Table of Contents

- Key Takeaways

- 1. Overview: Korean Institutional Capital, Locked Out of a $120B Market

- 2. Global Trends: What the $120B Experiment Proved

- 2.1 Distribution Wins

- 2.2 Custody

- 2.3 Staking

- 2.4 Crypto ETFs in Asia

- 3. Opportunities in the Korean Market: The Infrastructure Race Has Already Begun

- 3.1 Capital Moves Before the Law

- 3.2 What Determines the Winner

Researcher

Key Takeaways

- The product-market fit for spot crypto ETFs has already been proven in the U.S., where Bitcoin ETFs rapidly accumulated large AUM and even surpassed gold ETFs at their peak.

- In Korea, the core value of crypto ETFs is not retail access, since retail investors already use exchanges, but unlocking structurally constrained capital such as pensions, ISA accounts, insurance general accounts, and institutional portfolios.

- The U.S. ETF market shows that distribution is more important than first-mover advantage or low fees; BlackRock’s IBIT won because of brokerage availability, institutional model portfolio inclusion, brand trust, and liquidity flywheel effects.

- Korea can design a structurally stronger custody model than the U.S. by using multiple qualified custodians from the start instead of relying on a single dominant custodian.

- Korean financial institutions are already moving ahead of regulation through exchange acquisitions, custody buildouts, and infrastructure partnerships, and the eventual winners will likely be those that already control distribution, custody, AP capabilities, and index infrastructure when regulation opens.

This article is adapted from "Korean Blockchain Guidebook for Institutions 2026," jointly published by Four Pillars and Pantera Capital. The full report covers 14 more themes for companies and institutional investors.

1. Overview: Korean Institutional Capital, Locked Out of a $120B Market

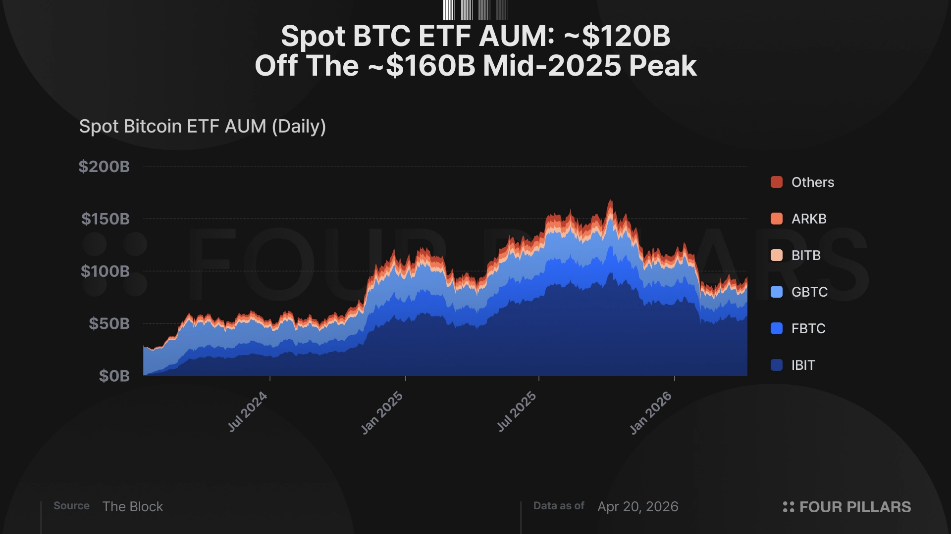

Crypto ETFs are no longer an experiment. The US spot Bitcoin ETF market sits at roughly $120B in AUM as of March 2026, down from a peak of $160B when Bitcoin traded above $118K. Cumulative net inflows since the January 2024 launch total $53B. BlackRock’s IBIT alone holds $54.76B and hit $80B in 374 days, the fastest any ETF has reached that milestone across all asset classes. By December 2024, US Bitcoin ETF AUM had surpassed gold ETF AUM for the first time, $129.3B versus $128.9B. Whatever position you hold on Bitcoin as an asset, the product-market fit of the wrapper is settled.

Korean institutional investors have no way to participate. NPS holds 614,409 shares of MicroStrategy worth approximately $79.1M, which sounds like a position until you measure it against NPS’s total AUM of ₩1,500T. That’s 0.005% of the book. It’s not a crypto allocation. It’s a rounding error produced by MicroStrategy’s inclusion in MSCI indices that NPS tracks passively. NPS has never made a deliberate decision to allocate capital to crypto. Its governance structure doesn't have a framework to evaluate one yet.

Korea has over 16 million crypto accounts, roughly 31% of the population. Those users already have access through Upbit and Bithumb. The ETF conversation is not about giving retail new access. It’s about unlocking the structural capital that cannot touch exchange-bought crypto: pension fund mandates, ISA wrappers, insurance general accounts. This is the same structural barrier that prevented US 401(k)s and IRAs from holding Coinbase-bought Bitcoin before the ETF launched. Korea’s ETF market sits at ₩300-400T ($208-267B). If crypto ETFs are approved, they plug directly into this existing infrastructure on day one.

Crypto investors represent roughly 36% of Korean voters. President Lee Jae-myung campaigned on permitting spot crypto ETFs, NPS direct investment, and a KRW-denominated stablecoin. The political will exists. What’s blocking movement is jurisdictional disputes and legislative technicalities, not opposition to the direction itself.

2. Global Trends: What the $120B Experiment Proved

2.1 Distribution Wins

The US’s two-year experiment carries lessons that transfer directly to Korea, and the most important one is that distribution beats everything.

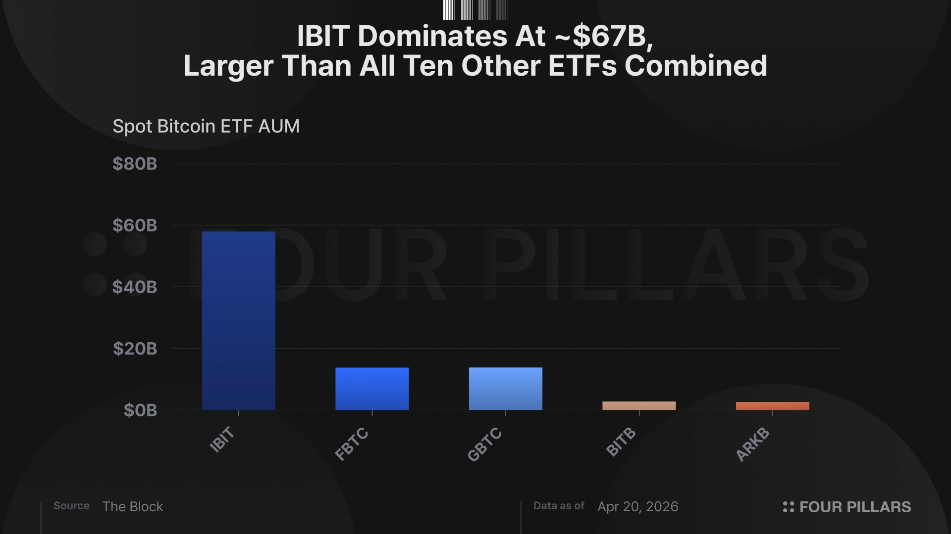

The US launched 11 spot Bitcoin ETFs simultaneously in January 2024. Eighteen months later, the top three (IBIT, FBTC, GBTC) hold 80%+ of total AUM, and IBIT alone commands over 50% market share. The ETF with the lowest fees did not succeed. Both BITB (0.20%) and ARKB (0.21%) had lower fees than IBIT’s 0.25%, but failed to attract capital inflows. What IBIT had was availability on every US brokerage platform, inclusion in institutional model portfolios, and a liquidity flywheel where tightest spreads attracted the most volume, which tightened spreads further.

The Grayscale lesson matters most for this audience. Grayscale operated Bitcoin investment products since 2013, a decade-long head start. After the ETF conversion, they maintained a 1.50% fee while competitors charged 0.20-0.25%, and the result was $21B+ in outflows. BlackRock filed in June 2023, launched in January 2024, and achieved market dominance in under twelve months. First-mover advantage without distribution infrastructure is worthless, which means the implication for Korea is that the “first to launch a crypto ETF” does not win. “Broadest brokerage distribution, pension access, and brand trust” wins.

On the fee side, Morgan Stanley’s MSBT launched April 8, 2026 at 0.14% and pulled $34M on day one as the first bank-affiliated spot Bitcoin ETF. This sets the floor. Korea’s ETF fee culture is even more compressed than the US, where domestic equity ETF averages sit below 20 basis points. At $30B in AUM and 18bps, the entire market generates roughly $54M per year in fees. Split among two or three managers, that’s $18-27M per firm, a rounding error on a large asset manager’s P&L.

The ETF is not a standalone business. It’s a platform entry point, with custody, prime brokerage, staking yield distribution, OTC execution, structured products, and derivatives all sitting on top. The full-stack revenue opportunity is 5-10x the management fee alone, which is why the M&A we’re seeing in Korea isn’t about ETF fees.

2.2 Custody

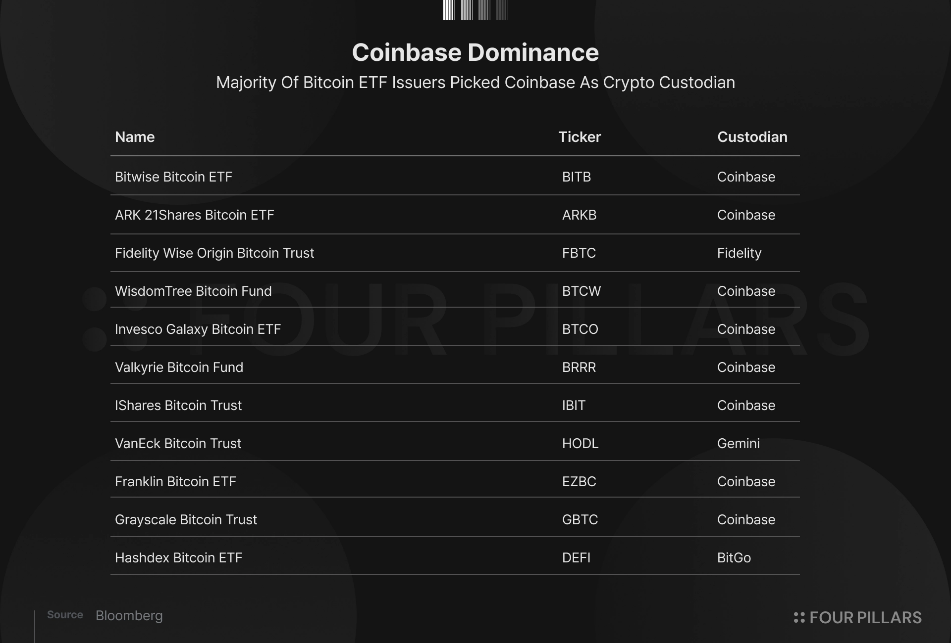

On custody, Coinbase holds over 80% of US spot Bitcoin ETF AUM. Eight of eleven ETFs use Coinbase as custodian, meaning approximately 1.5 million BTC sits with a single institution, roughly 7% of Bitcoin’s maximum supply. Only Fidelity self-custodies through Fidelity Digital Assets. A security incident, regulatory action, or operational failure at Coinbase simultaneously impacts the entire US ETF market. Korea’s multi-custodian starting point, with KODA (KB), BitGo Korea (Hana), and Korbit (Mirae Asset), is structurally superior, and Korea can design multi-custodian architecture from the outset rather than inheriting concentration by default.

2.3 Staking

Staking adds another lesson. BlackRock's ETHB listed on Nasdaq in March 2026, staking 70-95% of held ETH with a liquidity sleeve of 5-30% reserved for redemptions. Gross staking yield runs approximately 3.1% annualized, netting 1.9-2.2% after validator costs and the manager's share. Bitwise's BSOL launched in October 2025 staking 100% of held SOL at 6-7% annual yield and pulled $500M in AUM within weeks, capturing 89% of initial category inflows. The risks are real: staking yield is protocol issuance, not interest, denominated in native tokens rather than KRW, and unstaking queues create a liquidity mismatch against T+2 redemption windows. Tax treatment of staking yield in Korea is also undefined. But the product design question for Korean asset managers is whether to launch with or without a staking sleeve, not whether staking exists.

2.4 Crypto ETFs in Asia

What about markets outside the US? Hong Kong proves regulatory approval alone is insufficient. Hong Kong launched spot Bitcoin and Ethereum ETFs in April 2024 with three issuers, and pre-launch projections called for $25B in inflows. Actual AUM settled around $300M, 1.2% of expectations, with first-day trading volume of $11M. Mainland Chinese investors were blocked from access, Hong Kong's institutional investor base is narrow relative to the US, and no distribution infrastructure existed equivalent to hundreds of millions of US retirement accounts automatically eligible for allocation. Korea differs structurally (the $110B annual offshore outflow proves existing demand, the ₩300-400T ETF market provides ready infrastructure, and 16M existing crypto account holders represent a proven user base), but the Hong Kong lesson holds: regulatory approval without distribution channels, tax incentives, and institutional investment guidelines generates headlines, not AUM.

Japan adds context on where the region is heading. Japan's FSA is reclassifying roughly 105 major crypto assets as "financial products" in 2026, cutting the tax rate from miscellaneous income at a maximum 55% to separated taxation at 20%. The target timeline for spot crypto ETFs is 2028, and six major asset managers including Daiwa, Mitsubishi UFJ, and Asset Management One are already reviewing crypto product lineups. Korea has historically led Japan on crypto adoption (31% of the population holds crypto accounts versus Japan's single digits), but the pace of institutional framework development remains uncertain.

3. Opportunities in the Korean Market: The Infrastructure Race Has Already Begun

3.1 Capital Moves Before the Law

Korea's regulatory timeline cannot be promised. The Digital Asset Basic Act (DABA) is effectively deadlocked as of April 2026, stuck on three unresolved issues: exchange ownership caps, where individual 20% and corporate 34% consensus is forming but all five major exchanges already exceed these thresholds (Dunamu CEO at 25.53%, Bithumb Holdings at 73.56%, Mirae Asset's Korbit stake at 92%); stablecoin issuance authority, where the Bank of Korea insists on mandatory 51%+ bank equity participation while the FSC opposes; and foreign stablecoin regulation requiring offshore issuers like Circle to establish Korean subsidiaries. As one industry insider told Seoul Economic Daily, "even passage within this year looks uncertain, and factoring in enforcement decrees, we may have to wait until the following year."

None of this has stopped the infrastructure race. Korean financial firms are building as if approval is a question of when, not if, and the M&A map is filling fast. Mirae Asset acquired 92.06% of Korbit for ₩133.5B from NXC and SK Square in February 2026, integrating exchange, custody, and market-making capabilities under its "Mirae Asset 3.0" strategy against $418B in global AUM. Naver Financial announced a stock swap merger with Dunamu at approximately $10.3B enterprise value in November 2025, combining Naver Pay's 34 million users with Upbit's 8 million active traders, though the shareholder meeting has been delayed to August 2026 pending DABA uncertainty. Korea Investment & Securities is reviewing a stake in Coinone as of April 2026, reportedly targeting around 20%.

On the custody side, KB Financial has operated KODA since 2021 as Korea's first bank-affiliated crypto custodian, and Hana Financial runs a BitGo Korea joint venture with SK Telecom. Shinhan Financial is building an internal digital asset team. Binance re-entered the Korean market through its 67% Gopax acquisition, receiving FIU approval in October 2025.

The value chain analysis reveals where the gaps remain. Korea's ETF issuance capability exists through firms like Mirae Asset, Samsung Asset Management, and KB Asset Management, but regulatory approval is the bottleneck. KRX Chairman Jung Eun-bo has stated publicly that "market infrastructure is built and ready for crypto-linked ETF listing and trading," though listing requires a Capital Markets Act amendment classifying crypto as an eligible ETF underlying asset. The custodial layer is under construction but lacks ETF-grade licensing pending DABA passage.

Two gaps are genuinely unfilled. Korea has no institutional-grade authorized participant with both KRX membership and crypto settlement capabilities — in-kind creation requires APs to directly hold and transfer crypto assets, and no institution currently bridges both worlds. KIS's potential Coinone acquisition is expected to fill this gap. And there is no domestic crypto price index provider: the US relies on CF Benchmarks and CME for benchmark pricing, but Korea needs a transparent, auditable methodology volume-weighted across Upbit, Bithumb, and other domestic exchanges. Either KRX builds this internally or licenses externally.

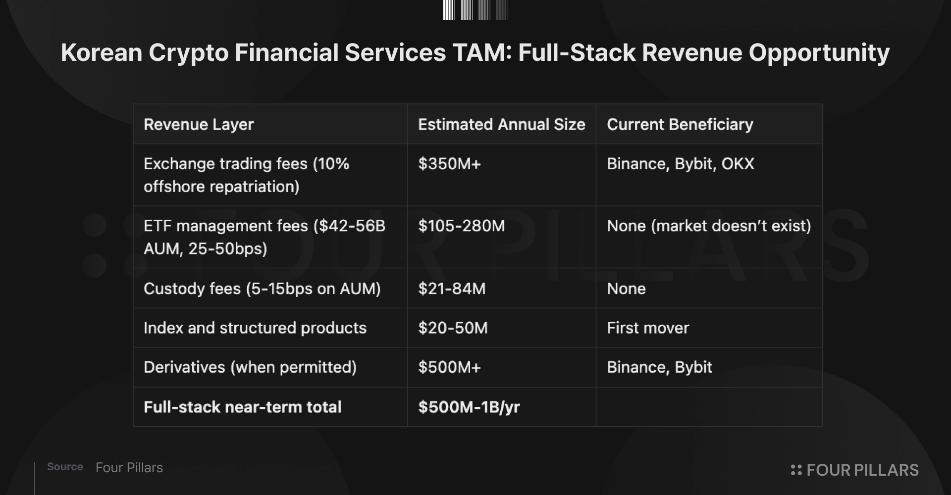

3.2 What Determines the Winner

The near-term revenue opportunity, sized from the bottom up:

Methodology: Exchange fee repatriation based on estimated Korean capital currently flowing to offshore exchanges, assuming 10% onshoring. ETF and custody fee ranges use projected Korean crypto ETF AUM of $42-56B at industry-standard fee rates (25-50bps management, 5-15bps custody), benchmarked against Korea's existing ₩300-400T ETF market. Derivatives sized against current offshore Korean derivatives volume. All figures are illustrative estimates, not forecasts.

The case for waiting: DABA passage timing is genuinely uncertain, early infrastructure investment carries real cost, and Samsung Asset Management could conceivably enter late and win on distribution alone as Korea’s number-one ETF manager by market share.

The case against: in a winner-take-most market, first movers lock in the liquidity-spreads-volume flywheel that late entrants never overcome. In the US, Franklin Templeton, WisdomTree, and Invesco combined hold less than 10% market share and are permanent minorities. Acquirable exchanges are running out (Korbit belongs to Mirae Asset, Coinone is in play, Upbit costs $10.3B, Gopax belongs to Binance), and there is no guarantee the same targets exist in 2027.

We believe the variable that resolves this is distribution infrastructure, not regulatory timing. The firms that will own this market are not the ones that file first after DABA passes. They’re the ones already holding the brokerage relationships, the custody stack, and the AP capabilities when the law changes.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![License Is All You Need [FP Weekly 27]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Ft4v9kemqys40d1.png&w=1920&q=75)

![MSTR and COIN [FP Weekly 26]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F6ivhjsmqq8e3w1.png&w=1920&q=75)