Table of Contents

- Key Takeaways

- 1. Overview: Agentic Commerce and the Role of Blockchain

- 1.1 The rise of agentic commerce and its structural bottlenecks

- 1.2 Three types of agentic commerce

- 1.3 Blockchain widens the payable surface of agentic commerce

- 2. Global trends: Where is Blockchain's Moat?

- 2.1 L1 connection layer: Connectivity standards are converging

- 2.2 L2 commerce layer: The agent commerce execution tier

- 2.3 L3 identity layer: Verifying the agent's identity

- 2.4 L4 delegation layer: Setting the boundary of an agent's authority

- 2.5 L5 payment layer: The money-movement rail of the agent economy

- 3. Opportunities in the Korean Market: Expansion of Super Apps and The K-layer

- 3.1 Agentic commerce is the breakthrough that solves the KRW stablecoin's use-case problem

- 3.2 If the super-app has payment and commerce layers ready, go after agentic commerce

- 3.3 If the layers are not there, build a K-layer

Researcher

Key Takeaways

- Agentic commerce refers to a new commerce model where AI agents act not only as shopping assistants, but also as transaction interfaces that can search, compare, order, pay, and settle on behalf of users or businesses.

- Agentic commerce can be divided into three levels: agent-assisted commerce where humans approve the final purchase, delegated commerce where agents act within predefined rules, and agent-native commerce where autonomous agents transact directly with APIs, data, models, or headless merchant endpoints.

- Blockchain’s main role is not to replace card networks, but to expand the payable surface of commerce into areas that traditional payment rails cannot efficiently serve, such as sub-cent micropayments, accountless API calls, and machine-to-machine transactions.

- Across the agentic commerce stack, blockchain’s strongest moat appears in permissionless commerce discovery, decentralized agent identity and reputation, and instant stablecoin settlement for autonomous T3 transactions.

- In Korea, agentic commerce could become the strongest use case for KRW stablecoins, while superapps with both commerce and payment layers, such as Kakao, Naver, and Toss, are well-positioned to lead the early market.

This article is adapted from "Korean Blockchain Guidebook for Institutions 2026," jointly published by Four Pillars and Pantera Capital. The full report covers 14 more themes for companies and institutional investors.

1. Overview: Agentic Commerce and the Role of Blockchain

1.1 The rise of agentic commerce and its structural bottlenecks

Agentic commerce is commerce in which an AI agent, after being granted authority by a human or a corporation, carries out some or all of discovery, comparison, ordering, payment, and settlement. The agent here is no longer a shopping-assist tool. It is the interface of the transaction and the party that executes it.

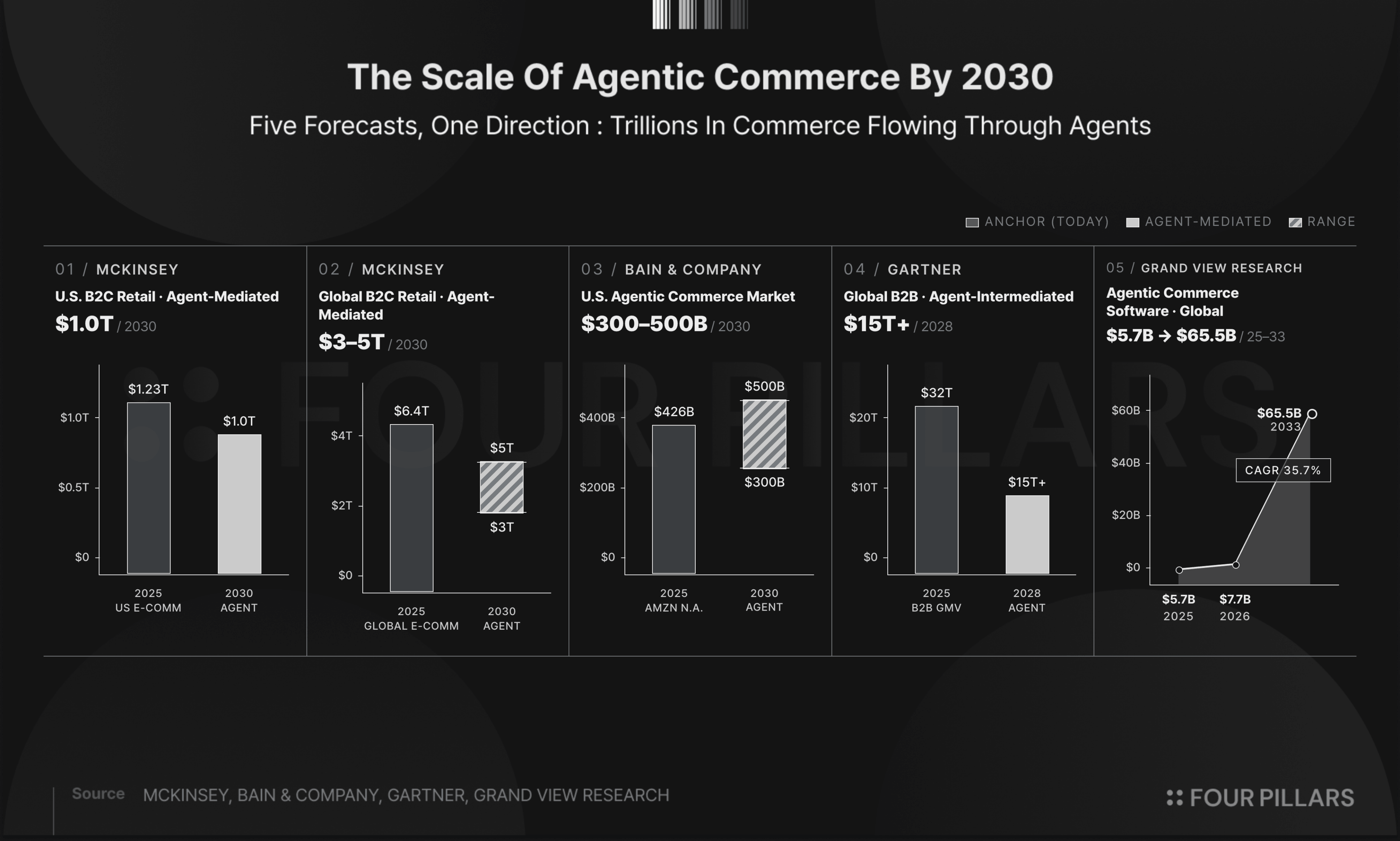

McKinsey projects that by 2030, global consumer commerce mediated by AI agents will reach USD 3 to 5 trillion. Gartner estimates that in B2B, up to 90% of purchases could pass through AI agents by 2028. Bain and Grand View Research point the same way through their estimates of U.S. e-commerce penetration and market size.

The first stage for agent-driven commerce is the existing e-commerce ecosystem. Card and bank-account rails process most of global commerce volume on top of decades of merchant networks, user bases, and settlement infrastructure. The early forms of agentic commerce, such as the assisted-shopping structures of Amazon, Walmart, and ChatGPT, also run on this infrastructure.

These payment rails, however, assume that a human does the paying. E-commerce itself grew on a flow in which a human consumer browses products and presses a payment button. The existing infrastructure assumes identity verification of a person or legal entity, prior registration, explicit authorization, and a post-hoc dispute process. In this setting, the agent is less an independent transacting party and more a delegated executor moving within the user's own payment method and authority.

Coinbase's Brian Armstrong describes how agents work inside this structure with a "parent-child model." The parent (the human) holds the account and the limits; the child (the agent) moves only within that granted authority. As agents rise into the role of transacting parties, this delegation model will become a bottleneck, and a range of agentic commerce modes with different delegation levels is already taking shape.

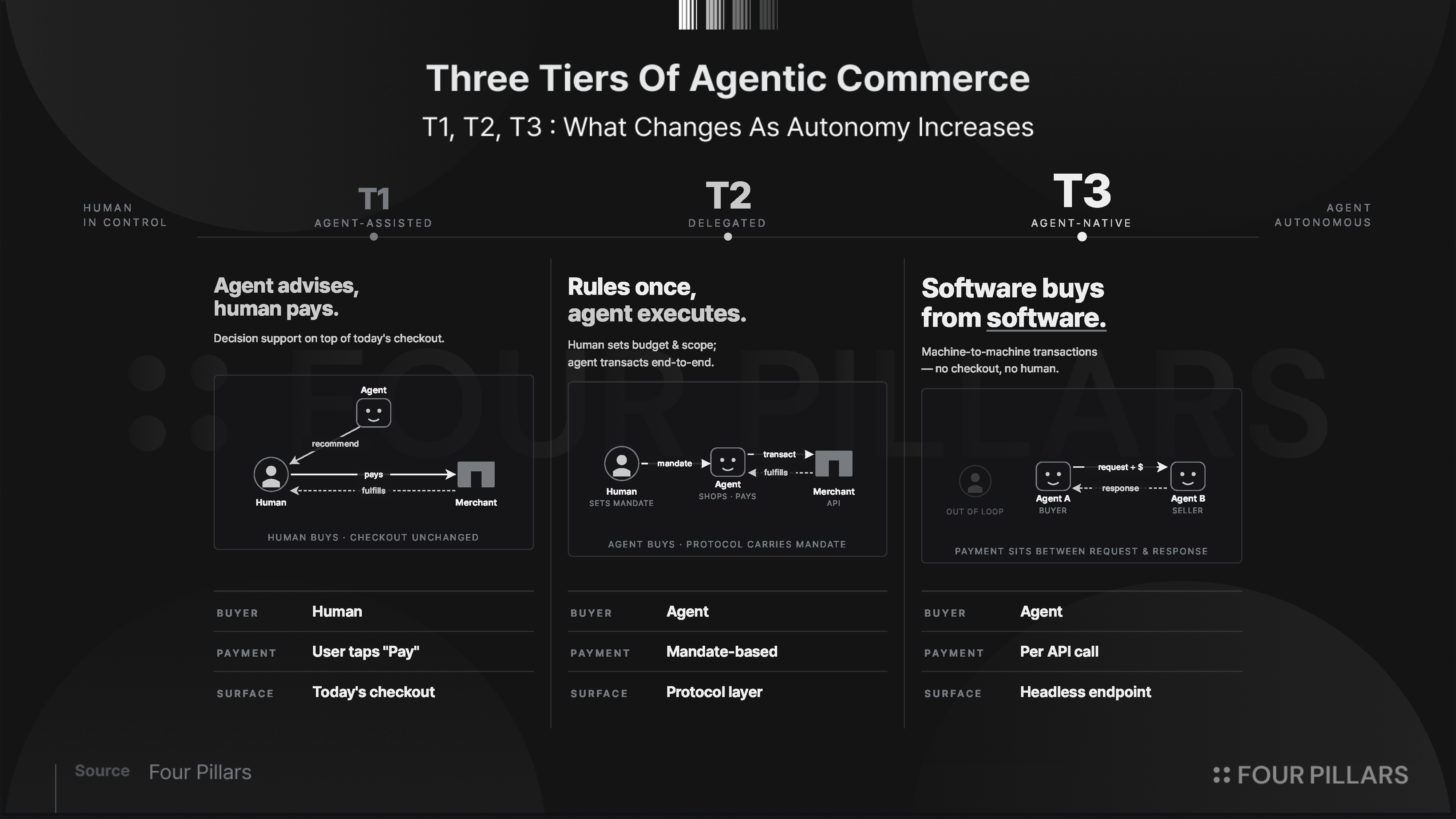

1.2 Three types of agentic commerce

Agentic commerce splits into three types by the level of delegation given to the agent:

- Agent-Assisted Commerce (T1): Agent UX sits on top of existing e-commerce. The agent handles discovery and comparison, but the human makes the final purchase and authorizes payment. The agent is a decision-making assistant, not a purchasing party. Examples include Amazon's Rufus, Walmart's Sparky, ChatGPT's Instant Checkout, and Gemini's shopping integration.

- Delegated Commerce (T2): The user sets rules in advance (budget, conditions, cadence, preferred brands), and the agent handles everything from discovery to payment within those rules. What matters here is user consent, control over the agent, and compatibility with existing retail infrastructure, more than the payment method itself.

- Agent-Native Commerce (T3): A permissionless structure in which demand and supply participate freely without prior registration or vetting. The agent directly calls digital resources (APIs, data, model inference, and so on) without a final human approval or shopping UI, and completes payment. Suppliers also act as "Headless Merchant Endpoints" that receive funds through APIs alone, without a website. This widens the payable surface of commerce indefinitely.

1.3 Blockchain widens the payable surface of agentic commerce

Most of today's discussion about agentic commerce sits in T1 and T2, both of which assume human involvement and a moderate level of delegation. These forms combine agents with the existing e-commerce flow, so the business model is easy to picture, and the commercial references that have surfaced so far cluster in this range. Over the past three to five months, though, builders from Web2 and SaaS backgrounds, along with people from Stripe, Coinbase, and other major payment-infrastructure firms, have been launching agentic-payment startups aimed at the fully autonomous T3 area. The share of discussion devoted to T3 is growing quickly. The competitive line between payment infrastructures is splitting by target area.

- T1, T2: Card networks and existing commerce protocols sit at the center of the standard, and stablecoin payment rails compete as complements.

- T3: On-chain stablecoin payment rails such as x402, and M2M payment standards such as MPP (Machine Payment Protocol) that support both card networks and stablecoins, rise side by side.

Blockchain-based stablecoin rails come forward across both areas because blockchain has three structural advantages in agentic commerce.

- Smart Wrapper structure: Pause, reward, and collateral logic can be written into the asset itself, so payment rules are enforced as code. Within a pre-delegated scope, transactions execute automatically without repeat approvals.

- Extremely low entry barriers: A wallet alone is enough to transact. No API key, no account. Suppliers can receive payment through a single endpoint without a business registration. In the case of x402, payment is embedded into the HTTP request itself, without the burden of a merchant account, a processor, onboarding, or chargebacks.

- A structure tailored to machine-to-machine (M2M) transactions: It covers areas that human-premised rails struggle to reach. Sub-cent agent-to-agent payments, 24-hour programmable cross-border settlement, and agent-to-agent transactions that run within a pre-delegated scope without repeated human intervention all fall in this range.

Blockchain does not push card rails aside. Cards have their own strengths and moats, and infrastructure work aimed at the agent environment is moving quickly, led by Visa, Mastercard, and Stripe. The range in which these responses work is limited, though. Batch settlement, proposed as a micropayment workaround, is effective up to about a few dollars per transaction. Sub-cent M2M transactions, endpoints that operate without a business registration, and payments by autonomous agents with no legal personhood are not easy for card infrastructure to absorb.

So the role of blockchain is not to take share from card networks. It is to widen the payable surface of the agent ecosystem. In T1 and T2, blockchain expands alongside card rails as a complement, and card networks extend into agent-friendly infrastructure. In the T3 long tail, where the economics of the traditional merchant model rarely work (accountless endpoints, ultra-small API calls, agent-to-agent task transactions), on-chain stablecoin rails have a more natural entry point.

Below we look at how agentic commerce is actually operating, where blockchain can build a distinct moat across each transaction type (T1 through T3), and which direction the market is moving.

2. Global trends: Where is Blockchain's Moat?

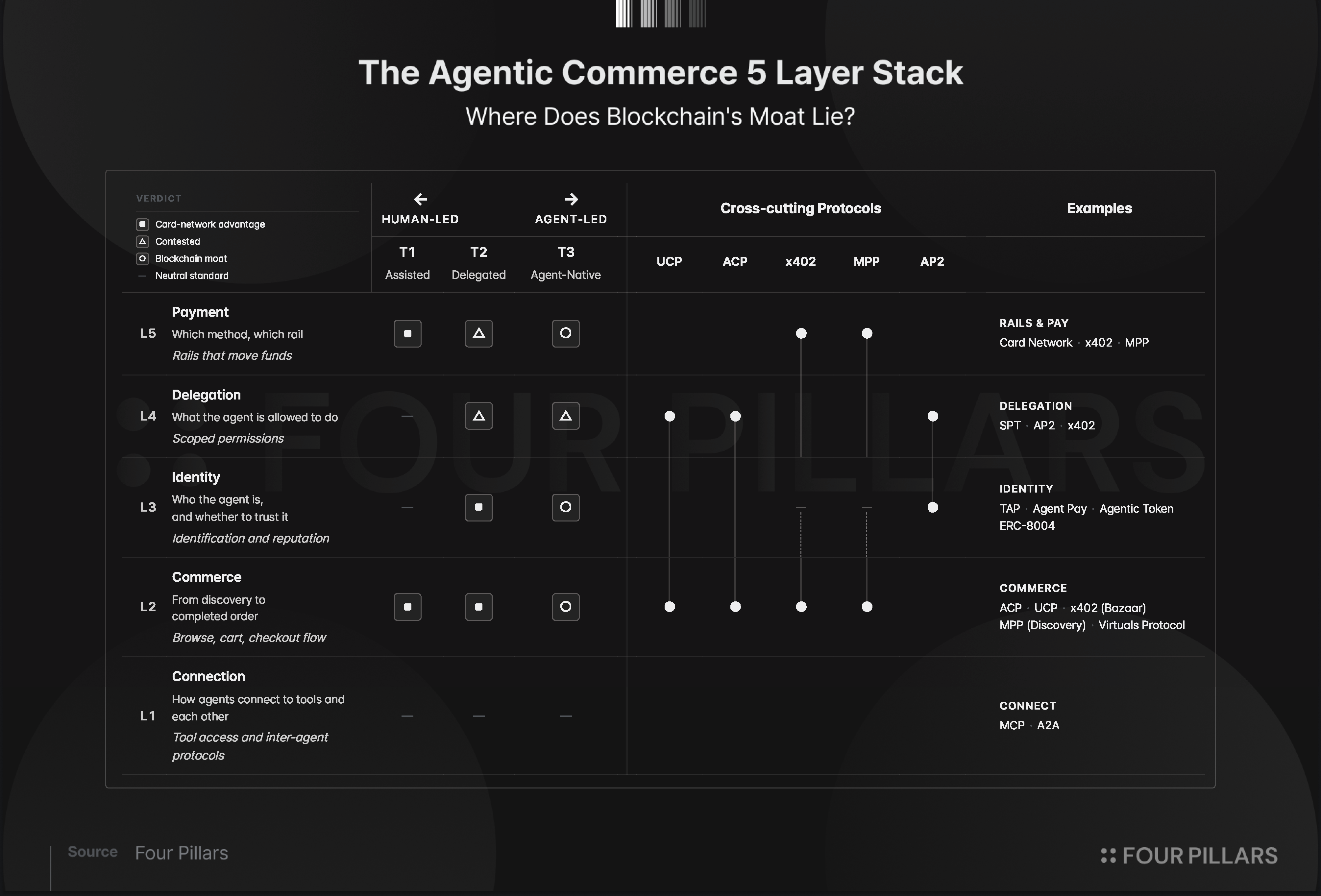

This article divides the flow of agent-driven commerce into five layers by the functional stages an agent passes through to finish a transaction: connection (L1), commerce (L2), identity (L3), delegation (L4), and payment (L5). T1 through T3 refer to the agent's Level of Delegation; L1 through L5 make up the Functional Stack that makes that delegation work.

On this basis, each layer is analyzed in three parts: (1) function and structure, (2) key player trends, and (3) implications. The implications section crosses each layer with the T1 to T3 axis and asks where blockchain can pull ahead of legacy card networks and hold a structural moat.

Many of the leading protocols in agentic commerce are not confined to a single layer; they work across several. ACP covers product discovery (L2) through delegation (L4), and x402 covers commerce (L2), delegation (L4), and payment (L5) in one protocol. This chapter still decomposes the framework by function because moat boundaries that blur at the protocol level become visible once the layers are separated.

2.1 L1 connection layer: Connectivity standards are converging

2.1.1 Function and structure

L1 is the channel through which an agent reaches external tools and other agents. In the past, each service was wired in individually with REST APIs. As the agent era arrived, work on a common specification picked up. The field settled on open-source standards rather than a single payment network's stack. Two protocols now carry most of the weight in agentic commerce.

- MCP (Model Context Protocol): Released by Anthropic in November 2024. Major Big Tech firms adopted it one after another, making it the de facto industry standard. It unifies the way an agent calls and runs tools, including external payment modules.

- A2A (Agent-to-Agent): Released by Google in April 2025 and currently managed by the Linux Foundation. It handles transactional interactions between agents, including unit-price negotiation and contract-terms coordination.

2.1.2 Key player trends

MCP has settled in as the de facto standard across Big Tech since Anthropic released it. On top of it, Stripe, PayPal, Circle, Coinbase, KakaoPay, Ant, and other major payment providers have entered a race to expose their payment functions as MCP servers agents can call. A2A is early, but it should become the core specification for complex economic agreements between buying and selling agents.

2.1.3 Implications: connectivity is the core of agentic commerce

L1 is not a layer where card networks and blockchain compete head-on. Both standards are payment-network-neutral, and neither camp has room to build a distinct moat here. The existence of MCP did, however, bring the effective spread of blockchain payments forward.

Take x402, covered later. The HTTP 402-based protocol was mostly used for one-off transactions such as token launches. Once combined with MCP, it moved past single-shot payment experiments and opened a path where an agent discovers paid API endpoints and calls them.

L1 is a neutral standard, but it supplies the connection point the upper layers need to grow. Traditional payment providers moved fast on MCP. The blockchain camp should drop the internal camp disputes and focus on securing connectivity with agents.

2.2 L2 commerce layer: The agent commerce execution tier

2.2.1 Function and structure

L2 is where the agent explores and compares what to buy, then moves through cart and order. Unlike L1, the competitive structure at L2 splits in two for the first time. An Opt-in axis that sits on top of existing e-commerce and card infrastructure, and a Permissionless axis based on blockchain, are developing in parallel.

2.2.2 Key player trends

- ACP (Agentic Commerce Protocol): Developed by OpenAI and Stripe, ACP standardizes how order and payment information moves among agent, user, and merchant so that a user can finish a purchase inside an AI interface. Its focus is the checkout and purchase-completion flow, not product discovery.

- UCP (Universal Commerce Protocol): An open-source commerce standard co-developed with Google, Shopify, Walmart, and others. UCP covers the full shopping process, from discovery through purchase to post-purchase support. It has backing from payment and commerce partners including Visa, Mastercard, and Stripe, and is designed to work with A2A, AP2, and MCP.

- x402 Bazaar, MPP Discovery: Service-discovery layers built into the blockchain-based x402 and MPP payment protocols. In each case, an agent queries endpoints that were deployed to spec, without a separate vetting step, finds them, and goes straight to payment. This is a permissionless structure.

- Virtuals Protocol: An agent launchpad on the Base chain. Users create an agent and tokenize its ownership and revenue rights through an IAO (Initial Agent Offering).

2.2.3 Implications: the permissionless structure is where blockchain's moat sits

At the T1 to T2 stages, the existing opt-in model, which has secured a familiar payment experience and a network of 150 million merchants, holds an overwhelming advantage. There are also non-opt-in approaches like Rye that aggregate existing commerce data and intermediate purchases without merchant onboarding, but the underlying assumption that the seller is registered as a merchant somewhere does not change. Once the field moves into T3 autonomous transactions, with constant interaction between agents and unknown suppliers, the seller-approval-based Opt-in approach hits clear limits. The T3 long tail is filled with suppliers, including headless endpoints, one-person firms, and autonomous agents, that have no legal entity capable of passing merchant vetting. For them, an Opt-in structure that depends on seller approval does not even allow entry.

In a permissionless protocol, where a wallet alone is enough to transact, these suppliers join the ecosystem right away. x402 Bazaar and MPP Discovery embed a discovery layer inside the payment protocol. Virtuals Protocol runs a separate commerce protocol. None of them has a merchant-approval gatekeeper. That is why blockchain secures a moat in areas the Opt-in structure cannot reach. Whether that moat turns into real competitive ground in T3 depends on the trust layer that sits on top, discussed below as L3.

2.3 L3 identity layer: Verifying the agent's identity

2.3.1 Function and structure

L3 verifies an agent's identity and trustworthiness. As agents multiply, telling legitimate agents that act for real customers apart from malicious bots has become a core challenge. An identity layer is required in permissionless environments without prior vetting. L3 is developing along two tracks: centralized identity systems led by card networks, and decentralized identity systems built on on-chain registries.

2.3.2 Key player trends

- TAP (Trusted Agent Protocol): An open framework co-developed by Visa and Cloudflare. An agent proves identity with a digital signature, and the merchant verifies it with Visa's public key. Verification runs in real time on every request, without prior vetting.

- Agent Pay / Agentic Token: An agentic payment framework Mastercard released in April 2025. At the center sits the Agentic Token, a Verifiable Credential (VC) designed so that an agent's transaction requests can be tracked against predefined rules and permissions. The agent transacts without exposing raw card data, and the user sets the agent's authority scope granularly, for example up to a certain amount per week for grocery orders. Agent identification, the scope of user authorization, and transaction traceability are integrated on a tokenization base.

- ERC-8004: A blockchain-based identity standard built from three parts (identity, reputation, and verification) organized in an on-chain registry. The agent's task success rate, uptime, and user feedback are recorded in a tamper-proof form. Follow-on layers are building on top of it, including the escrow-based ERC-8183.

2.3.3 Implications: the scalability ceiling, and why "trust" matters

How much the identity layer matters depends on the level of autonomy. At T1, the final transacting party is a human, so verifying the agent's identity separately offers little practical benefit. T2 also runs well on the central verification models led by Visa and Mastercard, thanks to an Opt-in market structure and a controllable agent population. T3 is the problem. Here hundreds of millions of autonomous agents form a long tail. Whether one uses the VC-issuance-based Agent Pay or the public-key-based TAP, defining identity inside the card network's jurisdiction runs into scalability limits and cannot absorb the agents that appear freely in permissionless environments. This is where on-chain registries such as ERC-8004 have a strong moat.

On-chain registries alone do not solve everything. Identity, reputation, and verification records are grounds for judgment, not binding instruments, and permissionless environments always leave room to game them. That is why escrow-based standards such as ERC-8183 are following. These standards are still drafts, so they are closer to an early blueprint than production infrastructure. Whoever lays the right control mechanisms on top and finds the balance between freedom and control will hold the largest moat of the next generation of agentic commerce.

2.4 L4 delegation layer: Setting the boundary of an agent's authority

2.4.1 Function and structure

L4 defines, in advance, how far an agent can go in paying on a user's behalf. Handing an agent a whole card or wallet is risky, so the structure passes on authority only within limits on amount, merchant, industry, time of day, validity period, and so on. Card-network-based approaches break authority down through virtual cards or one-time tokens. Blockchain-based approaches bound authority on-chain through pre-signatures. AP2 splits payment execution and user consent, and standardizes the consent portion separately as a Mandate.

2.4.2 Key player trends

- SPT (Shared Payment Token): A delegated-payment token Stripe built on its own payment infrastructure along the lines of ACP's delegated-payment specification. Issued as single-use, amount-limited, time-limited, it hands the merchant payment authority rather than card information.

- AP2 (Agent Payments Protocol): Led by Google, AP2 signs the user's intent, cart confirmation, and payment execution cryptographically, each as its own Mandate, and links them in a chain. It leaves an auditable record of what was permitted and which transaction actually ran.

- x402: x402 combines HTTP 402 with ERC-3009 (a pre-signature-based payment authorization spec) so that an agent proves authority for every request with a wallet signature. Without accounts or sessions, the smallest unit of authority maps to a single HTTP request.

2.4.3 Implications: no standalone moat, but a layer nothing works without

Delegation is an abstraction problem at heart: to whom, under what conditions, and up to what amount should authority pass? Because it sits on a level separate from the payment rail, the card camp and the blockchain camp are solving the same problem with different tools. Neither side holds a standalone moat here. L4 is still the ground on which L5 below stands. The scope of authority has to be clearly defined in advance, or ultra-small-amount payments cannot be repeated without abuse, and ex-post verification cannot assign liability to anyone specific.

2.5 L5 payment layer: The money-movement rail of the agent economy

2.5.1 Function and structure

L5 turns delegated authority into real money movement. Card rails assume prior registration of merchants and issuers and settle funds on a T+1 to T+3 cycle after multi-step approvals. Blockchain rails settle right away with just a wallet signature and a smart contract on stablecoins such as USDC. Per-transaction payments settle immediately, without prior registration or session maintenance. The two rails differ at the structural level.

2.5.2 Key player trends

- Card networks: Visa and Mastercard's existing merchant networks are the rails. Agent-oriented payment interfaces such as Visa's VIC (Visa Intelligent Commerce) and Mastercard's Agent Pay sit on top, adding tokenization and passkey authentication.

- x402: When an HTTP 402 response triggers payment, a smart contract automatically checks the signature and settles immediately on a stablecoin such as USDC. Per-transaction payments go through without accounts or API keys. Thousands of micro-settlements per second are possible at fees below USD 0.001 per transaction.

- MPP: An HTTP 402-based M2M payment protocol Stripe released in March 2026. It splits the settlement path by payment method. Fiat payments such as cards and BNPL settle over Stripe's payment network. Stablecoin payments settle directly on the Tempo blockchain. A batch structure that bundles thousands of small transactions into a single settlement transaction makes it a good fit for repeat-call agent traffic.

2.5.3 Implications: division of labor, not replacement

At L5, cards and blockchain are not fighting over the same market. Rail choice splits by the nature of the transacting party, not by amount. Spending that ends in a human approval fits cards, which have merchant infrastructure and consumer protection in place. API calls and repeated M2M transactions that agents run on their own fit blockchain, where per-transaction payments go through without accounts and settle 24 hours a day at sub-cent fees.

For that reason, T2, the middle ground between humans and agents, sees both rails coexist depending on the user's delegation conditions. T3, where agent autonomy is at its highest, is where blockchain holds a standalone moat.

3. Opportunities in the Korean Market: Expansion of Super Apps and The K-layer

3.1 Agentic commerce is the breakthrough that solves the KRW stablecoin's use-case problem

The heat has cooled a little recently, but the biggest topic in finance and blockchain is still the race for Korean won stablecoin leadership. Banks, Big Tech, and fintechs are each forming consortia, and a four-way field is setting in, but one fundamental question is still open. Where will it be used? In Korea, where payment infrastructure such as credit cards and simple payments is already world-class, simple remittance or B2B settlement does not give a KRW stablecoin enough of a case.

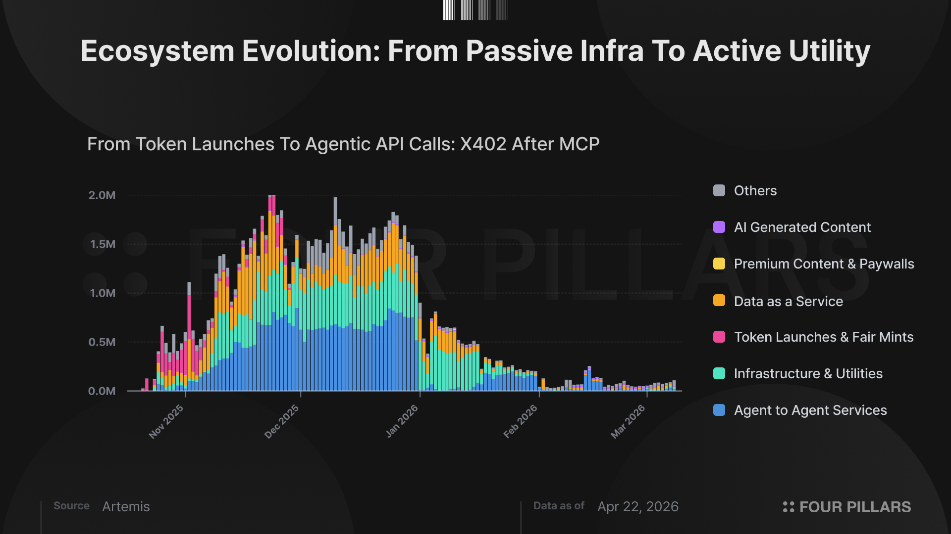

The answer shows up in stablecoin payment rails for agentic commerce. The numbers from x402, a leading example of such a rail, make the case concrete.

- Cumulative real-use transactions: about 109.5 million (from launch in May 2025 through April 2026).

- Daily real-use payments: about 60,000 on average over the past month, with a peak above 2 million.

- Fee structure: below USD 0.001 per transaction, enabling ultra-low-cost micro-transactions.

Applied to agentic commerce, and especially to agent-native commerce (T3) on headless merchant endpoints, this advantage produces changes traditional financial networks cannot match.

First, a large cut in fees. The 1.8 to 2.5% card fee that merchants have borne compresses to around USD 0.001 per transaction.

Second, a new market. Most of the roughly 100 million cumulative payments happened in a micropayment structure and could not have existed under existing card fee economics in the first place.

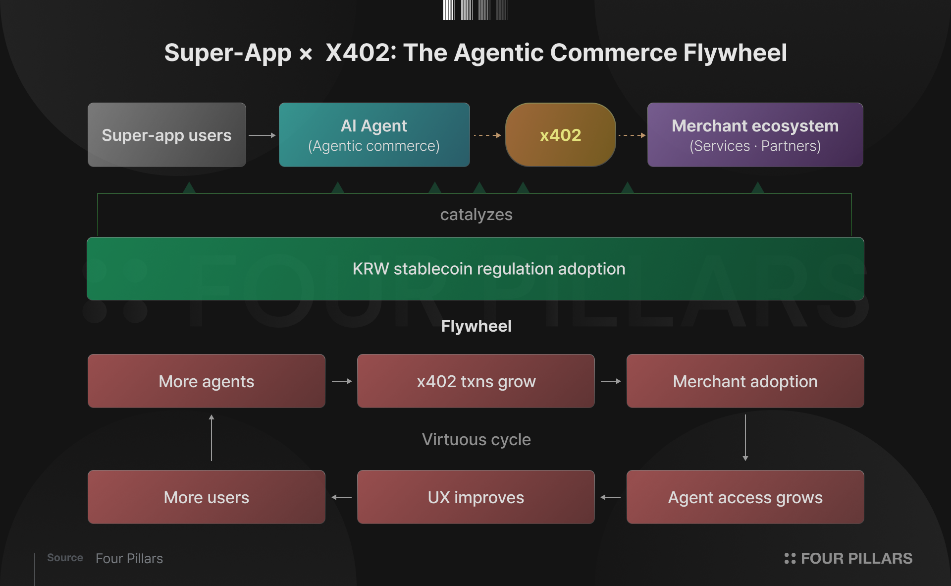

A flywheel comes on top. More agents mean more x402 payments. As payment volume piles up, merchant adoption of x402 expands. The more services open to agents, the better the user experience. Better experience pulls still more users toward agents.

Stablecoin payment rails both prove micropayments as a new market and open up T3-centric agent commerce. This asymmetry and the virtuous cycle it creates are the clearest use case for a KRW stablecoin. KakaoPay's recent move to join the x402 Foundation reads as a preemptive bet on this structure.

Any consortium that can build agentic commerce should design agent-native payment rails and merchant endpoints early, and use them as grounds for KRW stablecoin adoption. If these consortia skip the area where stablecoins are structurally suited and stay absorbed only in the leadership race, the case for adoption itself gets harder to make.

3.2 If the super-app has payment and commerce layers ready, go after agentic commerce

A technology lead does not guarantee an early move. The U.S. leads on LLM performance, but agent penetration into commerce has gone further in China. Alibaba's Qwen ran a bubble-tea campaign in February where discovery through Alipay payment happened inside a single chat window, in a T1 agentic commerce pattern. On the back of it, monthly active users went from 20 million in November 2025 to 200 million in February 2026. In the U.S., ACP and UCP are still at pilot-adoption stage.

The gap comes from service-ecosystem fragmentation. In the U.S., even Alphabet and Meta have their services split up, so every connection point between layers piles up friction in authentication, API specs, payment methods, and trust between operators. WeChat and Alipay, by contrast, have payment, reservations, public administration, and delivery inside a super-app, so the connection cost never appears. From the agent's side, the specs and trust systems that would otherwise need to be relearned at every layer boundary are gone.

The authentication, payment, and merchant relationships a super-app has embedded inside its own ecosystem sit directly on the agent's path. That is where the moat comes from. A delegated agent calls those relationships inside the super-app. A permissionless autonomous agent calls them through the merchant network the super-app exposes to an open protocol. Either way, payment and fulfillment pass through the super-app's infrastructure. While competitors are still stitching fragmented services together, the super-app can commercialize through its internal connections right away.

How one defines a super-app changes the list, but any super-app that owns the commerce layer (L2) and the payment layer (L5) has a clear moat in agentic commerce. In Korea, Kakao, Naver, and Toss are the obvious cases. Existing commerce apps with their own payment methods and commerce channels belong in the same pool. On this basis, building out agentic commerce is worth serious review.

Step by step, T1 starts with turning the existing human payment flow into something agents can call and building dedicated UI/UX around it. T2 raises agent autonomy one step, so the design has to decide how far the scope of delegated authority and the methods of payment authentication should go. T3, following KakaoPay's path, means exposing your infrastructure as a supplier to open protocols through a connection layer (L1) such as MCP, and mapping out how to combine with external standards.

The Electronic Financial Transactions Act assumes the user's own direct transaction instructions, and the security steps built up to block automation (CAPTCHA, two-step authentication, and so on) translate straight into friction on agent payments. Add user adaptation to agent payments, and the most reasonable path in Korea is to climb from T1 upward, where regulation is lighter.

3.3 If the layers are not there, build a K-layer

Super-apps hold the moat, but that does not close off the other players. On the assumption that the legal and systems bottlenecks described above are resolved, three directions open up in areas super-apps have not yet filled.

The first is the identity layer (L3). A bridge is needed that takes the identification, authorization, and trust standards forming at this layer globally and fits them cleanly onto Korea's Electronic Financial Transactions Act and the Act on Reporting and Use of Specified Financial Transaction Information. Bending them too much to Korean law cuts them off from global protocols, so foreign agents cannot reach domestic merchant networks. Bringing global standards in as-is clashes with the domestic supervisory system. Building the middle layer between the two is itself a moat in the Korean market.

The second is a Korean-style commerce layer (L2). Asking small and medium commerce, reservation, and content operators to open agent-compatible endpoints individually is a high bar. A single platform that pulls them together and offers standardized product information, payment, and fulfillment interfaces lowers the connection cost and brings demand in. Full openness makes reliability hard to secure; a prior-approval system limits accessibility and scale. Starting from a middle design that keeps registration and calls open to anyone but backs trust with risk-based tiered authentication, and then widening openness as the ecosystem matures, is the sensible path. That is the shape a merchant network needs to have for foreign agents, not only domestic ones, to call it.

The third is an individual service-provider question. Commerce operators, brands, and merchants can either join the first two layers as suppliers or plug into an existing super-app ecosystem. In practice Korea is a super-app country, so the latter tends to win in the short term on reach and conversion. The deeper the dependence, the more customer data and brand assets flow to the super-app, so designing dual channels that also open onto the commerce layer or the open protocol side deserves consideration.

The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.

![50% for Ethereum, 50% for Congress [FP Weekly 33]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2F1cg9d7msn1d3j2.png&w=1920&q=75)

![Coldcard Got Burned, Coinbase Froze [FP Weekly 32]](/_next/image?url=https%3A%2F%2Fkrotgrfjzckvumudxopj.supabase.co%2Fstorage%2Fv1%2Fobject%2Fpublic%2Fassets%2Fimg%2Fcontent%2Farticle%2Fnotion-import%2Fhv83s5msebytml.png&w=1920&q=75)