Table of Contents

- Key Takeaways

- 1. Why Are We in Crypto?

- 2. Korea Was a Mess

- 3. Korea Retail Trading Boomed

- 4. Korea Is Institutionalizing

- 4.1 The Foundation: Law Is Getting Clearer

- 4.2 The Digital Money: Stablecoin, and CBDC

- 4.3 The Financial Institutions and Conglomerates

- 5. Korea Is at the Turning Point

- Key Takeaways

- 1. Why Are We in Crypto?

- 2. Korea Was a Mess

- 3. Korea Retail Trading Boomed

- 4. Korea Is Institutionalizing

- 4.1 The Foundation: Law Is Getting Clearer

- 4.2 The Digital Money: Stablecoin, and CBDC

- 4.3 The Financial Institutions and Conglomerates

- 5. Korea Is at the Turning Point

Researcher

Key Takeaways

- Korea's fast-moving, speed-driven culture made it an early crypto hotbed, producing the 2017 kimchi premium, the 2021 NFT mania, and the painful 2022 Terra/Luna collapse before the market began to mature.

- Retail trading rebounded powerfully to roughly $77.5B in H2 2024 with close to 20% of the population invested, though liquidity has recently rotated toward a booming equities market.

- The market is now institutionalizing as clearer laws recognize tokenized securities, the Bank of Korea's CBDC pilot and private won stablecoins move toward coexistence, and major banks and platforms race to build the payments stack.

- Korea has long been restless and risk-seeking, always looking toward whatever comes next. That same restlessness once produced chaos in its crypto market, and now it is producing structure.

EastPoint:Seoul is the first private conference to bring together institutional leaders, regulators, and Web3 pioneers to shape the future of digital assets and the AI economy in Korea.

1. Why Are We in Crypto?

Everyone arrives in crypto for a different reason, and those reasons rarely fit into a single story. Some people are chasing a technology they believe in, while others are simply looking for the next way to grow their savings. The honest truth is that most of us hold several of these motivations at the same time.

A few of the most common reasons tend to sound like this:

- I want access to infrastructure that resists state censorship.

- I do not want my entire life savings sitting inside a single bank or brokerage.

- I enjoy a culture where I can connect and build a community with people all over the world.

- I believe crypto will become the financial backbone of the next generation.

- I want to make money.

These motivations overlap far more than they conflict, and that overlap is what gives the industry its energy. Because opinions are shared, praised, and torn apart in the open, ideas evolve at a speed that traditional finance rarely matches.

That same radical transparency is also why the space stays perpetually crowded with scams, genuine innovation, and competing visions of where it should go next.

No market has lived out that mix of mania and reinvention more vividly than Korea, which is where this story begins.

2. Korea Was a Mess

Korea is a famously fast moving country. It grew from postwar poverty into an advanced economy in barely two generations, and that experience taught an entire society that speed equals survival.

That catch up reflex never switched off, and the surrounding infrastructure keeps reinforcing it every single day. The fastest internet in the world, shops and services that run around the clock, and delivery that arrives within hours all train people to expect things instantly. A national temperament like this rewards those who act first and ask questions later.

Crypto slots into that mindset almost perfectly. It offers fascinating novel tech, a constant stream of narratives to follow, and the promise of fast money for anyone willing to move early. There was a strog synergy between the culture and the crypto asset class.

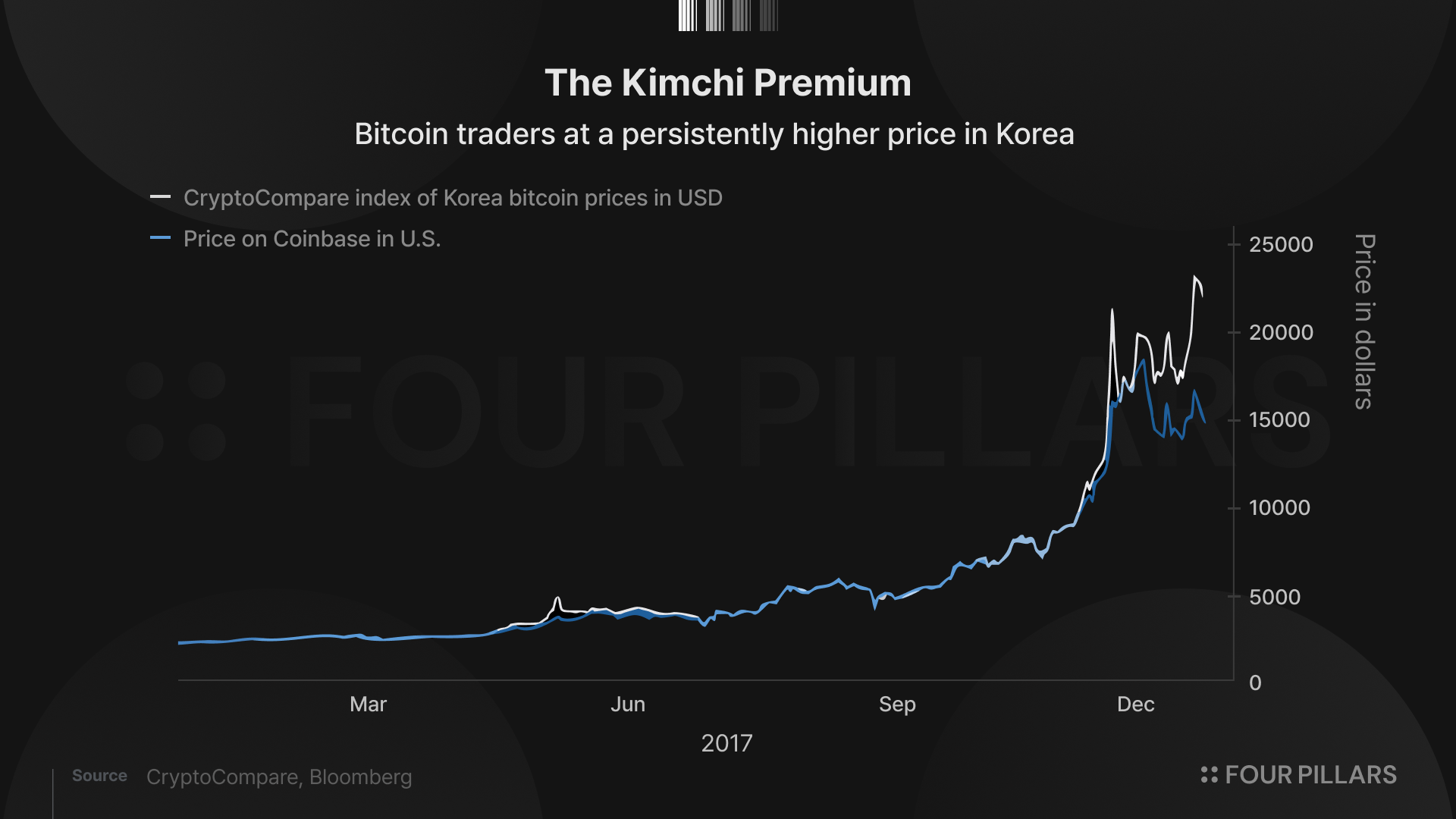

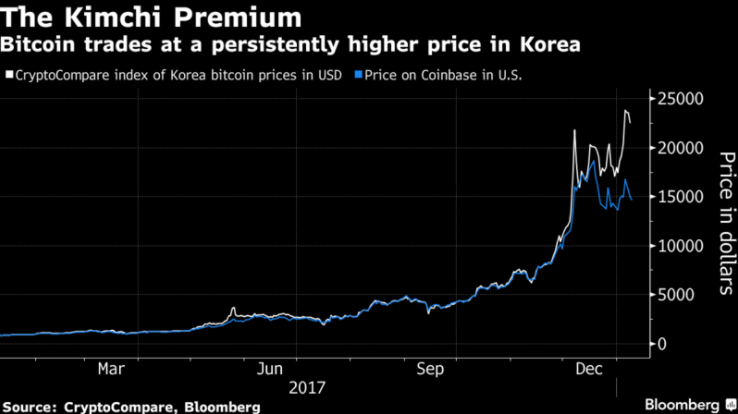

That synergy showed up early. By late 2017 the frenzy was so intense that bitcoin traded at a "kimchi premium" above 50% over global prices, a gap that existed simply because local demand outran what exchanges could supply (Also, the isolation of exchange was a cause).

Source: Bitcoin's kimchi premium is no free lunch

The next wave in Korea was the retail NFT mania of 2021, much of it built on Klaytn. Capital rushed into locally branded collections that had little utility to back them up. Because the market was so domestic and speculative, its decline ran even deeper than the global NFT crash.

Then came the reckoning, and Korea sat at the center of it. In May 2022 Terra and Luna, the ecosystem built by Korean founder Do Kwon, collapsed and erased roughly $40 billion in a single week. The contagion spread quickly, and by November 2022 FTX had failed too, part of a rout that wiped some $2 trillion off the global market from its 2021 peak.

The years from 2022 to 2023 became some of the darkest the local market had ever seen. Confidence collapsed, projects folded, and little beyond speculative trading was left. It was the kind of reset that forces an industry to rethink its foundations.

3. Korea Retail Trading Boomed

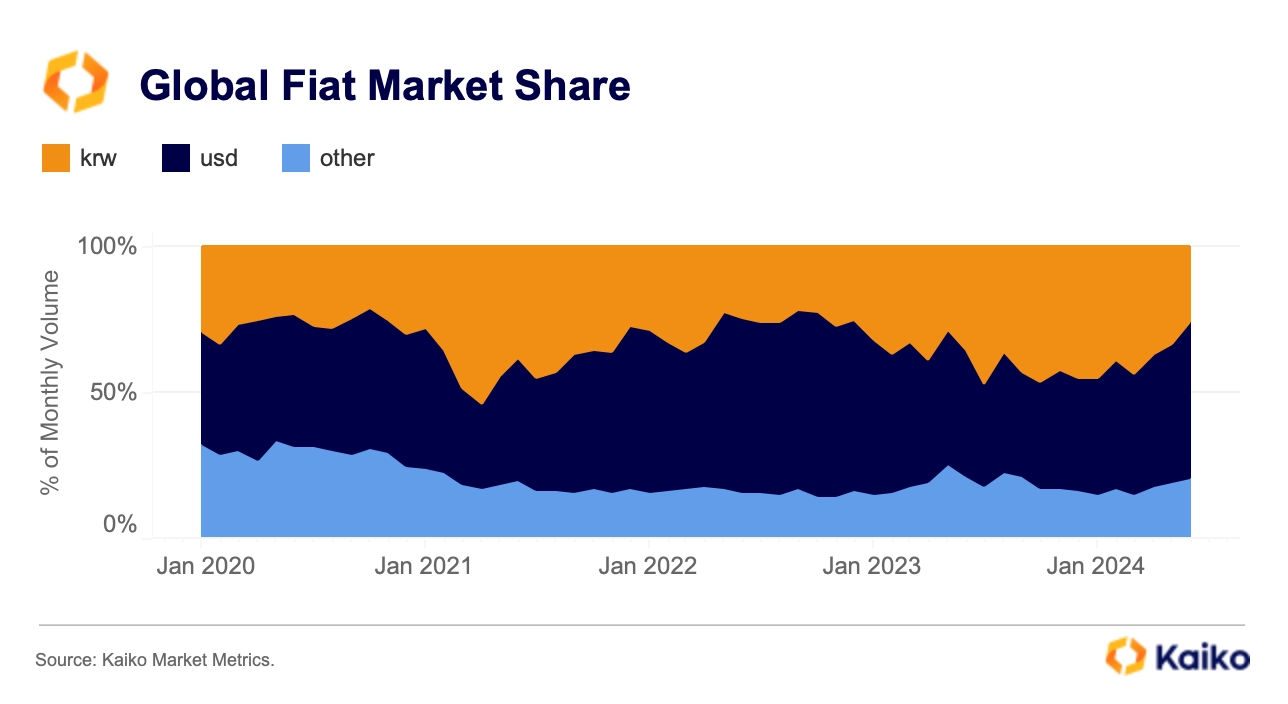

Source: The State of the Korean Crypto Market - Kaiko

However, as the market got better, Koreans came back to trade. If tokens have found genuine product market fit anywhere, it is in Korea, where retail traders have embraced digital assets with an intensity that few other markets can match.

What makes the Korean retail crowd distinctive is its comfort with volatility rather than its fear of it. These traders actively seek out sharp price swings, and they happily venture deep into long tail tokens that more conservative markets ignore.

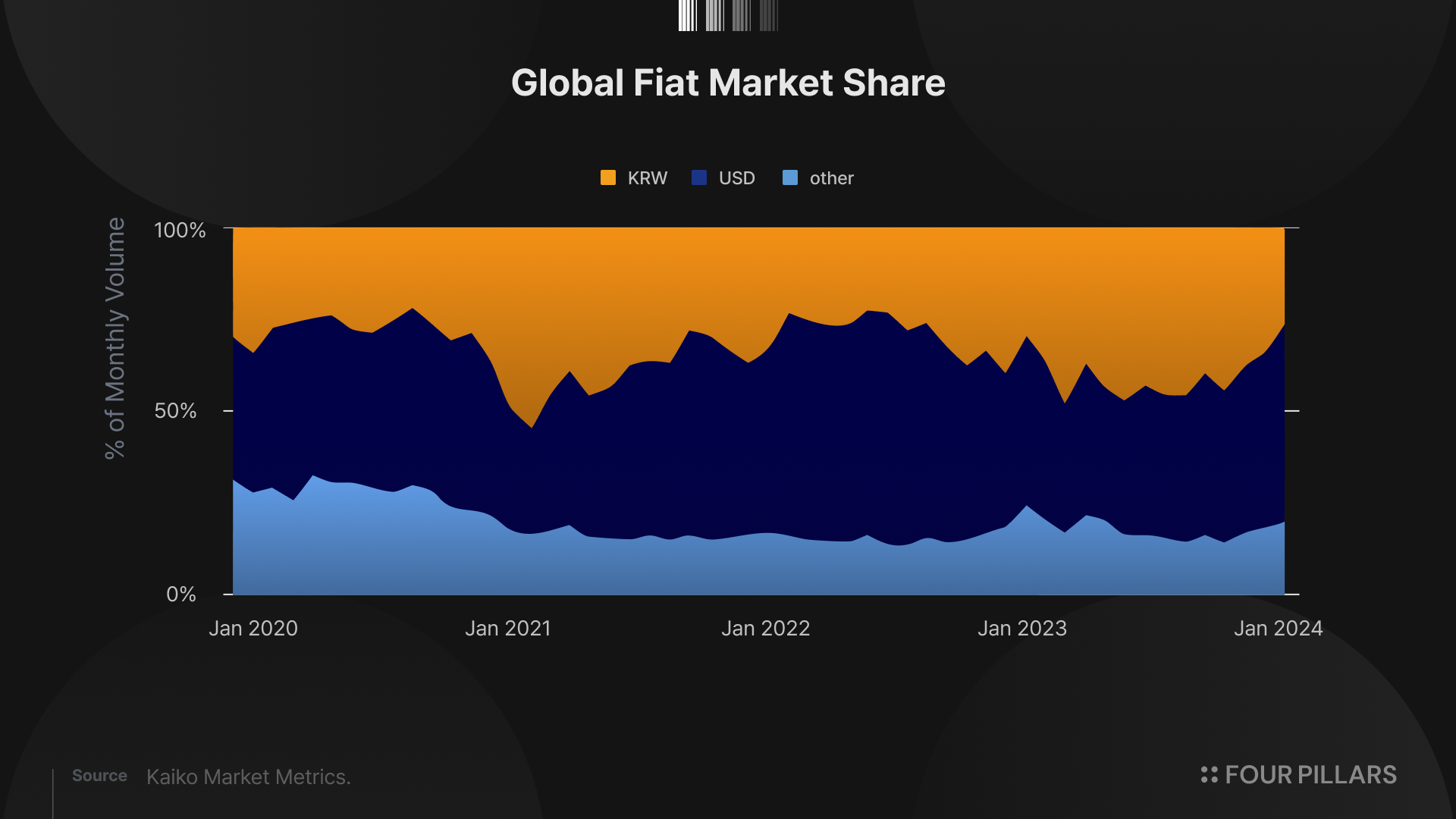

The appetite is strong enough to sustain a structural kimchi premium of roughly 2% to 3%, the persistent gap between local and global prices. That behavior turns Korea into a region where new tokens can find liquidity and attention almost overnight. Korea's crypto market roughly doubled to about ₩108 trillion, or $77.5 billion in the second half of 2024, with close to 20% of the population trading and the investor base past 16.2 million, outpacing the stock investors in 2025.

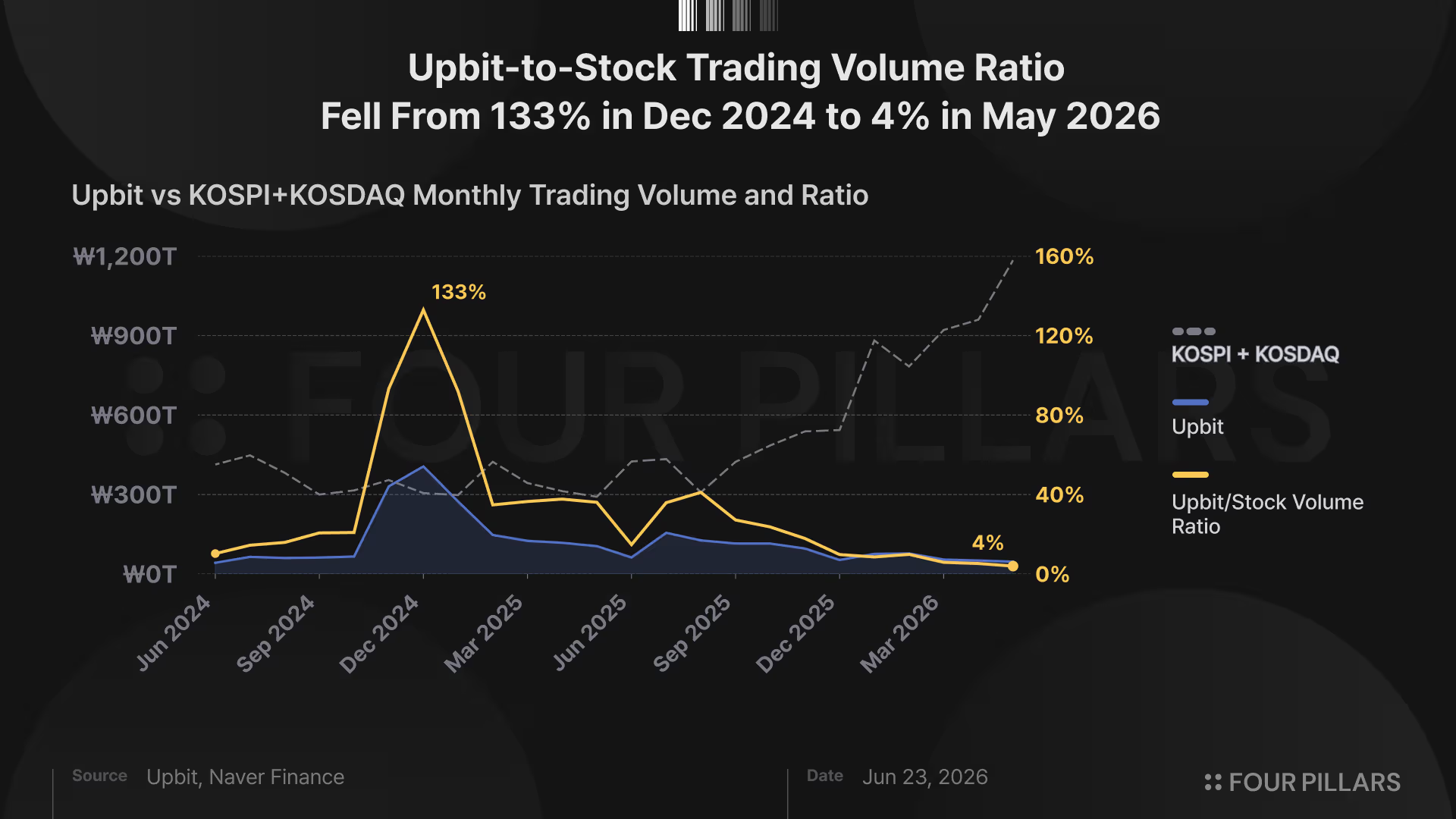

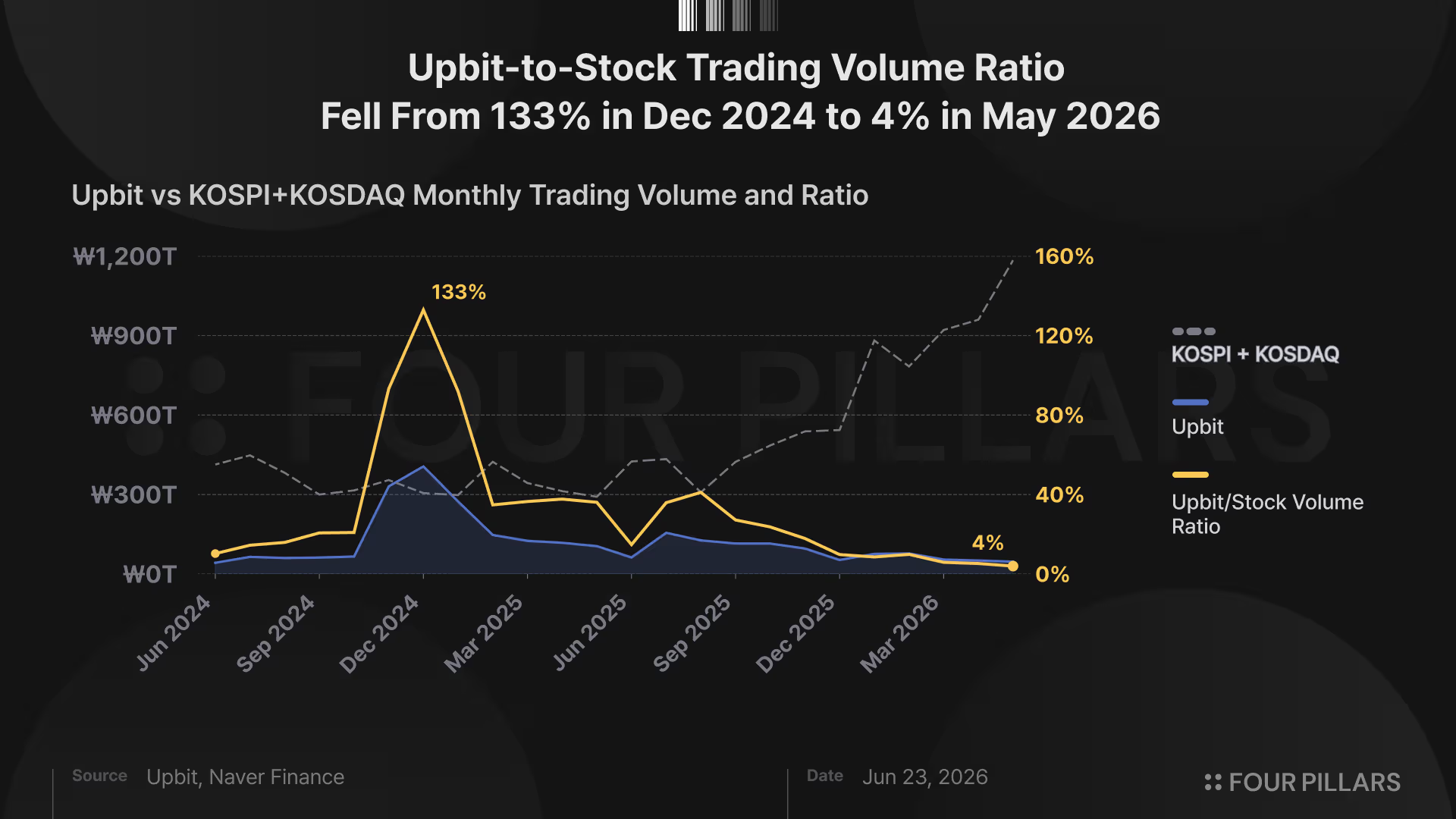

Lately, though, that appetite has rotated toward equities. The KOSPI rose 76% in 2025 to finish as the world's best-performing major market, individual investors' net buying jumped 54% over the prior year, and an AI and semiconductor supercycle added roughly $1.7 trillion in market value. Retail liquidity chasing the next big move simply found a louder story in chip stocks.

This is just a short-term rotation to more volatile investment. The volume has moved, but the building has not stopped, now the focus has shifted from retail screens to institutional strategies.

Source: Korean Exchanges Facing a Volume Plunge. Is It Really a Crisis? | FP RESEARCH

4. Korea Is Institutionalizing

The next chapter of Korean crypto is being written by institutions rather than retail, and that is the real shift in the background. Over the past eighteen months Korea has produced more concrete digital asset policy than in the previous eight years combined, and capital is moving into place behind the rules.

Three forces are converging at once: a legal foundation that finally recognizes tokenized assets, a discussion over digital money between private stablecoins and CBDC by Bank of Korea, and a land grab among platforms and conglomerates for the payments stack.

Now, The market is being institutionalized.

4.1 The Foundation: Law Is Getting Clearer

On January 15, 2026, the National Assembly passed amendments to both the Capital Markets Act and the Electronic Securities Act, the twin laws that together recognize tokenized securities.

They run on two distinct legal tracks and take effect in early 2027 after a one-year grace period: the Electronic Securities Act lets eligible issuers create tokenized securities on blockchain rails, while the Capital Markets Act lets those tokens trade as investment contract securities through licensed brokerages. The practical effect is a regulated on-ramp for bonds, real estate, and unlisted shares to move on-chain.

The Digital Asset Basic Act one of the most important and comprehensive pieces of legislation remains under discussion. If passed, it would reauthorize domestic ICOs for the first time since the 2017 ban and require stablecoin issuers to hold reserves of at least 100% of tokens in circulation. The draft also layers in FSC prior authorization, paid-in capital of at least KRW 1 billion, and bankruptcy-remote reserves so a failed issuer cannot drag down its bank.

The holdup has been due to lack of coordination, and have become a political issue. However, it is expected to pass within a year.

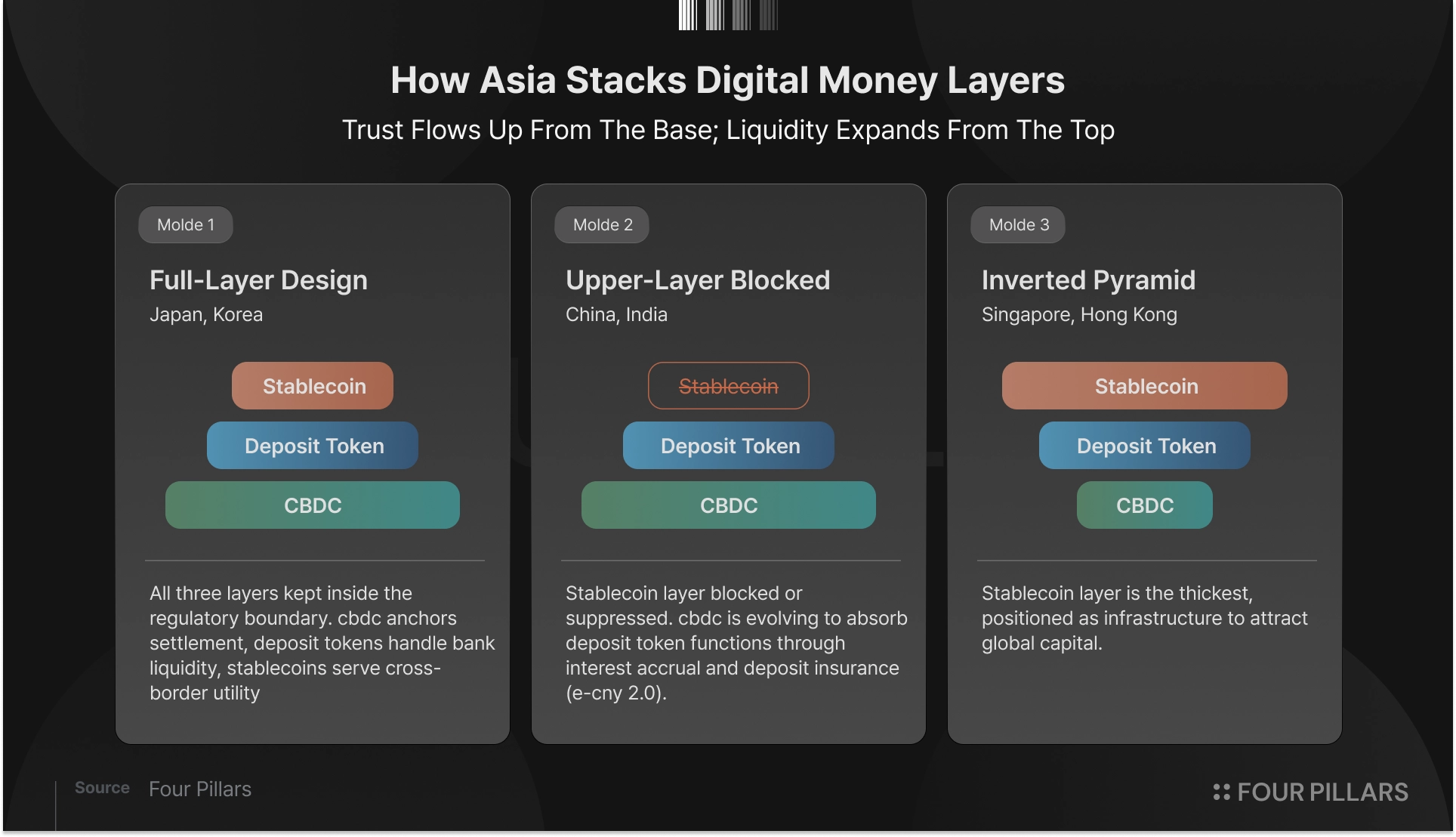

4.2 The Digital Money: Stablecoin, and CBDC

The bigger question is not who issues a won stablecoin first. Korea's payment rails are already well built, with cash down to just 15.9% of in-person transactions in 2024, so the real prize is not cheaper or faster payments but programmable, agentic commerce, money that software can hold and move on its own.

That logic is reshaping how the state-led option fits in, not pushing it aside. The Bank of Korea is pushing the Project Han River, its CBDC pilot, as the seven participating banks weighed the cost, a combined ₩35 billion($23 million) transaction was processed. Rather than retreat, the project returned with a concrete use case: routing government grant disbursements worth ₩110 trillion, or roughly $73 billion a year, over tokenized deposits.

The direction would be convergence rather than competition. CBDC and private stablecoins are being discussed to co-exist, and that dual-track approach is now one of the major movements in Korean digital money.

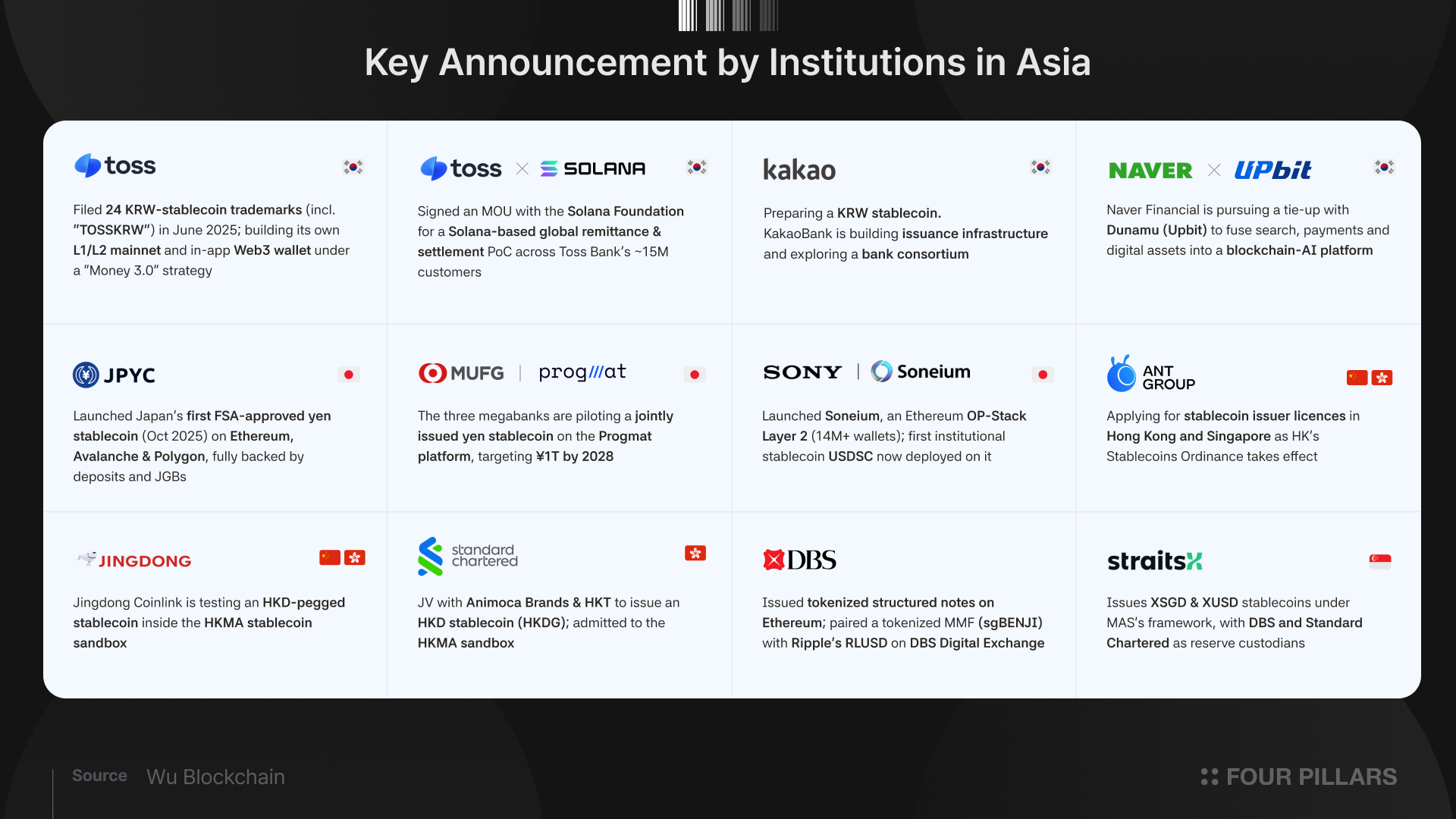

Private issuers are still working out where they fit within the regulatory framework. Most are still in testing like KRW1, launched by custodian BDACS with Woori Bank on Avalanche in September 2025, with each token backed 1:1 by won held in escrow, and a second deployment now testing on Circle's Arc network. For now, it remains a proof of concept rather than a product, with a market cap of around $97,000 and only a handful of holders a useful reminder that the rails are real, but the volume is not (yet).

Banks are coordinating. Korea's largest commercial banks, including KB Kookmin, Shinhan, Woori, NongHyup, IBK, Suhyup, Citi Korea and Standard Chartered Korea, with Hana the latest to join, are building a won stablecoin on shared infrastructure, each filing its own trademarks for separate tokens on a common rail. President Lee Jae-myung has gone further, naming a won stablecoin a national priority and citing $115 billion of 2025 capital flight out of Korean exchanges as the reason.

When rivals this size choose to cooperate rather than compete, the intent is hard to mistake.

4.3 The Financial Institutions and Conglomerates

If the traditional banks go for the cooperation path, the platforms represent a race. Dunamu, Kakao, Kaia, and Samsung are each chasing a different layer of the stack, issuance, settlement, and distribution, and increasingly the same players are colliding.

Dunamu, which runs the Upbit exchange, has launched GIWA, an Ethereum Layer 2 built on the OP Stack with no native token and uses ETH for gas. It is a direct bet on becoming the settlement rail for won and global stablecoins, and a way to loosen Dunamu's near-total reliance on trading fees.

On the issuance side, KakaoBank has moved its won stablecoin from trademarks into active development, filing twelve marks such as BKRW and KRWKKB and leaning on KakaoTalk's reach of nearly 49 million users for distribution. The lines are already blurring: Naver, is in discussion to acquire Dunamu, a deal that would fold issuance, settlement, and a consumer wallet under one roof.

5. Korea Is at the Turning Point

Regulation is still unsettled, and overall sentiment toward crypto remains cautious. With policy caught in political debate, institutions still lack the clarity they need to move decisively.

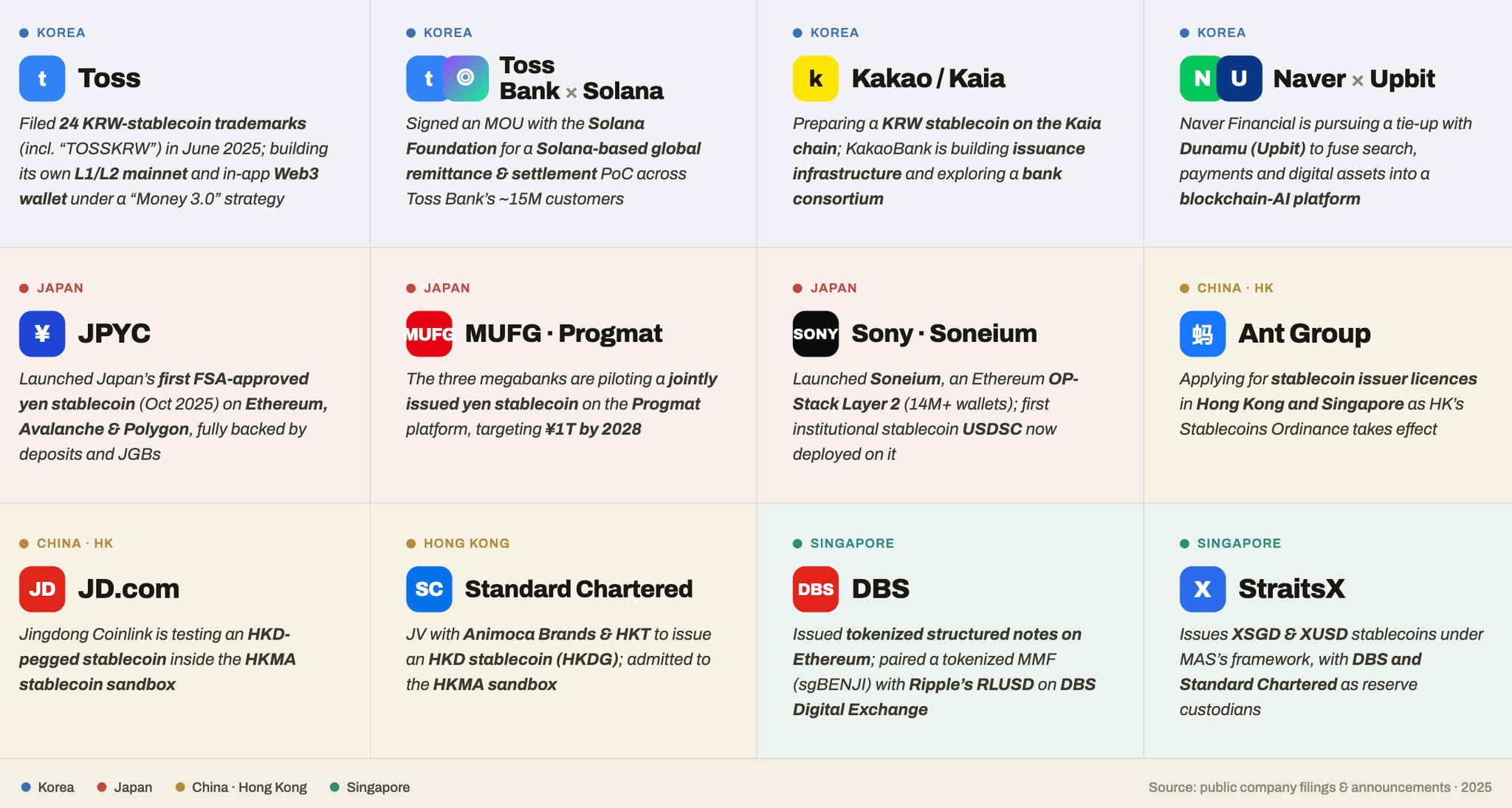

But Korea character tell that they don’t want to fall behind, and other markets are already moving. The U.S. has passed the Genius Act, Japan has licensed JPYC as its first regulated yen stablecoin, and Hong Kong has passed a Stablecoins Ordinance that has already enabled issuers like HSBC and Standard Chartered to enter the space.

Korea has one of the strongest retail user bases in the world, but institutional participation has lagged. That imbalance will increasingly pressure banks, conglomerates, and regulators to step in and build.

What makes Korea uniquely suited is there business with global vendors. The country does not mine commodities, yet its firms hold an $18.6 billion EPC backlog for nuclear plants, its chipmakers control roughly 80% of the global HBM market, and its shipbuilders carry more than 70% of global orders. These are long-tenor cash flows, anchored to real counterparties and mostly denominated in dollars, the kind of industrial base that fits the stablecoin payment and STO framework. There are rooms where inefficiency could be removed by adopting crypto in an institutial level.

Korea has long been restless and risk-seeking, always looking toward whatever comes next. That same restlessness once produced chaos in its crypto market, and now it is producing structure.

That is exactly what EastPoint:Seoul is built for. By bringing regulators, institutional leaders, and crypto protocols into the same room, it creates the space for the coordination and discussion this moment demands.

Now is the moment for coordination and discussion. Korea is at a turning point.

Key Takeaways

- Korea's fast-moving, speed-driven culture made it an early crypto hotbed, producing the 2017 kimchi premium, the 2021 NFT mania, and the painful 2022 Terra/Luna collapse before the market began to mature.

- Retail trading rebounded powerfully to roughly $77.5B in H2 2024 with close to 20% of the population invested, though liquidity has recently rotated toward a booming equities market.

- The market is now institutionalizing as clearer laws recognize tokenized securities, the Bank of Korea's CBDC pilot and private won stablecoins move toward coexistence, and major banks and platforms race to build the payments stack.

- Korea has long been restless and risk-seeking, always looking toward whatever comes next. That same restlessness once produced chaos in its crypto market, and now it is producing structure.

EastPoint:Seoul is the first private conference to bring together institutional leaders, regulators, and Web3 pioneers to shape the future of digital assets and the AI economy in Korea.

1. Why Are We in Crypto?

Everyone arrives in crypto for a different reason, and those reasons rarely fit into a single story. Some people are chasing a technology they believe in, while others are simply looking for the next way to grow their savings. The honest truth is that most of us hold several of these motivations at the same time.

A few of the most common reasons tend to sound like this:

- I want access to infrastructure that resists state censorship.

- I do not want my entire life savings sitting inside a single bank or brokerage.

- I enjoy a culture where I can connect and build a community with people all over the world.

- I believe crypto will become the financial backbone of the next generation.

- I want to make money.

These motivations overlap far more than they conflict, and that overlap is what gives the industry its energy. Because opinions are shared, praised, and torn apart in the open, ideas evolve at a speed that traditional finance rarely matches.

That same radical transparency is also why the space stays perpetually crowded with scams, genuine innovation, and competing visions of where it should go next.

No market has lived out that mix of mania and reinvention more vividly than Korea, which is where this story begins.

2. Korea Was a Mess

Korea is a famously fast moving country. It grew from postwar poverty into an advanced economy in barely two generations, and that experience taught an entire society that speed equals survival.

That catch up reflex never switched off, and the surrounding infrastructure keeps reinforcing it every single day. The fastest internet in the world, shops and services that run around the clock, and delivery that arrives within hours all train people to expect things instantly. A national temperament like this rewards those who act first and ask questions later.

Crypto slots into that mindset almost perfectly. It offers fascinating novel tech, a constant stream of narratives to follow, and the promise of fast money for anyone willing to move early. There was a strog synergy between the culture and the crypto asset class.

That synergy showed up early. By late 2017 the frenzy was so intense that bitcoin traded at a "kimchi premium" above 50% over global prices, a gap that existed simply because local demand outran what exchanges could supply (Also, the isolation of exchange was a cause).

Source: Bitcoin's kimchi premium is no free lunch

The next wave in Korea was the retail NFT mania of 2021, much of it built on Klaytn. Capital rushed into locally branded collections that had little utility to back them up. Because the market was so domestic and speculative, its decline ran even deeper than the global NFT crash.

Then came the reckoning, and Korea sat at the center of it. In May 2022 Terra and Luna, the ecosystem built by Korean founder Do Kwon, collapsed and erased roughly $40 billion in a single week. The contagion spread quickly, and by November 2022 FTX had failed too, part of a rout that wiped some $2 trillion off the global market from its 2021 peak.

The years from 2022 to 2023 became some of the darkest the local market had ever seen. Confidence collapsed, projects folded, and little beyond speculative trading was left. It was the kind of reset that forces an industry to rethink its foundations.

3. Korea Retail Trading Boomed

Source: The State of the Korean Crypto Market - Kaiko

However, as the market got better, Koreans came back to trade. If tokens have found genuine product market fit anywhere, it is in Korea, where retail traders have embraced digital assets with an intensity that few other markets can match.

What makes the Korean retail crowd distinctive is its comfort with volatility rather than its fear of it. These traders actively seek out sharp price swings, and they happily venture deep into long tail tokens that more conservative markets ignore.

The appetite is strong enough to sustain a structural kimchi premium of roughly 2% to 3%, the persistent gap between local and global prices. That behavior turns Korea into a region where new tokens can find liquidity and attention almost overnight. Korea's crypto market roughly doubled to about ₩108 trillion, or $77.5 billion in the second half of 2024, with close to 20% of the population trading and the investor base past 16.2 million, outpacing the stock investors in 2025.

Lately, though, that appetite has rotated toward equities. The KOSPI rose 76% in 2025 to finish as the world's best-performing major market, individual investors' net buying jumped 54% over the prior year, and an AI and semiconductor supercycle added roughly $1.7 trillion in market value. Retail liquidity chasing the next big move simply found a louder story in chip stocks.

This is just a short-term rotation to more volatile investment. The volume has moved, but the building has not stopped, now the focus has shifted from retail screens to institutional strategies.

Source: Korean Exchanges Facing a Volume Plunge. Is It Really a Crisis? | FP RESEARCH

4. Korea Is Institutionalizing

The next chapter of Korean crypto is being written by institutions rather than retail, and that is the real shift in the background. Over the past eighteen months Korea has produced more concrete digital asset policy than in the previous eight years combined, and capital is moving into place behind the rules.

Three forces are converging at once: a legal foundation that finally recognizes tokenized assets, a discussion over digital money between private stablecoins and CBDC by Bank of Korea, and a land grab among platforms and conglomerates for the payments stack.

Now, The market is being institutionalized.

4.1 The Foundation: Law Is Getting Clearer

On January 15, 2026, the National Assembly passed amendments to both the Capital Markets Act and the Electronic Securities Act, the twin laws that together recognize tokenized securities.

They run on two distinct legal tracks and take effect in early 2027 after a one-year grace period: the Electronic Securities Act lets eligible issuers create tokenized securities on blockchain rails, while the Capital Markets Act lets those tokens trade as investment contract securities through licensed brokerages. The practical effect is a regulated on-ramp for bonds, real estate, and unlisted shares to move on-chain.

The Digital Asset Basic Act one of the most important and comprehensive pieces of legislation remains under discussion. If passed, it would reauthorize domestic ICOs for the first time since the 2017 ban and require stablecoin issuers to hold reserves of at least 100% of tokens in circulation. The draft also layers in FSC prior authorization, paid-in capital of at least KRW 1 billion, and bankruptcy-remote reserves so a failed issuer cannot drag down its bank.

The holdup has been due to lack of coordination, and have become a political issue. However, it is expected to pass within a year.

4.2 The Digital Money: Stablecoin, and CBDC

The bigger question is not who issues a won stablecoin first. Korea's payment rails are already well built, with cash down to just 15.9% of in-person transactions in 2024, so the real prize is not cheaper or faster payments but programmable, agentic commerce, money that software can hold and move on its own.

That logic is reshaping how the state-led option fits in, not pushing it aside. The Bank of Korea is pushing the Project Han River, its CBDC pilot, as the seven participating banks weighed the cost, a combined ₩35 billion($23 million) transaction was processed. Rather than retreat, the project returned with a concrete use case: routing government grant disbursements worth ₩110 trillion, or roughly $73 billion a year, over tokenized deposits.

The direction would be convergence rather than competition. CBDC and private stablecoins are being discussed to co-exist, and that dual-track approach is now one of the major movements in Korean digital money.

Private issuers are still working out where they fit within the regulatory framework. Most are still in testing like KRW1, launched by custodian BDACS with Woori Bank on Avalanche in September 2025, with each token backed 1:1 by won held in escrow, and a second deployment now testing on Circle's Arc network. For now, it remains a proof of concept rather than a product, with a market cap of around $97,000 and only a handful of holders a useful reminder that the rails are real, but the volume is not (yet).

Banks are coordinating. Korea's largest commercial banks, including KB Kookmin, Shinhan, Woori, NongHyup, IBK, Suhyup, Citi Korea and Standard Chartered Korea, with Hana the latest to join, are building a won stablecoin on shared infrastructure, each filing its own trademarks for separate tokens on a common rail. President Lee Jae-myung has gone further, naming a won stablecoin a national priority and citing $115 billion of 2025 capital flight out of Korean exchanges as the reason.

When rivals this size choose to cooperate rather than compete, the intent is hard to mistake.

4.3 The Financial Institutions and Conglomerates

If the traditional banks go for the cooperation path, the platforms represent a race. Dunamu, Kakao, Kaia, and Samsung are each chasing a different layer of the stack, issuance, settlement, and distribution, and increasingly the same players are colliding.

Dunamu, which runs the Upbit exchange, has launched GIWA, an Ethereum Layer 2 built on the OP Stack with no native token and uses ETH for gas. It is a direct bet on becoming the settlement rail for won and global stablecoins, and a way to loosen Dunamu's near-total reliance on trading fees.

On the issuance side, KakaoBank has moved its won stablecoin from trademarks into active development, filing twelve marks such as BKRW and KRWKKB and leaning on KakaoTalk's reach of nearly 49 million users for distribution. The lines are already blurring: Naver, is in discussion to acquire Dunamu, a deal that would fold issuance, settlement, and a consumer wallet under one roof.

| Player | Initiative | Status |

| BDACS and Woori Bank | KRW1, 1:1 won-collateralized | Live pilot since Sept 2025; on Avalanche, testing Circle's Arc |

| Dunamu, parent of Upbit | GIWA, OP Stack Layer 2 for stablecoin settlement | Testnet live, mainnet planned; no native token |

| Kakao and KakaoBank | Won stablecoin distributed via KakaoTalk | In active development; 12 trademarks filed |

| Samsung Wallet | Offline distribution layer | In talks with Shinhan and Hana |

5. Korea Is at the Turning Point

Regulation is still unsettled, and overall sentiment toward crypto remains cautious. With policy caught in political debate, institutions still lack the clarity they need to move decisively.

But Korea character tell that they don’t want to fall behind, and other markets are already moving. The U.S. has passed the Genius Act, Japan has licensed JPYC as its first regulated yen stablecoin, and Hong Kong has passed a Stablecoins Ordinance that has already enabled issuers like HSBC and Standard Chartered to enter the space.

Korea has one of the strongest retail user bases in the world, but institutional participation has lagged. That imbalance will increasingly pressure banks, conglomerates, and regulators to step in and build.

What makes Korea uniquely suited is there business with global vendors. The country does not mine commodities, yet its firms hold an $18.6 billion EPC backlog for nuclear plants, its chipmakers control roughly 80% of the global HBM market, and its shipbuilders carry more than 70% of global orders. These are long-tenor cash flows, anchored to real counterparties and mostly denominated in dollars, the kind of industrial base that fits the stablecoin payment and STO framework. There are rooms where inefficiency could be removed by adopting crypto in an institutial level.

Korea has long been restless and risk-seeking, always looking toward whatever comes next. That same restlessness once produced chaos in its crypto market, and now it is producing structure.

Now is the moment for coordination and discussion. Korea is at a turning point.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.