the basic unit.

2. Global Trends: Institutional Staking Is Becoming a Structured Pipeline

2.1 Anatomy of the Pipeline: Five Functional Modules and Five Product Cases

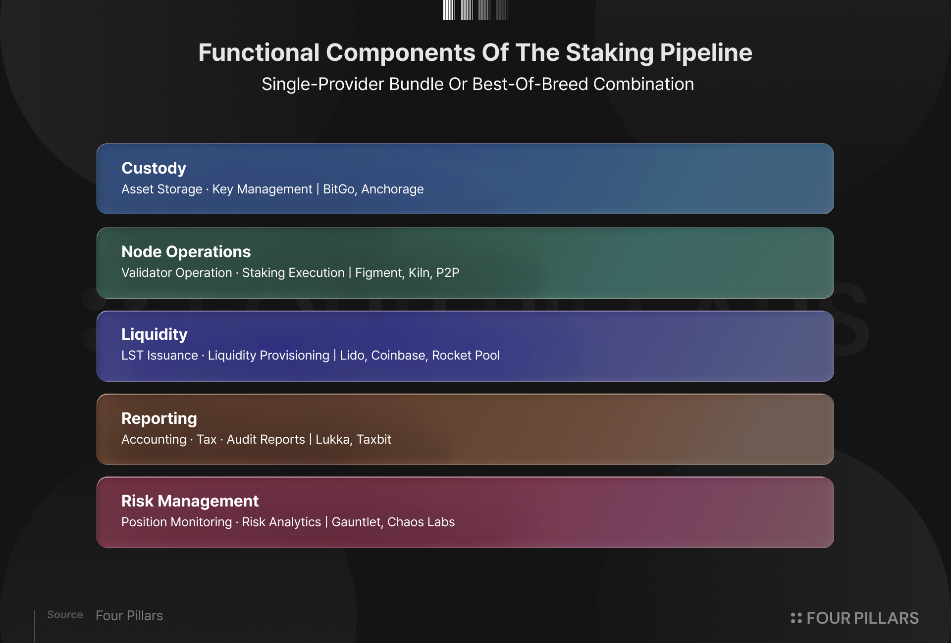

In global markets, staked assets no longer fit under a single staking service category. They have become a structured product stack that combines several functional layers: custody, staking execution, liquidity management, reporting, and regulatory compliance. The stack is assembled modularly to fit each institution's needs.

Behind this shift is the specific shape of institutional demand. For a retail user, staking is a simple choice: deposit where APR is highest. For an institution, it is an operational activity that pulls in accounting, tax reporting, risk management, liquidity planning, and compliance all at once. To meet that composite demand, institutional staking pipelines tend to break out into five functional modules.

Institutions can source these functions bundled from one provider, for example Coinbase Prime offering custody, node operation, and reporting together, or they can pick the best provider for each layer and build their own stack. Bundling keeps operations simple but gives up control and customization. Unbundling removes single points of failure and adds flexibility, but it demands real integration capability. These two approaches give rise to roughly five product cases in the market.

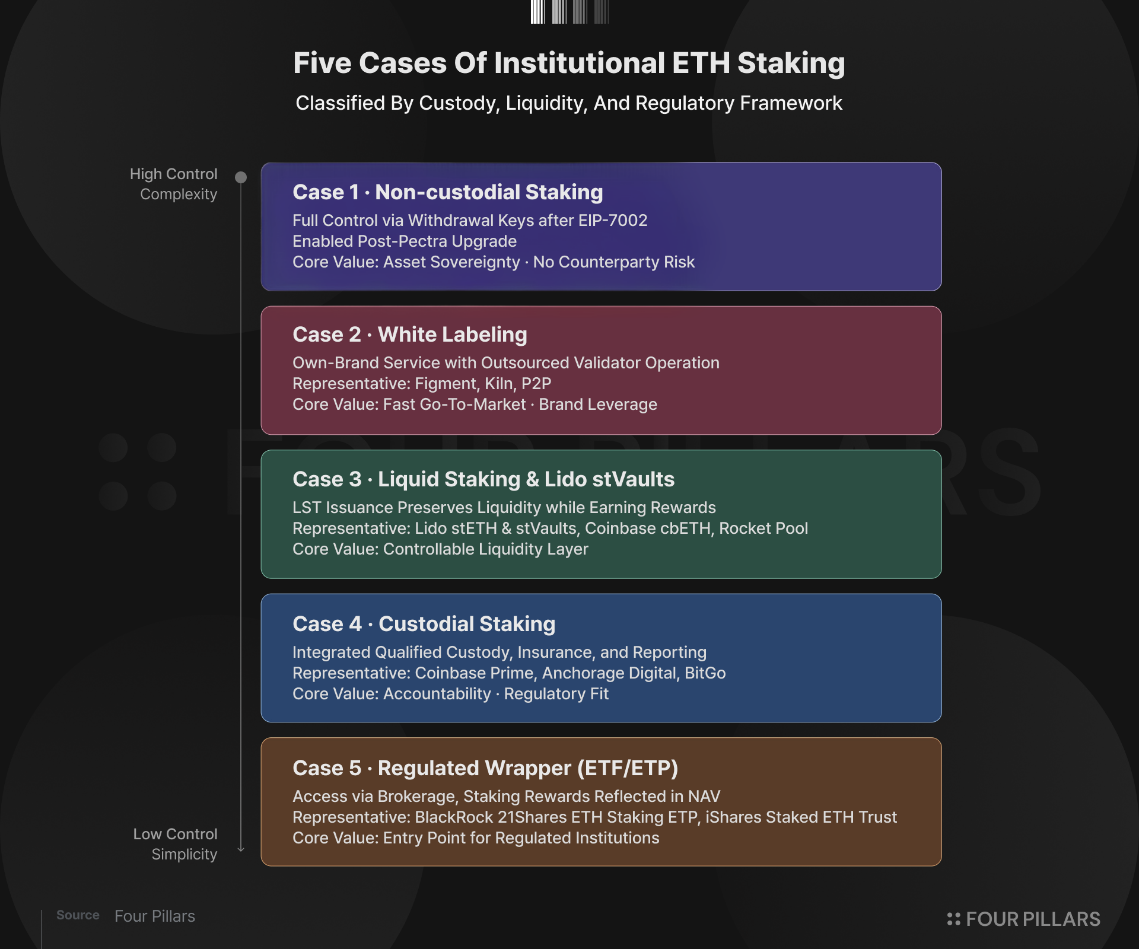

Case 1: Non-custodial Staking

In the first case, the institution keeps control of its assets and only outsources the staking itself. Ethereum does not support delegation at the protocol level, but the validator key that signs at the consensus layer can be separated from the withdrawal key that represents ownership of the staked ETH. That separation makes an indirect form of non-custodial staking possible.

Until early 2025, full non-custodial staking on Ethereum was structurally hard to pull off. Withdrawal authority was bound to the validator key, so if the staking provider holding that key did not cooperate, the institution had no way to recover its assets. The structure directly contradicted what institutions most wanted: control of the asset.

EIP-7002 (Execution Layer Triggerable Withdrawals), shipped in the Pectra upgrade in May 2025, removed that constraint. Withdrawals can now be triggered by the withdrawal key alone, the key representing ownership of the staked asset, and Ethereum finally has the foundation for practical non-custodial staking. Two frictions remain. A staking provider could still, in principle, execute a withdrawal using the validator key without the customer's consent. And the institution now has to manage the withdrawal key itself, which is a real UX hurdle in practice.

Case 2: White Labeling

Representative examples: Figment, Kiln, P2P, and other specialist operators

In the second case, only the infrastructure operation is outsourced to a specialist. The institution offers staking under its own brand while a specialist runs the actual validators, in either custodial or non-custodial form. This is how exchanges, wallet providers, and custodians that already have a customer base and a brand can ship staking products quickly without owning the operational complexity.

Case 3: Liquid Staking & Lido stVaults

Representative examples: Lido stETH & stVaults, Coinbase cbETH, Rocket Pool

The third case pairs liquidity with staking. Staking has always meant lock-up, and on Ethereum the unstaking window, which can run from several days to several weeks, is a real liquidity risk for an institution. Liquid staking issues a Liquid Staking Token (LST) against the staked position, so the institution keeps earning rewards while retaining liquidity and, on top of that, gaining on-chain usability.

Until recently, the main thing holding institutions back from existing liquid staking services was the lack of control. In Lido's original setup, the protocol manages operators by module and a user's deposited ETH is programmatically delegated, so an institution could not designate a specific operator or tailor the setup to its own requirements. Institutional ETH could end up pooled with ETH from anonymous individuals, which failed institutional needs around compliance, accounting, and reporting.

Lido's stVaults, recently live on mainnet, fix this problem and show where institutional liquid staking can go next. stVaults is a modular structure where the institution designates its own operators and builds a customized vault. The institution picks its trusted node operators, keeps control over deposits and withdrawals, opts into full or partial liquidity on the position, and negotiates its own fees. At the same time, it still gets the UX and operational convenience of Lido's infrastructure and benefits from the deep liquidity and strong network effects of stETH across the DeFi ecosystem, and the stETH minted against its position remains usable across on-chain finance for additional yield or for rapid withdrawals. That resolves almost every institutional pain point around ETH staking at once, and since launch it has been one of the most talked-about solutions on the market.

Case 4: Custodial Staking

Representative examples: Coinbase Prime, Anchorage Digital, BitGo

The fourth case merges custody and staking. The institution hands ETH to a licensed custodian that also runs the staking. It is the most straightforward path.

What matters here is accountability. Even the highest yield is a non-starter if custody is not safe and not compliant. For institutional investors, accountable custody is the precondition that comes before staking.

Coinbase Prime is the clearest example. Prime delivers the following as an integrated service:

- Qualified Custody: Asset custody as a qualified custodian under SEC regulation.

- Native Staking: Direct staking on supported networks.

- Comprehensive Reporting: Detailed reports covering reward accrual, return on principal, and tax data.

- Insurance Coverage: Insurance on assets held in custody.

Anchorage Digital goes one step further. Its federal bank charter from the OCC (Office of the Comptroller of the Currency) lets institutions access staking entirely inside the regulatory framework of traditional finance.

The trade-off with the custodial route is familiar: asset control is delegated to a third party, and intermediary fees run higher.

Case 5: Regulated Wrapper (ETFs and ETPs)

Representative examples: BlackRock iShares Staked ETH Trust, 21Shares ETH Staking ETP

In the fifth case, institutions reach staking exposure through traditional financial wrappers. ETFs and ETPs plug staking yield into the brokerage accounts, custody relationships, and regulatory frameworks an institution already uses.

BlackRock's iShares Ethereum Trust recently expanded its structure to include staking. Institutions can access it through existing securities accounts without a new custody relationship or wallet infrastructure, staking rewards accrue into the NAV, and the product carries the regulatory certainty of an SEC-approved vehicle.

In Europe, 21Shares and CoinShares already run ETPs that include staking rewards, which gives a viable entry point to institutions that cannot engage directly on-chain because of regulatory constraints.

The wrappers have its limits. Investors have no direct control over the underlying asset, and expanded uses such as posting staked assets as collateral or participating in DeFi are off the table. ETFs and ETPs are best understood not as substitutes for on-chain native strategies but as entry points or complements to them.

2.2 Competitiveness, Redefined: From Yield to Structural Design

Pulling the five cases together, the basis of competition in the overseas staked-asset market has shifted. The old contest, "who offers the higher APR," has given way to a new one: "who designs the better structure." Here, "structure" covers the custody setup that meets the institution's regulatory requirements, the product design that balances liquidity and staking, the reporting setup that meets accounting, tax, and audit demands, and the operational setup that spreads risk and preserves control.

The role of the players in the institutional staked-asset market is moving from staking-service provider to full-stack financial infrastructure provider. Global markets are already moving in that direction.

3. Opportunities in the Korean Market: Importance of Collaboration

Korea's institutional staking market is not yet at the execution stage. Corporate trading of virtual assets is opening in phases, but as of April 2026 the issuance of real-name trading accounts to professional-investor corporations has not formally begun, and the Digital Asset Basic Act is still under review in the National Assembly. Core regulatory variables remain unsettled: how yields are treated for accounting and tax, and the scope within which custodians can offer staking services. The first condition for any institutional staking pipeline is that "an institution can acquire virtual assets." In Korea, even that precondition has not fully cleared regulation yet.

That is exactly why the businesses likely to capture the early market after regulations clear are the ones already building asset-by-asset and structure-by-structure pipelines today. The point is not to wait until every rule is finalized. It is to design the operating model and partner structure now, so that the pipeline can connect the moment regulation opens.

3.1 Current State

In the Korean market, institutional staking is a structural-design problem more than a yield problem. Three characteristics of the current stage have to come first.

3.1.1 Korea's Distinctive Regulatory and Audit Environment

Corporate acquisition of virtual assets is heading toward being allowed. But core questions are still open: Is deploying an acquired asset into staking "investment" or "business activity"? Can a custodian use client assets for staking? Until those are answered, institutions cannot put real size on-chain.

Once real-name account issuance, justification of transaction purpose and fund origin, Travel Rule compliance, corporate tax disclosure, and liability attribution in case of incidents are all in scope, the criterion a Korean institution uses to choose a staking pipeline is not the highest yield. It is whether the structure can be explained inside Korea's regulatory and audit environment. The Financial Services Commission has, alongside expanding corporate market access, recommended using third-party custody managers, and its AML plan sets a direction of limiting transactions with overseas businesses and personal wallets to low-risk cases.

3.1.2 A Global Staking Market Where Roles Are Already Split by Module

As covered in Section 2, the global institutional staking market has developed into a structured stack of functional layers. Custody sits with regulated custody businesses such as Coinbase Prime, Anchorage, BitGo, and Fireblocks. Validator operation sits with specialist operators such as Figment, Kiln, P2P, and Blockdaemon. Productization and reporting sit with each asset manager. When building an institutional staking business in Korea, the live question is how to localize that structure to Korea's regulatory environment.

3.2 Whose Assets Will Be Staked, and to What End?

The first thing to pin down in any conversation about institutional staking is whose assets are being staked. An institution staking digital assets it holds on its own balance sheet, and an institution offering a staking service on top of client assets it custodies, are not the same business.

A related point: in Korea, staking is not treated under a single rule. Published legal commentary makes the distinction clear. A structure in which the user delegates directly from their own wallet and the service provider never holds the private key, and a structure in which the operator custodies, moves, or manages client assets and distributes rewards, can be assessed very differently. The weight of VASP status or licensing is not one uniform premise across "institutional staking." It rises sharply in the client-asset model in particular. Without sorting this out first, two very different regulatory and operational profiles get lumped under the same name.

3.2.1 Proprietary Asset (Treasury) Model

An institution deploys its own assets into staking. Since no asset transfer or client custody is involved, the regulatory burden is lighter. The real decision variables are the internal approval process, accounting and disclosure treatment for the staking position, liquidity policy (how to absorb the unstaking delay), and the risk and return that follow from validator operation quality. A corporation that acquires ETH and runs validators either itself or through a contracted operator falls into this category.

The open operational variable here is the relationship between the corporate investment cap (5% of equity capital) and the staking position. Whether staked assets count toward the cap at face, how assets in the unstaking queue are treated, and whether accruing rewards that push the position above the cap trigger mandatory disposal, are questions the guidelines have not yet settled. An institution looking at treasury staking needs to preserve enough design flexibility to absorb those answers when they come.

3.2.2 Client Asset-Based Service Model

The operator takes client assets into custody and offers a staking service that layers additional yield on top. Because custody, management, and transfer of assets are all in play, regulation and licensing weigh much more heavily. A package of obligations applies: the same-type, same-quantity actual-holding requirement under the Virtual Asset User Protection Act, VASP registration, ISMS certification, an internal control framework, and the bank's AML risk assessment. Once the Digital Asset Basic Act takes effect, custody-business registration, and potentially a trust-business authorization, may also be required. A custodian or an exchange offering a staking product fits here.

The two models both "do staking," but the infrastructure they require and the regulatory response they demand are very different. The first step for any institution looking at digital asset staking is to decide which of the two it is.

3.3 Differences by Digital Asset

Institutional staking looks like one product class, but the asset being staked reshapes the infrastructure, the operational difficulty, and the risk profile. Miss that, and the pipeline is designed wrong from the start.

3.3.1 Ethereum: The Most Important and the Hardest Asset

Ethereum staking does not support delegation at the protocol level. To run a validator, the institution has to stake 32 ETH or more (up to 2,048 ETH per single validator under current rules) and run the node itself. The absence of protocol-level delegation complicates pipeline design. What helps is that Ethereum separates the validator signing key (the BLS validator key) from the withdrawal credentials that control ownership of the asset. Using that split, an institution can build a non-custodial setup for ETH in which it keeps withdrawal authority over the asset and hands only validator operation to a specialist. Most institutional staking services offered by validator businesses are built on this pattern. Protocol-level delegation is not possible, but a de facto non-custodial delegation through key design has become the working standard for institutional staking on Ethereum.

The UX is still heavier than on networks that support delegation at the protocol level. On a delegated PoS network, a user picks a validator in their wallet and joins staking with a single delegation transaction. In Ethereum's non-custodial setup, the institution needs a working grasp of key structure: what the BLS signing key and the withdrawal credentials each do, how to configure keys at the time of deposit, how to set the withdrawal address, and how to sign the exit message. For an institution, that is not only a UX issue but a compliance issue. It has to be able to verify which key has which authority, who is signing what, and that the configuration matches what was intended.

The real choice set for an institution staking ETH comes down to four options. One: run the validator keys yourself, end to end. Two: keep asset control and hand off only validator operation to a specialist, non-custodially. Three: custody the asset with a regulated custodian that also runs the validator. Four: use a liquid staking protocol such as Lido. Beyond direct participation via on-chain protocols, this also includes structures where institutions access Lido Core or stVaults through regulated custodians. The asset's movement path and the party holding the keys change with each choice, which is why pipeline design matters so much on Ethereum.

Validator infrastructure stability and operator know-how are the variables that set risk and return on Ethereum. Slashing, which can cause meaningful loss of principal, is a sensitive one. Double signing triggers immediate slashing, and it is the kind of condition an operator mistake can produce on its own. Node downtime costs more than missed rewards; it incurs penalties, and sustained downtime eats principal. Attestation participation rate and block-proposal success rate are reflected straight into rewards, so operational quality drives the yield as well.

Infrastructure has to scale linearly with the size of the staked position, and entry and exit queues exist and move around. Queue delay collides directly with an institution's liquidity policy. BlackRock's registration materials for its Ethereum staking ETF say as much, stating that a "Liquidity Sleeve" of between 5% and 30% of total assets will be kept unstaked to meet redemptions. The same document notes that validator performance, uptime, and proper attestation all affect rewards. ETH staking is not a "deposit it and earn fixed interest" product. It is closer to an infrastructure business in which operational quality and liquidity design feed straight into both the yield and the loss defense.

In the Korean context, that points to a clear preference. Rather than a structure that relies on moving client assets outside or re-entrusting them to another party, the sensible first look is a structure that separates asset custody from validator operation and can be explained end to end. Overseas institutional products follow the same logic: the custodian keeps control over asset movement, and the staking service provider only handles validation. The early Korean market will be much more receptive to that shape.

3.3.2 Delegatable PoS Networks (DPoS): A Simpler Structure

On networks that support delegation at the protocol level, including the Cosmos chains, Solana, Sui, and Aptos, an institution delegates only validation authority to a validator while keeping ownership of its assets. No asset movement occurs, and the key custody setup stays relatively simple. From a regulatory angle, this structure is less likely to be treated as "transferring assets to a third party," so pipeline design is more compact than on Ethereum.

On delegation-style networks, though, staking delegation often comes with a delegation of on-chain governance voting rights. When a validator votes on proposals that carry regulatory weight, such as network upgrades, foundation fund movements, or sanctions and freezing measures, that vote can be read as an expression of the delegator's position. An institution picking validators therefore has to look at governance history and stance alongside validation performance, and it needs an internal process that either monitors the validator's governance activity directly or requires periodic reports.

3.3.3 Staking Setups That Move Custody Are the Ones to Avoid

Whatever the asset, a staking setup in which the institution's asset changes custody into the hands of a third party is the hardest form to justify under Korean regulation. The same-type and same-quantity holding obligation under the Virtual Asset User Protection Act, and the custody-business framework of the Digital Asset Basic Act, both point to designs that keep control of the asset with the institution or with a regulated custodian the institution has contracted.

3.4 Role Separation Is What Makes the Pipeline Work

An institutional staking pipeline has three parts: asset custody, validator operation, and reporting and evidence. Each part calls for a different kind of capability. The realistic design keeps custody and validator operation in separate hands. Custody goes to the institution itself or a regulation-friendly custody partner. Validator operation, performance optimization, slashing defense, incident response, and reward management go to a specialist. That split is efficient.

Custody sits inside the institution or with a regulated custodian. Private key control, withdrawal authorization, and legal ownership of the asset have to remain cleanly on the institution's side. In Korea, domestic custodians such as KODA and KDAC hold VASP registration and institutional-grade certifications (ISMS, SOC, ISO 27001), and under the Digital Asset Basic Act, custody will be carved out as its own registered category.

Validator operation belongs to a specialist. Running validators at scale, operating slashing-defense infrastructure and insurance, and absorbing protocol upgrades on time all rely on technical know-how built up through hands-on operation. You cannot stand that up in a short window. Operating history is the evidence that earns trust. As noted above, each digital asset shapes the operation differently. Ethereum needs key management and slashing defense. Solana needs high-performance node operation. Cosmos-family chains demand frequent upgrade response and on-chain governance participation. Each stack calls for its own technology and its own operator instincts. A strong track record on one network does not guarantee the same level on another. An institution running a multi-asset staking portfolio then faces a second axis of partner design: hand every asset to one operator, or pair each asset with the specialist best suited to it.

Reporting and evidence is the axis that wires the first two into the institution's internal decision-making. Staking positions, reward history, slashing events, and unstaking records have to flow into the institution's accounting, audit, and disclosure systems. For a Korean corporation that also means corporate tax filing, fair value measurement, and investment cap monitoring.

Having one provider do all three is unrealistic, and even where it is possible, an institution has strong incentives to split the work to avoid concentrated risk. When picking each party in the pipeline, a Korean institution will also lean toward a domestic combination over a foreign one. The explainability Korea's regulatory environment calls for, across real-name accounts, Travel Rule, audit, and incident liability, is secured most cleanly by providers that operate inside the domestic regulatory system.

3.5 Checklist for Preparing for Institutional Staking in Korea

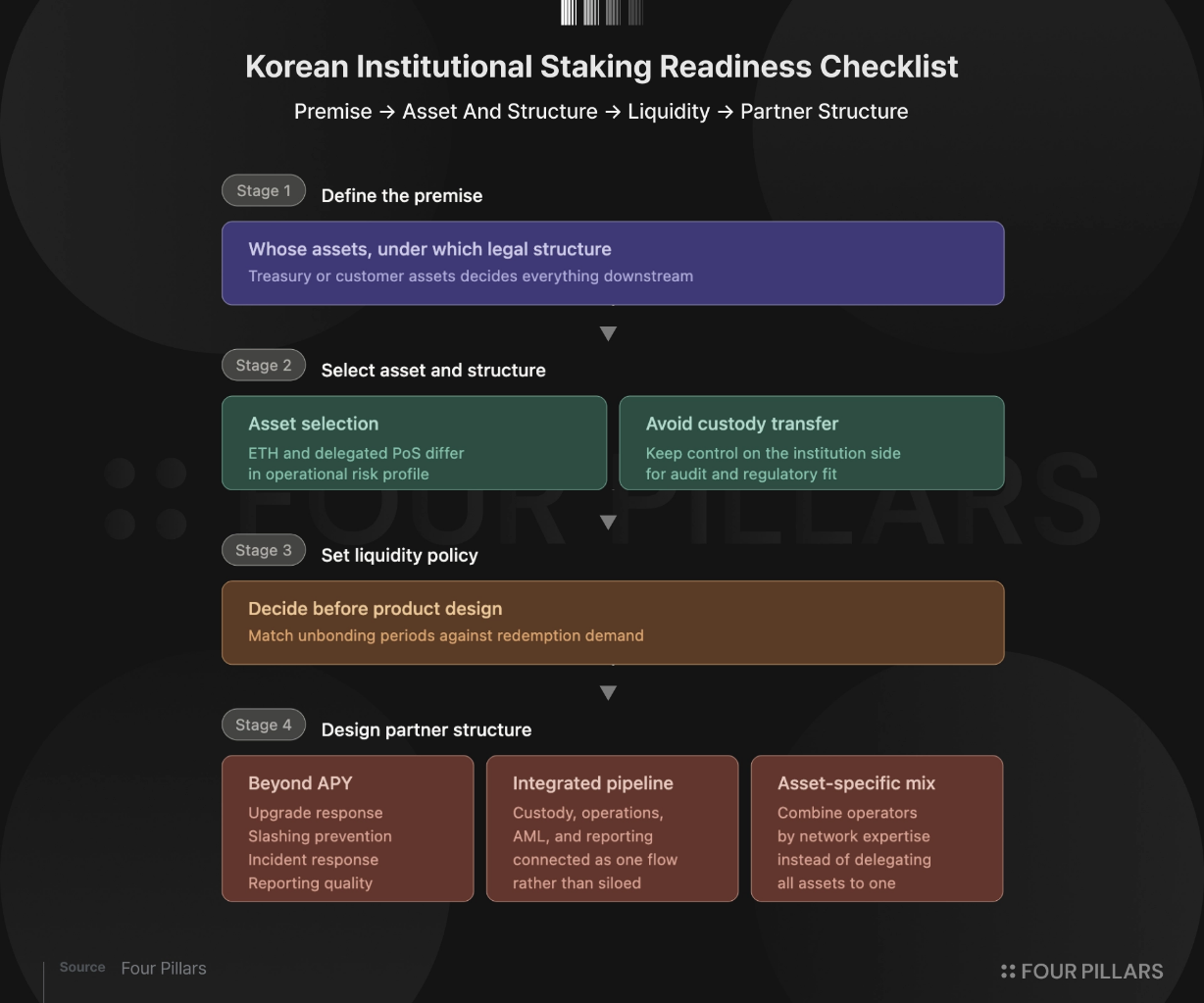

Given Korea's specifics and the differences across assets and structures above, here is what a Korean institution preparing for staking should check in practice.

- Decide whose assets, under what legal structure, will be staked. Treasury versus client assets changes the control structure and the partner set entirely.

- Treat asset selection as a question of operational difficulty and risk profile. Ethereum and the DPoS assets that support protocol-level delegation call for different pipeline designs from the start.

- A structure where custody moves is hard to justify under Korean regulation. Design on the assumption that control of the asset stays on the institution's side.

- Set the liquidity policy. How the unstaking window lines up with redemption and withdrawal demand has to be decided before the product is designed.

- Do not evaluate validators on APY alone. What matters more is the communication channel to the blockchain's foundation and core developers, response capacity for protocol upgrades, the slashing-defense setup, reporting and audit response, the incident response process, and the operator's ability to communicate with institutions.

- Design the whole partner structure, not the single player. Custody, validator operation, AML, and accounting reporting have to connect into one flow before the pipeline is institutional-grade.

- Validator operation itself can be split across specialists by asset. In a multi-asset portfolio, handing every asset to one operator is not obviously the best call. Composing operators by asset-specific track record and network expertise is often the better choice.

3.6 The Realistic Starting Point Is a Collaborative Structure

Completing an institutional staking pipeline in Korea takes two capabilities at once. One is a compliance framework that fits Korean financial regulation, paired with experience running institutional capital. The other is hands-on blockchain infrastructure experience: validators at scale, protocol-level risk management, governance participation.

The two capabilities come from different businesses. Traditional finance has depth in regulatory response and institutional capital operation. Crypto-native firms have depth in large-scale validator operation and protocol risk management. The know-how built inside one side cannot be replicated inside the other in a short window. So the pipeline is built naturally not as one provider doing everything, but as a combination of specialists each holding their own layer.

The realistic path for institutional staking in Korea is a division of labor between the two camps. Custody and regulatory response on the financial infrastructure side. Validator operation and on-chain risk management on the crypto-native side. That is the cooperative structure that can run first. The opening of the corporate market and the enactment of the Digital Asset Basic Act are laying the institutional groundwork for that cooperation. Whether the pipeline is operational on the day the market actually opens is what will decide who captures the early Korean institutional staking market.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![License Is All You Need [FP Weekly 27]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Ft4v9kemqys40d1.png&w=1920&q=75)

![MSTR and COIN [FP Weekly 26]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F6ivhjsmqq8e3w1.png&w=1920&q=75)