Table of Contents

Researcher

Peter Drucker, often referred to as the father of modern management, once said:

“The best way to predict the future is to create it.”

If one can turn an imagined future into reality through one’s own efforts, there may be no more certain form of prediction. In prediction markets, however, this statement takes on an entirely different meaning. If participants can alter an outcome through their own actions, a market that puts capital behind possible futures can become a market that actively creates those futures.

Recently, cases have emerged in which prediction markets appear to go beyond aggregating information to forecast the future, with participants potentially attempting to influence the settlement outcome itself. This article examines such cases to explore the structural vulnerabilities of prediction markets and the dual nature of the technology behind them.

1. Polymarket’s 5-Minute BTC Contract

To assess the case, it is first necessary to understand how Polymarket’s five minute Bitcoin contracts are structured.

Each contract asks whether the Bitcoin price at the end of a five minute window will be above or below its price at the beginning of that window. Participants can trade on either outcome. An Up position pays $1 if the settlement price finishes above the opening price and $0 otherwise. The contract therefore functions as a binary claim whose value depends entirely on the direction of Bitcoin’s price over a short and fixed period.

This structure creates a sharp settlement threshold. The contract is not primarily designed to capture Bitcoin’s longer term price direction. Instead, it is determined by whether the final price is above or below a single reference point at a specific moment. When Bitcoin is trading close to its opening price near settlement, even a small movement can determine the outcome of the entire contract.

Polymarket settles these contracts using an external oracle rather than its own order book. This means that the final outcome depends on the price reported by the oracle at the settlement point. The structural concern arises when a trader holds a position in the prediction market while also participating in the underlying Bitcoin spot market. If activity in the spot market can influence the price reflected by the oracle, the trader may have an incentive to affect the settlement condition rather than simply forecast it.

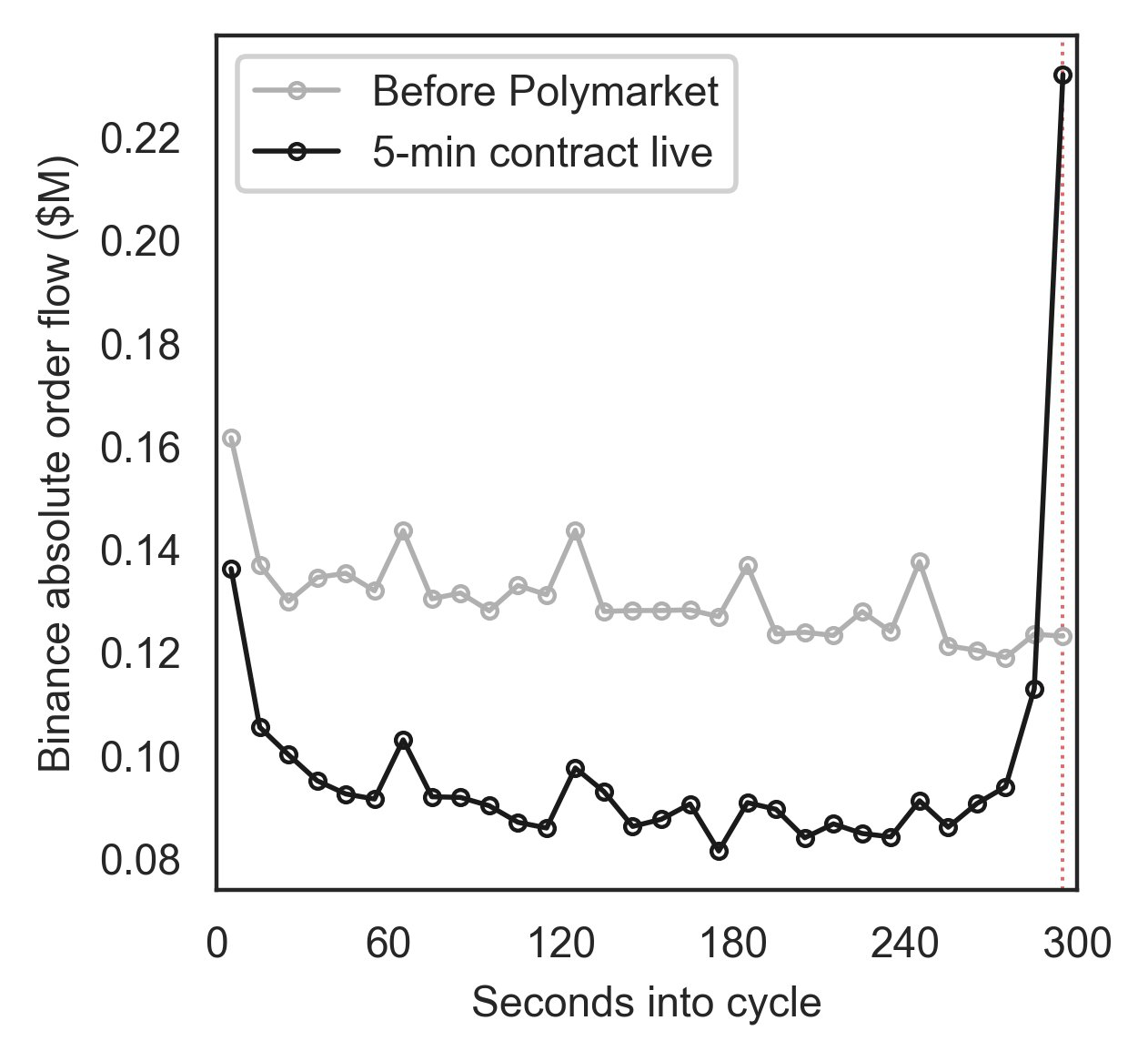

2. Signs of Manipulation During Settlement

Source: Settlement Manipulation in Prediction Markets

Recent research identifies a distinctive pattern following the launch of Polymarket’s five minute BTC contract. In the final seconds before settlement, Binance spot order flow increased sharply and prices often reversed shortly after the contract closed. A short lived price move does not, by itself, prove manipulation. However, it is less consistent with trading based on new information, whose effects would normally persist, and more consistent with trading activity concentrated around the settlement clock.

The paper proposes a simple mechanism. A trader may first take a position in an Up contract on Polymarket and then place spot market orders near the end of the settlement window. If the resulting price movement is reflected in the oracle price used for settlement, the Up contract may resolve in the trader’s favor. The same logic applies in the opposite direction for holders of Down contracts. The key issue is that the payoff from the prediction market position may be much larger than the cost of a temporary price movement in the underlying market.

The authors estimate that a small group of accounts captured approximately $8.2 million in profits during periods classified as potentially manipulated, while ordinary participants lost around $7.6 million. These figures should be interpreted with caution. The study does not directly observe an individual trader’s intent or legally establish manipulation. Instead, it presents an empirical case based on the timing of trades, post settlement price reversals, and the concentration of profits. Taken together, these patterns are strongly consistent with the hypothesis of settlement manipulation.

3. A Distorted Purpose: Is There a Solution?

Prediction markets are often valued for their ability to aggregate dispersed information and turn it into a collective view of the future.

However, this function becomes less reliable when market participants can influence the outcome they are trading on. Elections, sports, public opinion, public statements, and weather readings all present this risk. When traders are able to affect an outcome directly or indirectly, a market that is meant to answer “What is likely to happen?” can begin to reward those who ask, “How can this outcome be made to happen?”

Reducing this risk requires a more deliberate approach to market design.

First, markets that settle over extremely short time frames should be approached with caution. A five minute Bitcoin contract can be vulnerable to manipulation even when the underlying price information is otherwise useful. When settlement occurs within a narrow window, a small and temporary movement near the end of the contract may be enough to determine the result.

Longer duration contracts are not completely immune to manipulation. However, they are generally less exposed to short term intervention because the outcome reflects a broader period of price discovery. For this reason, prediction market platforms should establish clear minimum contract durations based on the characteristics of the market and the liquidity of the underlying asset.

Second, platforms need to reconsider what types of information are worth turning into markets. Polymarket and Kalshi gained attention because they were expected to reflect social and economic information more quickly than traditional media or opinion polls. In principle, markets on inflation, elections, or policy decisions can provide useful signals by aggregating the views of participants with different information.

However, some markets appear to be driven more by trading volume and attention than by informational value. For example, Polymarket hosted a market on whether Federal Reserve Chair Jerome Powell would say “Good Morning” during his Jackson Hole speech. The contract generated roughly $80,000 in trading volume, despite offering limited insight into monetary policy or the broader economic outlook.

If prediction markets are to justify themselves through their ability to produce socially useful information, platforms need clearer standards for what they list. Not every event or piece of information needs to become a tradable product. Blockchain and tokenization may make a wide range of assets and outcomes tradable, but technical possibility alone does not create social value.

Finally, oracle design needs to be treated as a core part of market integrity. Five minute Bitcoin contracts are settled using Chainlink price data. Chainlink states that its price feeds aggregate information from multiple exchanges and data providers. Yet public information does not make it easy to verify which exchanges are included in a given feed or how much weight each source carries.

The close relationship between Binance prices and Chainlink settlement prices raises an important question. It does not prove that Binance directly determines the settlement result. It does, however, make it difficult to assess how much influence a single exchange may have on the outcome and how diversified the oracle inputs are in practice.

In a prediction market, an oracle is not merely a technical data source. It determines which outcome wins and how funds are distributed. If users cannot evaluate the oracle’s methodology, source composition, and resistance to manipulation, the transparency and fairness of the market itself may be called into question.

4. Conclusion

Drucker’s idea that the best way to predict the future is to create it captures the value of innovation and execution. In prediction markets, however, the same idea can become problematic when participants are rewarded for influencing the outcome rather than forecasting it.

The issue is not whether prediction markets should exist. The more important questions are who can influence the outcome, how settlement is determined, and whether market design provides sufficient protection against manipulation.

Prediction markets should not be viewed through either blind optimism or blanket skepticism. Like any emerging technology, they need to be assessed through both their potential and their limitations. Their long term value will depend on whether platforms can preserve the role of markets as tools for information discovery rather than allowing them to become mechanisms for strategic intervention.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.