Table of Contents

Researcher

Key Takeaways

- Collector Crypt is a velocity business. The gacha machines keep close to 5 cents of every dollar that passes through them and have for 15 months, through a five-folding of volume to $200.5M a month.

- Every card pulled faces four doors, and the split between them is the business. Nearly everything goes straight back to the machine, with 71.8% of June volume in turbo mode. Keeps run at 1 to 2.5% of rip value, physical redemptions at 2.4 to 3.1% of GMV, and P2P marketplace trading under 1%.

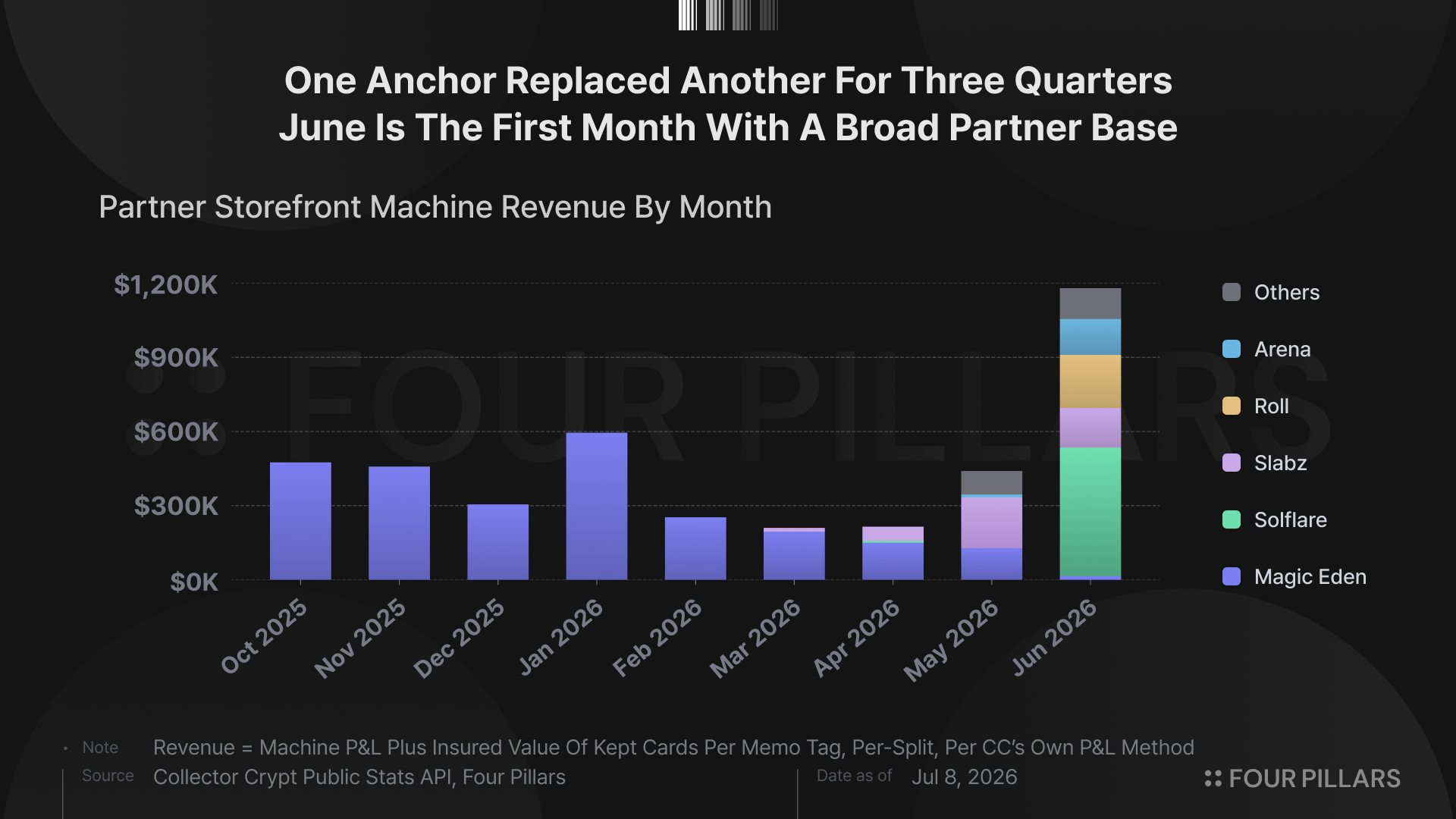

- The same gacha machines increasingly run under other brands. June broke the one-anchor pattern, 21 partner storefronts producing $1.18M with five above $70K each, on the roughly 6% of GMV partners represent.

- The vault is the hidden second business. $23M of below-market inventory has appreciated quietly since token launch, and it ties the machine’s take, the exit spread, and the treasury to a single variable, card prices.

- The token wraps all of it. A Panama foundation holds the IP, the cards, and the treasury, the float trades near 1x machine gross margin, and the same operational wallet that pays machine sellbacks has been funding CARDS buybacks for over a month, verified on-chain, while the mechanism a holder could underwrite remains undocumented.

When the Collector Crypt (CC) team took our call after my second article they rightfully disputed, they asked for one thing. Not an apology, but that accurate data reach the community, and that we understand the business well enough to read its chain correctly. This piece is that request taken literally. It is the last of a trilogy and the first with the complete picture, which is an admission in itself. The map arrived at the end of the journey, because the journey is what earned the map.

I pulled 5.97 million confirmed rips from CC’s public stats API, the platform’s full usable history from April 2025 through this week, each carrying its cost, outcome, machine, rarity tier, and wallet. This draft was fact-checked by the CC team before publication. The conclusions are mine.

28,750 wallets have put $805M through the machines since April 2025. The pages below walk through it in operating order. How the gacha machines earn, who plays them, who distributes them, what sits underneath them, and what the token wraps around all of it.

1. The Velocity Business

Collector Crypt sells randomized packs of graded trading cards, $25 to $2,500 a pull, each card backed by a physical slab in its vault and sellable back to the machine the moment it arrives. Every rip, sellback, keep, and redemption prints to Solana.

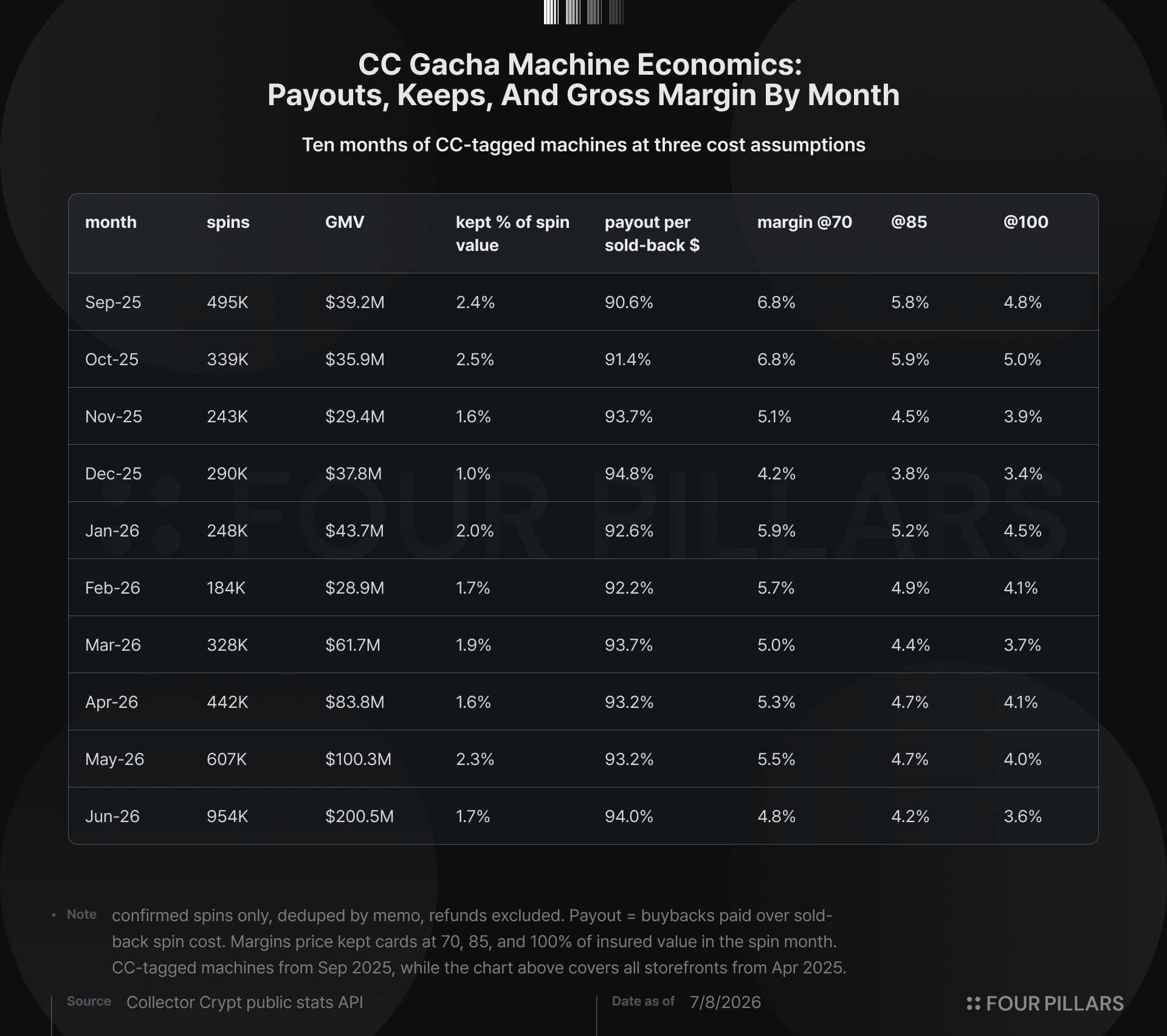

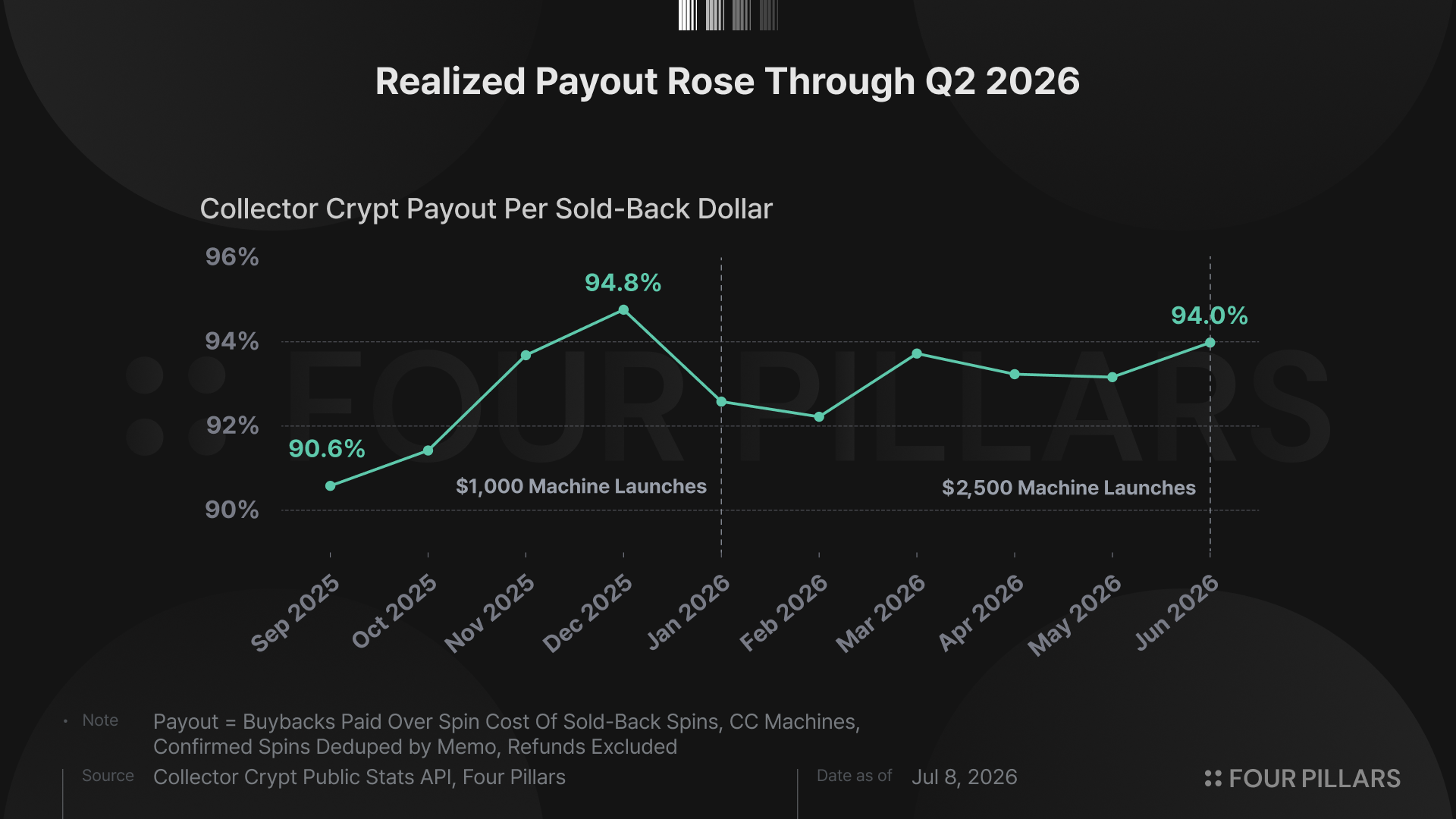

The gacha machine keeps close to 5 cents of every dollar that passes through it, and has for 15 straight months. My previous article shows margins collapsing from 11.2% to 5.6% over the same window because they count a kept card as pure profit until the day it ships. Price each kept card in the month its pack sold and the business earned 5.3% in April 2025, 5.8% through the autumn, and 4.2% this June, never outside a band of roughly 4~7.

The measurable facts of that stretch are four. Between September and December 2025, payout per sold-back dollar rose from 90.6% to 94.8%. The share of rip value users kept halved from 2.4% to 1.0%. The buyback rate did not move, exactly 90% on the $250 machine at every rarity tier in every month of per-rip records and exactly 85% on the small machines. And the insured value the machine dealt per rip dollar rose from roughly 1.02 to 1.06 times pack price. The data says that much. What combination of user behavior, inventory, card prices, or targets produced it is not something spin records can settle, and this report does not guess.

The timing does rule two things out. The $1,000 Grail machine did not exist until January, when it did $25.2M in its debut month, so the move was complete before the big machines my second article blamed had launched, and free packs only reached the $250 machine around March 2026, after it. Tuomas Holmberg said pack mix could not produce a move of that size. The data agrees.

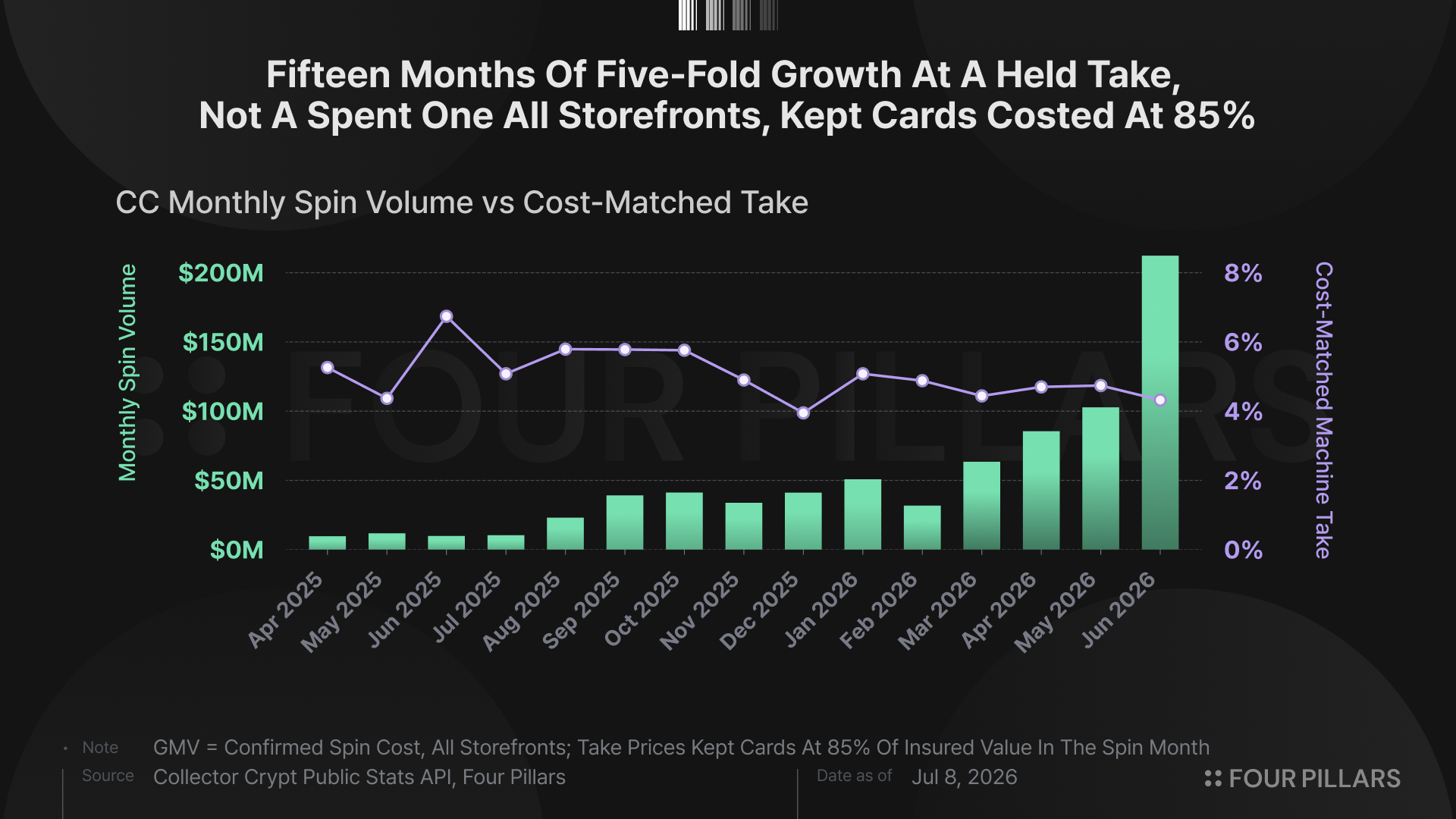

Volume exploded right through the shift. GMV rose from $39.2M last September to $200.5M in June while the take held, which means margin dollars roughly quadrupled to $8.4M a month, and average ticket size rose from $79 to $210 as Grail and Mythic buyers became the majority of flow. CC earns like a toll booth on a road whose traffic quintupled, not like a casino widening its edge.

Two forces guard the model’s edges. Beneath it sits a pricing oracle that scrapes eBay daily and weighs sale type and seller quality on every comp, the reason a machine paying out 94% of value does not get picked apart by stale prices, and in Tuomas’s blunt telling “the reason competitors outsource pricing to third-party models, alt.xyz in his examples, can advertise positive EV while delivering meaningfully negative, since a machine that stocks whatever looks cheap against an outside oracle fills itself with the oracle’s mistakes.”

He is careful to add that CC’s own pricing is not perfect yet either.

Above it sits GameStop, in the category since April and paying users 90% of Card Ladder value minus a 6% selling fee, roughly 84.6% net under terms still posted as of this week. That is a different value basis than CC’s insured-value payouts, and it is a public reference price all the same, one that makes the take’s floor the number to watch. June’s 4.2% was the tightest full month on record and early July ran tighter on a small sample.

2. The Collector’s Option

However the players sort, every card pulled lands at the same fork. It can go straight back to the machine, stay in the vault, ship home as cardboard, or change hands on the marketplace, and those four doors are the next four subsections.

2.1 Sellbacks

The dominant outcome. Users sell the card straight back at the posted buyback rate, 85% on small packs, 90% mid-tier, 93% at $1,000 and above, and 71.8% of June volume ran in turbo mode, the setting built for instant sellback. Tuomas calls the ladder deliberate, since high-value cards cost CC 90 to 93% of market to acquire, and a big machine paying out much less would hand competitors a cheaper inventory source than the card shows they fly to.

The slab returns to the vault to be dealt again, working capital collecting the spread on every pass.

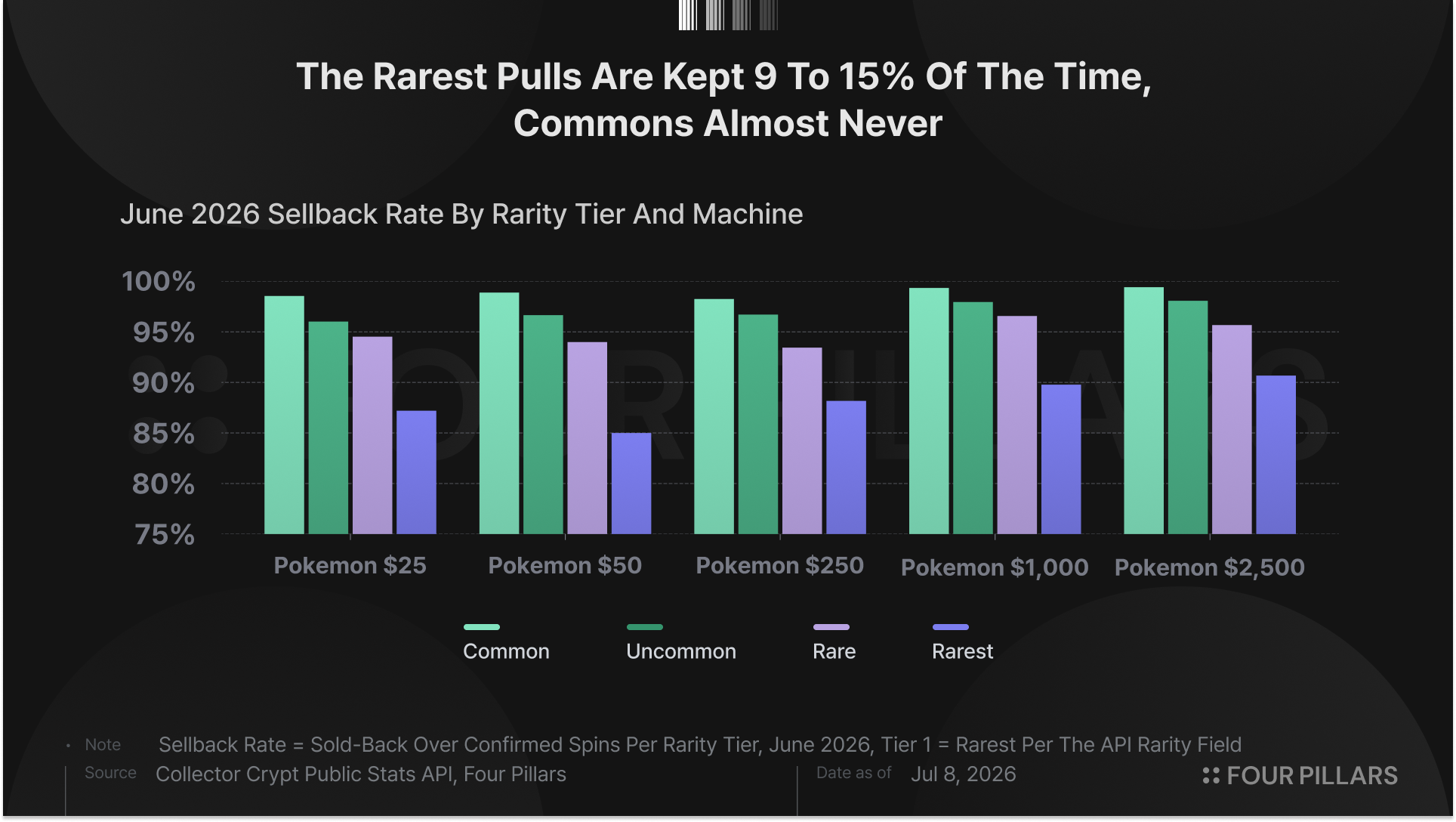

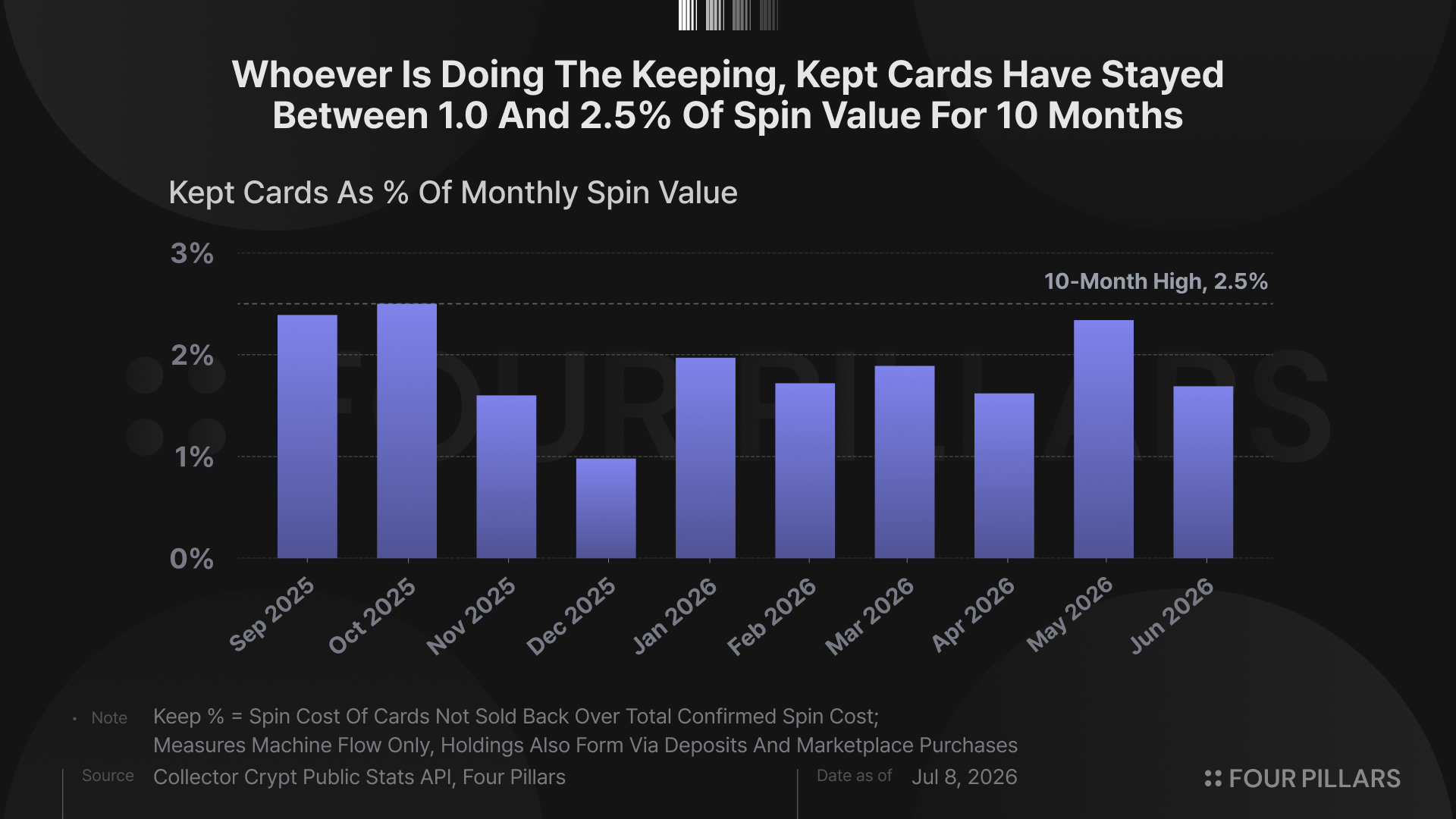

2.2 Keeps

Cards kept have run between 1.0 and 2.5% of spin value for the full measured history, and they are not the average pull. The rarest tiers get kept 9~15 times more often than commons, and at the multiples those hits carry, a keep costs CC more than the spin brought in at any plausible acquisition cost. A keep in this data is a hit being claimed, leakage the gacha machine’s posted EV prices in and funds from the sellback spread, the way every game funds its winners from the floor’s edge. What the flow cannot read is intent. Recycling commons is what any rational player does, collectors included, since nobody collects commons, so the keep pattern sorts users by what they keep rather than whether they gamble. Most of the top hundred keep almost nothing, a few keep only the monsters, and grail hunting is collecting too, it just costs CC money instead of earning it. Some of the residue is not organic demand at all, since CC attributes elevated common keeps on some machines to third-party strategy tokens that pull cards out to distribute to their own holders.

Collecting is the option CC is paying to keep open, not the base it runs on. The keep rate measures flow, not stock, and the stock is real, with leaderboard whales holding six-figure vaulted collections and the largest having accumulated $1.48M of kept cards even at a half-percent rate. Holdings also arrive through doors the spin data cannot see, since users deposit their own physical cards into the vault and buy listed cards from one another on the marketplace, so a low keep rate describes how a wallet plays the machine, not whether it collects.

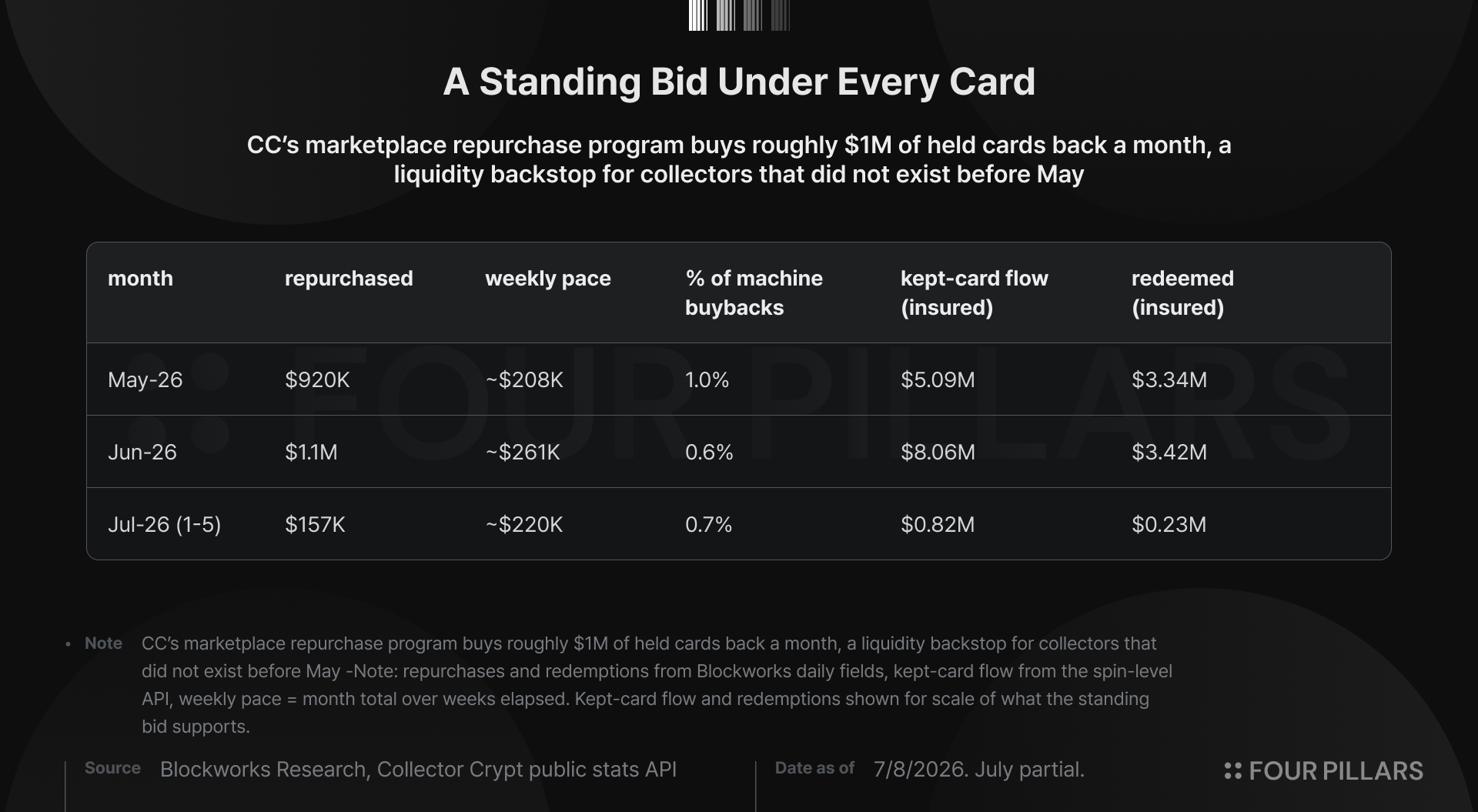

Since May a marketplace repurchase program has bought roughly a million dollars of cards a month back from holders at their discretion, a standing bid under every card that turns keeping into a liquid position instead of a lock-up.

2.3 Redemptions

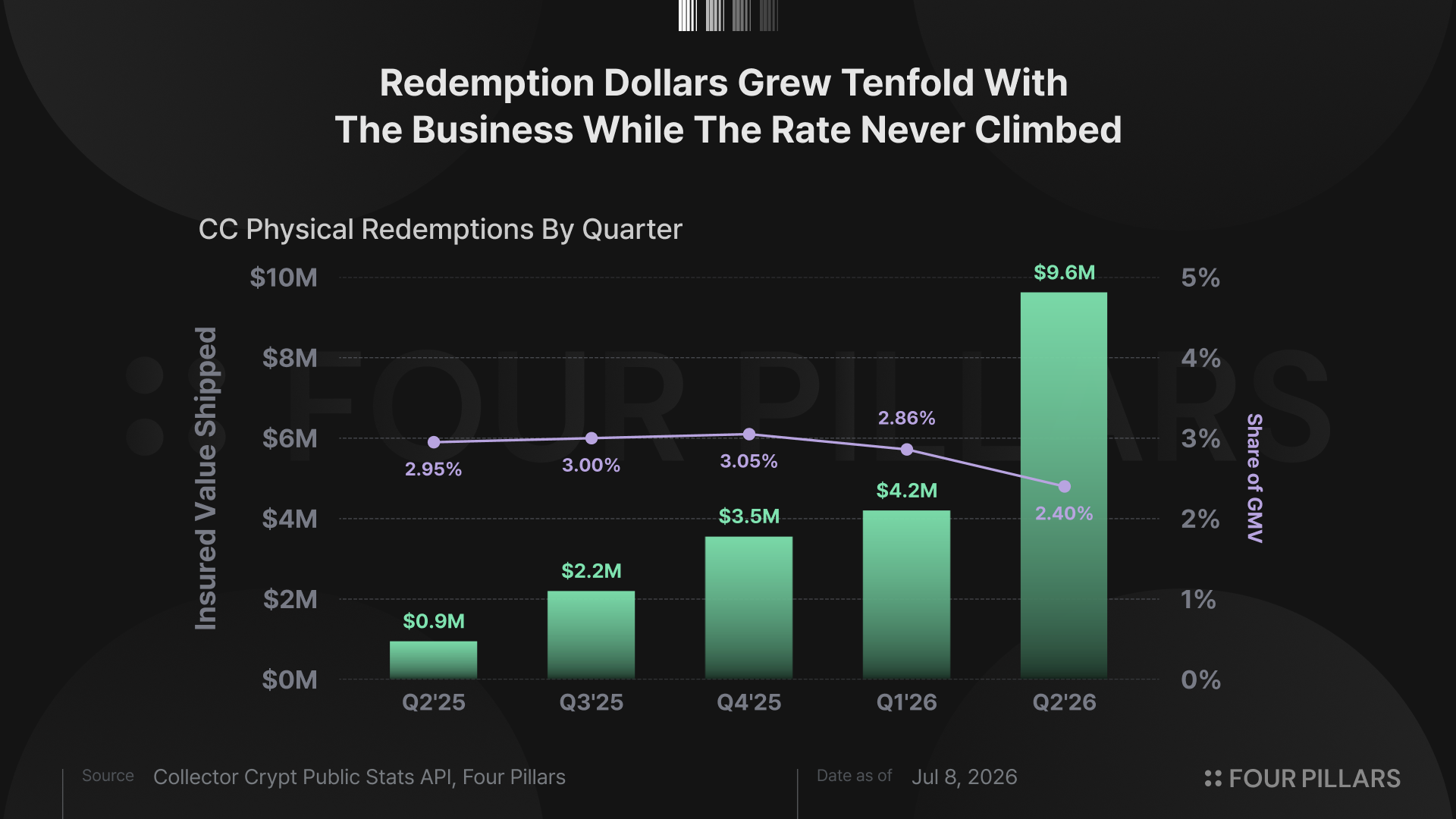

Physical delivery runs at a steady 2.5 to 3% of GMV, 5 straight quarters, with roughly 600 wallets shipping over 5,000 cards home in the latest 30D window per CC’s fulfillment data. Each redemption out-earns a sellback, since CC keeps the pack revenue and gives up a card acquired below market, and redeeming got cheaper this spring after CC brought vaulting in-house, dropped redemption fees entirely, and began subsidizing shipping. The whale cohort barely uses this door, with the top hundred accounting for roughly 6% of visible shipment activity, so physical demand belongs mostly to smaller collectors, though at least one power user has shipped seven figures of cards home. My June piece reported these redemptions an order of magnitude wrong from a broken on-chain proxy, and the corrected forensics live in the standing correction.

2.4 Secondary Trading

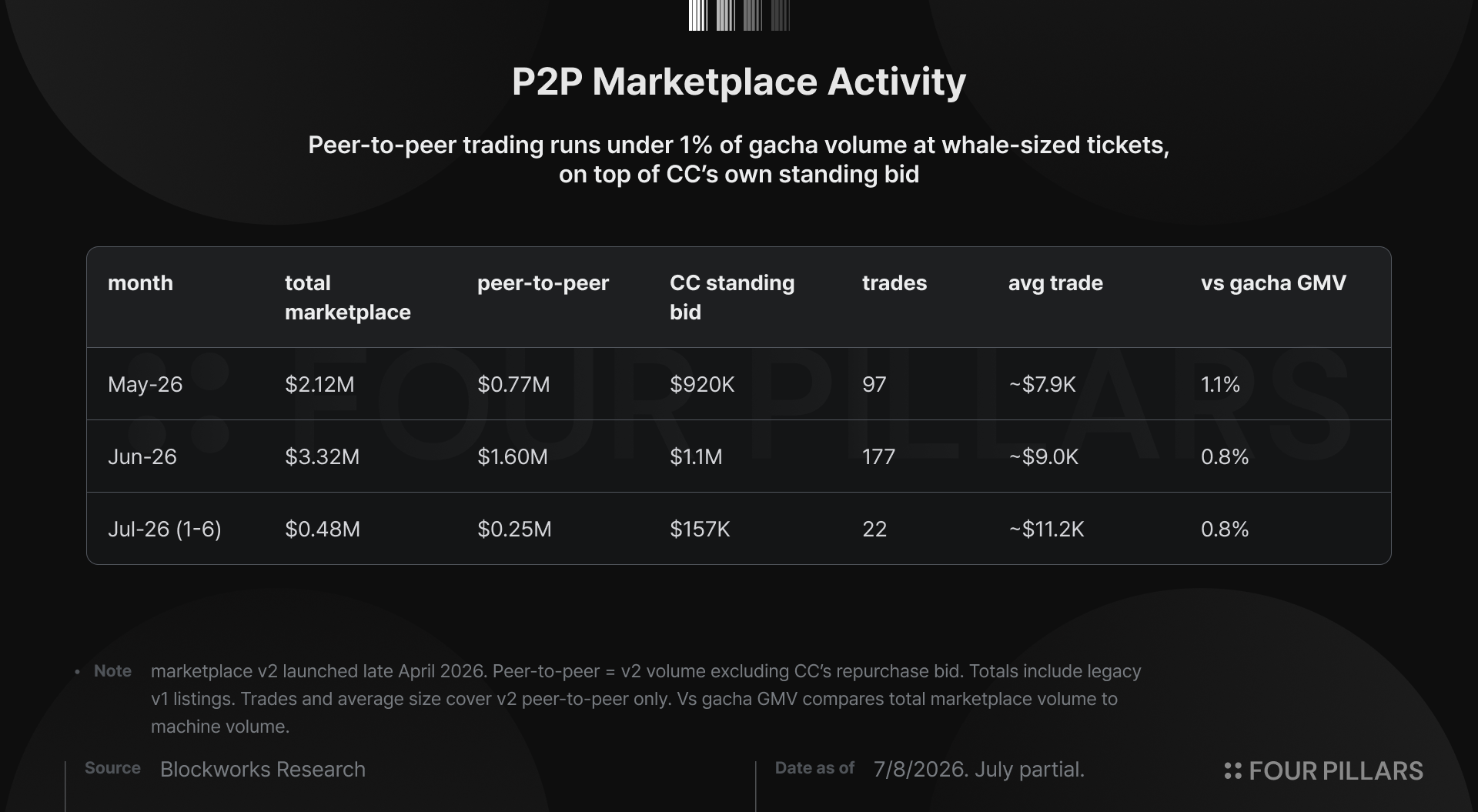

The last door is the youngest. A rebuilt peer-to-peer marketplace went live in late April, and it is small, whale-sized, and doubling. June cleared $1.6M of peer-to-peer volume across 177 trades, roughly $9K per trade and under 1% of gacha GMV, with about a hundred daily marketplace users against several thousand machine players.

Another third of marketplace volume is CC’s own standing bid, the repurchase program from 2.2 executing in public. A secondary market this thin says the collector economy is still an appendix to the machine. A secondary market doubling month over month on subsidized liquidity says CC is building the room where one could form.

Tuomas frames the ambition as “eBay with auctions to come and pack ripping an onramp that maybe 20 to 40% of the eventual collector base will ever use.”

2.5 The Power Users

That said, the demand side of the machine is about a hundred wallets deep. The top hundred by CC’s own points leaderboard produced $384.5M of lifetime volume, 48% of everything, while keeping 1.3% of spin value, half the rate of the other 28,650 wallets. The largest single wallet has cycled $37.7M through the gacha machine and kept half a percent. In the entire top twenty, exactly one wallet collects through the machine itself, keeping 17% of what it pulls at near-average card values. Monthly depositors tell the same story from the other side, roughly 5,500 in October collapsing to 2,400 by March and recovering to 5,900 in June while spend per depositor tripled.

3. Anchors to Stack

The same machine increasingly runs under other brands. Partner storefronts sell CC’s inventory through CC’s B2B rails under their own frontends while CC keeps its inventory spread. My June piece put partner revenue at $1.83M all-time based on a dashboard field that captures one-off mint events, and the recurring business is an order of magnitude larger.

Magic Eden’s machines peaked near $477K of monthly revenue in October 2025 and faded toward zero as its priorities shifted. Solflare ramped to roughly $520K in June. For 3 quarters the pattern was sequential anchors, one tenant replacing another, and June broke it, 21 partner tags producing $1.18M with 5 storefronts above $70K each. One month is not a trend. It is the first month the partner base looks like a stack rather than a spotlight, and whether the stacking holds is now a falsifiable quarterly test on the roughly 6% of GMV partners represent.

4. The Second Business

Every card in every machine was bought below market, and that spread is a business of its own. CC acquires inventory at roughly 85% of market through card shows, algorithmic eBay bidding, and bulk channels, and then prices move. Modern Pokemon roughly doubled off its December low on CC’s own index, vintage is up about 130% since October, and a card bought before that run and redeemed today carries an original cost closer to 70% of its current price. After a heavy recent month of buying at today’s prices, Tuomas puts blended cost back near 85%, and by his own framing neither side can prove the precise figure, which is why every margin in this report exists at three cost assumptions and the shape of the story survives all of them.

Source: Collector Crypt

Source: Collector Crypt

CC also reports that GameStop’s April entry has not materially moved its acquisition costs or win rates so far, a claim this report’s data can neither confirm nor refute.

The vault has grown from roughly $3M at token launch to about $23M, $18M of it tokenized, worth roughly 1/3 of the circulating float and compounding below the dashboards’ line of sight. Tuomas volunteered the reverse case himself, a real card-price downturn means losses on heavy inventory that machine margins would have to offset, and he is right. There is no hedge anywhere in this structure. The machine’s take, the exit spread on redeemed cards, and the vault’s mark all move with the same underlying, which makes Collector Crypt, measured end to end, one long position on card prices expressed three ways, a machine monetizing the flow, a spread monetizing the exits, and a book monetizing the mark.

5. What a $CARDS Holder Owns

The token wraps the whole position, and the wrapper is unusual. A Delaware C-corp employs the team and holds no economics. The IP, the cards, the stablecoins, the treasury, sits in a Panama foundation, and the foundation is the token. There are no venture investors on the cap table and employees hold tokens rather than shares. An acquirer buying the operating company would get, in Tuomas’s words, nothing. The stated philosophy is that a project cannot serve two masters, so it is either token or equity, and CC chose the token. The design eliminates the equity-versus-token conflict that has burned holders elsewhere, and it concentrates the entire underwriting question into one mechanism. How does foundation value reach a CARDS holder?

The arithmetic is simple even where the answer is not. CARDS trades at $0.2042, a $72M circulating market cap and $408M FDV as of June 7, 2026, against machine gross margin annualizing to roughly $68M from Q2 at the 85% cost band, so the float trades near 1x and the FDV near 6x gross margin with the card book alongside. The float is 20.5% of two billion tokens, insider allocations total 72% of supply across Foundation (36.75%), Team (19.5%), Pre-Seed (8.2%), Advisors (4.37%), and Seed (3.67%), with Community (20%), Genesis Launch Pool (5%), and Raydium LP (2.5%) making up the rest, and the remainder vests on a public schedule through November 2027. So gross is not net, June was the largest month in company history, and 16 months of unlocks sit between the two multiples. Underwrite the second and enjoy the first.

No documented mechanism carries foundation value to the token yet, but the flows themselves are no longer a matter of inference. A wallet first flagged by the community account Bobby has been buying CARDS in continuous small clips for over a month, funded with USDC sent directly from the same Gacha operational wallet that pays every machine sellback. I verified both legs on-chain this week, the funding and the buying, which was still running as this report went to press.

Earlier onchain work by Lukas Ruppert traced a $500K escrowed buyout of a pre-seed investor’s 4 million CARDS from treasury wallets in May and a separate $887K of TWAP accumulation in June. CC declines to confirm or deny any of it and says it will address buybacks in its own publication.

Operational revenue is visibly flowing into token buys. What is missing is the part a holder can underwrite, since an unacknowledged buyback can stop as quietly as it started, and converting visible flows into a stated mechanism is the highest-leverage disclosure CC could make.

6. Where I Land

Three pieces and one public correction later, the portrait is complete. Collector Crypt is a velocity business with a take that has held near 5 points through a full rebuild of how it charges, a distribution layer that just printed its first broad month, and an appreciating card book underneath it all, every leg long the same variable. The business is steady and growing.

Which leaves a strange and useful conclusion. The measurable part of Collector Crypt is now settled, and none of it is where the risk lives. What cannot be measured is the only thing left to underwrite. A TCG cycle nobody controls, and a foundation choice nobody outside can see. The cash flows are substantial but the mechanism that delivers them to tokenholders still is not, so a CARDS position today is a bet on TCG prices and on the foundation’s decision going forward, with documented or programmatic buybacks the single disclosure with the most room to re-rate the multiple.

The one question left is what the foundation does with its next dollar.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.