Table of Contents

- Key Takeaways

- 1. The Shift in AI Infrastructure Bottlenecks and the Rerating of Korea's Big 2

- 2. The IBKR Channel: Trading Infrastructure Is Catching Up, Halfway

- 3. Samsung Is a Global Megacap, but Trades at the Capital Efficiency of a Junk Asset

- 4. The Capital Inefficiency QFEX's Liquidity Market Solves

- 5. The Gap Between Asset Globalization and Trading Infrastructure Globalization

Researcher

Related Projects

Key Takeaways

- AI infrastructure bottlenecks have shifted from GPUs to memory, and Korea's Big 2 are being repriced as global assets. Samsung Electronics crossed $1 trillion in market cap, overtaking Berkshire Hathaway, while SK Hynix posted a Q1 2026 operating margin of 72%, ahead of Nvidia (65%), TSMC (58%), and Samsung (43%). The two companies, controlling more than 80% of the global HBM market, have begun to anchor pricing power in the AI cycle.

- Foreign capital is flowing in at a steep pace. Across just two trading sessions on May 4 and 6, foreign net buying on KOSPI exceeded KRW 6 trillion, and foreign ownership of KOSPI rose to 38.9%, a six-year high. With Korea's FSC laying the groundwork for an integrated foreign investor account framework, foreign investors are also gaining direct access to Korean equities through global brokerage channels for the first time.

- Inside IBKR, however, Korea's Big 2 do not receive the capital efficiency their global megacap status warrants. Official policy excludes Asian equities from Portfolio Margin; only rules-based (Reg T) margin applies. While US megacaps like Apple and Nvidia get portfolio-level hedge offsets, Samsung is treated as a far heavier collateral burden under foreign-equity rules. Even on the same AI supply chain pair trade, the capital efficiency gap between US-listed names and Korea's Big 2 widens substantially.

- Equity perpetual futures narrow this gap without requiring any change to incumbent infrastructure. They settle on index prices alone, bypassing issuer-country clearing systems, and bring foreign and US tickers into the same collateral framework through USDC settlement and 24-hour trading.

- QFEX allows traders to access AI infrastructure names like NVDA, AVGO, and CRWV alongside Korean assets like Samsung Electronics, SK Hynix, and EWY on a single collateral rail, with up to 10× leverage. The further AI trades move from index leaders down into the deeper infrastructure layer, the more clearly traditional brokerages reveal their constraints (ticker coverage, trading hours, foreign-equity margin penalties), and the stronger the structural case for QFEX's perpetual futures rail.

1. The Shift in AI Infrastructure Bottlenecks and the Rerating of Korea's Big 2

On May 6, 2026, KOSPI closed at 7,384.56, setting a new all-time high. The index has run +24% over just 13 trading sessions, +47% YTD. Over the same period, KOSPI has outpaced both the S&P 500 and the Nasdaq, and MSCI Korea has climbed to the #1 spot in APAC by USD-based returns. On the same day, Korea's market cap overtook the United Kingdom's to become the world's 8th largest.

At the center of the rally are Samsung Electronics and SK Hynix. Samsung surged +12% in a single session on May 6, crossing $1 trillion in market cap for the first time. It overtook Berkshire Hathaway to become the 12th most valuable company in the world, and the second Asian company in the trillion-dollar club after TSMC. The same day, SK Hynix crossed KRW 1,000 trillion in market cap. Combined, the two companies now account for 42.2% of the entire KOSPI, the highest concentration ever recorded.

The rerating is backed by fundamentals. SK Hynix posted Q1 2026 operating profit of about $27 billion at a 72% operating margin. In the same quarter, this margin came in above Nvidia (65%), TSMC (58%), and Samsung (43%). Across the entire S&P 500, the number of companies with operating margins above 70% can be counted on one hand. The company's CFO confirmed that 2026 HBM supply was fully sold out, and that demand visibility now extends three years beyond current capacity.

Samsung is in the same rerating zone. The company began HBM4 mass production in February 2026, formally entering the next-generation AI memory supply race, and Q1 2026 memory operating profit expanded to about $36 billion, nearly 5x the $7 billion-range a year earlier. Surpassing Alphabet to enter the global top 5 by quarterly operating profit signals that Samsung can no longer be priced strictly as a traditional memory-cycle business.

The mechanism behind this is a shift in AI infrastructure bottlenecks. The constraint in AI compute infrastructure has moved from GPUs to memory, and the two companies that control more than 80% of the global HBM market have begun to hold pricing power over that bottleneck. Nvidia allocating two-thirds of its HBM4 demand to SK Hynix, and OpenAI committing to 900,000 DRAM wafers per month from the two firms, are representative examples of this shift. The result: AI cycle capital flows have expanded from Silicon Valley into the Korean memory supply chain.

2. The IBKR Channel: Trading Infrastructure Is Catching Up, Halfway

Foreign capital has already priced this in. Foreign net buying on KOSPI hit KRW 3.02 trillion on May 4 and KRW 3.13 trillion on May 6, more than KRW 6 trillion across two sessions, with Korea's Big 2 absorbing the bulk of it. May 6 marked the second-largest single-day net buy in market history, and foreign ownership of KOSPI rose to 38.9%, a six-year high. YTD growth in foreign-held market cap (+86.7%) outpaced KOSPI itself (+75.2%), suggesting foreign capital was not buying the broader Korean market but concentrating disproportionately in the names leading the rally: Samsung and SK Hynix.

As capital intent crystallized, market access channels began to move. In January 2026, Korea's Financial Services Commission (FSC) authorized IBKR, Emperor Securities, TFI, and BancTrust to open Korean securities accounts. The structure is omnibus: foreign brokers establish omnibus arrangements with Korean securities firms, processing foreign retail orders within that wrapper. With this authorization, foreign investors gained the ability to trade Korean equities directly through global brokerages like IBKR.

The implications are not minor. Until then, foreign investors had to register an Investment Registration Certificate (IRC) with a Korean securities firm and open a separate KRW account. Language, currency, and settlement infrastructure were all entry barriers. The omnibus account materially reduces these frictions. IBKR supports KRW as a base currency, allowing simultaneous trading of KOSPI and US equities on a single platform.

This is the first stage of access normalization for Korean equities. The next stages are 24-hour foreign access to KRW FX, scheduled for July 2026, and entry into the MSCI Developed Market watchlist in 2027. UBS estimates about $24 billion in foreign capital inflow upon MSCI DM inclusion, and the omnibus channel functions as an early rail accelerating that flow.

But omnibus access does not yet mean foreign investors can trade Korea's Big 2 on the same terms as the Mag7. The real gap lies in capital efficiency.

3. Samsung Is a Global Megacap, but Trades at the Capital Efficiency of a Junk Asset

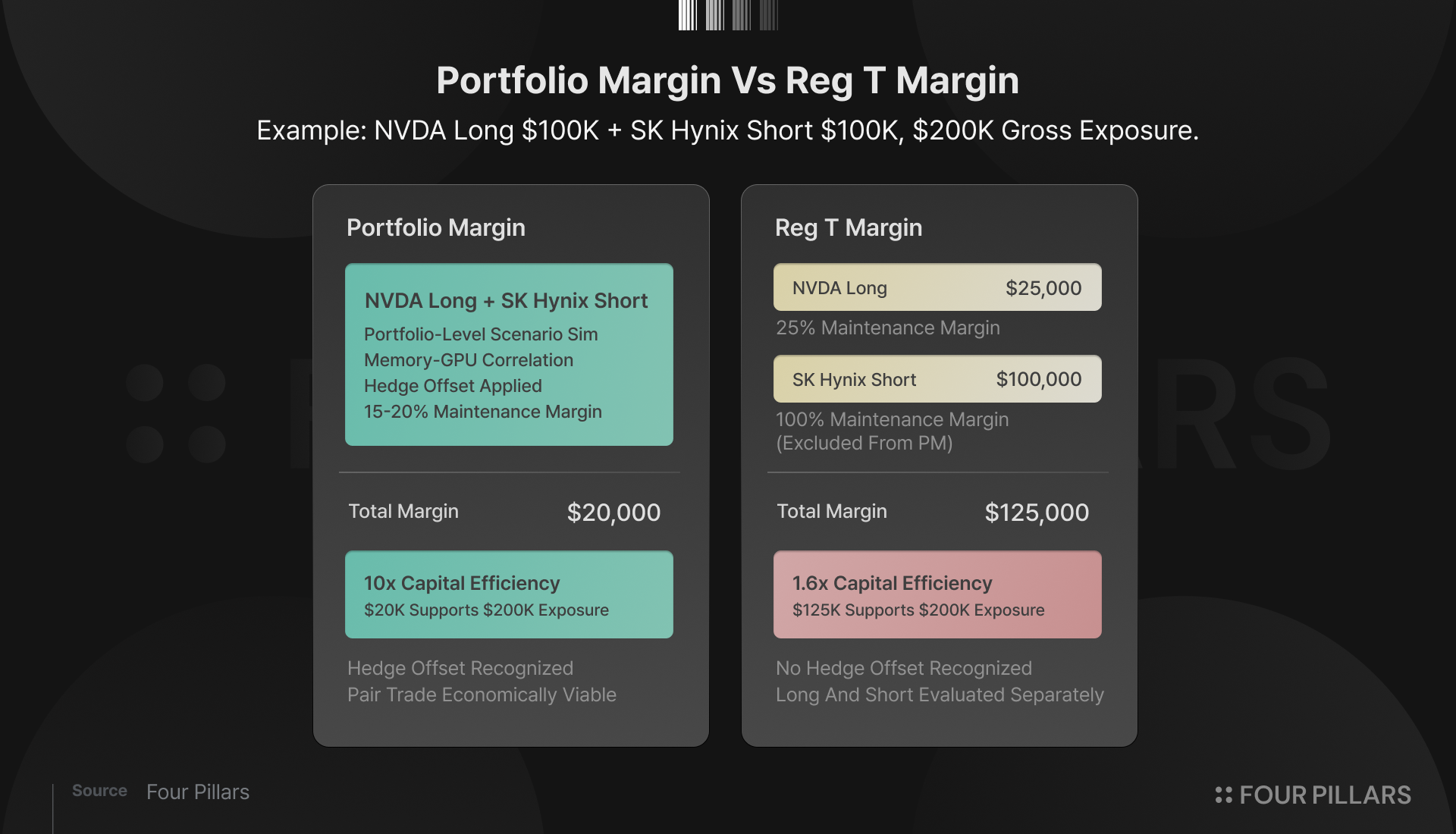

IBKR's official policy documents explicitly state that Canadian, European, and Asian equities are not eligible for Portfolio Margin (PM) and are processed under standard rules-based (Reg T) margin only. In other words, Korean equities sit outside IBKR's advanced margin system entirely.

Unpacking what this means: Portfolio Margin is IBKR's advanced margin system for active traders and hedge funds. It runs thousands of scenario simulations daily on each portfolio, recognizes hedge offsets, and compresses maintenance margin to about 15–20% per position. Compared with Reg T, which imposes 50% initial margin (FINRA standard) and 25% maintenance margin (FINRA floor) per ticker independently, capital efficiency differs substantially. PM is essentially required tooling for pair trades, options hedges, and multi-asset strategies.

US tickers live inside this system. Stable megacaps like Apple typically trade at maintenance margin around 15%. Nvidia and Tesla sit in the same structure. Required margins vary with volatility and portfolio composition, but US large caps are fundamentally part of portfolio-level risk computation.

Samsung, on the other hand, is a $1 trillion asset ranked 12th in the world, yet ineligible for IBKR Portfolio Margin. The moment it falls under rules-based margin, hedge offsets across the portfolio are not recognized, and IBKR's own house margin penalty for foreign equities is added on top. As a result, even an asset of equivalent economic scale to a US megacap trades at substantially lower capital efficiency inside an IBKR account.

For investors, this difference translates directly into deployable leverage. The same AI supply chain pair trade, long NVDA and short SK Hynix, gets split inside IBKR: the Nvidia leg is calculated as portfolio risk, while the SK Hynix leg is segregated under foreign-equity rules. With identical investment logic and identical capital, leverage and hedging work for the US-listed name; for Korea's Big 2, far more cash gets locked up.

This is a product of trading infrastructure limits. IBKR does not absorb settlement risk, currency risk, and local custody risk for foreign equities outside US clearing house (NSCC, DTCC) protection into its Portfolio Margin engine the way it does for US equities. Prime brokers like Goldman Sachs and Morgan Stanley, by contrast, bundle local settlement, custody, securities lending, and FX hedging to provide more flexible margin structures for large hedge funds. The gap, ultimately, sits not in the asset itself but in the access rail.

4. The Capital Inefficiency QFEX's Liquidity Market Solves

This capital efficiency gap will not close inside the existing infrastructure on its own. Two paths exist. First, Korea joins MSCI Developed Markets and IBKR expands its foreign-equity Portfolio Margin coverage. Second, an alternative market structure that bypasses physical equity settlement infrastructure emerges. The first path is bound to government and institutional timelines, earliest 2027, realistically 2028 or later. The second path is already operating, in the form of equity perpetual futures (Equity Perp).

Equity perps are derivatives that settle on index prices alone, without issuer cooperation. Because they do not hold underlying stock, dependency on the issuer-country clearing system drops sharply, and there is no longer a structural reason to treat foreign and US tickers differently in the margin system. USDC settlement reduces KRW conversion friction. 24/7 trading also matters: price discovery continues even while Korean exchanges are closed.

QFEX has listed more than 17 equity perps, providing exposure to the AI supply chain and Korean equities at up to 10× leverage.

AI infrastructure tickers like NVDA, AVGO, and CRWV trade alongside Korean assets like Samsung Electronics, SK Hynix, and EWY on the same USDC-collateralized 24-hour perpetual futures rail. Assets that traditional brokerages process under different trading hours, currencies, and margin rules now sit inside a single market structure.

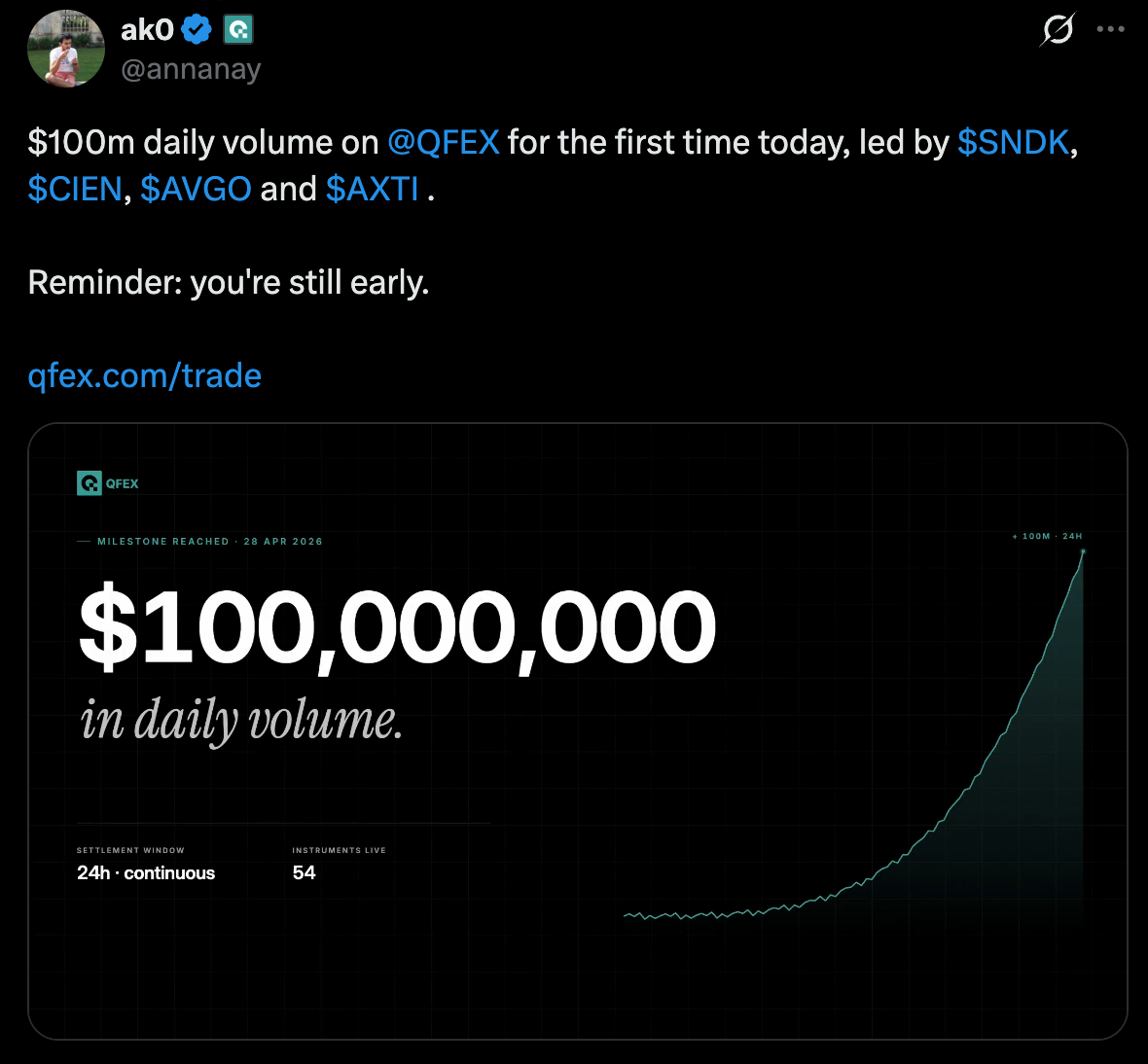

Source: X(@annanay)

What matters about QFEX crossing $100 million in daily volume on April 29 is not the size but the composition. The four tickers driving that volume were not NVDA or TSLA but SNDK, CIEN, AVGO, and AXTI. The common thread: not megacap AI software or GPUs, but the deeper infrastructure layers of AI data centers.

As AI trading moves from index leaders down into the deeper infrastructure layer, the constraints of traditional brokerages, ticker coverage and trading hours, become more visible. QFEX's perpetual futures structure is showing strength precisely in bringing this long tail of AI infrastructure names into a single 24-hour, single-collateral framework.

This market is not yet complete. Liquidity and price discovery face constraints during off-hours, and slippage on large orders is meaningful. Even so, among equity perpetual futures venues currently in operation, QFEX has positioned itself as the most meaningful liquidity hub for Korean equity trading. Other venues are also expanding their listings beyond crypto assets and US big tech, but for perpetual futures on non-US tech assets including Korea's Big 2, QFEX shows comparatively deeper order books, higher volumes, and broader ticker coverage.

5. The Gap Between Asset Globalization and Trading Infrastructure Globalization

The globalization of an asset is complete only when two things happen at once. First, the value of the asset becomes global. Second, the channels to trade it become global. Korea's Big 2 have completed the first half. A $1 trillion market cap, a 72% operating margin, pricing power over the AI cycle: markets have already begun to converge on this view.

The second half is only just starting. Omnibus accounts are open. The 24-hour FX market arrives in July. The MSCI Developed Markets roadmap targets 2027–2028. But the settlement infrastructure overhauls IBKR would need to normalize foreign-equity Portfolio Margin, and the work required for Korean equities to form liquidity aligned with US investor trading hours, are all bound to the timelines of governments and financial institutions.

Market cycles do not wait for those timelines. As a result, equity perpetual futures are asymmetrically narrowing the asset access gap ahead of regulated infrastructure, and QFEX is establishing itself as the deepest liquidity market in that void.

The report is based on the independent research of the author sponsored/funded by QFEX. The author of this report may have personal holdings or financial interests in assets or tokens discussed herein. However, the author affirms that no transactions have conducted using material non-public information obtained in the course of research or drafting. This report is intended solely for general information purposes and does not constitute legal, business, investment, or tax advice. It should not be used as a basis for making any investment decisions or as guidance for accounting, legal, or tax matters. Any references to specific assets or securities are made for informational purposes only and should not be construed as an offer, solicitation, or recommendation to invest. The opinions expressed herein are those of the author and may not reflect the views of any affiliated institutions, organizations, or individuals. The opinions and analyses expressed herein are subject to change without prior notice. In addition, beyond the individual disclosures included in each report, Four Pillars, may hold existing or prospective investments in some of the assets or protocols discussed herein. Furthermore, FP Validated, a division of Four Pillars, may already be operating as a node in certain networks or protocols discussed herein or may do so in the future. Please see below links in the footer for FP Validated's participating network disclosures and for broader disclosure details.